On March 21, 2024, the World Health Organization updated the 2023 Global Vaccine Market Report.Although the report is more based on the content from 2022, it still holds reference value for understanding the current global vaccine market.The analysis excluded content related to the COVID-19 vaccine. After proofreading, organizing, supplementing details, and providing a brief analysis by the author, the main monitoring results are as follows:

Post-Pandemic EraVaccine production remains highly concentrated/01/ Market Size

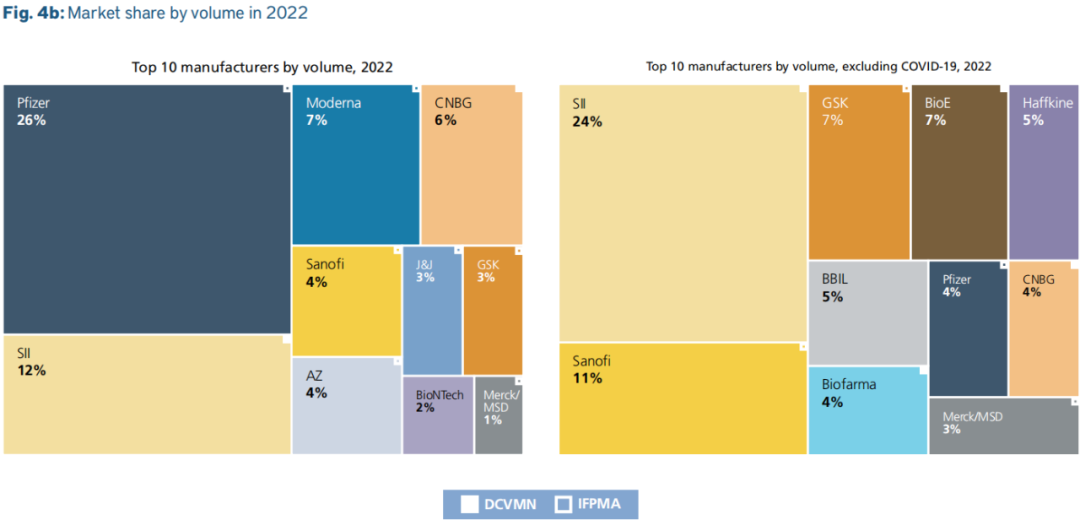

In 2022, the total global market supply of vaccines was approximately 5 billion doses (consistent with 2021 and pre-pandemic years). Vaccines with larger supplies included seasonal influenza, oral polio, and those containing diphtheria-tetanus components. In 2022, due to the advancement of measles catch-up campaigns in multiple European and American countries, the procurement volume of measles-rubella (MR) vaccines significantly increased.Ten manufacturers supply 75% of the world's vaccines and account for 85% of the global vaccine value.The remaining market is supplied by more than 80 other manufacturers.In terms of production and supply volume, the Serum Institute of India (SII) has become the world's largest vaccine manufacturer by producing and supplying 24% of the global vaccines with a low-price advantage.60% of the vaccines it produces are consumed in China, and a large portion is delivered to the African region, accounting for approximately 20% of India's exports. In 2023,SII has developed and successfully launched the domestically produced quadrivalent HPV vaccine (Cervavax) in China, and included the vaccine in the national immunization program with a competitive price advantage.

Among multinational pharmaceutical companies, Sanofi Pasteur ranks first by supplying 11% of the world's vaccines, with relatively high global shares in flu vaccines, IPV vaccines, Hib vaccines, and pentavalent vaccines.Next is GSK (7%). Apart from the relatively expensive shingles vaccine and the newly launched adjuvanted RSV vaccine (launched in 2023), meningitis vaccines, hepatitis B vaccines, hexavalent vaccines, and HPV vaccines also hold significant market shares globally.Pfizer and MSD account for 4% and 3% of the global vaccine supply, respectively, mainly due to their limited product types — Pfizer primarily relies on PCV13, while MSD mainly depends on quadrivalent/nonavalent HPV vaccines.The largest vaccine supplier in China is CNBG (4%)., as a state-owned institution,CNBGProduces the largest number of immunization program vaccines in China and also holds a position among suppliers of non-immunization program vaccines for children, such as influenza vaccine, varicella vaccine, EV71 vaccine, and oral rotavirus vaccine.Besides, Chinese manufacturers were unable to make it onto the list, indirectly reflecting —The overseas capabilities of Chinese vaccines need to be urgently improved. With the decline in birth rates, it is meaningless for domestic manufacturers to continue competing in the pediatric vaccine sector, which will only perpetuate the relative overcapacity. Adult vaccines, on the other hand, have relatively higher technical requirements, and currently, there are not many companies in China capable of developing high-value adult vaccines./02/ MarketOutput Value

