Domestic Blockbuster Drug Soars in Sales, Yet Investors Remain Cautious

Legend Biotech

Tumor Cell Immunotherapy Developer

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

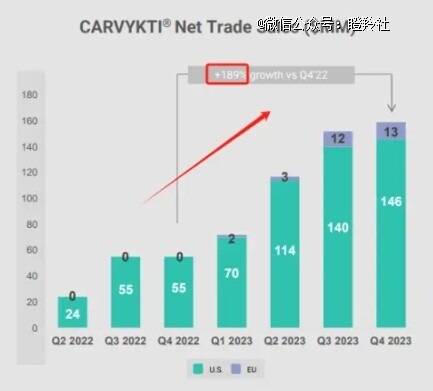

On the evening of April 16, Johnson & Johnson's Q1 2024 earnings report indicated: CARVYKTI, developed in collaboration with Legend Biotech, generated approximately US$157 million in net trade sales during the quarter.

Compared with the revenue of $72 million in Q1 2023, this quarter's year-on-year growth reached 118%, achieving more than double growth both in the United States and internationally.

Such a year-on-year high growth performance data seems to be not "bought" by investors both in and outside China, with Legend Biotech's US stock and its parent company Genscript Biotech's Hong Kong stock falling 3.07% and 1.2%, respectively, in the most recent trading session.

The issue may lie in the quarter-on-quarter data: compared to the revenue of $146 million in Q4 2023, the $157 million in Q1 2024 represents a mere 7.53% growth. It is important to note that the sales ramp-up of CARVYKTI, developed by Johnson & Johnson/Legend Biotech, has consistently been constrained by production capacity. In April 2023, a CMO agreement was signed with Novartis to address production bottlenecks, but the subsequent increase in output did not meet market expectations in terms of speed. In April this year, Johnson & Johnson/Legend Biotech once again signed an agreement with Novartis to expand production, underscoring the urgency of resolving supply constraints.

Although the quarter-on-quarter growth of CARVYKTI in the short term has not been as rapid as investors expected, it is still reasonable to anticipate that CARVYKTI will achieve $1 billion in sales within the year. A longer-term perspective is needed to assess CARVYKTI's sales ramp-up.

01

Capacity bottleneck to be resolved soon

According to reports, since the beginning of 2023, the production capacity of CARVYKTI has expanded by 100%. Johnson & Johnson and Legend Biotech are expected to achieve an annual production capacity of 10,000 doses by the end of 2025, which could support a sales peak of 5 billion US dollars.

In 2023, CARVYKTI's total annual sales reached 500 million US dollars. Can it be linearly inferred that the company sold just over 1,000 doses of CARVYKTI?

It should be noted that autologous cell therapy is strongly characterized by regionalized production and treatment. For instance, if the treatment is conducted in Europe, it would require localized facilities within Europe for preparation and supply. It is unlikely that products manufactured in China could be transported to Europe due to time or cost constraints.

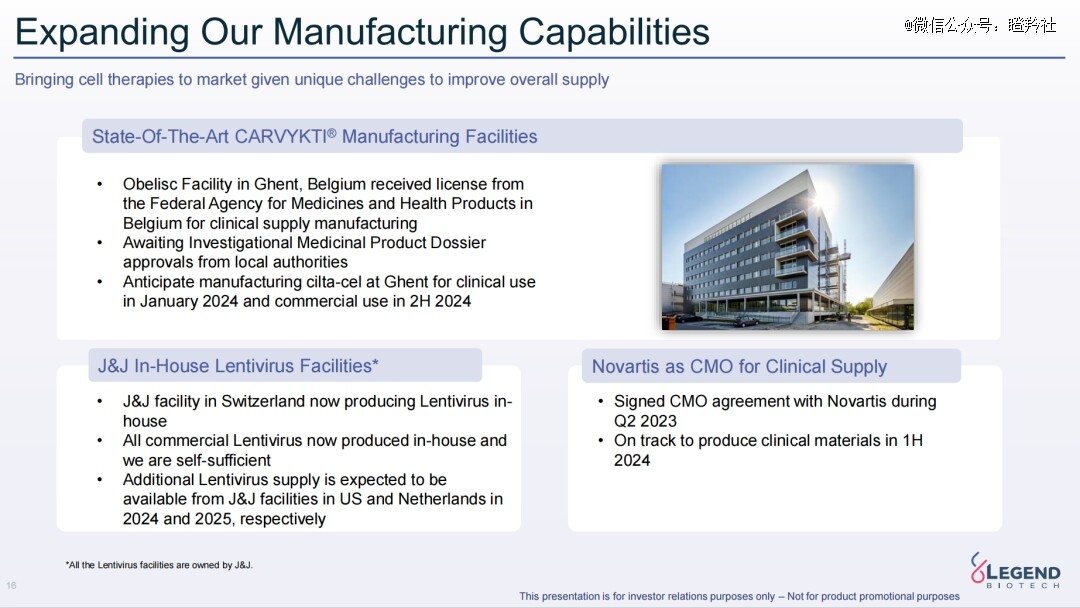

Currently, Johnson & Johnson/Legend Biotech has production capacity in New Jersey, USA; Ghent, Belgium; and Nanjing, China. The New Jersey, USA facility supplies all commercial products of CARVYKTI (in October 2022, the company doubled its investment in this facility to $500 million). The Ghent, Belgium facility began clinical production in January 2024 and will commence commercial production in the second half of 2024. In China, there are two facilities in Nanjing: one is GMP-ready, while the other is still under construction.

