Novartis Bets on Radioligand and RNA Therapies Instead of ADCs Amid Strategic Refocus

Novartis

Drug Development and Manufacturing

From 2018 to 2023, Novartis gradually evolved into a pure innovative pharmaceutical company: exiting the consumer health and medical device sectors, spinning off Alcon, selling its stake in Roche, transferring commercialization rights of certain ophthalmology products to Bausch + Lomb, and spinning off its generics business, Sandoz, in October last year.

Recently, Novartis released its first report card after the spin-off of Sandoz: full-year revenue for 2023 reached $45.44 billion, a year-on-year increase of 10%; net profit was $8.572 billion, a year-on-year increase of 62%.

As a pharmaceutical company that has consistently ranked in the global top 10 by market value for many years, Novartis has yet to have a single product that generates billions of dollars in revenue. However, Novartis's investments and outputs in CGT, small nucleic acid drugs, and nuclear medicine can be regarded as industry-leading.

Previously, Novartis stated its key focus areas were targeted protein degradation, cell therapy, gene therapy, radiation therapy, and xRNA technology platforms. In terms of disease areas, Novartis’ latest announced priorities are cardiovascular-renal-metabolic, immunology, neuroscience, and oncology. The company’s strategic layout is clearly reflected in its acquisitions or licensing activities during 2022 to 2023. Recent high-profile news includes the full acquisition of SinReno Pharma to obtain IgA nephropathy assets, as well as the acquisition of Bo Wang's siRNA cardiovascular assets.

Source: Novartis Investor Presentation

Notably, although Novartis, facing a patent cliff, has begun a global buying spree, its CEO clearly stated at the JPM conference in January this year that the company has no intention of acquiring ADC assets amid the ADC acquisition frenzy.

Novartis CEO Narasimhan stated: "We have a long history in ADC research, but we haven't been successful... To be clear, part of our strategic focus is to identify areas where we believe we can build long-term sustainable leadership, and we are investing in radioligand therapy."

"We believe that when the right target is found, the therapeutic index of radioligand therapy will provide a fairly wide window for achieving therapeutic effects without some safety issues."

The safety issues of ADCs are highly complex, and many ADC technology platforms are working to reduce toxicity while improving efficacy. Different ADCs exhibit varying toxicity profiles. For example, DS-8201 has a relatively high incidence of pulmonary toxicity, and recently, Daiichi Sankyo's TROP2 ADC Dato-DXd reported seven deaths due to interstitial lung disease in its Phase 3 clinical trial for non-small cell lung cancer. Novartis believes that this situation can be avoided in radioligand therapy and stated that as the supply of Novartis' radioligand therapy is no longer restricted, "Radioligand therapy is a better option, allowing the company to focus its capital more effectively rather than overextending itself in the search for ADC assets."

