Samsung Eyes Keytruda Biosimilar as $25 Billion 'Blockbuster' Faces Mounting Competition

Samsung Bioepis

Biosimilar Developer

After nearly a decade of dormancy, Merck's Keytruda (K drug, pembrolizumab) has finally outlasted the patent expiration of Humira, achieving a remarkable $25 billion in sales to successfully claim the throne of the world's best-selling "drug king" in 2023.

However, it's easier to attack than to defend. Behind Merck's Keytruda, GLP-1 drugs from Novo Nordisk and Eli Lilly are in short supply, with the market growth becoming increasingly fierce. More notably, a key patent for Keytruda is set to expire in 2028, and already, many biosimilars are poised to enter the market.

Recently, Samsung's entry into the K-drug biosimilar competition has drawn market attention. On February 21, Samsung Bioepis announced the initiation of Phase I clinical trials for the K-drug biosimilar SB27.

In fact, whether overseas or in China, there are quite a few companies eyeing the biosimilar versions of Keytruda. Industry insiders point out that if biosimilar products come to market in the coming years, the market position of Keytruda and MSD may face even greater competitive pressure.

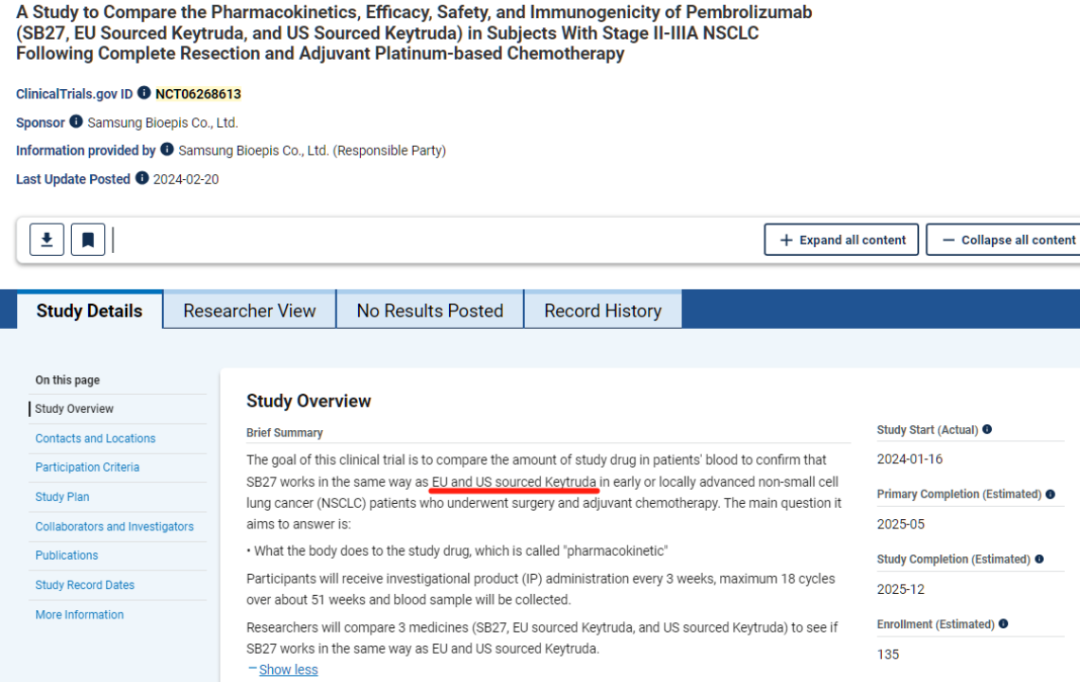

According to the public information from the U.S. clinical database ClinicalTrials.gov, Samsung Bioepis has initiated a Phase I clinical trial of SB27 for Stage II-IIIA non-small cell lung cancer patients who have undergone complete resection and adjuvant platinum-based chemotherapy.

