Domestic Ophthalmic Devices Surge with Continuous Industry Funding and Breakthrough Innovations

Eyebright Medical

Ophthalmic Medical Product R&D Provider

TowardPi

High-end Ophthalmic Medical Device Developer

Vision Pro

High-end Ophthalmic Consumables Developer

In the current generally cold medical primary market, the investment and financing in ophthalmology remains unusually active.

According to the VCBeat database, from January 1 to October 10, 2024, there have been 34 financing events in the ophthalmology primary market, nearly equal to last year's count, placing it among the leading segments within the medical industry.

Particularly noteworthy is the rise of industrial funds in the ophthalmology track among investment participants.Aier Eye Hospital, as one of the earliest chain institutions to establish an industry fund, has participated in the establishment of seven industrial M&A funds and institutions, leveraging 7 billion yuan of industrial capital; In November 2023, Heshi Eye Hospital participated in an ophthalmology industry fund; OK Lens leader OcuScience has invested over 700 million yuan in recent years, forming an investment matrix of a listed company plus four funds; Eyebright Medical, a leader in ophthalmic medical devices, has also participated in multiple funds...

From the past focus on market VC/PE investments to the current large-scale support from industrial capital, the ophthalmology industry is ushering in a new round of industrial incubation. Behind this shift lies the trend of building ecosystems for stronger collaborations within the industry, as well as the continuous evolution of ophthalmic technologies and products from the previous Fast Follow, Me too approach towards Me better and First in class innovations, bringing new growth opportunities to the sector.

At the same time,In the product sector, the progress in the ophthalmology industry is even more encouraging.Only in September this year, China-produced innovative brands have made new breakthroughs in multiple mid-to-high-end ophthalmic equipment and high-value ophthalmic consumables fields: Eyebright Medical received the "first China-produced" dual-channel high-speed vitrectomy head registration certificate; TowardPi launched its digital holographic swept-source OCT intraoperative navigation microscope for the first time; Wuxi Vision Pro Ltd.'s first China-produced trifocal intraocular lens independently developed officially hit the market...

Moreover, whether it's companies or investors, they are placing increasing emphasis on original innovation. During VCBeat's participation in this year's CCOS conference (the 28th Chinese Ophthalmological Society Congress of the Chinese Medical Association in 2024), it was discovered thatAlmost all manufacturers and investors are talking about root technology innovation.They believe that only by conducting forward research and development from the underlying root technology can they break through the limitations and blockades of ophthalmic patents, and truly stand shoulder to shoulder with international giants. This is the most crucial "battlefield" for domestic brands at present and in the future.

There is no doubt that the continuous establishment of the ophthalmology industry ecosystem, along with the constant emergence of innovative products, has given ophthalmology investors the strongest confidence to refuse to "lie flat."

As a very special organ of the human body, the eye, due to its complex optical properties, relies heavily on related equipment for the diagnosis and treatment of diseases.

"In clinical settings, the main equipment types in general departments usually do not exceed 10 kinds, while in ophthalmology, there are more than 30 types, making it one of the departments with the richest variety of equipment." Senior investor Li Yang (a pseudonym at the request of the interviewee) told VCBeat, "The number of people suffering from eye diseases is constantly increasing, so the usage and demand for ophthalmic equipment and consumables are continuously rising."

▲ Ophthalmic Instruments Partial Product Illustration Product images are from the official websites of various companies.

▲ Ophthalmic Instruments Partial Product Illustration Product images are from the official websites of various companies.

