The New Blockbuster's Looming Patent Cliff: Merck Pursues $15 Billion Deals to Secure Its Future

MSD

Pharmaceutical R&D and Manufacturer

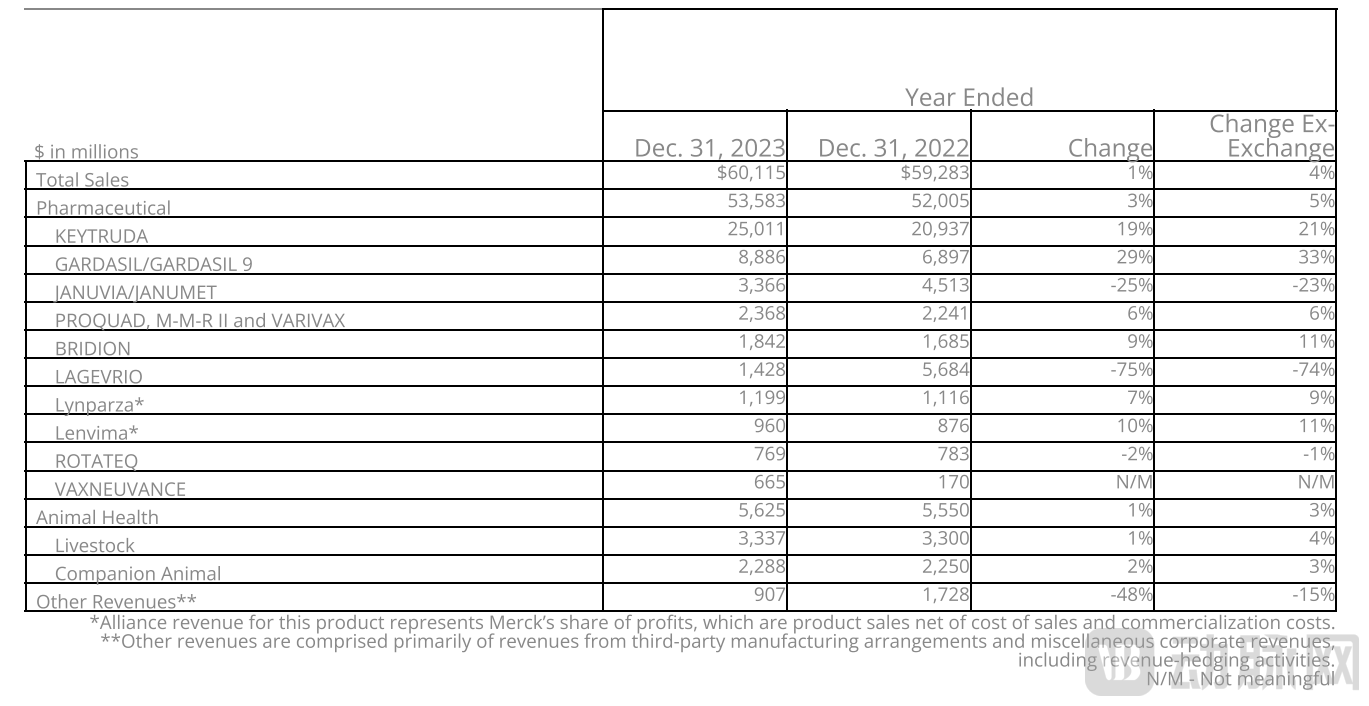

On February 1, MSD announced its 2023 performance, with total annual revenue reaching $60.115 billion, a year-on-year increase of 1%. Excluding the impact of the COVID-19 oral drug Lagevrio, the growth was 9% year-on-year. Among this, $25 billion in sales came from the newly crowned "blockbuster drug" Keytruda, representing a year-on-year increase of 19%.

During the earnings call on the same day, Rob Davis, CEO of Merck & Co., Inc., stated that the company is still seeking acquisition deals in the market ranging from $1 billion to $15 billion. "Although I am very satisfied with the progress we have made in expanding the depth and diversification of our portfolio, we do believe there is a need for more."

In the past three years, MSD has made two acquisition deals exceeding $10 billion each, gaining the pulmonary arterial hypertension drug sotatercept and a pipeline for ulcerative colitis. Behind the continuous search for acquisitions hangs the sword of Damocles over MSD.

Keytruda Has Long Coveted the Title of "Top Drug."