Public information shows that SB27 is a randomized, double-blind, three-arm, parallel-group, multi-center Phase I clinical trial designed to compare the pharmacokinetics, efficacy, safety, and immunogenicity of three versions of pembrolizumab (SB27, Keytruda sourced from the EU, and Keytruda sourced from the US) in patients with Stage II-IIIA non-small cell lung cancer who have undergone complete resection and adjuvant platinum-based chemotherapy. Participants will receive the investigational product (IP) every three weeks and provide blood samples for up to 18 cycles over approximately 51 weeks.

This time, all eyes are on the "top influencer" in the PD-1 field. Samsung Bioepis is already an expert in biosimilars. Established in 2011, Samsung Biologics, together with Biogen, co-invested to form Samsung Bioepis the following year, focusing on the development of biosimilars.

Although Biogen announced in 2022 that it would sell its equity in Samsung Bioepis to Samsung Biologics, Samsung Bioepis was not affected by the change in equity. As of February 2024, Samsung Bioepis has received global approval for multiple biosimilars, including SB4 (Benepali, etanercept), SB2 (Flixabi, infliximab), SB5 (Imraldi, adalimumab), SB3 (Ontruzant, trastuzumab), SB8 (Aybintio, bevacizumab), SB11 (Byooviz, ranibizumab), and SB12 (eculizumab). In addition, among the biosimilars under development, except for SB27 which is currently in Phase I clinical trials, SB15, SB16, and SB17 have all completed Phase III clinical trials.

Compared to the enormous investment and R&D risks of innovative drugs, biosimilars clearly offer higher certainty. As the world's largest biosimilar manufacturer, Samsung Bioepis holds more than 10% of the global biosimilar market share.

Now, the K drug that has caught the attention of Samsung Bioepis is Merck's most important drug.

Over the past nearly 10 years, Merck has spared no effort in developing a wide range of indications for Keytruda. To date, Keytruda has been approved for approximately 40 indications in the United States and over 10 indications in China. On the 4th of this month, Merck announced that Keytruda had received approval from China's National Medical Products Administration for use in combination with gemcitabine and cisplatin as a first-line treatment for patients with locally advanced or metastatic biliary tract cancer (BTC). This marks the 13th indication for Keytruda to be approved in China.

Timeline of K Drug's Approved Indications in China

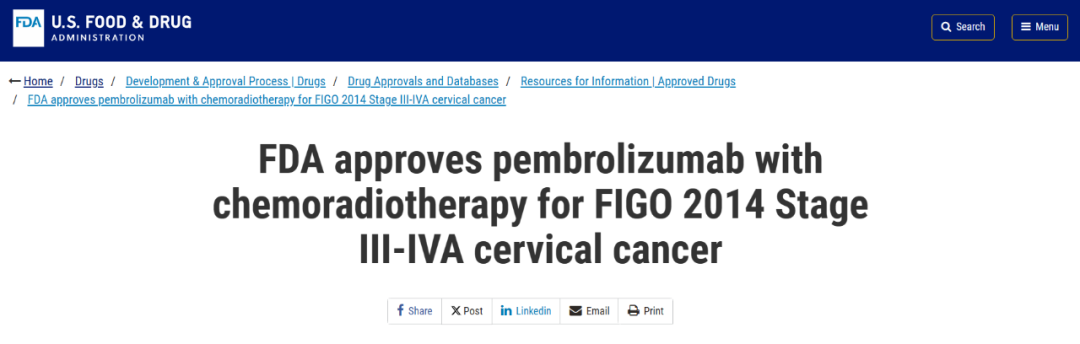

Last month, on January 12, Merck announced that Keytruda (K药) received FDA approval for use in combination with concurrent chemoradiotherapy to treat newly diagnosed stage III-IVA cervical cancer patients. This is the third indication for Keytruda in cervical cancer and its 39th indication approved in the United States.

At this point, whether it is used as a single agent, combination therapy, or adjuvant treatment, K drug has reached the top level among PD-(L)1 targeted drugs. Precisely because it holds a "far ahead" position in niche markets, the K drug has become a target for many competitors.