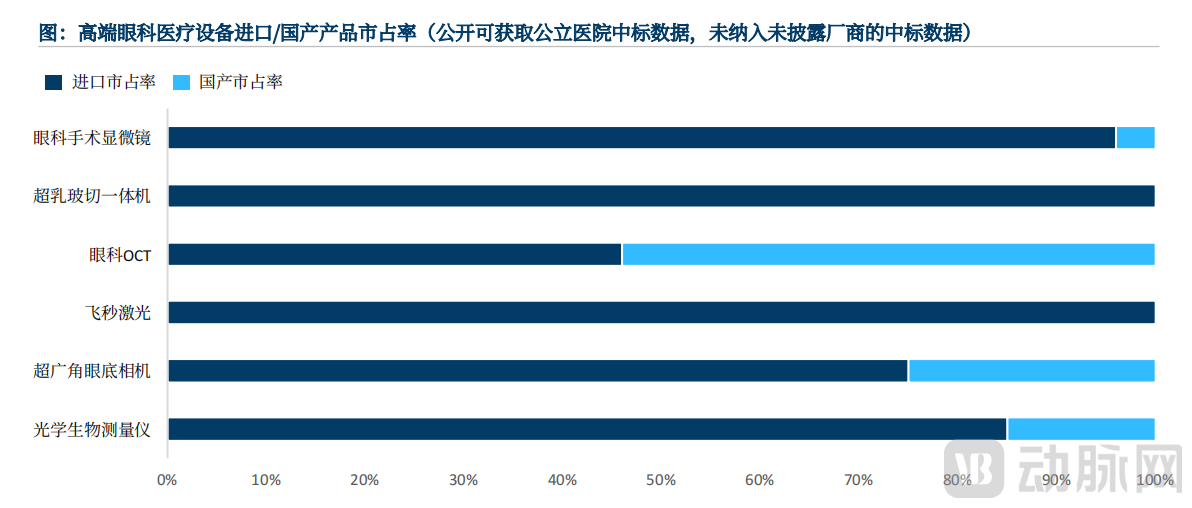

However, on the supply side, China's ophthalmic medical device sector has long been plagued by an extremely high rate of import monopolization.For example, in the field of ophthalmic medical devices, according to a 2021 survey by VCBeat, the market share of imported ophthalmic equipment suppliers accounted for as high as 98% based on sales revenue. Even when calculated by sales volume, this proportion exceeded 90%.

These products are almost exclusively from global top-tier brands, including ZEISS, Alcon, Topcon, Heidelberg, Canon, and other long-established high-end manufacturing giants from Germany, Japan, and the United States. Taking ZEISS as an example, in 2020, its femtosecond laser products held nearly 60% of the market share in China, ophthalmic surgical microscopes reached nearly 70% market share, and ophthalmic OCT achieved nearly 30% market share.

Behind the extremely high import monopoly rate lies an extremely high technical barrier. According to the founder of a domestic ophthalmic equipment innovation company who previously told VCBeat,The research and development and manufacturing of ophthalmic instruments is a typical track that is "easy to get into, but hard to master" and "low-end with low barriers, high-end with high barriers."

But thanks to the continuous efforts of China's innovative forces in recent years, China's ophthalmic device products (especially in the fields of high-value ophthalmic consumables and mid-to-high-end equipment) are experiencing a strong rise.

