Crisis Averted: Why I Believe in MicroPort's Future

MicroPort

High-end Medical Device R&D and Manufacturer

4On August 8, MicroPort announced that it had secured a $150 million convertible term loan facility with an annual interest rate of 5.75%, participated by GL Ventures and the company's management. It is also expected to receive over $300 million in credit support from financial institutions. The funds will be used to repay the convertible bonds issued in 2021 in June, cover expenses, and serve general corporate purposes.

On May 22, the matter was approved at the company's shareholders' meeting.

Although the "borrowing new to repay old" debt swap seems to have temporarily defused the alarm, in the latest financing plan, GL Ventures has set clear targets for MicroPort's loss reduction and profitability.

MicroPort's net profit targets for 2024, 2025, and 2026 are -US$275 million, -US$55 million, and US$90 million, respectively. In other words, if MicroPort fails to turn a profit within three years, GL Ventures has the right to demand early repayment of a five-year US$50 million loan and related interest.

This shows that the Sword of Damocles hanging over the hearts of everyone at MicroPort has not truly been removed, and this sword is slowly falling with the countdown of three years.Under the severe winter, how will MicroPort reverse losses into profits and rebuild a healthy cash flow? The company needs to propose corresponding measures for effective self-rescue.

At the earnings briefing held on April 8, MicroPort mentioned:"The company will firmly implement business focus, ensure revenue growth while continuously promoting cost reduction and efficiency enhancement, fully emphasize the health of cash flow, gradually improve profitability, and strive to significantly reduce losses in 2024 and approach break-even by 2025."

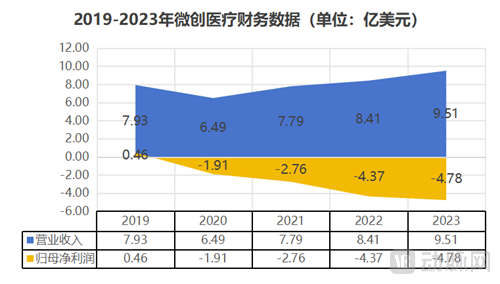

Data source: MicroPort Annual Report, Chart by VCBeat

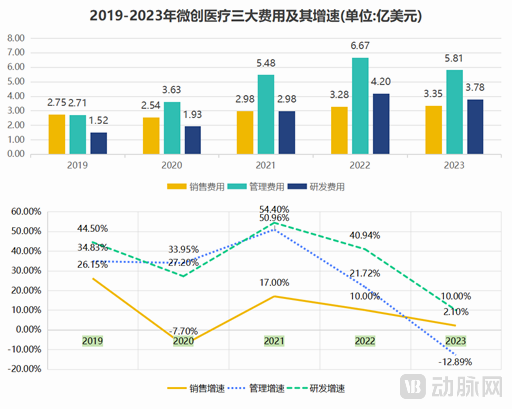

MicroPort has always been renowned in the industry for its substantial R&D expenditures and outstanding innovation capabilities.According to MicroPort's annual reports over the years, from 2018 to 2022, MicroPort's R&D investment showed a significant increase for five consecutive years, accounting for approximately 30% or more of total revenue, even reaching a peak of 50% in 2022. In contrast, this figure generally accounts for about 10% of the total revenue of Mindray Medical and Medtronic.

Data source: MicroPort Annual Report, Chart by VCBeat

"Perfection inevitably leads to deficiency; extremity inevitably results in reversal; fullness inevitably causes loss" — this is the wisdom imparted by *Lüshi Chunqiu* to future generations. Although, for MicroPort operating in the high-end medical device sector, R&D investment is a crucial means to achieve sustainable corporate development, enhance competitiveness, and improve economic returns, from the perspective of revenue for innovative companies, an overly high proportion of R&D investment may lead to reduced efficiency in capital allocation and difficulties in cash flow.

From the perspective of industry observers, what MicroPort has just faced is actually a delayed crisis.

The issuance of convertible bonds coincided with the vigorous development of innovative pharmaceuticals and medical devices, attracting capital inflows due to optimistic prospects. According to normal patterns, the peak of this capital-driven boom should have arrived earlier. However, an unexpected pandemic propelled the entire pharmaceuticals industry into a new development cycle, delaying the downward curve. Nevertheless, objective laws are hard to defy—although delayed, the trough in investment eventually arrived, and MicroPort, traditionally capital-intensive, was inevitably impacted.

