Japanese Pharma Giants Ramp Up Big-Deal BD Activities Targeting Chinese Innovative Drugs

Ascentage Pharma

Clinical-Stage Biopharmaceutical Developer

Takeda

Biopharmaceutical Manufacturer

Eisai

Pharmaceutical Product R&D and Manufacturer

Daiichi-Sankyo

Pharmaceutical R&D Developer

Recently, the domestic small-molecule oncology drug sector witnessed the largest BD deal in its history.

June 14,Ascentage Pharma and Takeda Pharmaceutical Company Limited Reach Exclusive Licensing Agreement for OlverembatinibAscentage Pharma will receive "a $100 million option payment + up to approximately $1.2 billion in potential option and milestone payments + double-digit percentage royalties." At the same time, Takeda Pharmaceutical Company Limited will subscribe to $75 million worth of newly issued shares of Ascentage Pharma, becoming the company's second-largest shareholder.

This is not the first time that Takeda has licensed in a pipeline of innovative drugs from China. As early as January 2023,Takeda Acquires Global Rights to HUTCHMED's Fruquintinib for $1.16 BillionRecently, Fruquintinib has been officially approved to enter the European market, becoming the first original Chinese drug to successfully enter the two major benchmark markets of the United States and Europe.

In fact, Takeda is not the only Japanese pharmaceutical company that has closely cooperated with China's innovative drug sector recently. In the past year, includingDaiichi Sankyo, Astellas, Eisai, Taiho Pharmaceutical, Chugai PharmaceuticalAll have experience in BD China's innovative drug development. Taking Taiho Pharmaceutical as an example, in March 2024, it reached an exclusive licensing agreement with Haihe Biopharma for Glumetinib tablets. Three months later, the drug was officially approved for marketing in Japan.

Behind the frequent exchanges between Chinese and Japanese pharmaceutical companies, industry insiders have also begun to speculate:Japanese pharmaceutical companies are showing a trend of becoming the super big buyers of China's innovative drug pipelines.This is not without basis. According to the 2023 corporate reports disclosed by several major Japanese pharmaceutical companies, "In the next five years, the proportion of overseas sales revenue is planned to exceed 50%, with overseas business mainly referring to business in China."

Not Looking at Traditional Chinese Medicine but at Innovative Drugs: Why Have Japanese Pharmaceutical Companies Changed Their Minds?

Before innovative drugs, Japanese pharmaceutical companies were actually more focused on Chinese herbal medicine in China.

InTsumura & Co.For example, in April 2021, Tsumura & Co. spent 1.2 billion yuan to acquire Tianjin Shengshi Baicao Chinese Herbal Medicine Technology Co., Ltd., a company specializing in prepared Chinese medicinal slices; in March 2023, Tsumura & Co. invested in the expansion of the Tianjin Chinese Medicine Industrial Base project; one month later, Tsumura & Co. acquired Ziguang Chenji, a well-known Chinese medicine brand in China, for 250 million yuan. It is reported that Tsumura & Co. has currently established more than 70 GAP (Good Agricultural Practice) herbal planting bases in China, whereas Tongrentang only has 12 GAP bases, showing a significant difference in numbers.

And besides Tsumura,Hisamitsu Pharmaceutical, Ota Seisan, Mitsui & Co., Ltd., Rohto PharmaceuticalJapanese giants such as Takeda have frequently acquired Chinese traditional medicine enterprises. For instance, in April 2024, Rohto Pharmaceutical, together with Mitsui & Co., invested $594 million to acquire 86% of the shares of the traditional Chinese medicine enterprise "Eu Yan Sang."

Of course, behind the large-scale acquisitions, Japanese pharmaceutical companies have also made a fortune. According to statistics, nowadays, more than 70% of global patents for traditional Chinese medicine have been occupied by Japan's "Kampo medicine," and over 80% of the 60,000 pharmacies in Japan sell Kampo formulations.

However, this has not drawn excessive attention from Japan's top 10 pharmaceutical companies, including Takeda, Otsuka Holdings, Astellas, and Daiichi Sankyo, none of which currently have relevant investments in traditional Chinese medicine. Instead, they have developed a strong interest in China's innovative drugs and are making aggressive moves. So, what exactly is the reason behind this?