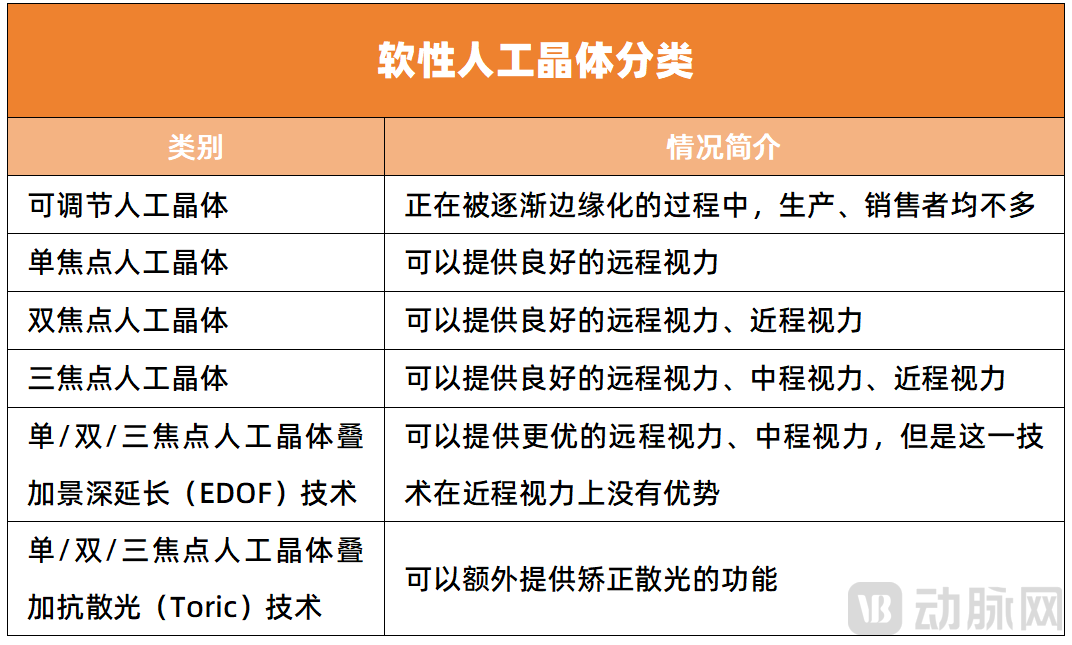

For example, in the field of high-value ophthalmic consumables, the research and development of artificial lenses is accelerating, and the gap with international giants continues to narrow.As an artificial lens made of polymer materials that can be implanted in the eye, intraocular lenses are used to replace the natural lens removed during cataract surgery. They are also the most widely used artificial organs and implantable medical devices worldwide. These lenses can be categorized into rigid intraocular lenses and soft intraocular lenses based on the material.

Currently, common soft intraocular lenses can be further divided into monofocal intraocular lenses, bifocal intraocular lenses, trifocal intraocular lenses, intraocular lenses with extended depth of focus technology, and intraocular lenses with astigmatism correction technology. Among them, monofocal lenses can only address the issue of lens opacity but cannot solve common problems such as myopia, hyperopia, or presbyopia for patients. However, bifocal and trifocal lenses can provide patients with more visual ranges.

▲ References:SIYU Medical Device ObservationVCBeat Mapping

The trifocal intraocular lens market in China is mainly dominated by Zeiss and Johnson & Johnson Vision. In this field, the AT LISA TRI 839MP model of intraocular lens under Zeiss is the primary choice for domestic patients. This lens model is made from hydrophilic acrylate material and adopts an aspheric structure. Previously, there was no truly domestically produced trifocal intraocular lens available in China, with constraints mainly lying in material design, optical design, and product registration.

In September, Vision Pro announced the official launch of its self-developed first domestically produced trifocal intraocular lens — ShiQuanJi®. This marks the beginning of the application of domestically produced trifocal lenses. Together with the bifocal intraocular lens previously launched by Eyebright Medical, the penetration rate of high-end domestically produced intraocular lenses is expected to increase, comprehensively accelerating domestic substitution.

In the field of high-end ophthalmic equipment, the development of phacoemulsification and vitrectomy devices is reaching an internationally advanced level, gradually reversing the monopoly of imported products.In ophthalmic clinical practice, vitrectomy is one of the most advanced surgeries in ophthalmology and is typically classified as a Level IV surgery. This procedure involves operations on the posterior segment of the eye, including the removal of the vitreous body and possible retinal manipulations. The advent of vitrectomy machines and vitrectomy probes has provided significant support for this surgery, but the development of related equipment is extremely challenging, and previously, there were no domestically produced brands in this field.

Also in September, the disposable vitrectomy cutter developed by Eyebright Medical received NMPA marketing approval. This is the first domestically developed vitrectomy cutter produced in China and the world's second dual-pneumatic vitrectomy cutter with a base cutting speed of 10,000 cuts per minute (cpm). (Based on cutting speed, current mainstream vitrectomy cutters are categorized into 5,000 cpm, 7,500 cpm, and 10,000 cpm; the higher the cutting speed, the less disturbance to the retina during surgery, thus ensuring greater safety.) Meanwhile, the vitrectomy machine independently developed by Eyebright Medical has entered the application phase and is expected to be approved early next year. In the field of phacoemulsification and vitrectomy, domestically produced equipment is achieving significant breakthroughs.

In addition to the two products mentioned above, domestic brands have also made new progress in many other fields.For example, in the field known as the "aircraft carrier" of ophthalmic medical devices—ophthalmic surgical microscopes—the digital holographic swept-source OCT intraoperative navigation microscope from TowardPi, a domestically produced brand, was first launched in September. This indicates that the era of high-end Chinese ophthalmic surgical microscopes is arriving at an accelerated pace.