First, the sum of R&D and management expense ratios decreased by 18 percentage points, but the strategy of maintaining marketing expenses became evident.

It is worth noting that, according to the 2023 annual report, MicroPort had already proposed targeted self-rescue measures before this crisis fully erupted. In 2023, the combined rate of the company's R&D and management expenses decreased by 18 percentage points year-on-year. Among these, R&D expenses dropped by 10%. At the same time, to ensure resource allocation aligns with strategic goals, the company’s organizational structure was effectively streamlined, resulting in an approximately 19% reduction in management expenses. In terms of marketing, despite a four-percentage-point decrease in the sales expense ratio, the absolute amount of expenses increased slightly year-on-year, reflecting the continued emphasis on sales.

Moreover, MicroPort also anticipates that the company's R&D expenses in 2024 will further decrease by 35% to 40% compared to last year. It is expected that by 2026, the R&D expense ratio will be controlled to less than 15%.

From the results, the company's substantial R&D investment has still paid off.From early 2023 to April 2024, MicroPort and its affiliated companies obtained 44 Class III first-time registration certificates from the National Medical Products Administration (NMPA) or completed significant changes, received FDA registration approval for 19 products, and obtained CE certification for 20 products.

Second, the impact of centralized procurement on mature products such as stents is gradually being absorbed, and efforts are being made to leverage centralized procurement for the rapid scaling of new products.

The three-year pandemic and the normalization of bulk procurement also served as important background and catalysts for this incident. Since 2020, MicroPort, as one of the leading companies in centralized procurement, has seen its attributable net profit shift from profit to loss.

Although the reduction in gross profit margin is irreversible, with the recent mildness of centralized procurement price cuts and most of MicroPort's product lines falling within the scope of centralized procurement, the advantages of leading companies are being continuously consolidated.

Industry insiders familiar with centralized procurement stated that, in fact, for local companies like MicroPort Medical that continuously develop new products and aim to achieve domestic substitution, centralized procurement, while reducing the profit levels of their "cash cow" products, also provides an excellent opportunity for new products to quickly enter the market. On one hand, as long as the company can follow up with effective post-procurement implementation, centralized procurement can become a new fast track for rapid volume growth. On the other hand, companies with leading shares in centralized procurement can also leverage hospital channel advantages to achieve cross-selling of their entire product line, including innovative products not yet covered by centralized procurement.

From the implementation of previous centralized procurement, MicroPort has consistently completed the supply tasks with assured quality and quantity. Under the normalization of volume-based procurement, the rules are expected to become increasingly mature, and the price reduction is anticipated to be more moderate. Therefore, the company's future profit margin is also expected to rise.

Third, focus on streamlining operations and strengthen project control.

Since 2019, MicroPort has successfully spun off five subsidiaries for IPO within four years, with a maximum of two major subsidiaries being spun off in a single year. The original intention of the spin-offs is to leverage financing as a catalyst for R&D, helping the subsidiaries grow rapidly, thereby driving more products to market, which in turn benefits the group and ultimately helps it grow into "China's Medtronic."

The prerequisite for MicroPort's "spin-off" is internal incubation, capturing the track early on. This approach itself is not problematic, as it means less upfront investment compared to directly purchasing a mature company. However, smooth financing in the past led to overexpansion in R&D, and MicroPort chose to simultaneously enter multiple tracks. This resulted in several subsidiaries having high R&D investments and long return cycles. Facing a capital winter and debt pressure, necessary downsizing has become the "best" option.

Reported by the media,MicroPort has strengthened the entire project management since 2023., and carry out "closure, merger, and transformation" for several subsidiaries including MicroPort Online, MicroPort Rehabilitation, Miracle Point Incubator, and Duowen Medical, aiming to address the issues of high investment and consecutive years of losses.

At the same time, the group has also joined the "layoff wave" sweeping through the medical industry. According to the 2023 annual report, MicroPort had 8,230 employees at the end of 2023, a decrease of 1,205 from the end of 2022, with some subsidiaries experiencing nearly a 50% reduction in staff. Moreover, the future evaluation criteria for the group from top to bottom will be directly linked to performance targets, aiming to motivate employees, allocate resources more reasonably internally, and improve resource utilization efficiency.