Firstly, it is limited by the fierce competitive environment of Japanese traditional Chinese medicine.According to statistics, there are currently over 200 Kampo medicine enterprises in Japan. Of the international market for Chinese patent medicines, which is worth between 16 billion and 20 billion US dollars annually, Japan occupies over 80% of the share. However, this is mainly concentrated in leading companies such as Tsumura and Kracie, making it difficult for newcomers to gain a foothold. Additionally, the overly rapid expansion of Japanese Kampo medicines has led to ongoing issues in the industry, such as the fatal incident involving Kobayashi Pharmaceutical and the well-known gastrointestinal medicine "Seirogan" being ordered to halt production and sales due to falsified test data, all of which have brought considerable controversy to Kampo medicines.

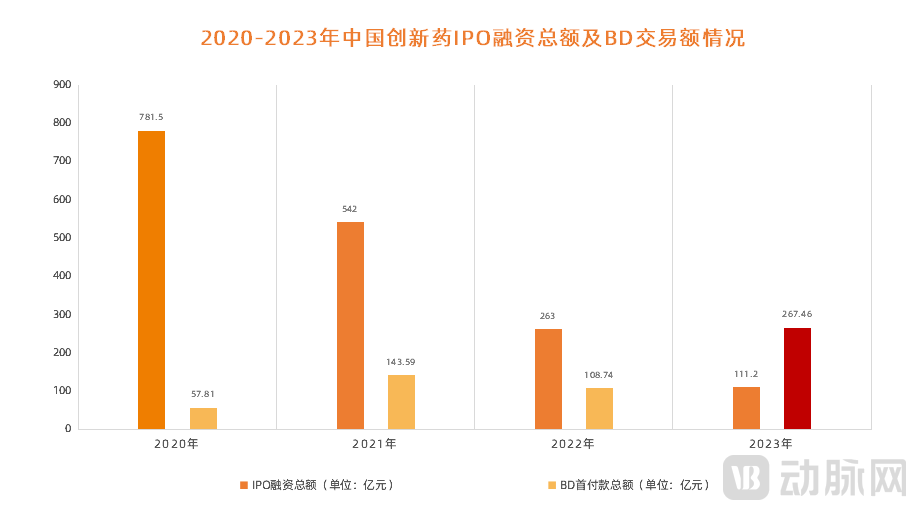

Figure 1. Total IPO Financing and BD Transaction Amount of China's Innovative Drugs from 2020 to 2023 (Data Source: PharmaCube)

Figure 1. Total IPO Financing and BD Transaction Amount of China's Innovative Drugs from 2020 to 2023 (Data Source: PharmaCube)

Secondly, China's innovative drugs are sparking an "overseas wave," with BD remaining highly active.In 2023, two key data points of China's innovative drug sector have been particularly eye-catching: First, the number of License-out transactions. According to statistics from VCBeat, in 2023, China had nearly 70 License-out transactions for innovative drugs, representing a 32% increase over 2022 and surpassing the number of License-in projects for the first time. Second, the total amount of BD (Business Development) deals. In 2023, Chinese innovative drug companies received an aggregate upfront payment of RMB 21.021 billion through project BD deals, surpassing the total amount raised via IPO channels for the first time and nearly doubling it. These developments provide unprecedented opportunities for Japanese pharmaceutical companies to make significant inroads into the Chinese market.

Finally, there is a high degree of similarity between Chinese and Japanese pharmaceutical companies in the field of disease research.It is reported that two innovative Chinese drugs recently licensed in by Takeda, Olverembatinib and Fruquintinib, as well as Glumetinib introduced by Taiho Pharmaceutical, are all anti-tumor drugs. Oncology is also one of the key pipelines focused on by pharmaceutical companies in both China and Japan. According to "Global Oncology Trends 2023: Outlook to 2027," in 2022, products under development by companies headquartered in China accounted for 23% of the oncology R&D pipeline, up from 10% five years ago and 3% in 2007, surpassing Europe for the first time. Similarly, in Japan, the top 10 pharmaceutical companies have heavily invested in the oncology field, which is also a major source of their revenue.