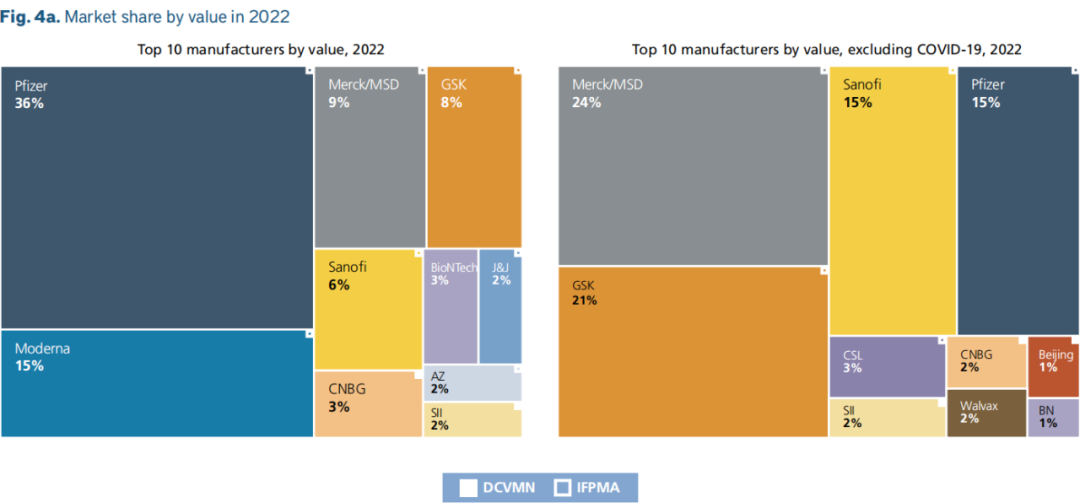

Vaccines produced by Merck, GSK, Sanofi, and Pfizer account for 65% of the global vaccine market.MSD/Merck has the highest global vaccine value share (24%), possibly mainly due to the strong sales of quadrivalent/nonavalent HPV vaccines in the Chinese market. Compared to its mere 3% share of the global vaccine supply, the primary reason for MSD’s vaccine value being at the top may be the enthusiasm of the Chinese market for the expensive nonavalent HPV vaccine.Although MSD also has inactivated hepatitis A vaccine, pentavalent oral rotavirus vaccine, 23-valent pneumococcal polysaccharide vaccine, etc., the price and market share are not relatively advantageous, and relying on these vaccines is not enough to elevate MSD to the top position.

Next is GSK, which relies on its unicorn product Shingrix (recombinant zoster vaccine) to make a significant impact globally. In 2023, GSK launched another blockbuster product, Arexvy (adjuvanted recombinant RSV vaccine), which is expected to generate over $1 billion in revenue in its first year.

