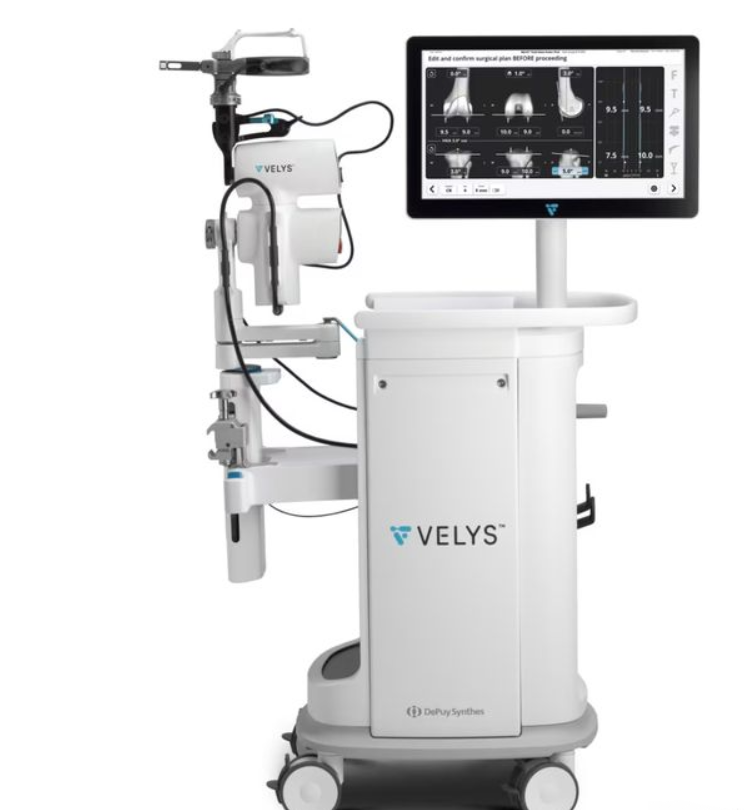

Recently, DePuy Synthes, the orthopedics division of Johnson & Johnson, announced that its Velys surgical robot has received approval from the U.S. Food and Drug Administration (FDA) for use in unicompartmental knee arthroplasty (UKA). This marks an expansion of the application scope of the Velys surgical robot in the field of orthopedic surgery, as it was previously approved in 2021 for total knee arthroplasty (TKA).

Rising Star in Robotics: The Rise of the Velys Surgical System

Background of the Velys Surgical Robot

DePuy Synthes, a subsidiary of Johnson & Johnson, is a global leader in orthopedic medical devices and solutions. Founded in 1895 through the merger of DePuy and Synthes, the company focuses on trauma, spine, joint reconstruction, sports medicine, and neurosurgery. DePuy Synthes is renowned for its innovative orthopedic products and technologies, including robotic-assisted surgery and 3D-printed implants, committed to improving surgical outcomes and patient quality of life. With operations in over 100 countries worldwide, it collaborates with top medical institutions and surgeons, continuously advancing orthopedic technology.

Advantages and Challenges of Unicompartmental Knee Arthroplasty

Unicompartmental Knee Arthroplasty (UKA) offers advantages such as preserving more natural bone and shortening recovery time. However, the procedure also faces several challenges, including surgical complexity, smaller incisions, and limited joint visibility, which contribute to a longer learning curve and variability in outcomes. The introduction of the Velys surgical robot aims to overcome these challenges through robotic-assisted technology, enhancing the precision and consistency of the surgery.

Innovation of VELYS Robotic System

- High-Precision Operation: The Velys robot and its Sigma HP knee implant system can provide accurate positioning during medial and lateral surgeries without the need for CT scans.

- Personalized Customization: Provide surgeons with actionable insights through data and real-time analysis, generate personalized surgical plans, thereby improving surgical outcomes and patient satisfaction.

- Reduced Postoperative Recovery Time: Due to the improved precision of the surgery, the surgical trauma is smaller, significantly shortening the patient's postoperative recovery time.

- Simplified Surgical Procedures: Complex surgical steps are streamlined through intelligent assistance and automation, enhancing operating room efficiency.