As of now, MicroPort Group has six listed companies under its umbrella, including the parent company MicroPort Medical, and five subsidiaries: MicroPort CardioFlow Medtech (688016.SH), MicroPort Heart Technology (02160.HK), MicroPort Robotics (02252.HK), MicroPort Neuromodulation (02172.HK), and MicroPort EP (688351.SH).

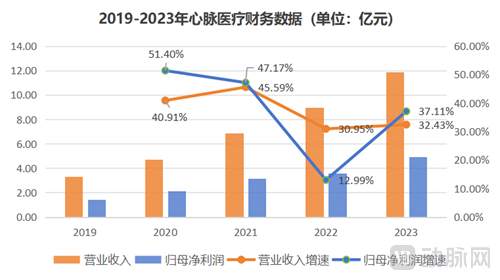

From the growth trajectory of MicroPort CardioFlow, which was the first to be listed on the Shanghai STAR Market in 2019,From 2019 to 2023, MicroPort CardioFlow Medtech Corporation's total operating revenue increased from 334 million yuan to 1.187 billion yuan, with revenue growth nearly fourfold, while the net profit attributable to the parent company also rose from 142 million yuan to 492 million yuan. In particular, in 2023, the total operating revenue saw a year-on-year increase of 32.43% compared to 2022, and the net profit grew by 37.98% year-on-year. MicroPort CardioFlow has undeniably grown into a leader in vascular intervention.

Data source: Heartpulse Medical Annual Report, VCBeat Chart

Since its listing, Endovastec has achieved remarkable results in both product development and market sales. The number of hospitals adopting and the terminal implant volume of Endovastec's innovative products, such as the Castor Branched Aortic Stent Graft and Delivery System, Minos Abdominal Aortic Stent Graft and Delivery System, and Reewarm PTX Drug Balloon Dilatation Catheter, have shown significant growth.

Among them, Castor is the world's first approved branched aortic stent for the treatment of aortic arch lesions. In recent years, its actual growth rate has been over 30%, and it has covered more than 1,000 terminal hospitals cumulatively. Moreover,Heartpulse Medical's overall profitability is stable, with a market share of about 30% in the aortic vascular interventional medical device sector.

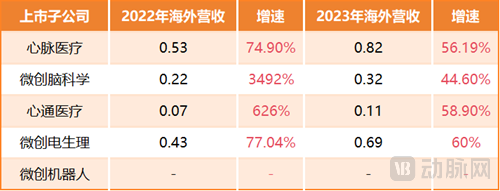

As the sales expense ratio steadily decreases and the degree of industrialization deepens, MicroPort CardioFlow Medtech Corporation faces the pressure of centralized procurement by strengthening cost control, improving operational efficiency, and enhancing company value through technological innovation.In terms of international expansion, the company's international business revenue increased by 51%, and its product sales have covered 31 countries.

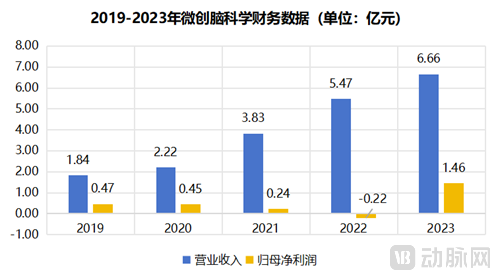

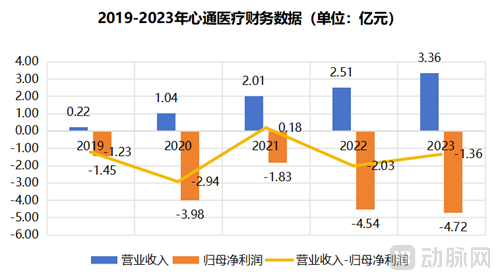

MicroPort's Neurointervention Business - MicroPort Brain ScienceAchieving a turnaround from loss to profit with strong growth after going public, total operating revenue reached 666 million yuan, an increase of 21.6% over the previous year; gross profit was 512 million yuan, a year-on-year increase of 30.2%; net profit was 135 million yuan. In addition, MicroPort NeuroScience also announced its first dividend distribution plan after listing, proposing a total dividend of approximately 64 million Hong Kong dollars, accounting for about 33% of the adjusted net profit.

