Novartis Strengthens China Presence with New Radioligand Therapy Team and Optimized Pipeline

Novartis

Drug Development and Manufacturing

Targeting the Chinese market, the "leading player" in the nuclear medicine sector has new moves.

Recently, a series of personnel changes announced by Novartis have drawn industry attention. Effective June 1, Zhang Ying, the current President of Novartis China, has been appointed as the Chief Commercial Officer (CCO) of Novartis International, leading the Commercial Launch Strategy (CLS) team and will be based in Basel. Meanwhile, Leo Lee, the current President of Novartis Japan, has been appointed as the President of Novartis China and will be based in China. Under Zhang Ying's leadership, in the first quarter of 2024, Novartis China achieved its first $1 billion quarterly performance, representing a 25% year-on-year growth.

In addition to replacing the "head" of its China branch, Novartis also announced the establishment of a new radioligand therapy team, based on its existing breast cancer, hematology oncology, lung cancer, and solid tumor pipeline teams in China. Wang Ziwen, currently responsible for new product planning in China under the International Business Division, will be appointed as the head of the Radioligand Therapy Team within the same division in China. Notably, this marks the first mention of a dedicated radioligand therapy team in China, making Novartis the first multinational pharmaceutical company to establish such a team in the Chinese market.

However, in the Chinese market, the field of nuclear medicine has not yet been fully explored, and there is still a lack of a mature ecosystem to support the widespread application of this advanced therapy. Nevertheless, as a leading company in the nuclear medicine sector, Novartis, with two radioligand conjugates (RDCs) already on the U.S. market, clearly has sufficient confidence. With the successful establishment of its radioligand therapy team in China, it is bound to make waves in this promising market.

Splurge on Building Product Lines

Precise Layout of the Next Growth Point

In terms of structure, the advantage of RDC lies in its drug payload being a radionuclide, which constitutes the biggest difference from other conjugated drugs. Relying solely on radiation to kill tumor cells, RDC does not need to enter the tumor cells and is less likely to develop resistance compared to ADC. By using different radionuclides, RDC can achieve either diagnostic or therapeutic functions, or even both, realizing an integration of diagnosis and treatment that ADC drugs cannot accomplish. Moreover, RDC can deliver radiation directly to cancer cells or their microenvironment, enabling personalized medication and precise treatment.

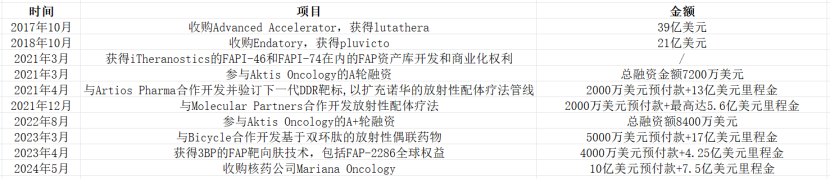

As early as 2017, Novartis began to continuously invest in radioligand therapy technology. In that year, Novartis acquired Advanced Accelerator Applications (AAA) for $3.9 billion, gaining access to the radioligand drug Lutathera (177Lu-dotatate) and related technology platforms. The following year, Novartis spent another $2.1 billion to acquire Endocyte, obtaining the rights to Pluvicto (177Lu-PSMA-617) and 255AC-PSMA-617.

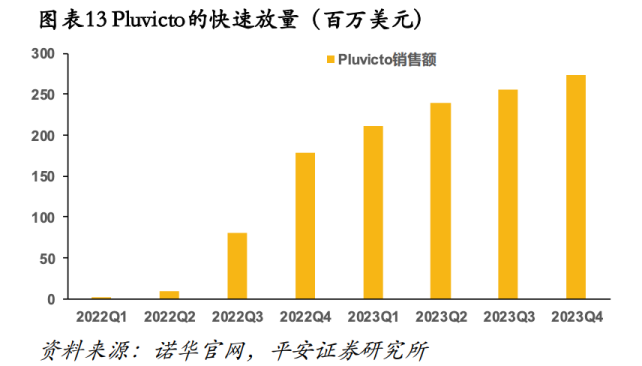

Among them, Lutathera is the world's first approved radioligand therapy (RLT), ushering in a new era of targeted radiotherapy. Pluvicto, on the other hand, is undoubtedly the "star product" in the radiopharmaceuticals field in recent years. In March 2022, the drug was granted accelerated approval by the U.S. FDA for the treatment of PSMA-positive castration-resistant prostate cancer based on its impressive clinical data. According to Novartis' 2023 financial report, Pluvicto achieved $980 million in sales revenue with a 260% growth rate, just a step away from breaking the $1 billion mark, making it the highest-grossing radiopharmaceutical treatment currently available.

