Johnson & Johnson Surpasses Stryker with Breakthrough VELYS Robotic System for Partial Knee Replacement

Johnson & Johnson

Medical Device R&D and Manufacturer

Click above “Medical Device Business Review"--Upper Right Corner"…"--Set asStar Mark

Source:Medical Device Business Review

Author: Jiang Lecture

Reproduction without authorization is prohibited, and reproduction is allowed only 24 hours later!

Total joint arthroplasty is considered one of the most successful orthopedic surgeries since the 20th century and is widely recognized as the most effective treatment for end-stage hip and knee osteoarthritis. The industry has made decades of continuous efforts to improve the outcomes of joint replacement surgeries, but the treatment effectiveness has now reached a bottleneck.

According to The Lancet, globally there are approximately650 Million People Suffer from Knee OsteoarthritisIn China, more than 1 million patients undergo this type of surgery each year, but clinically, there is still a dissatisfaction rate of around 8% to 15%. Therefore, improving the implantation technology of artificial joints has become a new direction for industry development.Robotic joint replacement systems capable of performing surgeries autonomously have become the mainstream approach in current practice.

Recently, Johnson & Johnson announced its DePuy Synthes orthopedic robot---VELYS Receives FDA Approval for Clinical Use in Unicompartmental Knee Arthroplasty (UKA).This marks a new chapter for the next-generation VELYS knee replacement technology, following its FDA approval for total knee arthroplasty (TKA) in 2021.

Image source: Johnson & Johnson official website

Aldo Denti, Chairman of Johnson & Johnson's DePuy Synthes Companies, stated: "VELYS combines our most advanced VELYS technology and adds a robotic-assisted product to the clinically proven UKA implant, which will...""Addressing some of the critical unmet needs in the field of knee replacement in the market"。

After this brand-new upgrade, the VELYS surgical robot has expanded its indications based on the total knee arthroplasty platform.Added UKA (Unicompartmental Knee Arthroplasty) application, specifically designed for partial knee replacement surgeries (medial and lateral), preserving the patient’s healthy bone and reducing recovery time., allowing surgeons to accurately guide implant placement without the need for CT scans.

Total Knee Arthroplasty (TKA) has long been regarded as the "gold standard" for the treatment of knee joint diseases, but traditional Total Knee Arthroplasty (TKA) for treating Knee Osteoarthritis (KOA)LimitationsIt is also evident in the directLarge injury area caused by the excision of the anterior cruciate ligament (ACL), unable to fully reconstruct the natural morphology of the knee joint.And other aspects that require extensive release of the joint capsule and ligaments.

Partial knee arthroplasty (UKA), compared to total knee arthroplasty (TKA), is a less invasive surgical procedure that offers more...Accurate Reconstruction of the Medial and Lateral Compartments of the Knee Joint, only the irreplaceable cartilage of the knee joint is replaced, without involving the entire knee joint, preserving the healthy part of the knee joint. Therefore, the patient's proprioception and joint function are superior to total knee replacement.

However, due to some joint replacement surgeries during the operationSmall incisionAndInsufficient Visibilityand other issues, which has led to the technology not being fully utilized in the market compared to total knee arthroplasty,Partial knee replacement surgery requires higher precision and technical expertise, with a high demand on the surgeon's experience., with a long learning curve.

As a global leader in medical devices, Johnson & Johnson's Velys surgical robot offers unique intraoperative insights, precise implant alignment and positioning, and more repeatable and consistent outcomes, all of which help address these challenges. Its groundbreaking technology and superior clinical performance provide a new treatment option for nearly 650 million patients with knee osteoarthritis worldwide.

Plug and play, integrated into any operating room

Compared with other bulky orthopedic robots on the market, VELYS is the first solution installed on the operating table, adaptable to the surgeon's workflow.Portable plug-and-play, no longer confined to the operating room.The efficient and compact design can be integrated into any operating room, reducing the footprint to less than half of some other robotic-assisted solutions.