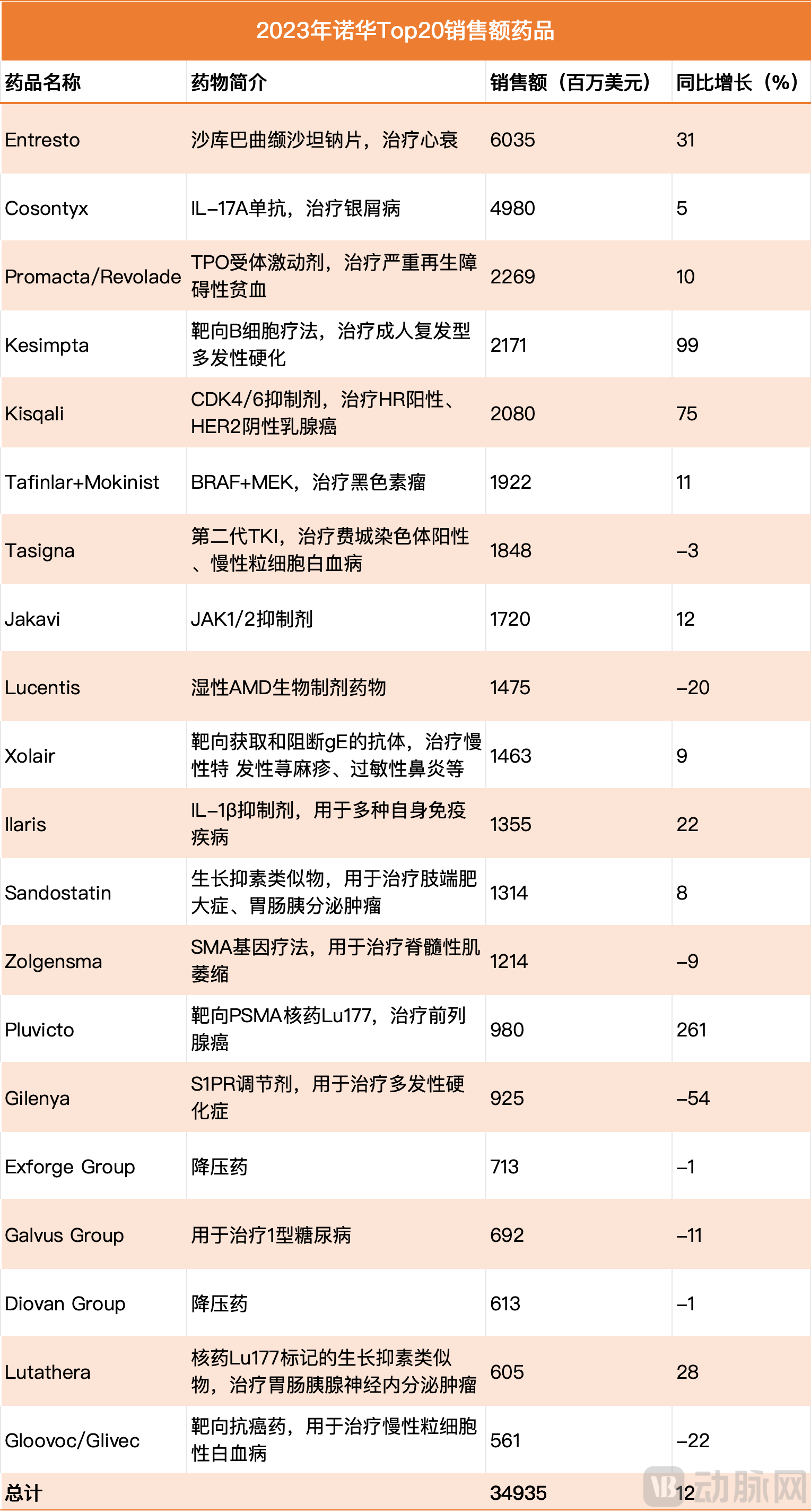

From Novartis' 2023 financial report, it is clear that Novartis has a solid reason for not purchasing ADC.In 2023, the fastest-growing drugs in sales for Novartis included: Entresto ($6.035 billion, Sacubitril/Valsartan Sodium, for heart failure, +31%), Kesimpta ($2.171 billion, Ocrelizumab, for adult relapsing multiple sclerosis, +99%), Kisqali ($2.080 billion, Ribociclib, for HR-positive, HER2-negative breast cancer, +75%), Pluvicto ($980 million, Lu177 radiopharmaceutical, for prostate cancer, +261%), Leqvio ($355 million, Inclisiran, the first siRNA drug targeting PCSK9 to lower lipids, +217%), and Scemblix ($413 million, the first STAMP allosteric inhibitor, for chronic myeloid leukemia, +179%).

Data source: Novartis 2023 annual report, compiled by VCBeat

$1 Billion Nuclear Medicine Pluvicto Is Just the Beginning

Novartis' rising star drug Pluvicto is the world's first PSMA-targeted radioligand therapy. It was approved for marketing by the FDA on March 23, 2022, for the treatment of patients with PSMA-positive metastatic castration-resistant prostate cancer (mCRPC). Just a year later, Pluvicto’s sales reached $980 million, on the verge of becoming a "blockbuster," further supporting CEO Narasimhan’s strategy of "not acquiring ADC assets."

Pluvicto consists of a combination of a targeting compound and the therapeutic radionuclide Lu-177, with a structure similar to ADC drugs. The mCRPC field has long lacked effective treatment options. Immunotherapy has been ineffective due to various factors such as a low tumor mutation burden and the "cold tumor" nature of mCRPC, preventing PD-1 inhibitors like Keytruda from making significant progress against mCRPC.

In the previous Phase 3 VISION clinical trial, the median overall survival for mCRPC patients treated with Pluvicto + standard therapy was 15.3 months, compared to 11.3 months in the control group, representing a 4-month extension in median overall survival.

Although the benefits are limited, Pluvicto has still received positive market feedback due to significant unmet needs. Last year, Eli Lilly purchased the radiopharmaceutical biotech company Point Pharma for a premium of $1.4 billion. Point Pharma's core pipeline, PNT2002, also focuses on the mCRPC indication, highlighting the potential in this field.

In October 2023, Novartis announced another set of positive Phase 3 data for Pluvicto: The PSMAfore trial met its primary endpoint of radiographic progression-free survival (rPFS), with an HR of 0.411. Compared to the control group, the median rPFS in the Pluvicto group more than doubled, reaching 12 months. Novartis will continue to collect OS data from the PSMAfore trial and expects to submit a new marketing application in 2024, which could potentially advance Pluvicto toward first-line treatment.

