Results of the 28-Category Medical Consumables Centralized Procurement Reshape the RMB 10-Billion Neurointervention Market as Johnson & Johnson and Stryker Lose Bids

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

Stryker

Orthopedic Product Developer

SINOMED

High-end interventional medical device R&D, production, and sales provider

HeartCare

Neurointerventional Medical Device Developer

Covidien

Medical Solutions Provider

Zenith Vascular

Cerebrovascular Device R&D and Manufacturer

Since the beginning of 2024, multiple centralized procurement initiatives have been carried out in the neurointervention market.

On March 6, 2024, the Beijing-Tianjin-Hebei 3+N Alliance announced that it would carry out volume-based procurement of neurointerventional coil devices. On March 19, 2024, the results of the volume-based procurement for 28 categories of medical consumables in the "Beijing-Tianjin-Hebei 3+N" region were announced, with guiding catheters, thrombectomy stents, and intracranial stents in the neurointerventional field included in the procurement list.

The "Jing-Jin-Ji 3+N" volume-based procurement of 28 categories of medical consumables has drawn significant attention from the industry. On one hand, although the frequency of past neuro-interventional procurements was high, the price reduction was relatively moderate at around 40%-60%. However, this procurement requires that out of three participants, only two can win, with one being eliminated, and there are no guaranteed winning terms. Under these rules, the price reduction in this procurement exceeded expectations. A total of 748 products participated in this procurement for 28 categories of medical consumables, with 202 products proposed as winners, resulting in a winning rate of only 27%.