As early as the first quarter of 2022, Keytruda surpassed the former "blockbuster drug" Humira (Humira) with sales of $4.809 billion compared to Humira's $4.709 billion, successfully taking the top position. However, in the 2022 annual report data, Humira narrowly won with $21.237 billion versus Keytruda's $20.937 billion.

In January 2023, Amgen's first Humira biosimilar, Amjevita, officially entered the U.S. market, marking the end of Humira's monopoly. Humira biosimilars developed by multiple multinational corporations such as Samsung, Novartis, Pfizer, and Boehringer Ingelheim will also be launched in the U.S. one after another. The patent cliff has brought about a predictable impact on performance — AbbVie’s revenue for the first three quarters of 2023 was $13.927 billion, a year-on-year decrease of 6.0%; among this, Humira's sales for the first three quarters were only $11.1 billion.

At the same time, Keytruda, which has just ascended to the throne of "King of Drugs," is also facing the countdown threat of a patent cliff. In 2008, MSD applied for the core patent protection of Keytruda — the compound amino acid sequence, with a term of 20 years. This means that in 2028, MSD will lose its patent protection for Keytruda.

"The Patent Cliff" is the Sword of Damocles hanging over innovative drugs from the moment they are born. Once the "patent cliff" arrives, no matter how outstanding the previous sales volume was, their market share will be rapidly eroded by generic drugs or biosimilars. Especially for blockbuster drugs at the level of "blockbuster drugs" such as Keytruda and Humira, the "backlash" of the patent cliff on the pharmaceutical companies to which they belong is even more severe.

Building a "Patent Thicket" to Explore New Indications and Combination Regimens

Generally speaking, innovative pharmaceutical companies facing a patent cliff have several ways out. One is the "patent thicket" strategy, which involves expanding new indications for the core molecule or combining it with other drugs to build peripheral patents for the drug. This not only expands the drug's audience but also effectively extends the product lifecycle.

Taking Humira as an example, AbbVie has built a "patent thicket" around Humira and each of its new indications. According to the US non-profit organization Initiative for Medicines, Access & Knowledge, AbbVie has applied for approximately 250 patents in the US related to Humira, 90% of which were filed after Humira was approved in 2002.

MSD's official website shows that Keytruda is currently under submission for review for five indications: hepatocellular carcinoma, resectable non-small cell lung cancer, HER2-negative locally advanced unresectable or metastatic gastric cancer, locally advanced unresectable or metastatic biliary tract cancer, and newly diagnosed high-risk locally advanced cervical cancer. These submissions involve countries and regions including the United States, the European Union, and Japan.

In addition to broadening the indications for single-agent therapy, MSD's development of Keytruda also focuses on exploring the potential of various combination therapies. On one hand, the response rate of PD-1 monotherapy is relatively low, and everyone is looking for combination regimens that can improve the response rate. On the other hand, numerous collaborative explorations also reflect MSD's potential anxiety in the face of the "patent cliff."

In 2023, MSD launched several Phase III clinical studies on combination regimens, such as the strong collaboration with Moderna to develop and commercialize the mRNA cancer vaccine mRNA-4157, initiating two studies on combination therapy for non-small cell lung cancer; TROP2 ADC MK-2870, introduced from Kelun-Biotech, started a pivotal Phase III study for first-line combination treatment of non-small cell lung cancer. In addition, cutting-edge therapies such as oncolytic viruses, tumor electric fields, TIL, microbiota, and CAR-M also appeared in the combination regimens.

The second path to addressing the patent cliff lies in seeking pillar drugs and promising pipelines beyond the "blockbuster drug." MSD's Q4 and annual financial data for 2023 both underscore the urgency of diversifying its portfolio.

Source: MSD 2023 Annual Report

From the 2023 annual financial report, MSD's pharmaceutical business revenue reached $53.583 billion, a year-on-year increase of 3%. Among this, Keytruda's revenue amounted to $25.011 billion, contributing 41.6% of the total revenue. Following closely, the HPV vaccine GARDASIL/GARDASIL 9 achieved a revenue of $8.886 billion, showing remarkable growth with an increase of 29% year-on-year, even surpassing Keytruda.

In terms of Q4 2023 data, Keytruda's sales reached $6.61 billion, accounting for 45% of the total Q4 sales; GARDASIL achieved $1.87 billion, representing 64.5% of MSD’s total pharmaceutical sales of $13.1 billion.