Currently, Novartis is still actively expanding the clinical value of these two marketed products, pushing them from late-line treatment to front-line treatment. In October 2023, Novartis announced the results of the Phase III PSMAfore study of Pluvicto in patients with mCRPC who were PSMA-positive and had previously received androgen receptor pathway inhibitor (ARPI) therapy at the ESMO Annual Meeting. The data showed that the trial met its primary endpoint, demonstrating more than double the radiographic progression-free survival benefit in chemotherapy-naïve mCRPC patients. These results are expected to drive Pluvicto towards first-line treatment. Recently, Novartis also updated the full population OS data from the PSMAfore study with positive results, and a new marketing application is anticipated to be submitted in 2024.

Lutathera Also Receives Good News. In January 2024, Novartis announced the latest clinical data from the phase III clinical trial NETTER-2 of Lutathera as a first-line treatment for gastroenteropancreatic neuroendocrine tumors (GEP-NETs) at the ASCO-GI meeting: the primary endpoint mPFS was extended from 8.5 months to 22.8 months, nearly tripling, with a 72% reduction in the risk of disease progression or death, and an overall response rate (ORR) as high as 43%. In the industry's view, these positive data have brought greater room for imagination regarding Lutathera’s therapeutic benefits in the field of cancer.

Moreover, Novartis is making continuous progress to further defend its position as the global leader in nuclear medicine. In addition to the two marketed RDC products mentioned above, Novartis also has several products under development, including 177Lu-FAP-2286, 177Lu-NeoBOMB1, and 225Ac-PSMA-617. According to the company's official website, 177Lu-FAP-2286 targets fibroblast activation protein (FAP) and is currently in Phase 1/2 clinical trials for solid tumors; 177Lu-NeoBOMB1 targets gastrin-releasing peptide receptor (GRPR) and is in early clinical trials for indications such as breast cancer and prostate cancer; 225Ac-PSMA-617 utilizes a highly potent α-emitting radionuclide with a shorter range, offering greater advantages over Pluvicto in cancer treatment.

(Part of Novartis' Related Transactions in the Radiopharmaceuticals Field)

In terms of production capacity layout, Novartis is also taking preemptive measures. At the beginning of 2024, Novartis announced that its new radiopharmaceutical production base in Indianapolis had received approval from the U.S. FDA for the commercial production of Pluvicto. It is reported that the Indianapolis production base is the second RLT production base approved by the FDA in the United States, which will increase the RLT production capacity to 250,000 doses per year in 2024 and beyond.

The unstoppable momentum in the international market has also led Novartis to decide to introduce these RLTs into the Chinese market. Novartis China told reporters from the New Media Center of the Pharmaceutical Economy News that while Novartis is deploying RLT globally, it is conducting continuous and extensive development and exploration in China, the most strategically significant market. Currently, Novartis has launched multiple registration clinical studies involving RLT therapies in China, including an RLT product for second-line metastatic prostate cancer indications already marketed in Europe and the US, as well as frontline prostate cancer indications under global synchronized development and several other RLT pipeline products in the early stages of development.

As Novartis stated, it has accumulated highly specialized expertise in the research and development, production, and clinical application of precision-targeted drugs and therapies containing radioactive components, as well as interdisciplinary and cross-industry collaboration. In the industry's view, these are precisely what the Chinese market lacks. How Novartis will strengthen its position in China’s nuclear medicine sector and consolidate its global dominance remains to be seen. The New Media Center of the Pharmaceutical Economy Newspaper will continue to follow developments.

The Radiopharmaceuticals Track Continues to Heat Up

Pharmaceutical giants enter the fray

The remarkable success of Lutathera and Pluvicto has made Novartis a standout leader in the RLT field, creating a wave of optimism that has also positively influenced the global market. Statistics show that from 2021 to 2023, the global radiopharmaceuticals sector raised over $60 billion in cumulative financing, with the total amount in 2023 increasing by 82% compared to 2022. In terms of business development (BD), large transactions in the radiopharmaceuticals space have become more frequent. In addition to Novartis, pharmaceutical giants such as Bayer, AstraZeneca, and Eli Lilly are accelerating their strategic moves.

Bayer ventured into the field of nuclear medicine relatively early. It launched Xofigo a decade ago and subsequently made significant acquisitions of innovative companies such as Algeta, Noria, and PSMA Therapeutics to further strengthen its RDC portfolio. Today, Bayer has become one of the pioneers and leaders in this field. Reportedly, Bayer currently has 7 RDCs in preclinical stages and 2 in early clinical stages (BAY 3546828, BAY 3563254) under development.