So, all things considered, under the current specific market environment, Japanese pharmaceutical companies are highly likely to become a significant force in China's innovative drug mergers and acquisitions and business development (BD). In fact, there are already some signs of this. Apart from frequent BD transactions, the presence of Japanese pharmaceutical companies has notably increased at major conferences and exhibitions in China. At the same time, the number of visits by representatives of Chinese enterprises to Japan is also on the rise.

The Rise of Japanese Pharmaceutical Companies Cannot Be Separated from "Buy, Buy, Buy"

As is known to all, Japan is the world's third-largest pharmaceuticals market. According to the article "Drug Development Strategy in Japan 2021" in Credovo magazine, Japan's pharmaceutical market reached 136 billion US dollars in 2020.In the 2023 "Top 50 Global Pharmaceutical Companies" ranking, Japan also occupies six seats, namely Takeda, Astellas, Otsuka, Daiichi Sankyo, Chugai Pharmaceutical, and Eisai.。

Figure 2. Operating Conditions of Japan's Top Ten Pharmaceutical Companies from April 2023 to March 2024 (Data Source: AnswersNews)

Figure 2. Operating Conditions of Japan's Top Ten Pharmaceutical Companies from April 2023 to March 2024 (Data Source: AnswersNews)

Of course, all of this is inseparable from the significant efforts made by Japanese pharmaceutical companies in mergers and acquisitions. According to reports, there have been two major BD deals in the history of Japan's pharmaceutical industry. One came from Takeda, which acquired Shire for $64 billion in 2019 in a "snake swallowing an elephant" move. This deal not only solidified its position as the global leader in rare diseases but also propelled Takeda into the top twenty pharmaceutical companies worldwide. The other deal came from Daiichi Sankyo, whose co-development of the strongest ADC drug DS-8201 with AstraZeneca elevated it to become the highest market-valued pharmaceutical company in Japan.

And until now,Japanese pharmaceutical companies are still in a frenzy of "buying up" global innovative drug assetsIn May 2023, Astellas spent $5.9 billion to acquire IVERIC Bio; in October 2023, Kyowa Kirin spent $477.6 million to acquire Orchard Therapeutics; in May 2024, Asahi Kasei acquired Callidita for approximately $1.1 billion... There are many similar transaction cases.

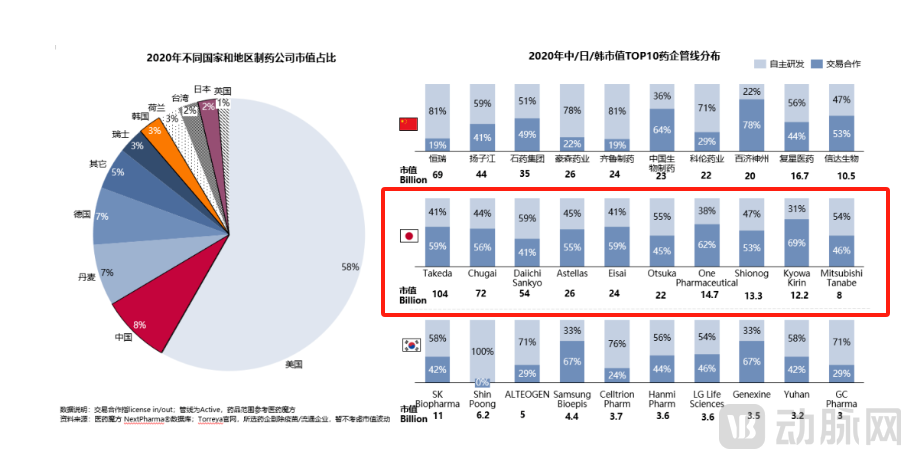

Figure 3. Pipeline Distribution of Top 10 Pharmaceutical Companies by Market Value in China, Japan, and South Korea in 2020 (Image Source: PharmaCube)

Figure 3. Pipeline Distribution of Top 10 Pharmaceutical Companies by Market Value in China, Japan, and South Korea in 2020 (Image Source: PharmaCube)

This trend can also be clearly perceived from the composition of Japanese pharmaceutical companies' pipelines. According to the report, the proportion of pipeline transaction cooperation among Japan's top 10 pharmaceutical companies is significantly higher than self-developed, with Takeda, Chugai Pharmaceutical, Astellas, Eisai, Ono Pharmaceutical, and Kyowa Kirin having a transaction cooperation ratio close to 60%.