Precise positioning, no preoperative imaging required

The high demand for precision in orthopedic surgery has always been a challenge for industry development. VELYS is specifically designed for medial and lateral surgeries, providing intraoperative insights, more accurate implant alignment and positioning, as well as more repeatable and consistent outcomes, enabling surgeons toGuide precise resection without CT scanBone and Implant Placement: Addressing Variability in Long-Term Treatment Outcomes.

Brand New Upgrade, Personalized Surgical Customization

Another major feature at the technological innovation end is that the new generation of VELYS will maximize the advancement of knee surgery.Customization, Precision。At the clinical use end, a single PROADJUST™ planning screen enables personalized surgical planning, capable of adapting to the patient's anatomical structure.Customized Individualized Surgery, helping to ensure the precise placement, alignment, and balance of the implant relative to the patient's soft tissue; enabling doctors to visualize and predict joint stability to support optimal patient outcomes.

Not just a robot, but a complete orthopedic medical ecosystem

In addition to robotic-assisted solutions, Johnson & Johnson is also positioning VELYS as a platform across various surgical specialties.An interconnected, integrated full set of digital healthcare ecosystemOn the one hand, it completes precise plane cutting control and real-time surgical evaluation based on previous technical foundations, and on the other hand, VELYS is compatible with multiple joint surgery supporting products under Johnson & Johnson, forming a complete Johnson & Johnson orthopedic surgery product ecosystem.

In addition to its outstanding product technology and design, Velys also demonstrates excellent clinical performance.

As the first desktop orthopedic surgical robot in its class, since its initial approval in 2021, Velys has demonstrated outstanding performance in the field of orthopedics, making it a global success.20 CountriesOr put into use in the region, and used forMore than 55,000 surgical casesIn China, provide surgeons with the information needed for surgery to help protect the soft tissue capsule, predict joint stability, and strive to restore knee function.

VELYS solutions are highly differentiated, help improve clinical outcomes and increase patient satisfaction, and provide a more attractive clinical solution compared to existing options on the market. From the perspective of the global orthopedic surgical robotics market size,Knee replacement surgery accounts for 40.5% of the market share.There are still significant opportunities in the orthopedic field to combine robotics with digital surgery technology.

Following this approval, the all-new generation VELYS surgical robot will take on a significant market expansion mission, further accelerating its adoption in the U.S. market. This will also further solidify Johnson & Johnson's position in the orthopedics field.Help it regain market share from competitors like Stryker.

If you are interested in this Johnson & Johnson product

Scan for registration~

In the orthopedics field, Johnson & Johnson is one of the earliest pioneers. In 1998, it acquired DePuy, becoming the leader in the orthopedics sector. Thirteen years later, it acquired Synthes, which held an ultra-high market share (around 50%) in the orthopedic trauma field and ranked among the top five in the global orthopedics market, further solidifying its position.The leading position in the global orthopedics field.

But in the field of surgical robotics,Johnson & Johnson's development has been full of ups and downs.. Especially in the niche field of orthopedic surgical robots, multiple brands have launched fierce competition. For example,StrykerThe orthopedic robot Mako has surpassed 1,000 installations, while the orthopedic robots from Smith & Nephew and Zimmer Biomet are further eroding Johnson & Johnson's market share. As a result, for quite some time, when mentioning giants in the orthopedic robot industry, only...Stryker, Zimmer Biomet, MedtronicThree companies, Johnson & Johnson is no longer what it used to be.

In recent years, Johnson & Johnson has been striving to transform itself into a giant in the field of orthopedic surgical robotics. Around the start of 2020, Johnson & Johnson began to make significant advances in the robotics sector, compensating for its technological lag in surgical robotics through multiple acquisitions and technical mergers.

Surpassed by newcomers, Johnson & Johnson naturally不甘落后. In 2018, Johnson & Johnson acquired at an undisclosed price.Acquisition of French Surgical Robot Developer Orthotaxy, which is used to develop the next generation of robotic-assisted surgical platforms for orthopedics, also provided important technical support for the approval of the VELYS surgical robot this time.

