Source of the article: Elephant IPO

On March 15, the CSRC released five major policy documents. These documents clearly focus on improving the quality of listed companies by studying the enhancement of financial listing criteria, optimizing sector positioning rules, and providing the market with higher-quality and more diverse investment options.Further tighten the review of unprofitable enterprises, requiring them to fully demonstrate their ability to sustain operations and disclose forecasts.To calculate the profitability, listen to the opinions of relevant industry departments on a case-by-case basis regarding scientific and technological innovation attributes.

This means that companies applying for the fifth set of listing standards on the Sci-Tech Innovation Board, as well as those under review or with intentions, are facing new uncertainties, making it more difficult to go public.Previously, there have been signs that the review of the fifth set of standards for the Sci-Tech Innovation Board has tightened. In 2023, only one company, Zhi Xiang Jin Tai, went public under the fifth set of standards, significantly lower than the eight companies in 2022 (Ya Hong Medicine, Mai Wei Bio, Shou Yao Holdings, Rong Chang Bio, Hai Chuang Pharma, Yi Fang Bio, Meng Ke Pharma, and MicroPort EP), and as of 2024, none have yet.Listed on the Fifth Set of Standards of the Sci-Tech Innovation BoardEnterprise.As of now, only 8 enterprises remain in the queue for review after submitting their listing applications under the Fifth Set of Standards.Status of 8 Companies Under Review