So, what exactly is driving Japanese pharmaceutical companies to keep indulging in "buying sprees"?

It is reported that in the history of Japan's pharmaceutical industry development,Have had two experiences of collective overseas trips.The first time can be traced back to the 1980s. As Japan's economic growth slowed and the aging population problem became increasingly severe, the Japanese government began to control drug prices. Starting from 1988, drug prices across China were reduced every two years, with an average decrease of over 6% each time. Affected by this, the domestic businesses of several pharmaceutical companies in Japan declined significantly. In order to seek survival and development, they had to accelerate overseas expansion, officially ushering in the "Me-too" era.

It is also in this era that Japanese pharmaceutical companies have experienced a comprehensive boom, with their scale rapidly expanding and reaching a peak around 2010. The top five pharmaceutical companies, represented by Takeda and Daiichi-Sankyo, successively entered the global TOP30. In this regard, industry insiders stated, "The successful feat of Japanese companies' Me-too drugs going overseas in those years is even hard for them to replicate.。”

Perhaps due to being overly successful, directly harming the commercial interests of American pharmaceutical companies, the FDA subsequently tightened the approval of Me-too drugs. In 2010, Me-too drugs successively entered the patent cliff period, causing a significant drop in sales and profits for many Japanese pharmaceutical companies.

It was during this period of confusion that,The Second Collective Overseas Expansion of Japanese Pharmaceutical Companies — The Trend of Generic Drug Export is EmergingThis mainly started in 2008, when Takeda acquired U.S.-based Millennium Pharmaceuticals for $8.8 billion; Eisai acquired U.S.-based MGI Pharma for $4 billion; and Daiichi-Sankyo acquired Ranbaxy for $4.6 billion... Japanese pharmaceutical companies have been entering overseas markets through generic drugs. According to statistics from Japan's Ministry of Health, Labour and Welfare (MHLW), the substitution rate of generic drugs in Japan reached 72.6% in 2019.

This is no coincidence. In this regard, a professional analyzed the successful experience of Japanese pharmaceutical companies' mergers and acquisitions for VCBeat. He mentioned, "In addition to specific era factors, the cumulative products of Japanese pharmaceutical companies themselves and the gradual opening of the domestic market have provided prerequisites for their mergers and acquisitions. Moreover, the M&A model that Japan has explored over half a century—Enter developed markets with innovative drugs, find commercial entry points through strategic acquisitions and mergers, establish joint ventures, leverage their local marketing networks to quickly open up the market, and gradually form independent company operations in the later stage., which also reduces transaction risks and opens up more possibilities."

China's Innovative Drugs: The Next Stop for Japanese Pharmaceutical Companies

Historically, the U.S. innovative drug market has been the "main battlefield" for Japanese pharmaceutical companies' mergers and acquisitions. This is partly because the U.S. possesses more mature pipelines, which can enhance R&D capabilities while also expanding product portfolios. On the other hand, it is based on considerations of market expansion. Through the vast commercial platform and market entry point that the U.S. offers, Japanese pharmaceutical companies can accelerate their expansion into the global market.