The absolute dominant position in the market for all-femtosecond laser refractive surgery equipment has long been occupied by foreign brands. Among them, Carl Zeiss's product, VisuMax®, is the world's only device capable of performing all-femtosecond laser refractive surgery. In this area, domestic research and development progress is rapidly catching up. In May this year, the first domestically produced "femtosecond laser corneal refractive surgery equipment" (Finevision2000), independently developed by Xianwei Vision with 100% proprietary intellectual property rights, was mass-produced in Nanjing. It has currently completed nearly a thousand animal experiments and laboratory studies and is advancing with registration clinical trials.

Ophthalmic Optical Biometers Use Non-Contact Methods for Measuring Anatomical Features of the Eye, Accurately Measuring Axial Length (AL), Anterior Chamber Depth (ACD), Corneal Curvature (Km), Lens Thickness (LT), White-to-White Corneal Diameter (WTW), and Other Ocular Biometric Parameters. Therefore, They Are Widely Used in Clinical Fields Such as Preoperative Examinations for Cataract Surgery and Axial Length Measurements for Refractive Errors. In May This Year, Intalight Saiwei Released Its Second-Generation Visual Swept-Source Biometry Technology. According to the Official Introduction, This Technology Provides a 9mm Range Full-Corneal Topography, Offering More Comprehensive Information for IOL Selection and Demonstrating Strong Evaluation Capabilities Both Before and After Cataract Surgery.

Behind the continuous emergence of products is the rapid commercial scaling.Taking ophthalmic OCT as an example, the research conducted by VCBeat found that in 2022, among the OCT devices listed on public hospital procurement platforms (national and provincial procurement networks), a total of 485 units were awarded, with 467 traceable units. Among the traceable ophthalmic OCT products, domestically produced ones accounted for 45%, which is approaching half, showing a clear trend of domestic substitution. Notable companies such as Big Vision Medical, Intalight Saiwei, Morion Medical, TowardPi Medical, Weiren Medical, and Zhiding Medical have emerged (listed in alphabetical order based on the pinyin initials of company names). Meanwhile, the progress of domestic substitution in multiple niche fields is also accelerating.

▲Image Source: "2024 Blue Paper on the Current Status and Future Development Trends of the High-End Ophthalmic Medical Device Industry"

▲Image Source: "2024 Blue Paper on the Current Status and Future Development Trends of the High-End Ophthalmic Medical Device Industry"

It is not difficult to find that in the field of high-value ophthalmic consumables and mid-to-high-end equipment, domestically produced innovative products are "blooming in multiple areas." At the same time, the continuously expanding product lines and daring, innovative domestic newcomers provide ophthalmology investors with a sufficiently rich selection of high-quality investment targets.

“Root technology is the source of enterprise development and industry development."A high-end ophthalmic device product can command a high price for only two reasons: either it is the only one in the industry, or it is the best in the industry." During the CCOS conference, a founder of a listed company in the ophthalmology industry made such a statement.

What is Root Technology? It refers to a technology that can derive and support one or more technology clusters. In other words, root technology is the root of the technology tree, continuously nourishing the entire technology tree and largely determining its prosperity or decline.

For example, in the TMT field, the Android system is the "root" of the Android mobile phone industry; the Microsoft Windows operating system is the "root" of PCs; and the Ethereum ERC20 protocol is the "root" of many cryptocurrencies.

“Innovative enterprises with root technology advantages have greater potential in the future and are more favored by investors."Senior investor Li Yang said, 'On the one hand, these companies have stronger R&D capabilities and accumulation, enabling them to break through the restrictions and blockades of international giants' patents and compete head-on with imported brands; on the other hand, fundamental technologies allow them to expand into more product lines. In the future, they will not be limited to ophthalmology alone, which can better mitigate market risks.'"

However, the R&D difficulty of root technology is also extremely high. A founder of ophthalmic equipment mentioned that if an enterprise insists on forward R&D from the underlying root technology, the time cycle will be extended, making every decision in this process extremely critical. Because once the decision direction is wrong and the technology route goes awry, the result is spending hundreds of millions of yuan and five to six years of effort, only for the final product to fail to meet market expectations.

Therefore, to continuously advance in the underlying root technology pathway, it requires even greater strategic determination from participating companies, as well as the support and patient companionship of the industry ecosystem.