Data source: MicroPort Neurology Annual Report, Chart by VCBeat

In 2023, MicroPort NeuroTech's overall market share in China rose to 8.2%, consistently ranking first among domestically produced products. Moreover, China sees 3.4 million new stroke patients annually, with a market potential several times larger than that of the U.S. and Europe. The market is still in the early stages of domestic substitution, indicating vast growth opportunities. As a leading Chinese enterprise specializing in neuro-intervention, MicroPort NeuroTech has established a certain leading position in both product offerings and channel distribution, which is expected to drive long-term, sustained high growth in revenue and profits.

Next, let's look at MicroPort's more rapid growth.Cardiac Valve Business - MicroPort CardioFlowIn 2023, MicroPort CardioFlow achieved a total operating revenue of 336 million yuan, representing a 33.9% increase from the same period last year; the gross profit was approximately 230 million yuan, marking a 41.8% year-on-year increase.

Data source: MicroPort CardioFlow annual report, chart by VCBeat

The rapid growth of HeartFlow Medical is mainly driven by the increase in sales revenue of TAVI products in China and overseas. According to the 2023 annual report, the number of TAVI product adoptions in hospitals in China has led to a rapid increase in the number of surgeries.The implant volume in China increased by approximately 45% compared to 2022, with a cumulative total of 554 hospitals in China (117 newly added in 2023), achieving a global total of 3,820 implants, of which the number of overseas implants increased by 90% year-on-year, and sales revenue also grew by 59% compared to last year.

As an innovative listed company, turning losses into profits is also one of the core strategies. In 2023, the combined R&D and management expense ratio of MicroPort CardioFlow decreased by 26 percentage points, while the sales expense ratio increased by 2 percentage points. If this trend continues, MicroPort CardioFlow is expected to become the first profitable valve company in China next year. Like MicroPort itself, MicroPort CardioFlow also focuses on creating platform-based innovative products and is highly committed to product diversification and international business.

In January 2024, MicroPort CardioFlow completed the acquisition of Shanghai Zuoxin, integrating the group's left atrial appendage-related medical device business and achieving a strategic restructuring of its structural heart disease operations. This merger also further enhanced internal business synergy within the group and strengthened the market competitiveness of this business segment.

The Fourth, MicroPort EPIn 2023, revenue reached 329 million yuan, a year-on-year increase of 26.46%; net profit attributable to shareholders was 5.6885 million yuan, a year-on-year increase of 85.17%; basic earnings per share were 0.0121 yuan, a year-on-year increase of 65.75%.

Currently, the penetration rate of cardiac electrophysiology procedures in China is low, making it a continuously expanding field. MicroPort EP is one of the few global manufacturers capable of completing a full layout of both cardiac electrophysiology devices and consumables. It is also the first domestically produced manufacturer in China able to provide a complete solution for three-dimensional cardiac electrophysiology devices and consumables, breaking the long-term technological monopoly held by foreign manufacturers in this field.

Although the company's gross margin slightly decreased by 6.6% compared to 2022 due to the impact of China’s centralized procurement price cuts, the gross margin of new products is expected to gradually increase with the rise in production and sales volume, the acceleration of domestically produced raw material substitution, and the optimization of manufacturing processes. It is reported that the company's products have cumulatively covered more than 1,000 hospitals, with a year-on-year increase of over 50% in three-dimensional surgeries. In terms of overseas expansion, the company’s international sales revenue increased by more than 50% year-on-year, with its products covering a total of 35 countries and regions worldwide.

Finally, MicroPort Robot is currently the world's only surgical robot company with business coverage across the five "golden tracks" of endoscopy, orthopedics, peripheral vascular, natural orifice, and percutaneous puncture.

In 2023, the company achieved a total operating revenue of 1.046 billion yuan, representing a year-on-year increase of 258%. This growth was mainly driven by the strong market performance of the company's core product, TuMi, following its approval and market launch for multi-department applications, as well as the successful overseas promotion of orthopedic surgical robots. As of March 2024, TuMi's four-arm laparoscopic surgical robot has won nearly 20 bids in China and completed the commercial installation of 11 units, with 10 units installed domestically in 2023 alone. By the end of the year, TuMi also secured its first overseas order, marking a new breakthrough in globalization.

However, the company's losses cannot be ignored. In 2023, the company's adjusted net loss was 869 million yuan, a decrease of 110 million yuan or 12% compared to last year, but it still has a way to go before turning a profit.In response, the company's proactive cost-control measures have begun to take shape, with reductions in R&D expenses and management costs both reaching 25%. The net outflow of free cash flow has also decreased by 42%.