But to catch up with the leading pace of the top three orthopedic robot companies, this is far from enough. Subsequently, Johnson & Johnson spun off its medical technology division in 2019.Acquired Auris Health for $3.4 billion.

Through this acquisition,Johnson & Johnson has been able to hire robotic surgery expert Frederich Moll, M.D.Moll is the CEO and founder of Auris Health. One of his major achievements is co-founding Intuitive Surgical—one of the largest players in the surgical robotics market—earning him the title of "Father of Surgical Robotics."

Besides spending a huge sum to acquire Auris Health, Johnson & Johnson has consecutively laid out plans in the surgical robotics field in recent years:

In 2019, Johnson & Johnson continued to acquire the pelvic surgery navigation software developed by JointPoint, a surgical navigation technology company.

In 2020, Johnson & Johnson acquired the remaining shares of Verb Surgical, which was previously co-founded with Google, and fully took over Verily's robotic surgery business.

With the support of DePuy Synthes' orthopedic technology and Dr. Moll, as well as multiple acquisitions of leading robotics companies, Johnson & Johnson has achieved significant progress in the field of orthopedic robotics after gathering such extensive resources. They successively launched the first-generation total knee surgery robot and the second-generation unicompartmental knee surgery robot VELYS, respectively.Received FDA Approval for Market Launch, and continuously capture market share in the United States and multiple European countries.

Orthopedics, as the core business of Johnson & Johnson, has achieved comprehensive success under restructuring and transformation since last year, with the knee robot sector being the fastest-growing segment.

According to the latest releaseTop 10 Global Orthopedic Device Companies Ranking DataIt shows that, as the second largest business segment of Johnson & Johnson Medical Technology, the revenue of DePuy Synthes Orthopaedics reached 8.9 billion US dollars in 2023.Regained the top position in the global orthopedics market with a narrow win over Stryker by a $200 million advantage.Knee joint business, as one of the细分领域 of Johnson & Johnson's orthopedics, achieved a revenue of $1.456 billion last year, ranking first in the business segment with a growth rate of 7.1%.

Behind the rapidly growing financial data for knee joints, one aspect is directly related to the approval of the VELYS knee surgery robot and its rapid increase in sales in the European market. Another aspect is Johnson & Johnson'sRepositioning in the Knee Joint Field, adapting the VELYS surgical robot to work in conjunction with complementary products such as the Attune artificial knee, the TruMatch knee replacement surgery solution, the ACTIS stem cell artificial hip, the PINNACLE artificial ball-and-socket joint, and the KINCISE hip replacement surgery solution.Comprise a complete set of "hardcore" product ecosystem for Johnson & Johnson's orthopedic surgeries.

The approval of VELYS not only gives Johnson & Johnson's orthopedic business a breather in a highly competitive market but also helps it regain market share from competitors like Stryker. The new generation VELYS surgical robot compared to traditional orthopedic surgical robotsThe Advantage of Differentiation, but also has the opportunity to revitalize Johnson & Johnson.

The growth data brought by the VELYS knee surgery robot is also sufficient to explain why orthopedic giants such as Stryker and Medtronic are competing to enter the knee surgery robot field.

Currently, in terms of the approval of orthopedic products from major companies, apart from the recent approval of Johnson & Johnson's VELYS surgical robot, in the field of joint replacement,Stryker, Zimmer BiometHave also already occupied a place in the market, moreoverSmith & Nephew, Globus Medicalis also constantly catching up.

Stryker:Mako Orthopedic Surgical Robot

In 2017, Stryker launched the Mako system for total knee arthroplasty in the United States. It has now been widely used worldwide, with a global market share of 9%. The system has also received certification from the CFDA and is currently one of the few orthopedic surgical robots capable of performing joint replacements in China.

Zimmer Biomet: ROSA Knee Robotic-Assisted Surgical System

In 2019, Zimmer Biomet launched the ROSA Knee orthopedic surgery robot, which received FDA approval for knee surgeries. In May 2021, it won the Orthopedic Product Innovation of the Year award at the Healthcare Asia Medical Technology Awards.