Moreover, Legend Biotech's management mentioned two major factors limiting the production capacity of BCMA CAR-T products earlier: the shortage of lentiviral vector supply and the issue with the CAR sequence slot.

At the beginning of the year, the FDA approved Johnson & Johnson's Swiss plant, which is a large reactor for producing lentivirus. In the future, the company will be able to achieve self-sufficiency in lentiviral vectors and will no longer be limited by their supply. In addition, Johnson & Johnson’s plant in the Netherlands, Europe, is under construction and will support the lentivirus supply for CARVYKTI within the year.

As for the cooperation with Novartis, Novartis will provide actual clinical production materials in the first half of 2024.

In this case, with the release of production capacity from European plants in Belgium, Switzerland, and the Netherlands, CARVYKTI's market potential in Europe is expected to be unlocked (currently, only around or less than $16 million in sales for 2024 Q1 came from the European market). Meanwhile, with the official entry of its partner Novartis into the U.S. market, rapid volume expansion is also anticipated.

Therefore, it is predicted that the second half of 2024 could be a critical period for the accelerated increase in CARVYKTI's sales volume, at which time close attention can be paid to the quarter-on-quarter data.

02

FDA Approval Opens Space for Second-Line MM Treatment

Where does the demand come from? The patient population suitable for CARVYKTI is expanding.

In early April, the FDA approved CARVYKTI for the treatment of patients with relapsed or refractory multiple myeloma (RRMM). CARVYKTI is also currently the *only* targeted BCMA therapy approved for second-line treatment of RRMM, including CAR-T therapy, bispecific antibodies, and ADCs.

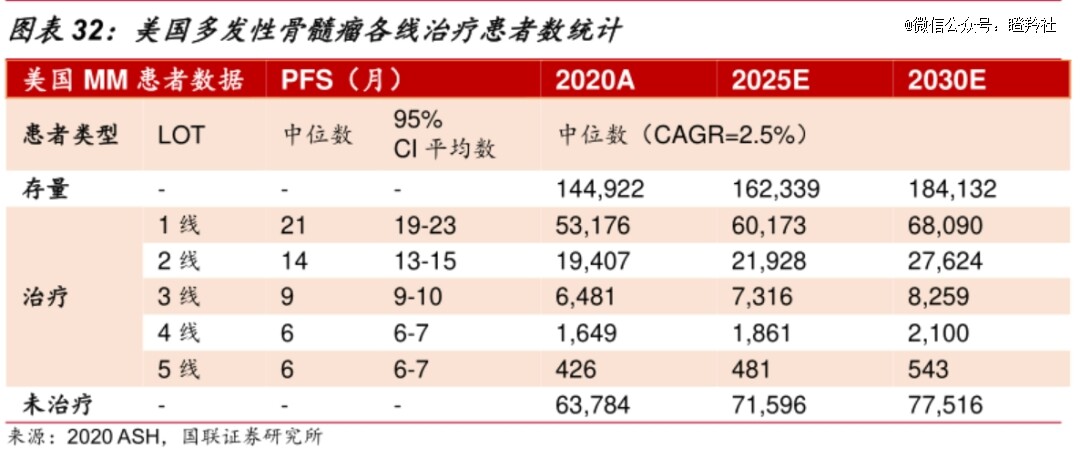

According to Guolian Medicine's forecast: In 2025, the number of second-line RRMM patients in the U.S. will be more than double the number of third-line and above patients; whereas, in 2020, the number of first-line multiple myeloma patients in the U.S. was 53,200, nearly twice that of second-line patients.

Looking at the broader scope, according to Legend Biotech's management, if the company can secure approvals for second-line RRMM treatment from regulatory agencies in the U.S., Europe, and Japan, the total number of potential patients per year could reach 80,000. Even if only one-tenth of these patients receive the treatment, it would still account for 8,000 doses of production capacity.

After succeeding in the second-line push, CARVYKTI begins to advance to the first line, with CARTITUDE-5 and CARTITUDE-6 clinical trials targeting first-line patients eligible for bone marrow transplantation and those who are ineligible, respectively.