$1 billion is just the beginning for this radiopharmaceutical. Pluvicto faced supply constraints last year, which impacted product scaling. In January this year, Novartis announced that its new radiopharmaceutical production facility in Indianapolis received FDA approval to commercially manufacture Pluvicto. The Indianapolis facility is Novartis' second RLT production site approved in the U.S., which will increase RLT production capacity to 250,000 doses annually by 2024 and beyond. In December last year, Novartis established an RLT production base in Haiyan, Zhejiang, China, with operations expected to commence by the end of 2026 to supply Chinese patients.

Novartis will also continue to expand its network of treatment centers from the current approximately 300 institutions to around 500, in order to reach the expected peak sales of $3 billion for Pluvicto.

Novartis CEO Narasimhan also pointed out that Novartis is developing other actinium-based compounds, which could bring the next wave of drugs in the prostate cancer field for the company. In addition, Novartis has clinical candidates targeting FAP, GRPR, and integrins, aiming to go beyond the treatment scope of Lutathera for gastroenteropancreatic neuroendocrine tumors and Pluvicto for prostate cancer, expanding into broader therapeutic areas such as breast cancer, colorectal cancer, lung cancer, and pancreatic cancer.

Leqvio Surges 217%, Moving Towards the Top Small Nucleic Acid Player

Cardiovascular Field Generated $6.391 Billion Revenue for Novartis in 2023, a 36% Increase Year-on-Year. Novartis has only two marketed drugs in the cardiovascular field: its flagship product Entresto and Leqvio, the first siRNA drug targeting PCSK9 for lipid-lowering.

Novartis launched Leqvio in the U.S. market in January 2022. Leqvio's revenue reached $112 million that year and $355 million in sales in 2023, a significant year-over-year increase of 217%. Leqvio has now been approved in 94 countries, contributing to its further market penetration. In Q4 2023, 3,500 institutions globally ordered the product, marking a 13% growth compared to Q3.

PCSK9 inhibitors can significantly reduce low-density lipoprotein cholesterol (LDL-C) levels. The main competitor of Leqvio is Amgen's Repatha, the world's first approved PCSK9 drug. Repatha achieved blockbuster sales of $1.117 billion in 2021, increased to $1.296 billion in 2022, capturing over approximately 70% of the market share, and continued strong sales with $800 million in the first half of 2023.

As an siRNA therapy, one of Leqvio's greatest advantages is its dosing interval of once every six months, compared to Repatha's dosing frequency of every two weeks or monthly. The better compliance has earned Leqvio positive market feedback. According to Novartis, the future sales growth of Leqvio can be benchmarked against Entresto. Evaluate Pharma predicts that Leqvio’s peak sales will reach $3 billion.

In the past two years, Novartis has taken more determined steps in the small nucleic acid field. In January 2022, Novartis collaborated with Alnylam, a giant in the small nucleic acid space, to utilize Alnylam's proprietary siRNA technology to develop an innovative therapy aimed at restoring functional liver cell regeneration in patients with end-stage liver disease. Last July, Novartis announced the acquisition of DTx Pharma for up to $1 billion, gaining its proprietary Falcon platform to develop siRNA therapies for neuroscience indications. Following that in August, Novartis entered into a second collaboration with Ionis, a pioneer in ASO nucleic acid drugs, acquiring the lipid-lowering ASO drug Pelacarsen. This January, Novartis purchased multiple cardiovascular small nucleic acid pipelines from Bohwang Pharmaceuticals for a total of $4 billion.

Novartis is positioning itself to take the leading role before the wave of small nucleic acid truly arrives. In the currently marketed small nucleic acid drugs, Sarepta and Ionis have divided the ASO product market, while Alnylam dominates the siRNA market. However, as more multinational corporations (MNCs) enter the field, the situation where these three biotech companies control the small nucleic acid domain is gradually dissolving. Only in the second half of 2023, three small nucleic acid products from MNCs were approved: Eplontersen, an ASO therapy from AstraZeneca/Ionis, Nedosiran, an RNAi therapy from Novo Nordisk, and Izervay, a nucleic acid aptamer drug from Astellas for treating geographic atrophy.

But for now, the main indications for small nucleic acid drugs are still concentrated in the rare disease field. As of the first half of 2023, the highest-selling small nucleic acid drug is Spinraza, with sales of 800 million USD, indicated for spinal muscular atrophy.Novartis' Leqvio will bring small nucleic acid drugs into a new era: truly entering the field of common diseases, achieving sales of over 2 billion or even 3 billion US dollars, and becoming a new mainstream therapy to compete with antibodies and small molecules.