In October 2023, Eli Lilly successfully acquired Point Biopharma for $1.4 billion, aggressively entering the targeted radiotherapy market. POINT's core asset, PNT2002, is a PSMA-targeted therapy for metastatic castration-resistant prostate cancer (mCRPC), with PSMA being overexpressed in the vast majority of prostate cancers (>85%). POINT has developed unique intellectual property for the radioactive API and formulation of PNT2002, which combines the PSMA-targeting ligand PSMA-I&T with the beta-emitting radioisotope lutetium-177 (Lu-177). PNT2002 is currently in Phase III clinical trials.

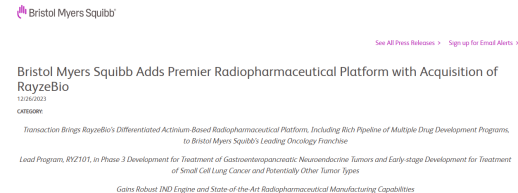

Subsequently, BMS also acquired nuclear medicine newcomer RayzeBio for $41 billion at a premium. This marks the largest acquisition in the history of nuclear medicine transactions, further increasing industry attention on this track. Through this acquisition, BMS gained a clinical RPT program targeting gastroenteropancreatic neuroendocrine tumors (GEP-NET) and extensive-stage small cell lung cancer (ES-SCLC). Additionally, BMS will acquire RayzeBio’s differentiated radiopharmaceutical technology platform based on alpha radionuclides, along with several innovative products under development, including targeted radiopharmaceuticals such as RYZ101 and RYZ801.

Among them, RayzeBio's leading candidate drug RYZ101 is an actinide-based radiopharmaceutical therapy (RPT) targeting somatostatin receptor 2 (SSTR2). It is reported that the α-emitter of actinide-based RPT has high potency and short range, which can improve efficacy and targeting compared with currently available RPTs on the market. RYZ101 is currently in Phase III trials for SSTR-positive GEP-NET patients and Phase 1b trials for ES-SCLC patients, used in combination with standard therapies. If the Phase III clinical trial is successful, RYZ101 will become the first approved actinium-225 radiopharmaceutical therapy.

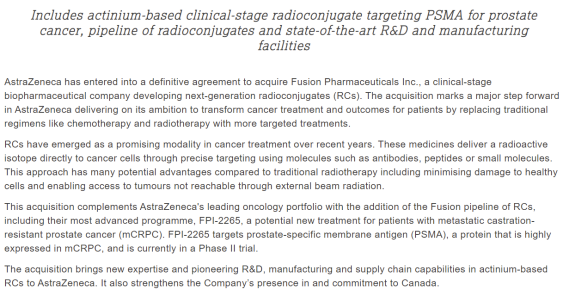

Since 2024, the radiopharmaceuticals sector has continued to heat up. In March, AstraZeneca announced the acquisition of Fusion Pharmaceuticals for $2 billion, making it a wholly-owned subsidiary. In fact, AstraZeneca had previously collaborated with Fusion to research targeted alpha therapies and drug combinations. Four years later, aiming at the growing demand in the radiopharmaceuticals field, AstraZeneca chose to directly acquire Fusion. Fusion’s core product is FPI-2265, a new therapy for metastatic castration-resistant prostate cancer that targets prostate-specific membrane antigen and is currently in Phase II clinical development.

In May, Novartis stepped in once again, announcing the acquisition of Mariana Oncology, a radiopharmaceutical company. Novartis will gain access to the latter's preclinical research pipeline for cancer and clinical supply capabilities, further strengthening its position in radioligand therapy (RLT). This acquisition includes a portfolio of RLT projects targeting a range of solid tumor indications (such as breast cancer, prostate cancer, and lung cancer), including MC-339, the lead actinium-based RLT project for small cell lung cancer. Facing an expanding market and a surge of competitors, Novartis’ deepening engagement in business development (BD) may also be a key strategy to address the intense competition in the radiopharmaceuticals space and consolidate its leadership position in this field.

According to MEDraysintell data, the global nuclear medicine market size will increase from $6 billion in 2019 to approximately $30 billion by 2030. Seeing the development prospects of the nuclear medicine track, pharmaceutical giants have already placed their bets. With more and more drugs coming to market and the further improvement of the industrial ecosystem, highly efficient, low-toxicity, theranostic targeted nuclear medicines may become the mainstream therapy for the next generation of cancer treatment. In this dynamically evolving blue ocean market, who will seize the first opportunity remains to be seen.

www.yyjjb.com.cn

Insight into Industry Trends

"Pharmaceutical Economy Report"

Academic Official Account

Focus on the Frontier of Oncology Academia

Terminal Official Account