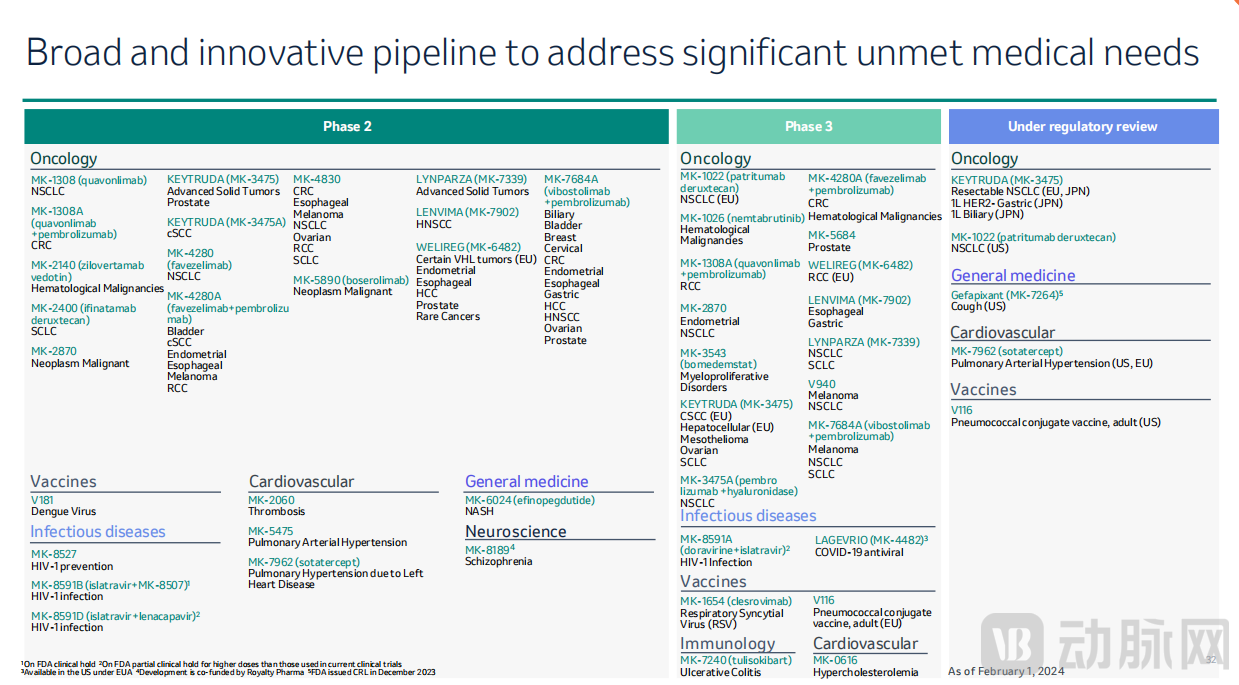

In addition to its commercialized drugs, MSD has over 80 assets in Phase II clinical trials and more than 30 in Phase III. In 2023, MSD completed project approvals for over 25 drugs with major regulatory agencies worldwide, initiated Phase III trials for over 20 pipeline assets, and announced plans to "launch more Phase III clinical trials in 2024."

However, it is not easy to find a drug that can match the scale of the "King of Drugs."

In 2021, Merck & Co., Inc. acquired Acceleron for $11.5 billion (the second-largest biopharmaceutical deal of the year). This acquisition brought Sotatercept, a drug for treating pulmonary arterial hypertension, which has already submitted a BLA application to the FDA and is expected to be approved in March. Data from the Phase III clinical trial showed a significant improvement in exercise test scores in a key polycyclic aromatic hydrocarbon (PAH) trial.

Currently, MSD has high hopes for Sotatercept and is working to submit documents to the FDA, hoping it will become one of its "successor" blockbuster drugs. According to a report by FierceBiotech, Evaluate's latest report listed the 10 most valuable products currently in development, among which Sotatercept had the highest predicted net present value (NPV) at $11.6 billion, with expected sales reaching $2.6 billion by 2028.

In 2023, MSD acquired Prometheus for $10.8 billion (the third-largest biopharmaceutical deal of the year). This transaction is seen as MSD's attempt to enter the autoimmune field. Currently, the pipeline targeting ulcerative colitis and Crohn's disease is in Phase II clinical trials. At the time of the deal, MSD stated that the ulcerative colitis treatment drug PRA023 has "multi-billion-dollar peak sales potential."

In addition to acquisition deals, CEO Rob Davis also mentioned, "We also see collaboration as an important tool."