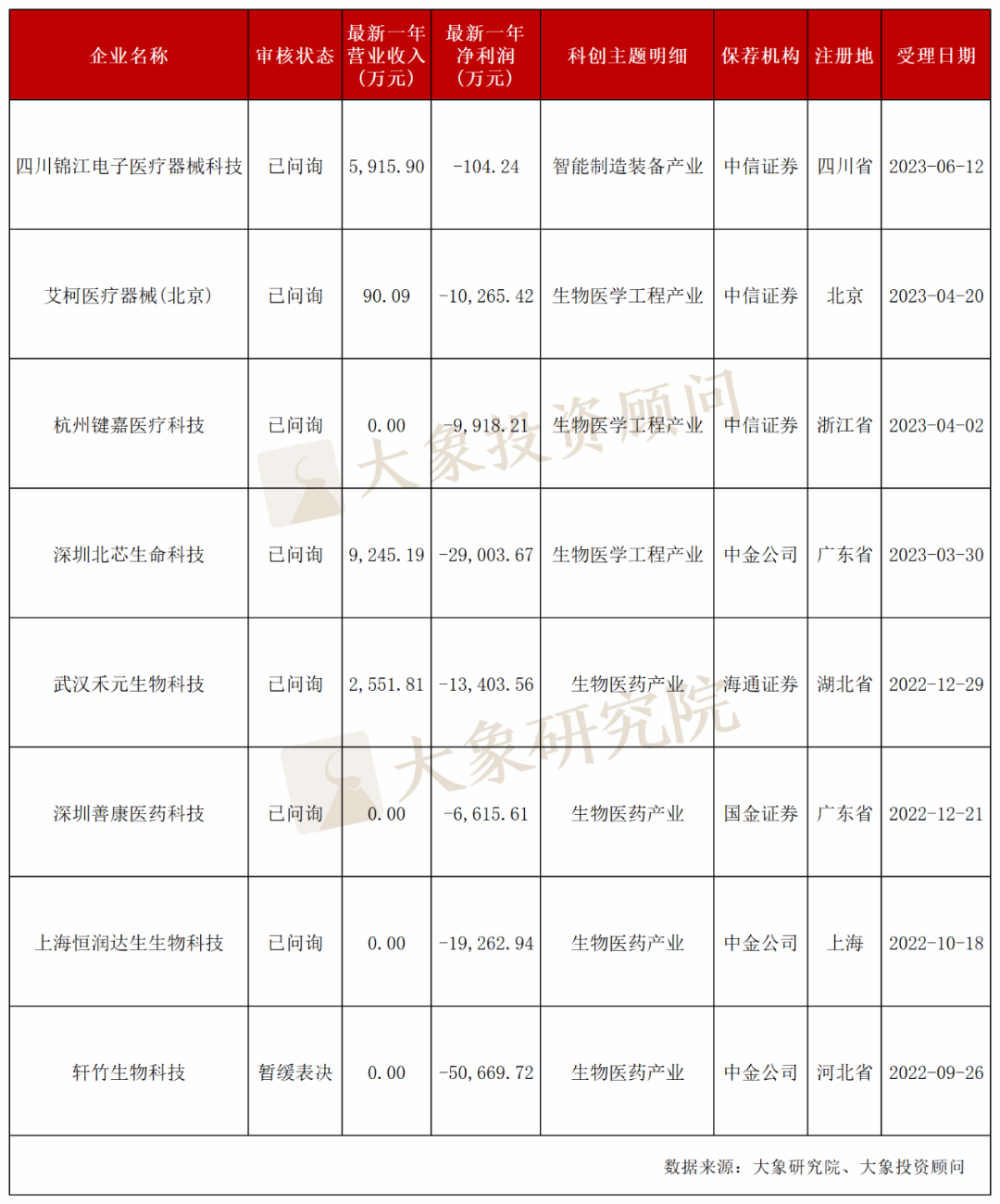

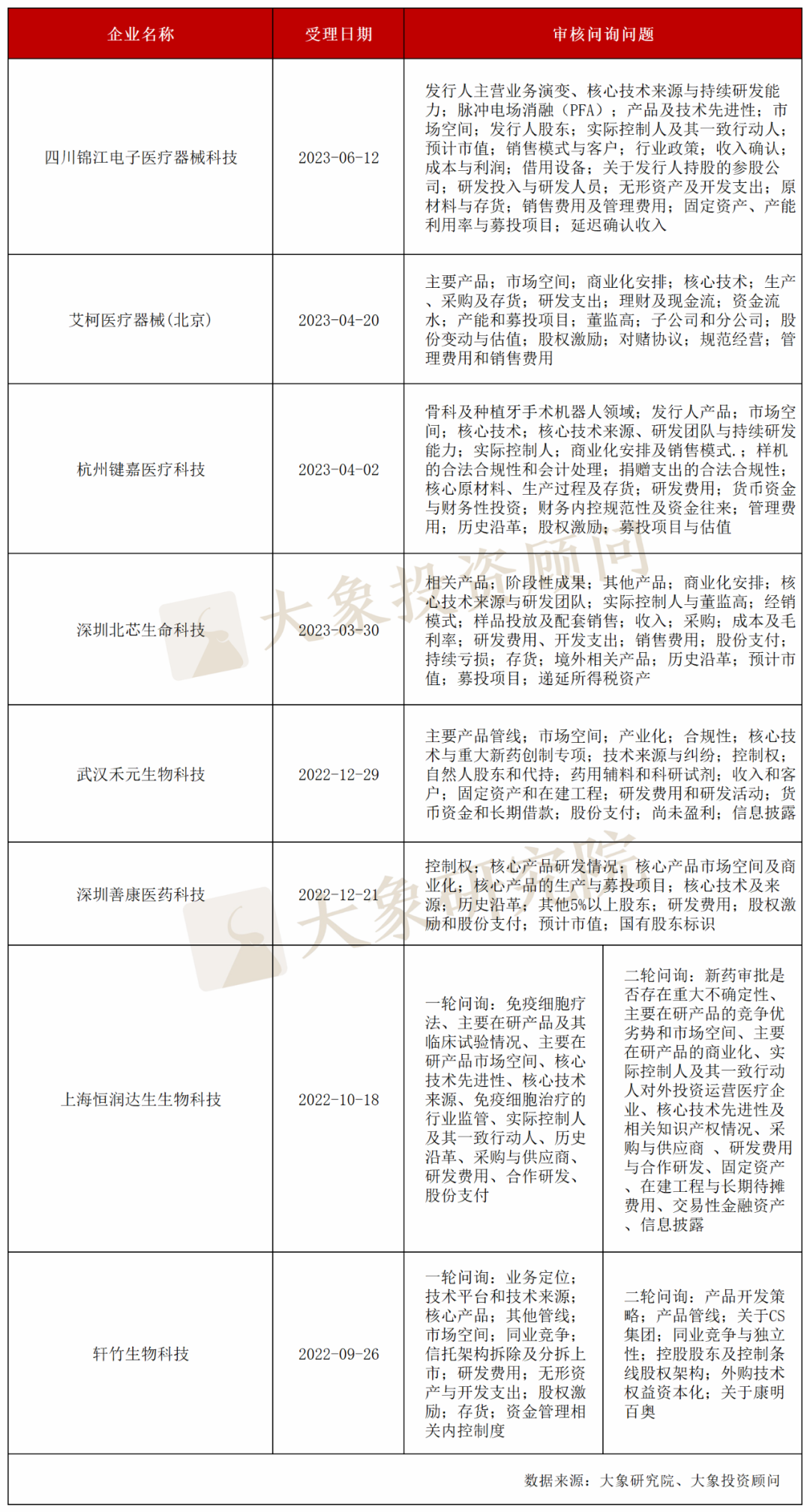

According to the information gathered by Elephants, as of now,STAR MarketOnly 8 companies remain in the queue for listing applications under the fifth set of standards, with 7 in the status of "questioned" and 1 postponed. The specific situation is as follows:1、Details of Sci-Tech Innovation ThemesAdopted by 8 companiesSTAR MarketRegarding the detailed situation of the theme of the STAR Market for the fifth set of standards for listed companies under review, four are in the biopharmaceutical industry, three are in the biomedical engineering industry, and one is in the intelligent manufacturing equipment industry.2. Distribution of Registration LocationsEight companies adopting the fifth set of STAR Market standards for listingIn China, there are 2 in Guangdong, and 1 each in Beijing, Hebei, Hubei, Shanghai, Sichuan, and Zhejiang.3. From the perspective of the sponsor institution,From 8 companies adopting the fifth set of STAR Market standards for listingFrom the perspective of sponsors, there are 3 from CICC, 3 from CITIC Securities, and 1 each from Guojin Securities and Haitong Securities.4. From the perspective of corporate review and inquiry issuesSix out of eight companies adopting the fifth set of STAR Market standards for listing have undergone one round of inquiries and responses, while two have experienced two rounds of inquiries and responses, among which,The exchange focuses on the core technology, core products, market space, commercial arrangements, estimated market value, R&D expenses, cash flow, fundraising projects, equity incentives, historical evolution, and other issues of enterprises., The specific situation is as follows:5. Enterprise Specifics

(1) Sichuan Jinjiang Electronic Medical Device Science and Technology Co., Ltd.