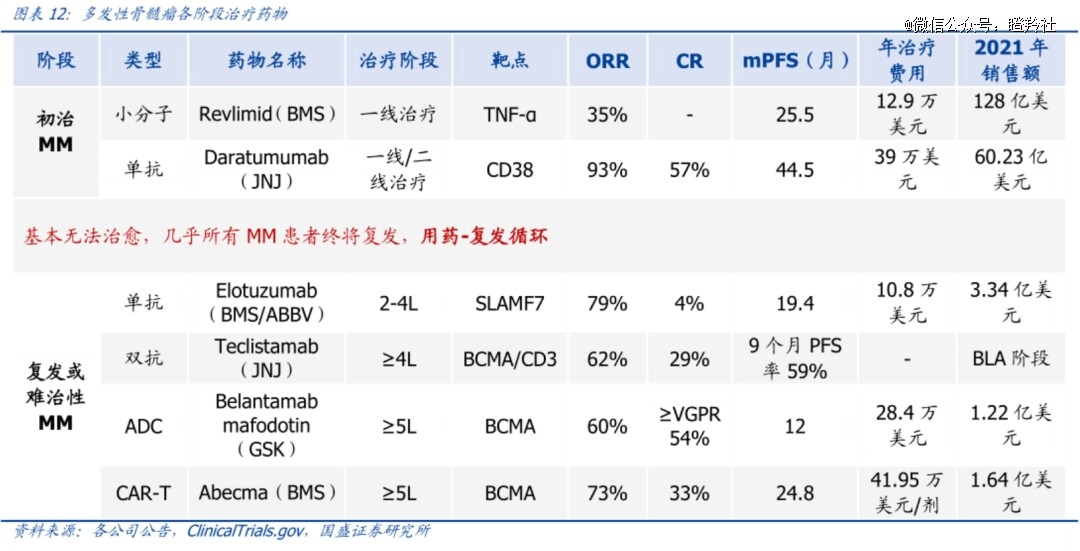

From the perspective of drugs for various stages of MM treatment, CARVYKTI can only achieve its targeted $5 billion in sales if it successfully advances to frontline MM therapy. Looking at the historical sales of past MM treatment drugs, Johnson & Johnson's CD38 daratumumab and BMS's lenalidomide, both of which exceeded $5 billion in peak sales, were approved for frontline treatment.

However, in terms of annual treatment costs, one dose of CARVYKTI costs $400,000, which is higher than daratumumab and lenalidomide. Therefore, it may have an advantage in achieving sales targets.

03

Follow-up in a Clear Situation

Legend Biotech's current development situation is very clear, almost just waiting for the increase in CARVYKTI sales to achieve a "recovery."

The sales growth cycle of pharmaceuticals is always prolonged. For instance, the current top-selling drug "K drug" was first approved by the FDA in 2014, and it may take over 10 years to reach its sales peak (it continues to set new sales records each year).

In a typical Biotech and MNC BD deal structure, as overseas sales increase, the licensor’s royalties are pure profit with no cause for concern. However, the collaboration model between Legend Biotech and Janssen (a Johnson & Johnson company) is a risk-sharing one. When initial sales have not yet scaled up, it requires bearing enormous expenses for clinical trials and sales costs.

As of the end of 2023, Legend Biotech's cash equivalents and short-term investments were approximately USD 1.3 billion. Although the full-year loss for 2023 narrowed to about USD 145 million (losses in 2021-2022 were over USD 400 million each year), with the increase in product revenue, cash flow is sufficient to support long-term operations. However, this is also a positive outcome formed by the parent company continuously selling equity or raising funds (such as out-licensing DLL3 CAR-T, and Genscript selling equity in exchange for liquidity, etc.).

According to MT NEWSWIRES, on March 20, 2024, Legend Biotech filed a registration statement with the U.S. Securities and Exchange Commission for the sale of securities from time to time (shelf registration for mixed securities).

For Legend Biotech, financial pressure is inevitable as the two major clinical trials, CARTITUDE-5 and CARTITUDE-6, are in the enrollment phase, and the commercial promotion of CARVYKTI is at a critical stage, which will undoubtedly accelerate cash burn.

Based on the challenges faced by Legend Biotech and the product potential of CARVYKTI, many overseas analysts and institutions have given the company a "buy" rating.

However, for Genscript Biotech, the powerful backer of Legend Biotech, the stable growth model brought by the continuous commercial revenue of CARVYKTI from Legend Biotech is obviously more attractive than a one-off deal. Therefore, the possibility of completing an acquisition is not high.

Once this difficult period is over, the situation facing Legend Biotech will become extremely clear.

Conclusion:The future growth value that CARVYKTI brings to Legend Biotech is beyond doubt. The short-term sales shortfall compared to market expectations may just be a minor episode. As solutions to challenges are confirmed, an even steeper growth curve may still lie ahead.

[This article is authorized for release by瞪羚社, a WeChat Official Account partner of Zero2IPO. This platform only provides information storage services.] If you have any questions, please contact (editor@zero2ipo.com.cn) for Zero2IPO to handle.