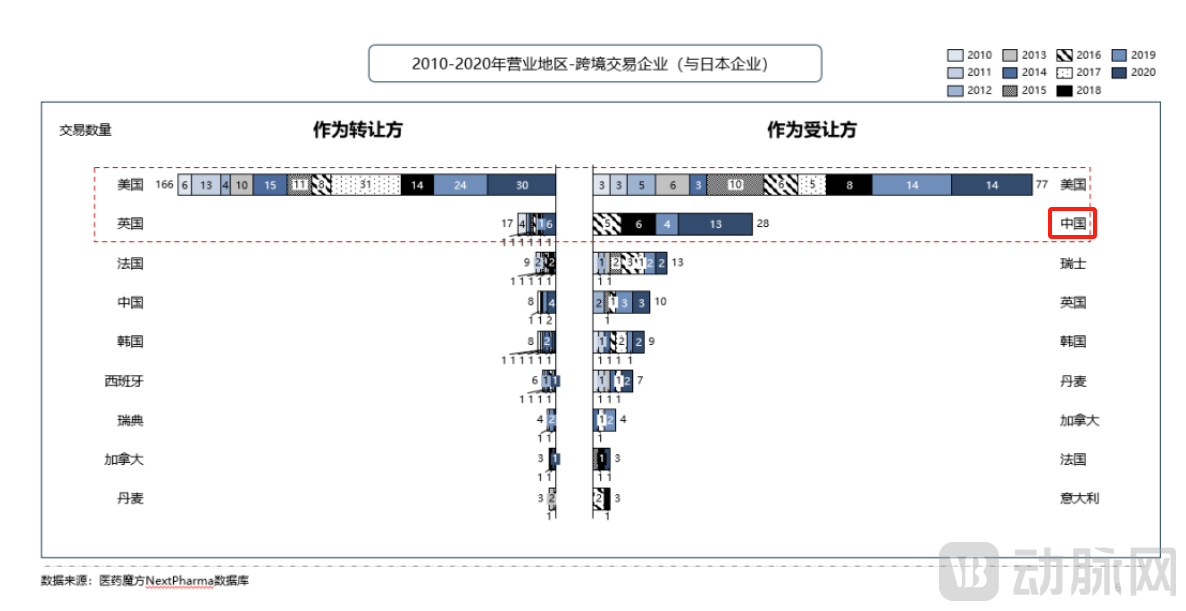

Figure 4. 2010-2020 Operating Regions - Cross-Border Trading Enterprises [Japan] (Image Source: PharmaCube)

Figure 4. 2010-2020 Operating Regions - Cross-Border Trading Enterprises [Japan] (Image Source: PharmaCube)

However, in the current highly competitive environment, Japanese pharmaceutical companies also hope to develop the second-largest trading market outside the United States. Based on the number of transactions and their value in recent years, they have mainly set their sights on China. According to incomplete statistics from the PharmaCube NextPharma database,From 2018 to 2020, there were 23 licensing deals between Chinese and Japanese pharmaceutical companies, involving a total amount exceeding 30 billion yuan.。Coupled with several large transactions recently, Japanese pharmaceutical companies are increasingly engaging with China's innovative drug market.

Of course, all this is based on a certain foundation. First of all, for Japanese pharmaceutical companies, entering China's innovative drug market is not only to get rid of the dependence on the single American market,Another key point is that China's innovative drugs are starting to feature more pipelines with certainty, which will partly offset market losses caused by product patent cliffs.。

Taking Takeda as an example, the introduction of Ascentage Pharma's Olverembatinib this time is actually a complement and continuation of its own hematological tumor pipeline. This is because the patent for Takeda's globally first third-generation BCR-ABL inhibitor, Ponatinib, will expire around 2026, and Olverembatinib can seamlessly compensate for the losses brought by the patent cliff of Ponatinib. Of course, Olverembatinib can also firmly establish itself in the market. It not only has obvious generational advantages over first- and second-generation BCR-ABL inhibitors but is also effective for CML patients who are resistant or unresponsive to Ponatinib and Asciminib, with significantly improved safety. It is a potential billion-dollar molecule, with estimated peak sales of $1 billion to $1.5 billion.

And besides having a high-quality pipeline with certainty,The gradually opening-up cooperation model in China's innovative drug market has also gained favor from Japanese pharmaceutical companies.In this collaboration between Takeda and Ascentage Pharma, in addition to the pipeline deal, Takeda also acquired shares in Ascentage Pharma, becoming its second-largest shareholder. This approach not only allows investors to gain a voice at a relatively low cost but also provides the target company with an opportunity to continue operations, benefiting both parties in terms of business development (BD). In fact, this method has already seen successful cases in China's innovative drug market, such as Amgen's $2.7 billion investment in BeiGene in 2019 to become the company’s largest shareholder, and Sanofi's €600 million investment in Innovent Biologics in 2022.