Smith & Nephew: Cori Orthopedic Robot

In 2020, Smith & Nephew launched the orthopedic robot Cori, which received FDA approval. It is a handheld smart device controlled by surgeons, applicable for total knee replacement and unicompartmental knee replacement. In 2023, it was launched in China, becoming one of the first robotic systems in China to meet the recommended standards of the robotics industry.

In addition, another strong competitor in the field of joint replacement surgical robots is Globus Medical. Dan Scavilla, CEO of the company, said in the earnings call in November 2023 that they areAwaiting FDA Approval for Its Knee Robot,Expected to launch in the first half of 2024.

According to GlobalData analysis, robot-assisted knee reconstruction is one of the fastest-growing surgeries, with...Approximately 700,000 cases globally by 2030, with a compound annual growth rate of 8% from 2021 to 2030. The shift in the model of using surgical robots for orthopedic treatments has greatly driven the market growth rate.

According to relevant analysts' speculation, between 2011 and 2021, patient interest in robotic knee and hip replacement surgeries grew exponentially. With the increase in market penetration, these procedures are gradually becoming the primary treatment method for knee-related conditions in the market.

Let's bring the focus back toKnee Surgery Robot Market in China。

Currently, the number of robot-assisted joint replacement surgeries performed annually in China has increased from 0 in 2015 to 243 in 2020, and is expected to grow further at a compound annual growth rate of 162.8% starting from 2020.Increase to 79,964 units by 2026.

The large number of patients and surgeries has also spurred a broader market space for robot-assisted joint replacement in China. According to Frost & Sullivan, the market size in China is expected to reach 332 million US dollars by 2026, maintaining rapid growth with a CAGR (Compound Annual Growth Rate) of 68% during this period.