More importantly, with the general favorable policies, MicroPort Robotics also actively expressed in the investor communication meeting:The company's revenue is expected to reach 200 million yuan in 2024. Moreover, this 200 million yuan does not include the additional revenue from consumables that will be added in 2024.

Data source: Annual reports of various companies, compiled by VCBeat

At the same time, unlike many innovative medical device companies that focus mainly on the domestic market, MicroPort's overseas market presence is very prominent. In 2023, the group's overseas business achieved revenue of 57 million US dollars, increasing by 54%. MicroPort's Chief Financial Officer, Sun Hongbin, also stated,"It is expected that in the next few years, the group's overseas expansion will enter a high-growth harvest period, with total overseas revenue growing at an annual rate of no less than 50%."

In 2023, the market size of China's medical device industry has broken through the trillion-yuan mark. It seems that MicroPort is gradually moving farther away from its dream of building a trillion-yuan empire, but given the long-term potential and substantial opportunities in the healthcare sector, rewinding to 1998 when the company was just founded may offer some insights into MicroPort’s future.

When MicroPort was established in 1998, the area around Zhangjiang Park, where the company was located, was still surrounded by green farmland. At that time, China's high-end medical device market was far from reaching a trillion yuan.When Dr. Changhao Chang returned to China from the United States and founded MicroPort, he initially focused on medical devices used for minimally invasive interventional treatments, such as coronary drug-eluting stents for the treatment of coronary heart disease. By promoting domestically produced alternatives, he forced the price of imported products to drop by two-thirds, which in turn drove a million-fold increase in the number of cardiac stent surgeries in China, allowing a large number of Chinese patients to access affordable domestically produced stents.

In 2021, the moment MicroPort broke through the 100 billion yuan market value was unforgettable for all investors and also inspired the founder to proclaim the dream of building a trillion-yuan MicroPort Group.But industrial transformation always has a cyclical, wheel-like development trend, especially for the technology-intensive, high-investment, risk-and-reward coexisting medical industry.

It is undeniable that from 1998 to the present, MicroPort has completed the transition from a single product line,The transformation and expansion into more than 600 medical solutions. Now, the company's most important "1+12+5" platform has been basically completed.Covering 12 directions: cardiovascular and structural heart disease, cerebrovascular neuromodulation interfaces, large vessel life support and peripheral, electrophysiology and arrhythmia management systems, medical robotics and digital healthcare, gynecology, urology, and gastroenterology medical care, joint spine trauma sports medicine, ophthalmology respiratory and home healthcare, cancer treatment and patient life support, endocrine in-vivo diagnostics and reproduction, synthetic biology regenerative medicine revitalization, functional skincare cosmetic surgery and aesthetic medicine.Basically covering all departments in the hospital.

Although it is expected that inevitably some businesses will be abandoned during the future streamlining and transformation, this "cost of growth" may be unavoidable for China's domestic innovative medical device enterprises in their development. Despite MicroPort often being criticized for its losses and sluggish stock price, it is an undeniable fact that several of its businesses started from scratch and successfully joined the ranks of the top tier in China within a short period.

At the earnings briefing in April and the shareholders' meeting in May, the company conveyed an important message to investors and the public: MicroPort Medical "has no going-concern issues," and short-term control of R&D and management costs "will not affect the company's revenue situation in the next three years."

Moreover, regarding the medium- and long-term planning, Sun Hongbin stated"Be open to the integration or divestiture of businesses.", which means that in the future, the company will scientifically and reasonably dispose of its assets, especially business segments that are still bleeding heavily, ultimately achieving sustainable self-sustaining growth with a lighter burden.

"According to the data, the company's losses in 2024 will significantly narrow, with an expected reduction of over 60%. In the coming years, the company aims to maintain annual revenue growth of more than 20%, continuously reduce costs and increase efficiency, and steadily improve profitability to approach break-even by 2025."

Once frenzied about spinning off and going public, MicroPort is now racking its brains to pay the price for "bigness." However, it is undeniable that as the first mover in China's medical device industry, MicroPort still holds the "spark" of innovation. Amidst the winter of the healthcare industry’s development cycle, it continues to reshape corporate value and responsibility, actively transforming itself to re-emerge with a new posture.

This three-year "bet," we will wait and see!