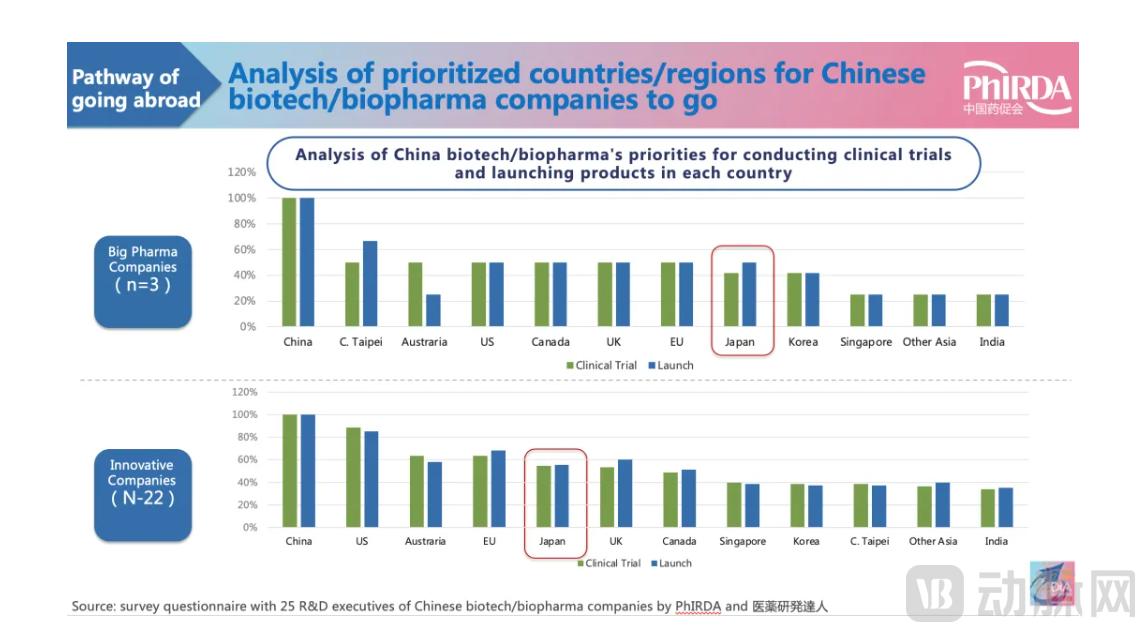

Figure 5. Market Priority Levels for Chinese Pharmaceutical Companies Conducting Clinical Trials and Registering Products Overseas (Image Source: China Pharmaceutical Innovation and Research Development Association)

Figure 5. Market Priority Levels for Chinese Pharmaceutical Companies Conducting Clinical Trials and Registering Products Overseas (Image Source: China Pharmaceutical Innovation and Research Development Association)

Of course, for China's innovative drug industry, entering the Japanese market is also a good option. First, China and Japan share many similarities in pharmaceutical policies, genetic factors, disease profiles, and more. Secondly, Japan has a number of large pharmaceutical enterprises with strong buying power and willingness, and they are increasingly focusing on China's innovative drug market. Lastly, economic benefits are another factor: China and Japan are geographically close, which helps reduce both time and financial costs. However, the intermittent impacts of geopolitics and national policies cannot be ignored.

But no matter what, it is certain that "marriages" between the pharmaceutical industries of China and Japan will occur on a large scale in the future, benefiting China's innovative drug exports and BD (Business Development).

1. "The Super Buyer of China-Produced Innovative Drugs" —— Gazelle Society;

2. "Record-breaking BD in Small Molecules" — Archimedes Biotech;

3. "Comparison of Pharmaceutical BD Transactions in China, Japan, and South Korea" — PharmaCube.

4. "The International Journey of Traditional Large Pharmaceutical Companies: Timing and Ambition" — Amino Observation.