Two Powers Compete, Who Will Prevail

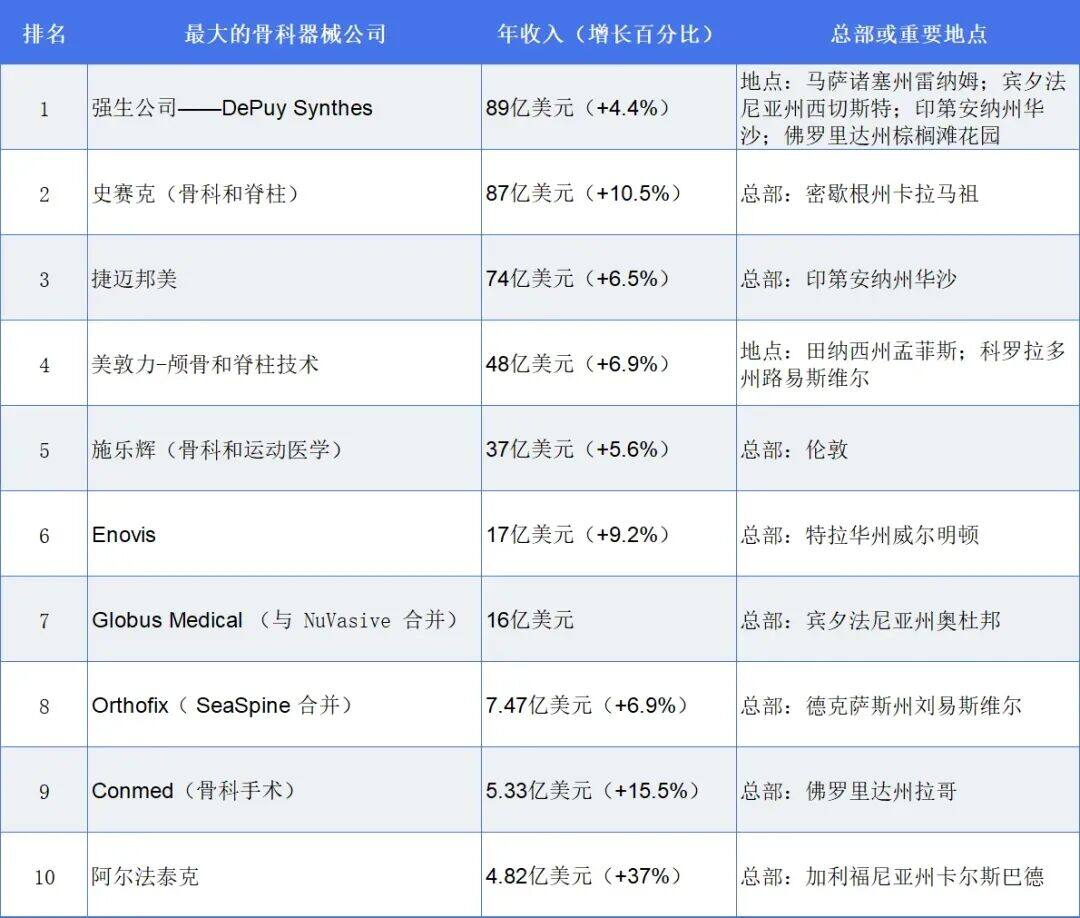

Johnson & Johnson's DePuy Synthes Achieved Remarkable Results Last Year, with Orthopedic Business Restructuring Helping It Become the Industry Leader. This Year, DePuy Synthes Has Become the World’s Largest Orthopedic Device Company. Since Its Approval in 2021, VELYSTM Has Completed Over 55,000 Orthopedic Surgeries Across 20 Countries and Regions Worldwide. In 2023, DePuy Synthes’ Revenue Growth Accelerated to 4.4%, but Stryker’s Orthopedics and Spine Business Grew Faster at 10.5%.

(Image source: Medical Device Innovation Network)As the largest competitor, Stryker is gaining strong momentum by popularizing its Mako robotic surgery system in knee and hip surgeries. Last year, the Mako system surpassed the milestone of 1 million surgeries globally. Its growth rate is expected to further accelerate, with plans to advance shoulder and spine applications by 2024. The success of Mako has prompted many of Stryker’s competitors to become more active in robotics and digital surgery, showcasing Stryker's solid leading position in the orthopedics field. Therefore, Stryker is expected to return to its peak next year, but the final market landscape remains to be seen.

A Bright Future for Orthopedic Surgical Robots

According to the latest industry report by market research and intelligence provider Fact.MR, the global orthopedic surgical robotics market is gaining strong momentum. The market size is expected to reach $2.35 billion by 2024 and continue to expand at a compound annual growth rate (CAGR) of 13.5% from 2024 to 2034.The growth of orthopedic surgical robots is primarily driven by the rising prevalence of osteoarthritis, with an increasing number of patients seeking total knee replacement surgery to alleviate pain and discomfort caused by the condition. As the elderly population grows, the incidence of orthopedic issues such as osteoporosis is also on the rise, further boosting the demand for surgical robots. By 2034, the global orthopedic surgical robot market is projected to reach $8.34 billion.In terms of regional market distribution, by 2034, the North American market is expected to account for 51.2% of the global market share. Of this, the United States will represent 94.4% of the North American market, with its orthopedic surgical robot sales projected to achieve a compound annual growth rate (CAGR) of 13.3%. The East Asian market also shows strong performance and is expected to grow at a CAGR of 15.8% between 2024 and 2034. With the continuous increase in patients suffering from orthopedic injuries and spinal diseases in China, the scale of China's orthopedic robot market is also steadily expanding. According to calculations by Eshare MedTech, the size of China’s orthopedic robot market reached 500 million yuan in 2022.By product type, the sales of disposable orthopedic surgical robots are expected to reach US$ 885.5 million by 2024. "Orthopedic surgical robots improve surgical accuracy, shorten operation time, thereby increasing success rates and enhancing patient experience. This is the main factor driving market growth," said analysts at Fact.MR.Despite the bright market prospects for orthopedic surgical robots, competition within the industry is also intensifying. As technology continues to advance, major companies are increasing their R&D investments and launching more advanced and efficient surgical robotic systems. The competition between Johnson & Johnson's DePuy Synthes and Stryker in this field is particularly fierce, with both actively expanding their product applications and market coverage.

For medical institutions and surgeons, choosing the right surgical robot system is not only related to the success rate of surgeries and the recovery speed of patients, but also affects the overall operational efficiency and economic benefits of the hospital. The challenges come not only from continuous technological innovation but also include how to strike a balance between cost-effectiveness and clinical outcomes. At the same time, companies must also face changes in market demand and adjustments in the policy environment. What does the future hold for orthopedic surgical robots? We will wait and see.

▲ Source of the article: Medical Device Innovation Network▲Please indicate the source above when reprintingDisclaimer: This article is intended solely for the purpose of information transmission and is for reference only. It does not constitute any advice on investment or treatment; please exercise caution. If it involves issues related to the content, copyright, or other aspects of the work, to protect the rights and interests of both parties, please contact us, and we will handle it immediately. If any platform reprints this article, it must take responsibility for the content itself; the Medical Device Innovation Network is not responsible for any secondary dissemination caused by the reprint.