How long can K drug maintain its market exclusivity in the next few years? What kind of competitive situation will the entry of biosimilars bring? Could the "moat" built by K drug become a "bridal gown" for competitors in the broader market? The market is paying close attention to these questions.

As time goes on, more and more biosimilars of K drug are "coming to light."

According to the ClinicalTrials database, besides Samsung Bioepis, at least two other companies have registered trials for biosimilars of Keytruda.

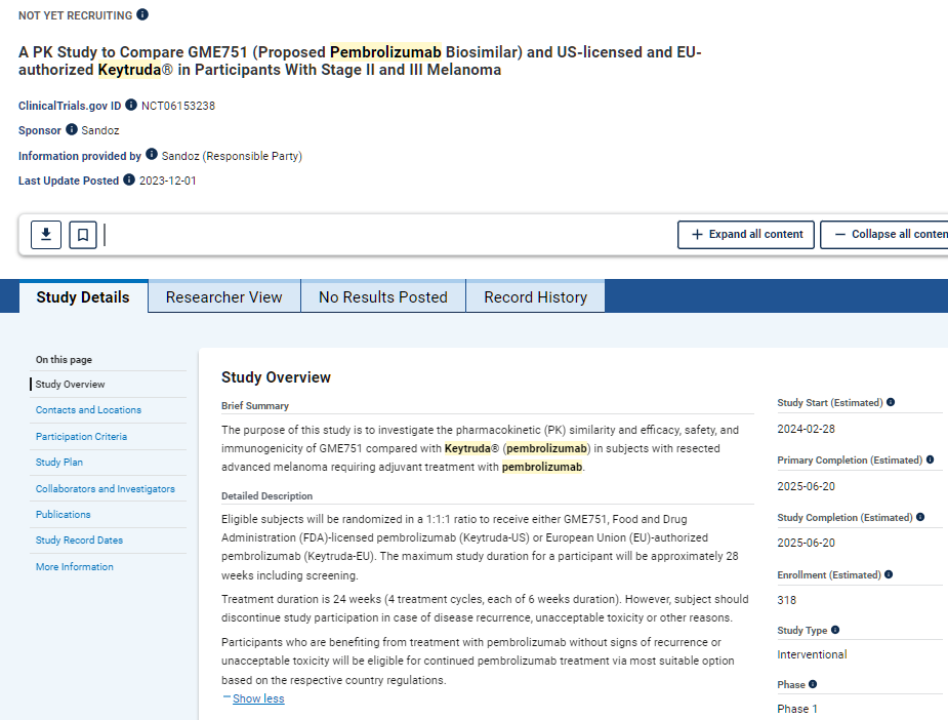

On December 1 last year, Sandoz, a giant in generic and biosimilar drugs, registered a "head-to-head" clinical trial (NCT06153238) of K medicine and GME751. The trial began on February 28 this year and will compare GME751 with K medicine in patients with resected advanced melanoma who require adjuvant treatment with K medicine. It is reported that GME751 is the biosimilar product of K medicine.