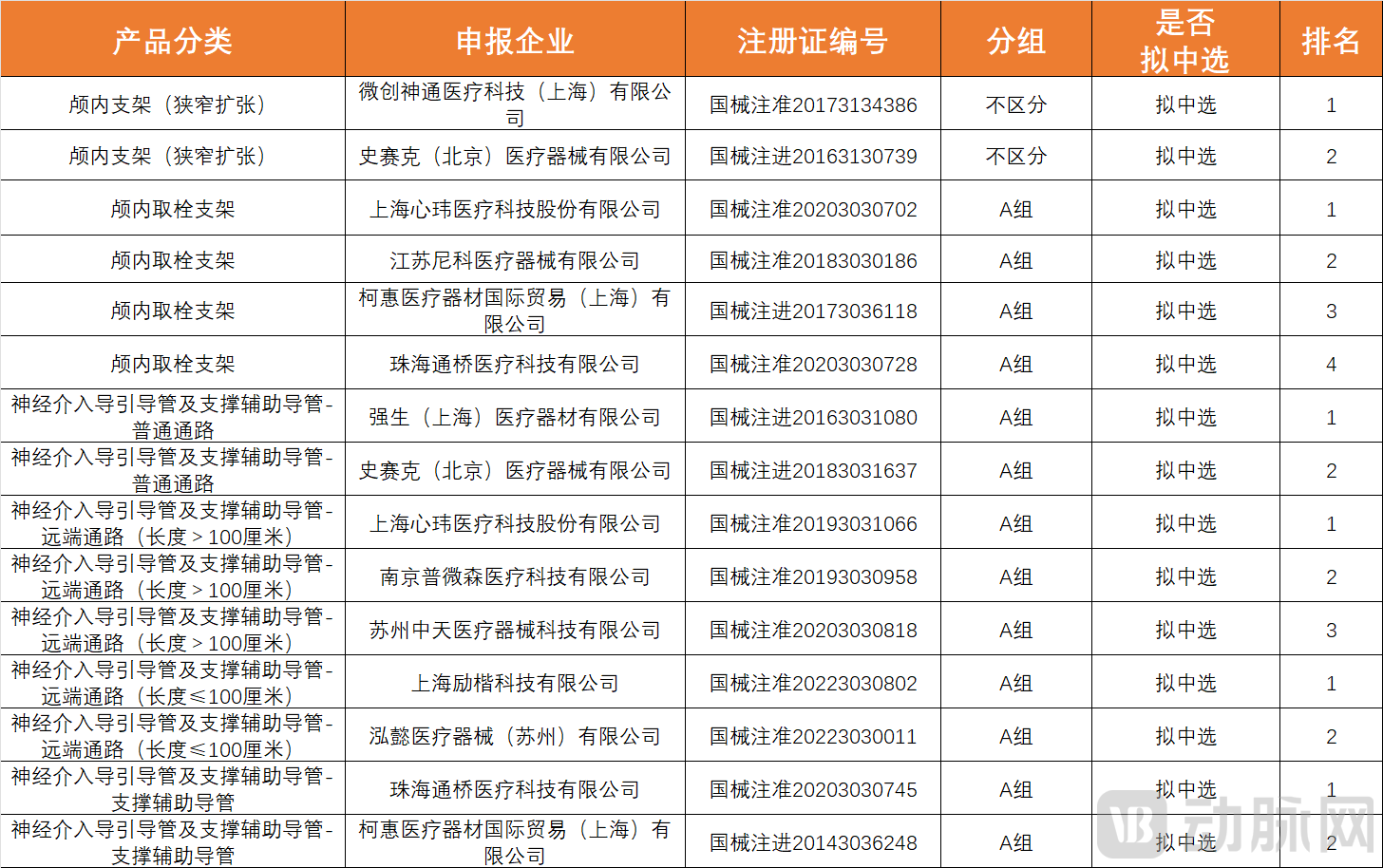

In the field of neurointervention, amidst fierce competition, the intracranial stents (for stenosis dilation) by MicroPort and Stryker are tentatively selected, while SINOMED did not make the cut; in the category of intracranial thrombectomy stents Group A, HeartCare, Jiangsu Nico Medical Equipment Co., Ltd, Covidien, and Zhuhai Tonbridge Medical Device Co., Ltd. are tentatively selected, with products from over 20 companies not selected; for neurointerventional guiding catheters and supportive auxiliary catheters Group A, Johnson & Johnson, Stryker, HeartCare, Zenith Vascular, Zhuhai Tonbridge Medical Device Co., Ltd., and Covidien are tentatively selected, with products from more than 111 companies not selected.

Main Winning Bids for Neurointerventional Products in the 3+N28 Category of Medical Consumables Group Procurement in the Beijing-Tianjin-Hebei Region

On the other hand, this provincial alliance accounts for about 15% of the national market scale, and companies that lose the bid will be unable to sell their products in this region for two years.If companies can break through in the centralized procurement, they will be able to increase their market share and are expected to achieve high growth and high penetration of their products. This round of centralized procurement will have a significant impact on the market landscape.

Three Years After the Implementation of the Volume-Based Procurement Policy, Centralized Procurement Has Become a Watershed for Industry Development. Some Companies That Did Not Actively Participate in Centralized Procurement Have Lost Market Share, While Others Have Opened Up Markets with Originally Low Market Penetration Through Centralized Procurement or Centralized Negotiations, Surging to First Place in Market Share via Procurement.

Mastering the Centralized Procurement Game Becomes Key to Market Success; Centralized Procurement Reshapes the Market Landscape of Different Segments. In the Billion-Dollar Neurointervention Market, What Effects Will Centralized Procurement Bring?

The neurointerventional products included in this centralized procurement are intracranial stents (stenosis dilation), intracranial thrombectomy stents, neurointerventional guiding catheters, and supportive auxiliary catheters.

From the results of this centralized procurement market, domestic companies and foreign enterprises are evenly matched.U.S.-based Medtronic actively participated in the centralized procurement bidding, while Johnson & Johnson and MicroVention also secured a certain share in the procurement. In terms of the proportion between domestically produced and imported products, this round of centralized procurement has led to a better-than-expected elimination rate for foreign enterprises.

In terms of foreign investment bids, Stryker's intracranial stent product is proposed to be selected; Medtronic's Covidien thrombectomy stent was awarded through a circuit breaker mechanism, while Johnson & Johnson and Stryker Group B were eliminated. In the highly competitive neuro-interventional guiding catheter category, one ordinary pathway product from Johnson & Johnson and Stryker Group A is proposed for selection; in the distal pathway category, none of Johnson & Johnson, Medtronic, or Stryker were selected.

Among Chinese manufacturers, SINOMED's intracranial stent was not selected, and JiaChi Bio's thrombectomy stent, neurointervention guiding catheter, and support assist catheter - distal access (length > 100 cm) were not selected in Group A for both products.

The biggest winner among the domestic companies in this centralized procurement is HeartCare, which ranked first in Group A for both its intracranial thrombectomy stent and distal access catheter products.

In terms of the extent of price reduction, under the background of rule-setting guidance for price reduction, the price reduction in this centralized procurement was significant. Among them, the price reduction for guiding catheters, which are auxiliary products in the neurointerventional pathway category, was particularly substantial.