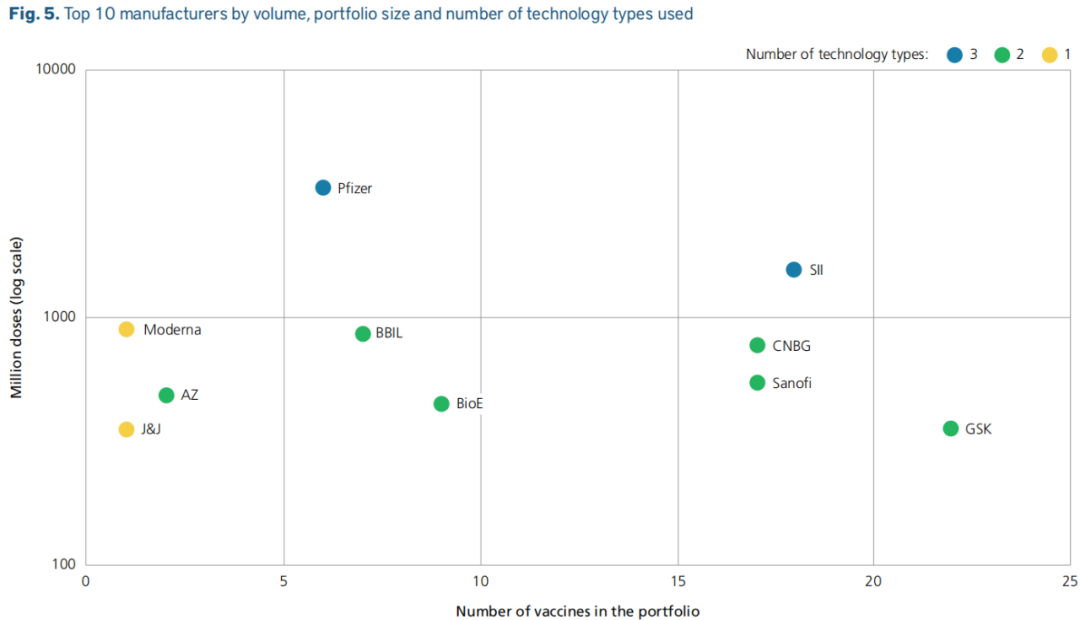

Sanofi and Pfizer are tied for 3rd place — Sanofi's flu vaccine and pentavalent vaccine, along with Pfizer's 13-valent pneumococcal vaccine, hold significant global market shares, which are key to the high vaccine output value of these two multinational manufacturers.In China, the state-owned enterprise Sinopharm Group and the private company Walvax Biotechnology have become the two leading enterprises with the highest output value. Taking Walvax Biotechnology as an example, the key to achieving this accomplishment lies in possessing two blockbuster products: the 13-valent pneumococcal vaccine and the bivalent HPV vaccine.New technology platforms have played an important role in expanding the production of COVID-19 vaccines. The current market relies heavily on nine manufacturers, which possess multiple vaccines and various vaccine technology platforms. In 2022, these vaccine manufacturers collectively accounted for approximately 70% of the global vaccine supply (excluding COVID-19 vaccines). Among them, four are located in the Americas and Europe, three manufacturers are in India, and one is in China (Sinopharm Group).