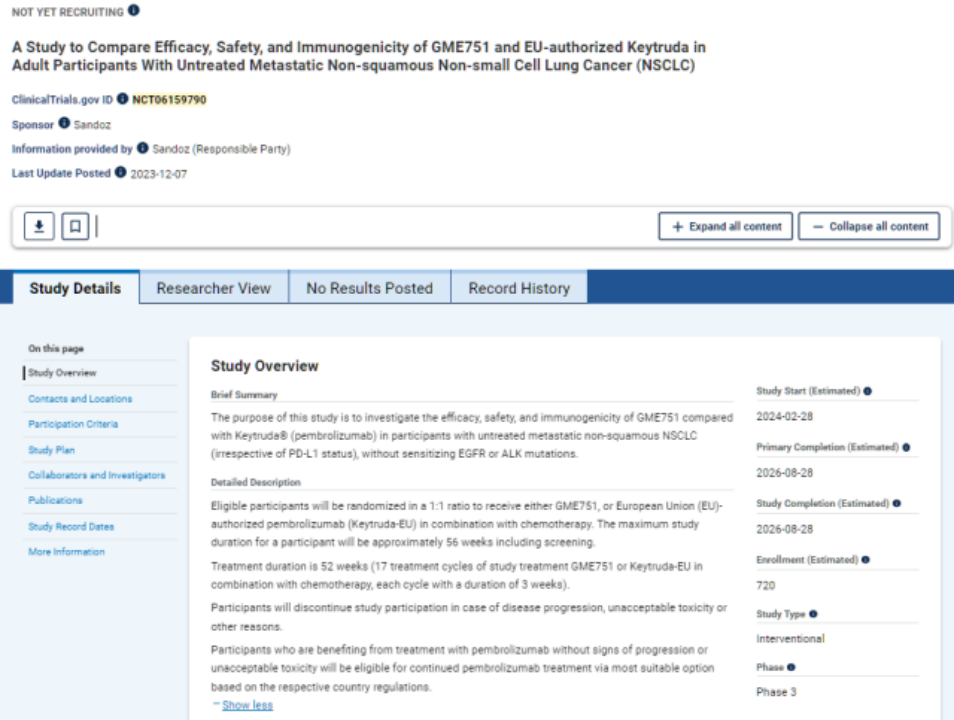

Just a few days later, on December 7, Sandoz registered another Phase III "head-to-head" trial (NCT06159790) for its K药 biosimilar GME751. This trial, also set to begin on February 28 this year, aims to compare the efficacy, safety, and immunogenicity of GME751 with the EU-approved K药 in adult participants with untreated metastatic non-squamous non-small cell lung cancer (NSCLC).

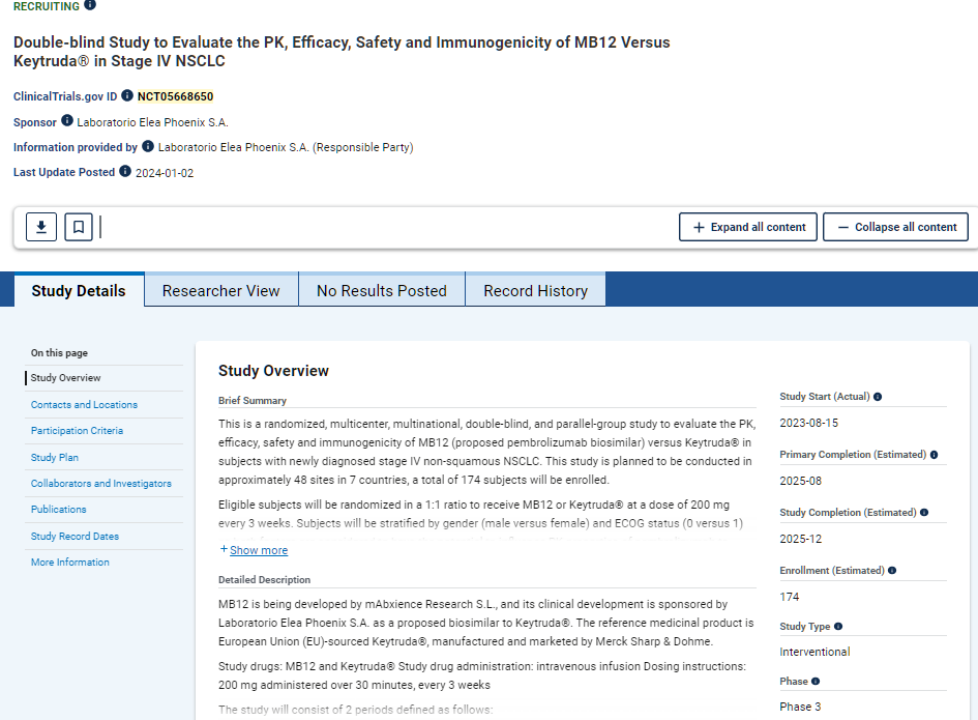

On January 2 this year, mAbxience Research, controlled by Fresenius, registered a Phase III head-to-head trial (NCT05668650) for MB12, a biosimilar of K medicine. The study began in August 2023 and involves newly diagnosed Stage IV non-squamous NSCLC patients.