How will the significant price reduction of access products impact the market landscape?

According to the development patterns of multiple high-value consumable product bulk procurement in the past, the reduction in prices has alleviated the burden of diseases to a certain extent, which enhances patients' willingness to pay, and the number of surgeries will increase rapidly in the short term. On the other hand, after the implementation of bulk procurement, the concepts, operational habits, and usage preferences of clinical doctors are also changing, leading to a significant increase in the utilization rate of innovative devices under the same surgical procedure.

The significant price reduction in the centralized procurement of access-related auxiliary products will free up market space for the clinical application of therapeutic products, leading to changes in the market structure. Access-related products primarily serve as auxiliary support during interventional surgeries and are essential consumables for every interventional procedure, with a usage frequency much higher than therapeutic devices. The guiding catheters included in this centralized procurement provide a stable pathway for other interventional devices, facilitating their access to specified locations within blood vessels. They are widely used across various vascular interventional treatments.

In the past, under the DRGs/DIP payment system, the high unit price of auxiliary products limited doctors' use of innovative devices. With a cap on surgical fees, the cost of a guiding catheter was around 20,000 yuan. When doctors used high-priced access guiding catheters in clinical practice, they often avoided using other expensive treatment products like aspiration catheters or occlusion balloon catheters, resorting instead to off-label use of guiding catheters. The price reduction from this centralized procurement will drive different products back to their original indications, allowing doctors and patients to access better products.

After centralized procurement, the use of core therapeutic products becomes more beneficial, and therapeutic product categories are welcoming expansion opportunities, especially aspiration catheters.Off-label use of guiding catheters in clinical practice will first drive the growth of aspiration catheter products. In addition, the reduction in the price of access-related consumables will create more room for the use of innovative devices in clinical treatment, providing an opportunity for innovative products in the neurointervention field to increase their penetration rate.

Although the neurointerventional market has a high frequency of centralized procurement, innovative products have not achieved full coverage of centralized procurement. Companies are expected to leverage centralized procurement products to drive the growth of the entire product category market.

The price reduction in centralized procurement also aligns with the competitive landscape of the neurointervention industry. Guiding catheters, which saw a significant price drop, are products with relatively lower approval thresholds. In China, there are already 117 registered certificates for neurointervention access catheters, while there are only 17 registered certificates for aspiration catheters.

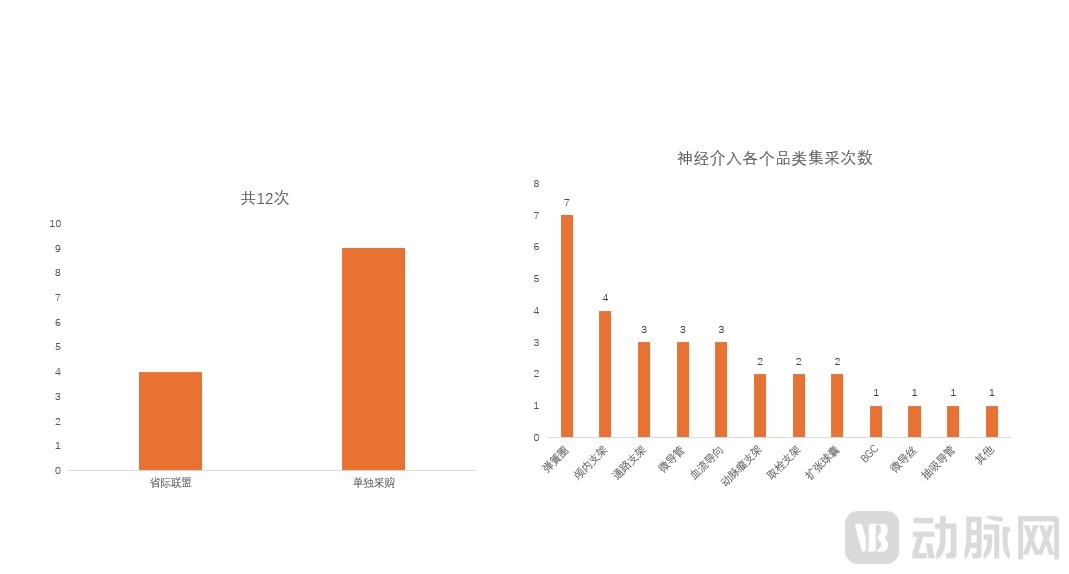

According to IQVIA statistics, intracranial stents, access catheters, and microcatheters are the neurointerventional products with the most procurement rounds after coils.