Types of Vaccine Demand and Growth Drivers

/01/ Vaccine Category

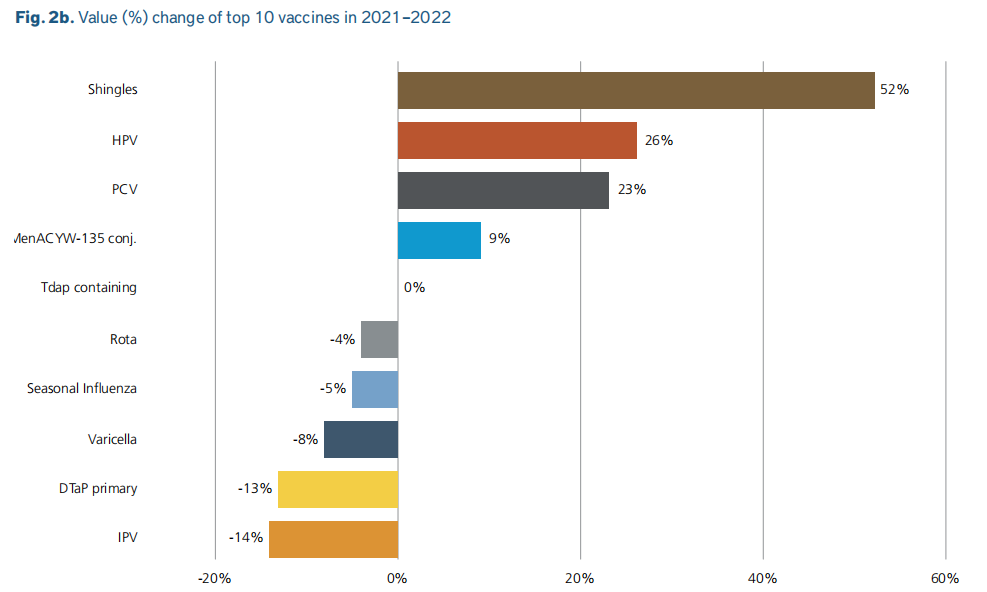

The value of global vaccines has continued to grow over the past four years, partly due to —— the increased use of high-value adult vaccines (which are usually more expensive, such as pneumococcal conjugate vaccines and herpes zoster vaccines for the elderly), andThe Rapid Growth of HPV Vaccine Demand Driven by China's Self-Pay Market。

The fastest-growing is the shingles vaccine, mainly attributed to the rapid growth of GSK's shingles vaccine Shingrix output value in the past few years, including in countries such as the UK, France, and Australia.Developed countries have replaced the attenuated herpes zoster vaccine, which has been used for many years, with a more potent and expensive recombinant herpes zoster vaccine., leading to an increase in global demand and total output value.

The increase in HPV vaccine is second only to the shingles vaccine, mainly due to the significant growth in China's self-paid market.: On one hand, developed countries have basically completed the EPI process, with relatively stable demand or even a decrease (such as the impact of the single-dose method); on the other hand, despite the rapid advancement of the expanded immunization process in low- and middle-income countries, the procurement price remains low under the tiered pricing mechanism. ("Tiered pricing mechanism" see below)From the above content, it can be seen that whenMany countries overseas have moved from "HPVVaccine Track"Switch to"WithHerpes Zoster Vaccine"While globally the focus is on the adult pneumococcal conjugate vaccine market, in China the emphasis remains on the HPV vaccine market."Stalemate”——Including the current R&D pipeline focusing on high-valent HPV vaccines, which indirectly reflectsChina may not have truly opened up the adult vaccine market situation./02/ Regional Population

Driven by the high price and high demand for vaccines in the U.S. market, the Americas region has the highest vaccine expenditure. This is followed by the Western Pacific region, where the demand is primarily driven by China — mainly due to the increased demand and vaccination rates for higher-priced vaccines such as the HPV vaccine and the 13-valent pneumococcal conjugate vaccine.Middle-income countries purchased 60% of the global vaccine supply, accounting for 34% of the total value, while high-income countries accounted for 29% of the global supply and 63% of the value. This value increase was driven by higher vaccine prices compared to other groups.Since the RSV vaccine was launched in mid-2023 and revenue data for this vaccine had not been obtained before the report was released, the report did not forecast the potential impact and growth drivers following the vaccine's market launch.

Vaccine Supply and Procurement

/01/ VaccineSupply Security

China’s self-funded vaccine market is still dominated by imports. The report pointed out that vaccines produced by Chinese manufacturers in 2022 accounted for only 13% of the total vaccine consumption value in China. Due to the decline in demand for COVID-19 vaccines in 2022,Significantly decreased compared to 2021 (13% vs. 30%)In addition, 60% of the vaccines produced by Chinese manufacturers are administered domestically, while the rest are exported to other countries or regions (including COVID-19 vaccines, mainly to other countries in the Western Pacific region).