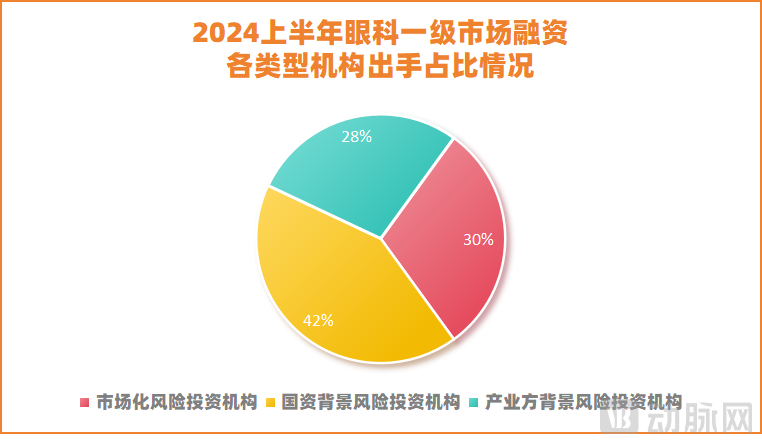

Obvious changes are taking place in the ophthalmology medical primary market.

According to data from the VCBeat database, in the first half of 2024, among the financing events in China's ophthalmology sector, state-owned venture capital institutions accounted for about 42%, market-oriented institutions accounted for about 30%, and industry background institutions represented by CVCs accounted for about 28% (approximately 25% in 2023), with the latter continuing to increase.

▲VCBeat Mapping

▲VCBeat Mapping

Behind the surge of industrial capital entering the market lies the industry's great expectation for building an industrial ecosystem.

Taking Oupu Kangshi, a leading company upstream, as an example, the company has invested nearly 1 billion yuan and formed an investment matrix of "listed company + four funds," continuously making moves in fields like ophthalmic devices: along the ophthalmology and optometry industry chain, Oupu Kangshi’s investments cover multiple segments including prevention and treatment, screening, surgery, and drug therapy, selecting products with technological advancement and market potential.

Specifically, Orthokon's investment in Guangzhou Visionbright focuses on applying AI technology to develop visual function and glasses-free 3D products; Guangzhou卫视博develops artificial vitreous and retinal reinforcement products, with its representative product, the foldable artificial vitreous balloon, being an internationally pioneering artificial organ for eye preservation that can precisely simulate the structure and function of the human vitreous body; and Diovision Medical has developed a microscopic surgical robot...

He's Ophthalmology, downstream in the industry, has also recently signaled its intention to participate in the co-construction of the industry ecosystem. "As He's Ophthalmology advances steadily, we will actively collaborate with all parties in the ophthalmology industry to strengthen alliances and expand, optimize, and enhance the industrial ecosystem," said Zhou Jinfeng, Secretary of the Board of Directors of He's Ophthalmology, at the Ophthalmic Device Industry Development Forum held concurrently with the CCOS conference.

In specific areas, He's Eye Care will continue to communicate and interact with innovative companies in the fields of high-end equipment, consumer healthcare, ophthalmic drugs, and artificial intelligence, providing various forms of support such as industry cooperation and investment to jointly promote the development of the industry.

“With the entry of industrial capital, the existing high-quality target assets in the ophthalmic device field will be completely divided within two to three years, and the industrial incubation will enter a new cycle."Senior investor Li Yang said, 'Some companies with good growth potential and outstanding products will benefit from the relatively abundant funds and well-established channels of publicly listed leading firms, allowing them to grow faster. They can also more easily endure the current capital winter, and in the future, become an important part of the leading company’s product chain through mergers and acquisitions.'"

However, Li Yang also suggested that the new forces in China's domestic ophthalmic device sector will inevitably go global in the future, and some companies will become giant enterprises on par with Zeiss. Therefore, for some innovative companies, they must not become complacent during their growth. While tightly seizing the new wave of industrial incubation, they should avoid becoming subordinate and instead have sufficient "ambition." They must always focus on high-end products and aim to be platform-based enterprises, carving out a differentiated path amid fierce industry competition.

Only in this way can China-produced ophthalmic devices have a more brilliant tomorrow.