Jinjiang Electronic is an innovative enterprise that focuses on the research, development, production, and sales of high-end innovative medical devices for diagnosis and ablation in the field of cardiac electrophysiology. The quality and performance of its core products fully match those of international leaders. With over two decades of deep cultivation in the cardiac electrophysiology field, the company has a profound understanding of bioelectrical signals and a strong foundation in electronic engineering, providing safe and efficient comprehensive treatment solutions for patients with rapid arrhythmia worldwide.On December 28, 2023, the National Medical Products Administration announced the official approval of Jinjiang Electronic's "PulsedFA Disposable Cardiac Pulse Field Ablation Catheter" and "LEAD PFA Cardiac Pulse Field Ablation System" for innovative product registration, marking the first cardiac PFA-type products approved in China.According to the filing materials, from 2020 to the first half of 2023, Jinjiang Electronic's revenue was 41.339 million yuan, 60.6159 million yuan, 59.159 million yuan, and 39.4197 million yuan, respectively; the net profit attributable to parent company was 24.7252 million yuan, -16.5897 million yuan, -1.0424 million yuan, and -40.1691 million yuan, respectively.The company's losses in the first half of 2023 were quite significant.Jinjiang Electronic explained that in 2021, the company increased its R&D investment; in 2022, it expanded its sales channels, resulting in a significant increase in sales expenses; in the first half of 2023, the company recorded a large amount of share-based compensation and won the centralized procurement bid for consumable products, entering a product transition period.Jinjiang Electronic stated in its latest response that it is expected to turn a profit in 2025. However, considering the continued investment in research and development and sales expenses, as well as uncertainties in the future market, there is still an anticipated risk of ongoing losses.(2) Aikang Medical Devices (Beijing) Co., Ltd.

The issuer is an innovative medical device enterprise that has entered the commercialization stage and focuses on the field of neurointervention.It is reported that the company, based on the unmet clinical needs and huge market potential in the field of cerebrovascular diseases, has built a full product line layout for neurointervention, leading the innovative development in the field of neurointerventional therapy.As of the date of signing the prospectus, the company's three core innovative medical device products—the Lattice flow diverter stent, Cosine71/58 distal access catheter, and Sine27 microcatheter—have obtained Class III medical device registration certificates and have been commercialized. Additionally, four products are in the registration stage, and several other products are in clinical or preclinical stages.Research and Development Stage.From 2020 to 2022, Aikang Medical achieved revenues of 0 respectively.Yuan、0YuanAnd 90.09 million yuan, the net profit attributable to the parent company was -35.7244 million yuan, -89.4501 million yuan, and -103 million yuan, respectively.The company stated that the main reasons for the continuous losses are, on the one hand, that since its establishment, the issuer has been engaged in the research and development of innovative medical devices, which have long R&D cycles and require continuous investment before commercialization. The R&D investment during the reporting period was substantial; on the other hand, the issuer's core products, such as the Lattice flow diverter stent and other neurointerventional medical devices, were successively approved in 2022 and began generating sales revenue starting from December 2022. These products are still in the early stages of commercialization, resulting in a small scale of operating revenue.It is reported that in the first half of 2023, Aikang Medical's net profit attributable to parent company was -317 million yuan, and the net profit attributable to parent company after deducting non-recurring gains and losses was -77.5791 million yuan. As of the first half of 2023, the company's undistributed profit was -400 million yuan.In the reply to the review inquiry letter, Aikang Medical introduced that the company achieved main business revenue of 891,500 yuan in 2022 and 37,289,100 yuan from January to June 2023. With the increase in the incidence of cerebrovascular diseases due to the aggravation of aging, the construction of stroke centers, the promotion of stroke prevention and treatment which enhances the penetration rate of neurointerventional surgeries, as well as policy support for domestically produced medical consumables, it is expected that the market for neurointerventional medical devices will maintain rapid growth in the future. Based on a comprehensive assessment of industry prospects, and considering factors such as the company’s business development plan and industry outlook, it is projected that the company's revenue scale will maintain a relatively high growth rate from 2023 to 2024. It is estimated that by 2024, when the company reaches the break-even point, its annual revenue will be approximately 207 million yuan, with a net profit of 3 million yuan.(3) Hangzhou Jianjia Medical Technology Co., Ltd.

The company is a high-tech enterprise focusing on the research, development, production, and sales of surgical robots and related products. It is committed to building a technologically advanced surgical robot platform, providing hospitals with safe, precise, and intelligent surgical solutions.