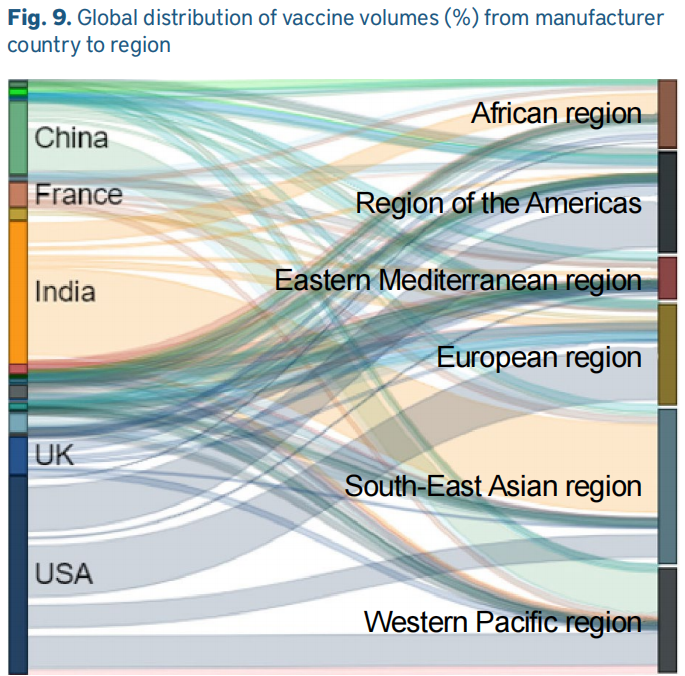

U.S. manufacturers produce 35% of the global procurement volume, mainly supplying the Americas, Southeast Asia, Europe, and the Western Pacific regions.Southeast Asia, with less than 10% of the global population, accounts for approximately 30% of global vaccine usage.The African region receives 12% of vaccines produced in other parts of the world but accounts for only 1% of global production./02/ Self-procurement and PricingGrading Mechanism