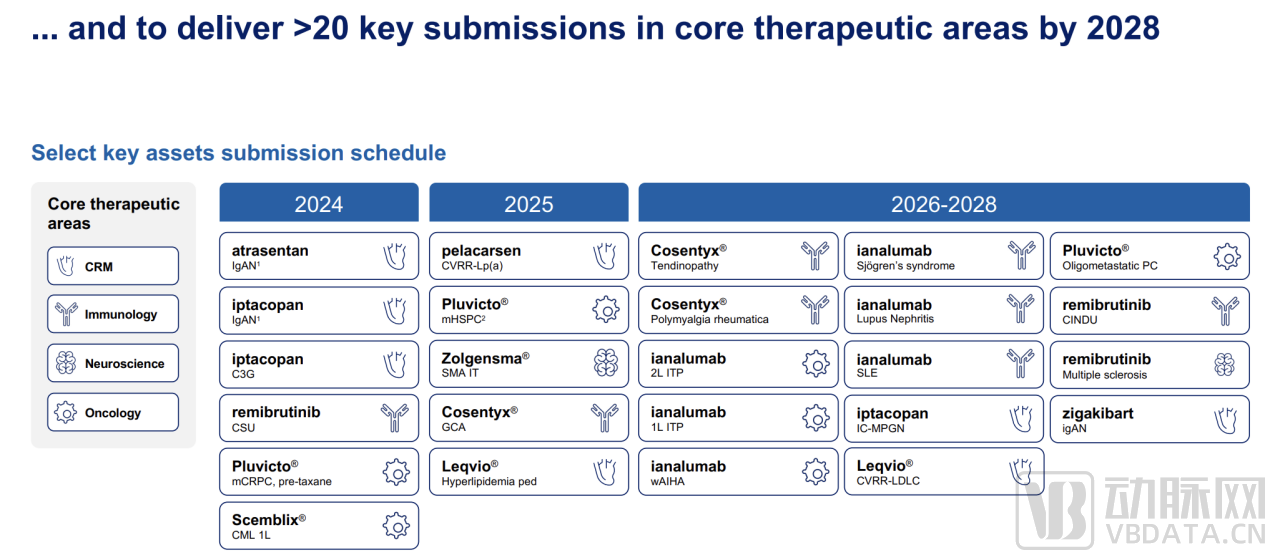

A More Diversified Growth in the Next Five Years

Source: Novartis Investor Presentation

Looking ahead to 2024-2028, Novartis' expansion in the cardiovascular-renal-metabolic and autoimmune fields will be particularly significant.By the end of 2023, iptacopan for the treatment of adult paroxysmal nocturnal hemoglobinuria (PNH) will be launched as the first oral monotherapy, and since then kidney disease will become an important commercial field for Novartis.

Iptacopan is currently in the critical research phase for many other complement-mediated diseases (CMD), including C3 glomerulopathy (C3G), IgA nephropathy (IgAN), lupus nephritis (LN), and cold agglutinin disease (CAD).

Among the ten positive Phase 3 clinical results listed in Novartis' annual report, four are related to kidney disease. This includes the Phase 3 ALIGN study of the ETA antagonist atrasentan for the treatment of IgA nephropathy, which has reached its primary efficacy endpoint. Based on these results, Novartis plans to file for marketing approval in 2024.

And the Chinese market. In 2023, Novartis’ performance in China reached $3.3 billion, growing by 17%. In its annual report, Novartis also specifically emphasized that China is a key development region for the company.

Novartis has opened up the "price-for-volume" strategy for autoimmune drugs in China. In 2023, the price of Secukinumab was reduced again to 870 yuan, with approximately 500,000 domestic patients choosing Secukinumab as their treatment option, achieving nearly 100% availability in prefecture-level cities, hospitals, and DTP pharmacies. In 2023, Omalizumab successfully renewed its inclusion in the medical insurance directory, while its upgraded pre-filled formulation also entered the insurance coverage, benefiting 180,000 patients in China. For pharmaceutical companies, securing medical insurance reimbursement for autoimmune products that require long-term or lifelong use allows them to tap into a new user market among the pyramid population measured by income, and the lower they go, the broader the cross-section of the population.

In addition, Leqvio (Lekewei®) was approved in China last June, becoming the first siRNA drug in the country, and has already achieved early robust growth in the self-pay market.

Perhaps with the market changes, Novartis' strategy on ADC assets may undergo some adjustments. However, at present, Novartis is indeed one of the MNCs most qualified to refrain from ADC deals.

References

Smurf One, https://mp.weixin.qq.com/s/CXlAkxFcyfBxqW2OiiwoDw

VCBeat, https://mp.weixin.qq.com/s/Ie0KHVTce3ppahnXubV8WQ