Neurointerventional Procurement Data Source: IQVIA

This centralized procurement will become a turning point in China's neurovascular market competition. "Low-barrier" auxiliary products will shift from being marketing-driven to cost-driven, making room for "high-barrier" therapeutic products (aspiration catheters, intracranial stents, drug-coated balloons, and drug-eluting stents) in the market and promoting the overall upgrading and transformation of the industry.

Neurointervention is the fastest-growing细分领域 in the high-value耗材 of cardiovascular and cerebrovascular diseases. By the end of 2023, China's population aged 60 and above has reached 290 million. The rapidly increasing elderly population, combined with a relatively low渗透率 of cardiovascular and cerebrovascular disease treatments, will drive持续增长 in the cardiovascular and cerebrovascular耗材 market. The number of neurointerventional surgeries has reached 350,000 to 400,000 per year, with a growth rate of over 30%. Based on hospital admission prices, the市场规模 of the neurointervention market has reached 20 billion yuan.

Data Source: Neurointervention Faces a Market of Over 20 Billion — CICC

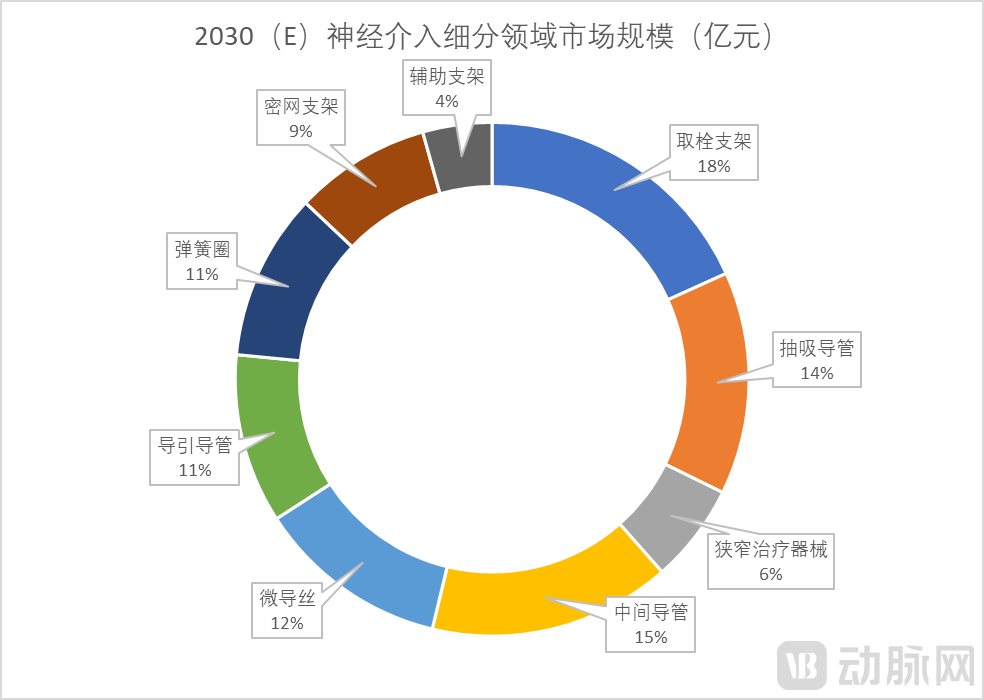

High-value consumables for neurointervention include five major categories of products: ischemic, hemorrhagic, stenotic, carotid artery, and vascular access devices. According to a previous forecast by CICC, by 2030, access devices will account for 38.0% of the neurointervention market, with an expected market size reaching 10.56 billion yuan.

From the development of ischemic and hemorrhagic conditions, surgical treatment for hemorrhage has become relatively mature after 20 years of progress; while interventional procedures for ischemia only began to develop gradually after 2017, with a low initial base of ischemic surgeries in the early neurointerventional market. However, the incidence of ischemia is much higher than that of hemorrhage. With the establishment of stroke centers, the volume of ischemic surgeries in China has reached parity with, or even surpassed, that of hemorrhagic surgeries.

In 2023, the market share of domestically produced products in the neurointerventional field reached 25%. Chinese companies in the neurointerventional sector are developing rapidly, with domestic firms establishing advantages through differentiated competition.