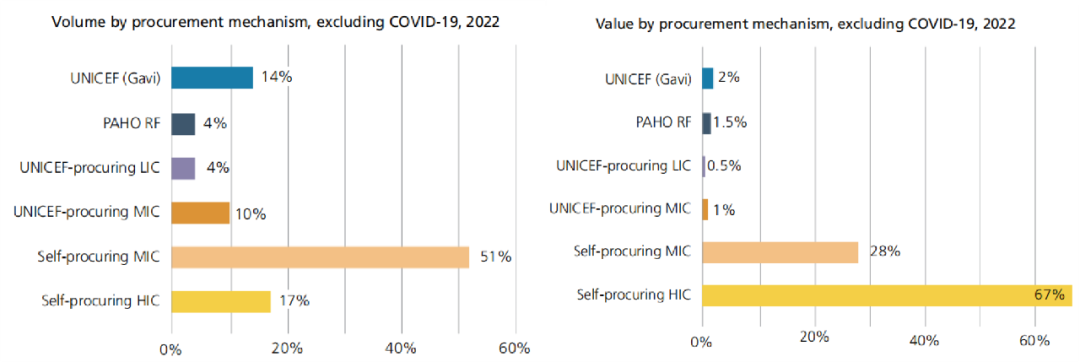

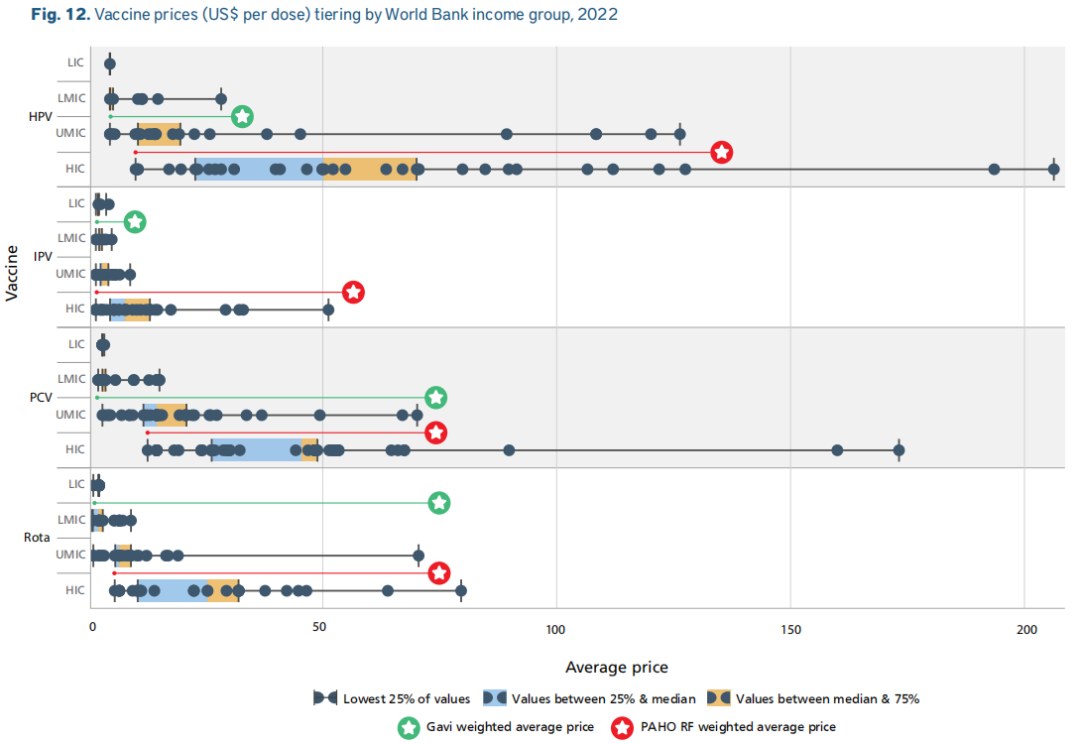

Due to the imbalance in economic development, a tiered mechanism for vaccine procurement prices has been implemented under the efforts of international organizations such as the United Nations, WHO, and Gavi — procurement prices are determined based on income levels.In terms of procurement mechanisms, middle-income and high-income countries almost always procure vaccines independently within their own countries. These procurements account for approximately 75% of the market in volume and around 90% in value. Centralized procurement mechanisms, such as those by UNICEF and the Pan American Health Organization (PAHO), account for the remaining 25% in volume and 10% in value, respectively. Compared with other procurement types, UNICEF and PAHO’s price tiering mechanisms have saved significant costs. For example, the cost of HPV vaccines procured through PAHO in 2022 was approximately $10 per dose, while the average price for procurement by middle- and high-income countries was between $21 and $67. Similar conclusions can be drawn for key vaccines such as PCV and Rotavirus (Rota). Significant price differences also exist between income groups for vaccines like Tetanus, Diphtheria (100 times), Hepatitis B (25 times), HPV (18 times), PCV (17 times), and Rotavirus (15 times).

Compared with other procurement types, UNICEF and PAHO’s price tiering mechanisms have saved significant costs. For example, the cost of HPV vaccines procured through PAHO in 2022 was approximately $10 per dose, while the average price for procurement by middle- and high-income countries was between $21 and $67. Similar conclusions can be drawn for key vaccines such as PCV and Rotavirus (Rota). Significant price differences also exist between income groups for vaccines like Tetanus, Diphtheria (100 times), Hepatitis B (25 times), HPV (18 times), PCV (17 times), and Rotavirus (15 times). Although low- and middle-income countries benefit from the vaccine price classification mechanism to purchase vaccines at low prices, upper-middle-income countriesThe price of vaccines paid in China is usually equivalent to or higher than that in high-income countries. As one of the upper-middle-income countries (as defined by the World Bank), the prices of some vaccines in China are basically the same as those in developed countries in Europe and the United States. For example, the procurement prices of HPV vaccines in upper-middle-income countries (UMIC) overlap significantly with those in high-income countries (HIC).

Although low- and middle-income countries benefit from the vaccine price classification mechanism to purchase vaccines at low prices, upper-middle-income countriesThe price of vaccines paid in China is usually equivalent to or higher than that in high-income countries. As one of the upper-middle-income countries (as defined by the World Bank), the prices of some vaccines in China are basically the same as those in developed countries in Europe and the United States. For example, the procurement prices of HPV vaccines in upper-middle-income countries (UMIC) overlap significantly with those in high-income countries (HIC).