During the period from 2019 to 2021 and January to September 2022 (hereinafter referred to as the "reporting period"), the company's revenue was 106,800 yuan, 291,300 yuan, 0 yuan, and 0 yuan, respectively.Owned by MotherNet profits were -RMB 32.2809 million, -RMB 49.9192 million, -RMB 99.1821 million, and -RMB 277 million, respectively, with cumulative losses exceeding RMB 458 million.

Continuous losses have brought significant financial pressure to Jianjia Medical. From 2019 to 2021 and January to September 2022, the net cash flow generated from the company’s operating activities was -9.091 million yuan, -39.2418 million yuan, -70.24 million yuan, and -116 million yuan respectively, accumulating to -234 million yuan. The company has been in a continuous state of cash outflow, with the cash flow gap continuously widening.Jianjia Medical admitted that before the successful listing, the company's operating funds mainly relied on external financing. If the expenditures required for operational development exceed the available external financing, it will put pressure on the company's financial situation.(4) Shenzhen Beixins Life Technology Co., Ltd.

The company is a national high-tech enterprise focusing on the research, development, production, and sales of innovative medical devices for precision diagnosis and treatment of cardiovascular diseases. It is committed to developing precise solutions that bring transformative changes to the diagnosis and treatment of cardiovascular diseases.

The company's core product, the intravascular ultrasound (IVUS) diagnostic system, is China's first self-innovated 60MHz high-definition high-speed IVUS product approved by the National Medical Products Administration (NMPA). The core product, the fractional flow reserve (FFR) measurement system, is the first domestically produced product in China to be approved by the NMPA in the gold-standard FFR field. Both of these products have entered the special review process for innovative medical devices in China and are expected to bring about a transformation in the clinical practice of precisely guiding percutaneous coronary intervention (PCI) surgeries.

Data shows that from 2020 to the first half of 2023, the operating revenue of Northcore Life was 1.6746 million yuan, 51.7621 million yuan, 92.4519 million yuan, and 92.8794 million yuan, respectively; the net profit attributable to parent company for the same period was -49.8453 million yuan, -4.45 billion yuan, -2.90 billion yuan, and -62.3462 million yuan. As of June 30, 2023, the accumulated uncompensated loss at the consolidated level of the company was -6.15 billion yuan, with a balance sheet ratio of 14.47%.Although the company's revenue continues to grow, its net profit remains in a persistent loss. The stock exchange has required the company to disclose its accumulated uncompensated losses and their causes, and to explain whether the fact that the company has not yet turned a profit and has large accumulated losses in the most recent period affects its ability to continue as a going concern.In response, Northcore Life explained that this was mainly due to the company still being in the early stages of commercialization. During the reporting period, the company's main revenue came from its first marketed product, the FF system, and the revenue scale was relatively small, which was not yet sufficient to cover the company’s daily operating costs and various expenses.As of June 30 this year, the accumulated uncompensated losses at the company's consolidated level amounted to -615 million yuan. After a certain period of development, the company is highly likely to reduce its losses or even achieve profitability. The company stated that its current cash funds are sufficient to meet operational needs for a predictable period in the future, and the substantial accumulated losses as of the latest period will not affect its ability to continue as a going concern.