On September 1, 2020, NeuClone Pharmaceuticals, a biosimilar company headquartered in Australia, announced that two of its biosimilars under active development (K-medicine and O-medicine) had reached the late stage of preclinical development. In addition, MB12 from Laboratorio ELEA, BCD-201 from Biocad, and other companies are also accelerating the development process of K-medicine biosimilars.

Bringing the focus back to China, companies such as Qilu Pharmaceutical and Henlius have also launched initiatives for the biosimilar of Keytruda.

On December 4, 2023, the Drug Clinical Trial Registration and Information Disclosure Platform showed that Qilu Pharmaceutical had registered a Phase 1 clinical trial of QL2107 Injection in healthy volunteers.

Although Qilu has not disclosed any information about QL2107. However, based on the publicly available trial details, this product is speculated to be a biosimilar of K medicine. This Phase I clinical trial plans to enroll 168 healthy volunteers and is expected to be completed in June 2024.

Henlius follows closely behind. According to the Henlius official website, the K drug biosimilar HLX17 is currently in the IND stage. On August 29, 2023, Henlius submitted the HLX17 clinical trial application (acceptance number: CXSL2300579), and no public trial information is currently available for inquiry.

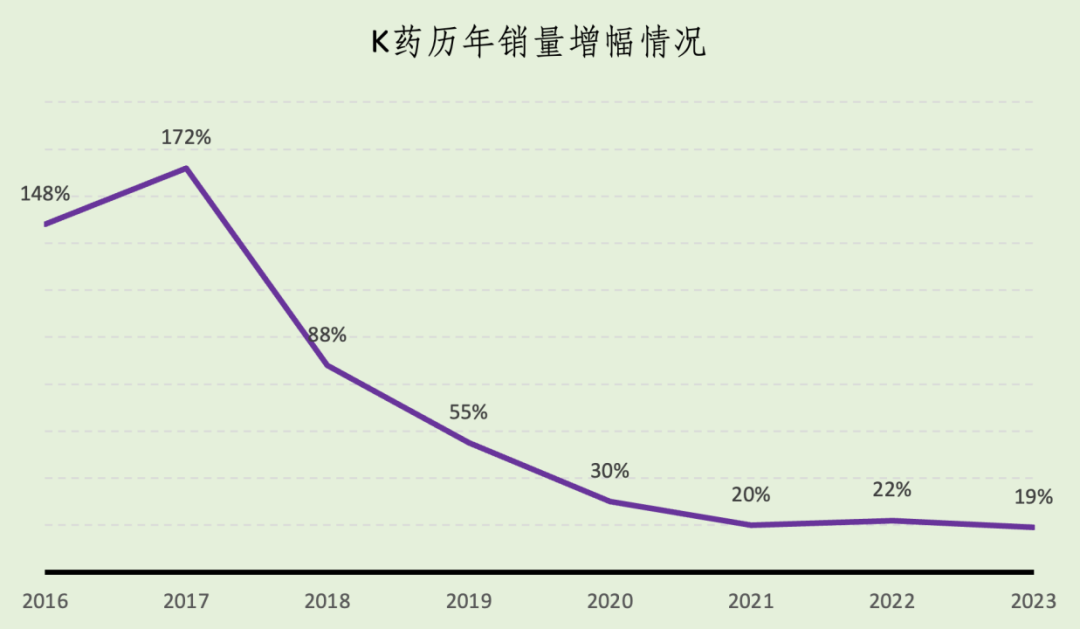

Facing the increasingly approaching patent cliff and the growing emergence of biosimilars, how much longer can Merck's Keytruda remain on the "blockbuster drug" throne? According to Merck's financial report, behind the $25 billion sales of Keytruda in 2023 was a 19% growth rate, showing a slowdown compared to the 22% sales growth in 2022.