Crises and Issues

Unequal Vaccine Distribution——The total vaccine usage in the African region increased from 8% in 2021 to 12%. However, prior to COVID-19, Africa's vaccine usage typically accounted for about 20% of the global share — this may indicate that the consumption of COVID-19 vaccines in the region during the pandemic was relatively low, indirectly reflecting the inequity in global vaccine distribution.Moreover, over 90% of the regional consumption in the Eastern Mediterranean Region relies on imported vaccines from vaccine manufacturers in other countries.Measles Unabated, Cholera on the Rise——In 2023, despite the efforts of the measles vaccine "strong immunity," as of July 2023, 116 out of 195 countries had still not returned to pre-pandemic performance. At the same time, cases of cholera (a Class A infectious disease in China) have risen again after decades of fighting the disease, with an increase even in countries where it has not been seen for years — 35 countries reported cases in 2021, growing to 44 countries in 2022. This trend continued into 2023 and was exacerbated by a severe shortage of oral cholera vaccines and subsequent changes.Growth in the adult vaccine market is limited——Despite COVID-19 VaccinesA Milestone Event in Promoting Adult Vaccination, but the adult vaccination platform is still a frontier area for many countries. Excluding COVID-19 vaccines, less than 10% of adult vaccines are supplied to low-income countries, while the figure is 51% for high-income countries.The adult vaccine market in China is still in its infancy. According to domestic research data, the coverage rate of the popular HPV vaccine is only about 15-20%, and the vaccination rate for the flu vaccine is only around 5-10%. The vaccination rates for adult vaccines such as the shingles vaccine, pneumococcal polysaccharide vaccine, and hepatitis E vaccine are even lower.

Future Trends Based on Reports and AI Predictions

Based on the report content and AI knowledge base, several potential trends in the global vaccine market were predicted:

- Technological Advancements and Innovation:With the development of new technology platforms, such as mRNA technology, it is expected that more vaccines will be rapidly developed and brought to market, especially in response to emerging and re-emerging diseases.

- Regionalization of the Supply Chain:Affected by the disruption of global supply chains during the COVID-19 pandemic, regions may push to enhance local and regional production capabilities to reduce reliance on external suppliers.

- Price ComponentLevelAffordability: It is expected that the price differences for vaccines between different income groups will continue, but there may be more efforts to reduce such disparities and improve vaccine affordability, especially in middle-income countries.

- Growth of the Adult Vaccine Market: With the aging population and increasing awareness of preventive care for adult diseases, the adult vaccine market may experience significant growth.

- Global Cooperation and Public Health Security: The experience of the pandemic has highlighted the importance of global cooperation, and it is expected that there will be more international agreements and cooperation mechanisms in the future to address global public health emergencies.

- Digital Health and Vaccine Tracking: The application of digital technologies, such as blockchain and digital tracking systems, may play a larger role in the vaccine market to ensure vaccine traceability and reduce the risk of counterfeit and substandard vaccines.

- Equity in Vaccine Distribution: The equity of global vaccine distribution will become a significant issue, particularly in enhancing the accessibility of vaccines in low- and middle-income countries.

- Impact of Environment and Climate ChangeClimate change may affect the pattern of vaccine demand, for example, by altering the geographical scope of disease transmission, which may lead to an increase in market demand for certain vaccines.

- Changes in Policy and Regulatory Environment: With the global increase in awareness of vaccine importance, new policies and regulatory measures may emerge to support vaccine development, approval, and distribution.

- Increase in Public Health Investment: It is expected that there will be a global increase in investment in public health infrastructure, including vaccination programs, to enhance preparedness and response capabilities for future epidemics.

Reference link:https://www.who.int/publications/m/item/global-vaccine-market-report-2023

Scan the WeChat QR code, add the editor of the Biological Products Circle, and those who meet the requirements can join.

Biological Products WeChat Group!

Please indicate: Name + Research Direction!All articles reproduced in this official account are intended to convey more information, with the source and author clearly stated. Media or individuals who do not wish to be reprinted can contact us (cbplib@163.com), and we will immediately delete the content. All articles represent the views of the author and do not represent the position of this website.