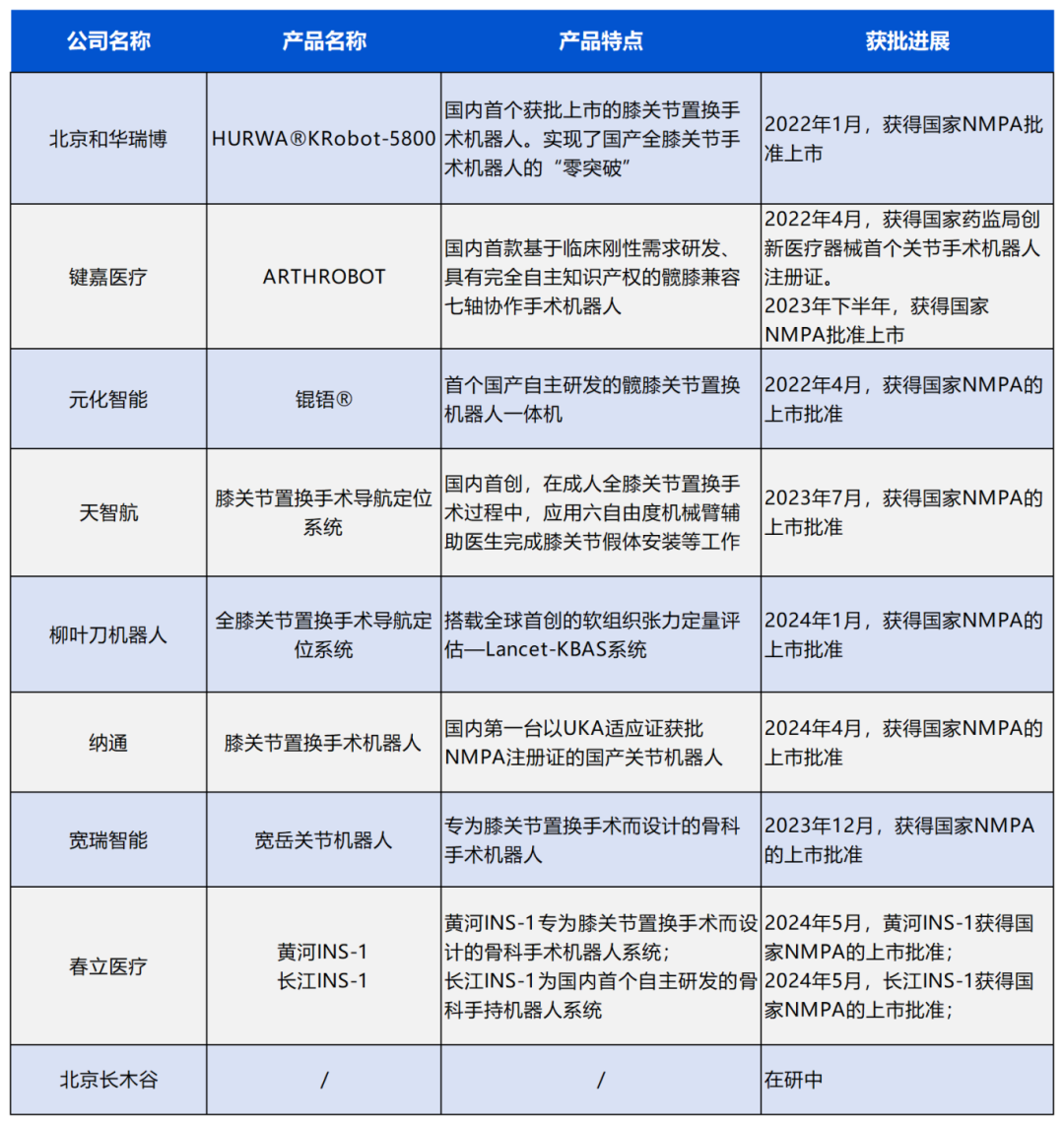

The rapid expansion of the market scale has not only intensified competition among overseas giants but also drivenMade in China BreakthroughAlthough the senior orthopedic surgical robot companies are mainly concentrated in Europe and the United States, and most domestic companies are still in the early stages of development in the medical surgical robot field, they are not willing to fall behind and are striving to catch up.

April 2022,Minimally Invasive®自主研发的鸿鹄®Skywalker®骨科手术机器人获得中国国家药品监督管理局(NMPA)的上市批准, becoming the first and only orthopedic surgery robot in China equipped with a domestically developed, proprietary intellectual property mechanical arm, and has been approved for marketing. It is also currently the first andThe only domestically produced orthopedic surgical robot to have simultaneously received certification and market approval from the NMPA (China), FDA (United States), and CE (European Union).

Notably, Honghu® Skywalker® is compatible with total knee arthroplasty (TKA) and total hip arthroplasty (THA), enabling precise intraoperative positioning, accurate knee osteotomy and acetabular grinding, and the precise restoration of the patient’s lower limb alignment. It achieves more accurate and efficient bone cutting, bone grinding, and prosthesis placement than traditional hip and knee replacement surgeries. Since the instruments for cup installation and knee osteotomy are basically the same as those used in traditional surgery, it significantly shortens the learning curve for surgeons, allowing for quick mastery and proficiency.

In addition to minimally invasive medical technologies, a large number of orthopedic companies in China have also emerged, focusing on the market for robotic-assisted knee surgery. Statistics show that at least 20 companies in China are developing robotic systems for knee replacement surgeries, includingMinimally Invasive Medical, Jiana Robotics, Chunli MedicalAnd other companies, as well as multiple joint robots under development in China.

(Only part of the data is displayed. If there are any errors in manual statistics, please contact us for modification.)

As orthopedic surgical robots from Chinese manufacturers have been successively approved, the industry landscape has also become more diversified. Behind the accelerated approval of domestically produced robots, it is precisely due to encounteringThe Collection and Procurement of Orthopedic Surgical Robot Consumables Accelerates the Trend of Domestic Substitution in China.

Starting from the end of July 2019, the centralized procurement of high-value orthopedic joint consumables began, with the average price decreasing from 30,000 yuan to less than 10,000 yuan, resulting in an overall reduction of more than 80%. The significant shrinkage in the artificial joint market share has unleashed the potential of other related markets.