On October 19, 2023, MSD and Daiichi Sankyo entered into a collaboration to jointly develop three ADC candidates: patritumab deruxtecan targeting HER3 (for which an application for market approval has received FDA priority review); ifinatamab deruxtecan targeting B7-H3; and raludotatug deruxtecan targeting CDH6. MSD paid $4 billion as an upfront payment and committed to $1.5 billion in continuous payments over two years for this collaboration, with potential future milestone payments reaching up to $16.5 billion, totaling approximately $22 billion.

Whether "we are still looking for acquisition deals ranging from $1 billion to $15 billion," or the Damocles sword of Keytruda hanging overhead, it all seems to suggest that MSD is poised for action in 2024.

According to John Boylan, a healthcare analyst at Edward Jones, "MSD generates strong cash flow every year, which should allow it to achieve growth through internal research investment and acquisitions." The 2023 annual financial report indicates that MSD expects its performance to continue growing in 2024, with annual revenue projected to reach between $62.7 billion and $64.2 billion.

First, there is a continuous increase in R&D investment. In 2023, MSD's R&D investment reached as high as 30.531 billion US dollars, while in 2022, the R&D investment was only 13.548 billion US dollars, increasing more than doubled year-on-year. Notably, the related costs caused by acquisitions and divestitures alone amounted to 8.19 billion US dollars.

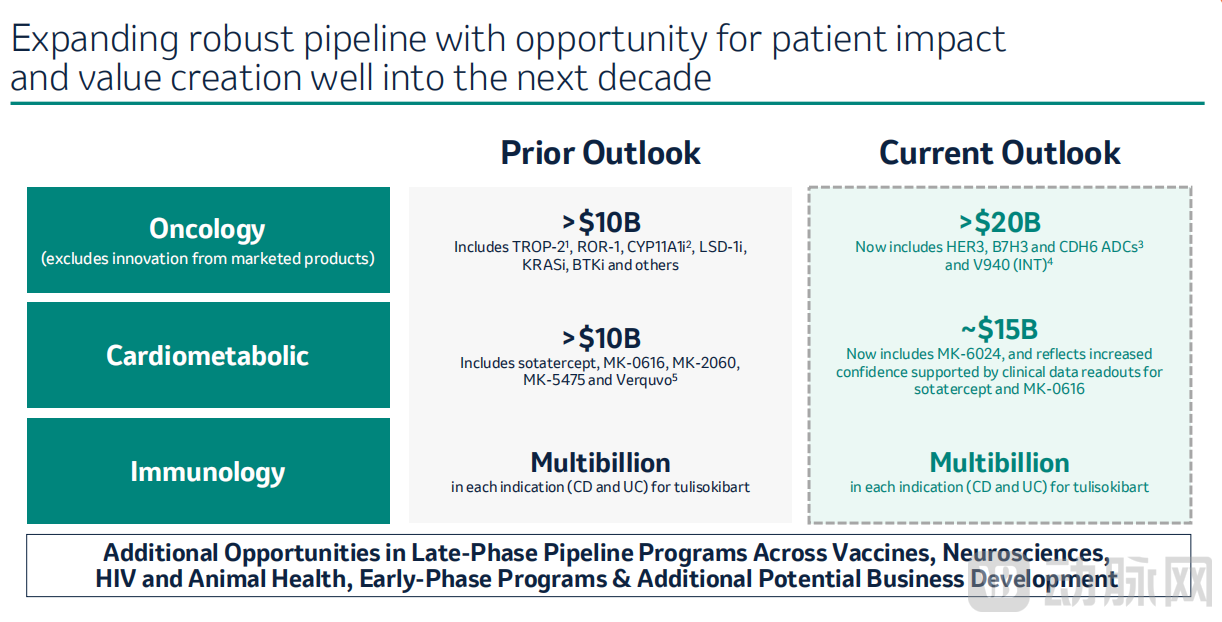

In terms of fields, the sales in the fourth quarter and the entire year of 2023 reflected the continued growth in oncology and vaccines. Looking ahead to the next decade, MSD's focus remains on the oncology portfolio, cardiometabolic, and immunology.

(2023Q4 Ten-Year Forecast and Outlook)

(2023Q4 Ten-Year Forecast and Outlook)

In the research pipeline, neuroscience, endocrinology, and metabolic diseases may be the early directions of its strategic layout.

(2023Q4 R&D Pipeline)