(5) Wuhan Heli Biotechnology Co., Ltd.Heyuan Biotechnology is an innovative biopharmaceutical company that owns a globally leading plant bioreactor technology platform. The company has established a core technology system of "one unique plant expression system, two technical platforms": using the rice endosperm cell bioreactor for efficient recombinant protein expression platform (OryzHiExp) and the recombinant protein purification technology platform (OryzPur), forming a complete industrialization system for pharmaceuticals, pharmaceutical excipients, and research reagents.However, Heyuan Bio, established in 2006, has insufficient R&D capabilities. More than 10 years later, its core products are still in the research and development stage and have not yet been commercialized.Because of this, Heryuan Biotechnology has been mired in losses.From the first half of 2019 to 2022, Heyuan Bio's operating revenues were RMB 10.25 million, RMB 21.5659 million, RMB 25.5181 million, and RMB 6.0496 million respectively; during the same periodNet profit attributable to母公司分别为-49.9357 million yuan, 53.3516 million yuan, -134 million yuan, and -58.2987 million yuan. Accumulated losses of nearly 300 million yuan in just three and a half years.Heyuan Bio's financial data shows a declining trend in revenue and net profit over the past few years, raising concerns about its future profitability. The company has opted for the STAR Market listing standards; however, its core products have yet to enter the commercial sales stage, and it has been in a long-term loss-making state, relying on continuous financing for support. Its dispersed equity structure and decreasing stability make the reasonableness of its valuation questionable.(6) Shenzhen Shankang Pharmaceutical Technology Co., Ltd.The company is mainly engaged in the research, development, production, and sales of innovative drugs for addiction treatment, such as preventing opioid relapse and treating alcohol use disorder. It is an international innovative drug R&D enterprise with independent intellectual property rights and a global perspective, committed to creating a "Chinese solution" for addiction treatment.The core product of Shangkang Pharmaceutical is naltrexone implant, which is used to prevent relapse in detoxified opioid addicts and treat alcohol use disorder. SK1801 Naltrexone Implant has currently reached the New Drug Application (NDA) stage; SK2007 Naltrexone Implant received approval for Phase II clinical trial in August 2022. It is expected that this product will complete Phase III clinical trial and submit a drug marketing registration application by 2025, and be launched within 2026.Due to the companyCore products have not been launched yet.City sales, the company has been in a loss state. From 2019 to June 2022, the company's operating income was respectively$0, $0, $0, $0; The net profit attributable to the parent company for the same period was -30.2978 million yuan, -33.2313 million yuan, -66.1561 million yuan, and -47.6798 million yuan, respectively. During the reporting period, Shangkang Medicine reported a total loss of approximately 177 million yuan.As ShanKang Pharma has no products on the market yet and is in the stage of new drug development, its continuous increase in R&D investment has led to a persistently negative net cash flow from operating activities during the reporting period.From January 2019 to June 2022, the net cash flow from operating activities of Shangkang Pharmaceutical was -18.7752 million yuan, -27.5205 million yuan, -51.3022 million yuan, and -32.3432 million yuan, respectively.(7) Shanghai Hengrun Dason Biotechnology Co., Ltd.The company is an innovative biopharmaceutical company focused on the research and production of breakthrough immunotherapy products, primarily targeting treatment areas such as malignant hematological diseases and solid tumors.As of the date of this prospectus, the company has formed a pipeline layout for products in various stages from early research and development to mature clinical trials, and is currently conducting 11 research projects corresponding to 10 major products, including CAR-T, CAR-NK and other technologies.Hengrun Dason Lacks Core Products and Revenue Sources. During the past reporting period, the company failed to submit a new drug marketing application and had no products on the market for sale, with almost zero main business revenue. Meanwhile, the current situation of consecutive losses cannot be ignored, with a loss as high as 193 million yuan in 2021.From 2019 to June 2022, the companyAchieved operating revenue of 194,700 yuan, 0 yuan, 0 yuan, and 0 yuan respectively; net profit attributable to parent company was -117 million yuan, -103 million yuan, -193 million yuan respectively during the same period.-117 million yuan.The company is under pressure to turn a profit in the short term. In terms of revenue, the progress of the company's products has been delayed, and it is expected that only two products will be approved for marketing in the short term. In a highly competitive market environment, if there is no significant price advantage, Hengrun Dason faces the challenge of capturing market share from Yikaida and Benoda. At the same time, the company’s research and development and sales expenses are enormous, requiring substantial financial support, which could pose a significant challenge to profitability.(8) Xuanzhu Biotechnology Co., Ltd.The company is an innovative pharmaceutical enterprise rooted in China with a global perspective, focusing on major disease areas such as gastroenterology, oncology, and non-alcoholic steatohepatitis (NASH). It is committed to the continuous development and commercialization of Class 1 new drugs with core independent intellectual property rights to address unmet clinical treatment needs. The company possesses two major R&D systems for small-molecule chemical drugs and large-molecule biologics, driving innovation through a dual-engine approach. This has resulted in a product pipeline that encompasses various types of drugs, including small-molecule chemical drugs, monoclonal antibodies, bispecific antibodies, and antibody-drug conjugates — a rare combination in China.Since none of the products have been launched, during the reporting period (January 2019 to September 2022), Xuanzhu Biotech's operating revenue was 0 yuan, and its attributable net profit was -3.62 billion yuan, -1.62 billion yuan, -4.62 billion yuan, and -3.97 billion yuan, respectively.As of the end of September 2022, Xuanzhu Biotech's accumulated undistributed profit was -1.108 billion yuan.The prospectus also shows,In 2022, the company's audited net profit attributable to parent company shareholders was -5.07 billion yuan, and the net profit attributable to parent company shareholders excluding non-recurring gains and losses was -4.93 billion yuan. The net cash flow generated from operating activities was -3.86 billion yuan.In other words, over four years, Axsome Bio has accumulated losses of nearly 1.5 billion yuan.Xuanzhu Biotech stated in the prospectus that the company is still in the product research and development stage, with high R&D expenditures. No drugs have received commercial sales approval, and no drug sales revenue has been generated. The company will not be profitable or able to distribute profits for a certain period in the future, and it may never become profitable.At the same time, Xuanzhu Biotech also emphasized that even if the company is able to become profitable in the future, it may not be able to maintain continuous profitability. It is expected that after the initial public offering and listing, the issuer will not be able to distribute cash dividends in the short term, which will have a certain degree of adverse impact on shareholders' investment returns.On March 8, 2023, Xuanzhu Bio's meeting was postponed.At the review meeting, the Listing Committee focused on inquiring about the technical advantages of its R&D products, the market space for major products, and the advantages of commercialization planning, among other issues.