Analogous to the burst of innovative fields such as balloon treatment and interventional robots after the centralized procurement of coronary stents, looking forward to the future from the current point of orthopedic consumables centralized procurement,Precision, digitalization, and intelligent methods in orthopedics will become new profit growth points and industry mega-trends.Innovative medical services dominated by surgical robots will also become an important part of future healthcare reform, bringing more vitality to medical institutions.

In addition,Policies have also given a strong boost to this robotics track.

The "13th Five-Year Plan Outline for the Development of the Orthopedic Robotics Industry" requires a 30% increase in the orthopedic robotics industry by 2020; the draft "Medical Equipment Industry Development Plan (2021-2025)" lists surgical robots as a key development area... Multiple policies encourage deeper exploration into robotics.

In March 2022, the National Healthcare Security Administration issued the "Guidelines for Improving the Pricing and Relevant Policies of Orthopedic 'Surgical Robots' and '3D Printing' Assisted Operations (Draft for Comments)," which further...Establishes norms and benchmarks for the industry.It is certain that domestically produced orthopedic robots are transitioning from unregulated growth to standardization and marketization, and truly outstanding products will emerge to continuously lead the field.

At the forefront of policy, what kind of orthopedic robotics companies can take the lead and become dark horses in this field? In fact, whether...Whether it's product development or commercialization, it's a tough battle for companies.

In product developmentThe foundation of orthopedic surgical robots is determined by the underlying technical capabilities of the product, which will decide the future upper limit.Taking Johnson & Johnson's VELYS robot as an example, the human-machine interaction algorithm barrier established through underlying technology, along with extensive clinical function module data processing methods, forms the core and differentiated competitive advantage of VELYS in commercialization.

The technical embodiment of the product focuses on clinical effectiveness as the core, namely, whether it can address the pain points of traditional surgery. Stability, precision, operational convenience, and compatibility with various surgical methods are all key concerns for doctors during usage. This also represents the core competitiveness that will define the future expansion of the orthopedic surgical robot market.

In terms of commercialization, it is necessary to achieve the scaled growth of robots on the basis of technology and clinical efficacy. Reasonable pricing and comprehensive supporting services are required to drive the healthy development of the enterprise's industrial chain.

Taking the domestically produced Lancet robot as an example, Its commercial strategy is similar to that of Johnson & Johnson. On one hand, its total knee replacement surgical robot has achieved excellent clinical performance in many well-known tertiary hospitals. On the other hand, it has comprehensively laid out its industrial chain and continuously extended its product lines. By promoting cross-departmental and multi-product line strategies, it has built a complete set of intelligent assisted surgery solutions, forming aA complete closed-loop commercialization solution, generating tens of millions in revenue.

Currently, in the global knee surgery robotics sector, giants such as Johnson & Johnson, Stryker, and Zimmer Biomet have embarked on a comprehensive competitive race. Meanwhile, China’s domestic knee surgery robotics industry is also about to enter a "harvest season" of widespread regulatory approvals. Driven by significant market demand and favorable policies, enhancing product innovation capabilities and strengthening commercialization strategies will be key to the rise of Chinese manufacturers.

The content of this article is for reference only and does not constitute investment advice. Readers are expected to effectively distinguish. Due to human factors, there may be some information gaps. If there are any issues with the company information, please contact us in a timely manner. Thank you for your understanding.The interpretation of policy-related content represents the views of this platform only, and the official documents shall prevail. If any platform reprints this article, it must take responsibility for the content of the article itself. Medical Device Business Review is not responsible for the impact caused by secondary dissemination after reprinting.

To improve the platform content and provide users with a better experience, Comment Master sincerely invites you to participate in our short survey. More valuable suggestions are welcome in the comment section~

*Advertisement

▼More Book Recommendations▼

If you find the content helpful, welcomeStar Mark、Like、Forward!

Your support is our greatest motivation