According to the financial reports of listed companies, the revenue growth of HeartCare was mainly driven by the sales of devices for acute ischemic stroke (AIS) thrombectomy, intracranial stenosis treatment, and innovative access medical devices. In the ischemic field, the company offers a full range of products including thrombectomy stents, occlusion balloons, and aspiration catheters. It also features the 4F HeartCare intracranial thrombus aspiration catheter, the 3mm HeartCare stent MeVO combination solution, and the HeartCare 8F extra-large caliber aspiration catheter.

The R&D products mainly focus on the stenosis and hemorrhage markets, including drug-eluting balloons, carotid artery stents, flow diverter devices, and other products.

The performance growth of Zhuhai Tonbridge Medical Device Co., Ltd. mainly comes from intracranial support catheters, intracranial PTA balloon dilation catheters (Rx), and intracranial thrombectomy stents. The R&D pipeline is primarily focused on the stenosis and hemorrhage markets, including intracranial drug-coated balloons, intracranial stents, drug-eluting self-expanding stents, flow diverter devices, and remote support catheters.

Minimally Invasive Brain Science mainly relies on flow-diverting dense mesh stents, rapamycin-targeted drug-eluting stents, and coil-driven growth in the hemorrhagic field. The R&D pipeline is primarily focused on the ischemic and stenosis markets.

In the first half of 2023, Peijia Medical's hemorrhagic, ischemic, and access products accounted for 27.3%, 39.1%, and 33.1% of divisional revenue, respectively. The R&D pipeline is primarily focused on the ischemic market, including products such as aspiration catheters, intracranial stents, and intermediate guiding catheters.

In terms of pipeline layout, several domestic neurointerventional companies have basically achieved comprehensive coverage in the hemorrhagic, ischemic, stenotic, and access markets, and have also established advantages in different细分 fields.HeartCare and Tonbridge Medical are more competitive in the ischemic market, while MicroPort NeuroTech and Peijia Medical have an edge in the hemorrhagic market. In terms of R&D pipelines, leading domestic companies are consolidating their strengths while extending their reach to cover broader markets.

The rapid development of the neurointerventional market coincides with the period of centralized procurement in China's medical device market, significantly shortening the pre-procurement lifecycle of products compared to the pre-healthcare reform era. How companies leverage the industry characteristic of complementary use of high-value consumables during centralized procurement to strategically plan and enhance performance has become crucial.

In the Chinese market, centralized procurement has become the main factor in market differentiation. Four years after the implementation of centralized procurement, industry profits have been compressed, the localization process of multinational corporations (MNCs) has accelerated, and the share of domestically produced products has significantly increased due to centralized procurement. The iteration of industry products has also sped up. Centralized procurement has profoundly reshaped the competitive landscape of the industry, and enterprise development has diverged during this process.

Overall, to gain an advantage in the centralized procurement, it is necessary to plan before taking action.

Before the centralized procurement, enterprises need to utilize efficient channels to increase hospital penetration and gain doctors' recognition of the products, enhance brand influence, boost hospital usage, and prepare for grouping in volume-based procurement. Only by entering Group A with a larger reported volume can they strive for a larger market share.

In centralized procurement, different regions have different characteristics, and companies need to deeply understand the procurement rules and accurately report quantities and prices. Taking the Beijing-Tianjin-Hebei 3+N procurement as an example, this procurement alliance often sees significant price reductions; provinces such as Anhui and Fujian have higher procurement frequencies, more types of products under procurement, and also participate in more alliance procurements.

In terms of centralized procurement strategies, companies need to thoroughly understand the rules and accurately assess pricing and reduction percentages. Looking at past cases, some companies have strategically lowered prices to gain larger market shares, while others have emphasized product advantages to secure price protection through separate groupings.

After centralized procurement, in the field of high-value interventional medical devices, how to achieve product synergy to boost sales across all categories is also crucial. Overall, companies still need to strengthen their foundational capabilities, leverage technological innovation platforms, develop innovative product solutions, reduce costs through manufacturing advantages, enhance sales and marketing efficiency, and accelerate the launch of innovative products in order to have greater room for success in centralized procurement.

Reference: Exploration of the Fifth Round of National Procurement Risks for Interventional Consumables and Corporate Bidding and Transformation Strategies —— IQVIA

Neurointervention Faces a Market of Over 20 Billion — Chinese Enterprises Are Ready to Take Off — CICC

Just Now! The Results of the 28 Categories of Consumables Centralized Procurement Announced, Over 70% of Products Eliminated… — Medical Device Dealers Alliance