Actually, last year "827"After the policy, there were no more unprofitable companies listed on the STAR Market until this year."315”New PolicyExplicitly propose strict scrutiny of unprofitable enterprises, requiring such enterprises to fully demonstrate their ongoing operational capabilities and disclose projected profitability. Additionally, opinions from relevant industry departments should be obtained on a case-by-case basis regarding attributes such as technological innovation.

Not ProfitableCompanies can go public, but not all of them. The futureNot ProfitableWhen enterprises apply for IPO, the focus will be on their ability to sustain operations. The capital market is investor-oriented, allowing a broad range of investors to gain returns and a sense of achievement; profitability naturally becomes a key indicator.

At the same time, the market also bears the responsibility of supporting the growth and development of the technology industry. This is especially true for the STAR Market, which plays a crucial role in driving technological innovation.It is one of the core propositions, and the issue of scientific and technological innovation attributes has naturally become a focus of regulatory attention; therefore, unprofitable enterprises are paying close attention to core technical capabilities and R&D capabilities.

It can be foreseen that after the "315" new policy, it will become more difficult for unprofitable companies to go public. Unprofitable companies planning to冲刺IPO need to be fully prepared and standardize themselves according to the requirements for unprofitable companies under the new policy.If a company has a solid scientific research foundation and secures funding through an IPO, it can achieve leapfrog development and become a high-quality investment target. Of course, if an unprofitable company lacks sufficient technological strength, going public carries risks.

Disclaimer: This article is intended solely for the purpose of information transmission and is for reference only. It does not constitute any advice on investment or treatment. Please exercise caution in distinguishing the information. If it involves issues related to the content, copyright, or other aspects of the work, to protect the rights and interests of both parties, please contact us, and we will handle it immediately. If any platform reprints this article, it must take responsibility for the content of the article. The Medical Device Innovation Network is not responsible for any secondary dissemination caused by reprints.