For biosimilars, the "USD 250 billion market pie" is undoubtedly highly attractive. Market analysts believe that the newly crowned "blockbuster drug" must take precautions and prepare in advance for the upcoming new round of competition.

Previously, Merck stated that Keytruda (K药) would advance into the treatment of early-stage tumors. In 2021, Keytruda received approvals for multiple early-stage tumor indications, including triple-negative breast cancer, renal cancer, and melanoma. Jannie Oosthuizen, President of Global Oncology at Merck, further predicted that by 2025, 25% of Keytruda’s total revenue might come from early-stage diseases.

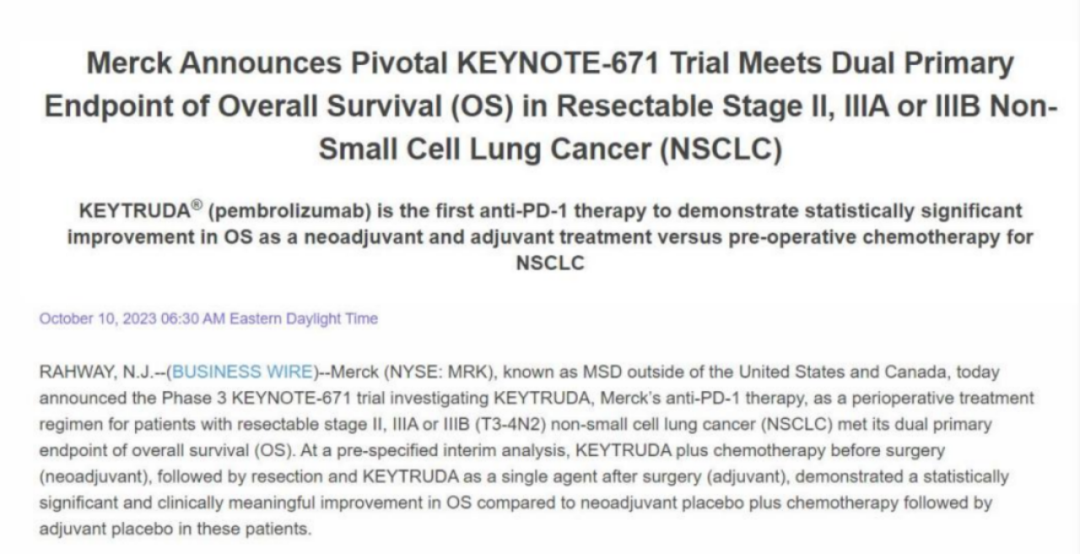

Last October, Merck released the Phase III clinical data of Keytruda (K药) in the treatment of early-stage NSCLC. Market analysis indicated that the positive results from the KEYNOTE-671 clinical trial might refresh the clinical treatment pathway for early-stage NSCLC. This significant perioperative clinical progress could potentially help Keytruda extend its reign as the "king of drugs."

At the same time, Merck is also actively developing a subcutaneous injection formulation of Keytruda.

On March 21, 2023, the CDE website announced that Merck's Class 1 new drug MK-3475A injection had received implied permission for clinical trials, intended for the development of lung cancer treatment. According to publicly available data, MK-3475A consists of the anti-PD-1 monoclonal antibody pembrolizumab and hyaluronidase, in a subcutaneous injection (SC) formulation. It is currently undergoing international multicenter Phase III clinical research, aiming to demonstrate that MK-3475A is not inferior to intravenous K-drug in terms of pharmacokinetic parameters.

The birth of the "King of Medicines" relies not only on luck but also on strength. Can K Medicine blaze a new legendary path? The New Media Center of *Pharmaceutical Economy Report* will continue to follow up.

Editor: Shuwen

www.yyjjb.com.cn

Insight into Industry Trends

"Pharmaceutical Economy News"

Academic Official Account

Focus on the Frontiers of Oncology Academia

Terminal Official Account