Billion-Dollar G-CSF Market: Who Will Dominate—Qilu, CSPC, or Hengrui?

Qilu Pharmaceutical

Specialty Formulations and Active Pharmaceutical Ingredients (API) Developer

Note:This article does not constitute any investment opinions or suggestions; please refer to official/company announcements for accuracy.This article only introduces drugs related to medical health, not a recommendation of treatment options (if involved), and does not represent the platform's position.Any article reprinted needs to be authorized.

In the pharmaceutical industry, the colony-stimulating factor drug market has always been a highly focused area. Colony-stimulating factor drugs play a significant role in treating diseases such as neutropenia caused by radiotherapy and chemotherapy. With the growth of medical demand and the development of pharmaceutical technology, the scale of this market continues to expand, and the competitive landscape is becoming increasingly complex.

MaxEntropy Consulting's "Special Research Report on the Colony-Stimulating Factor Drug Market" comprehensively analyzes the classification and application field data of colony-stimulating factors, the competitive landscape, and market trends, providing critical references for enterprises to formulate strategic decisions and seize market opportunities. Next, based on selected content from the report, we will focus on conducting an in-depth analysis of the competitive landscape in the colony-stimulating factor drug market.

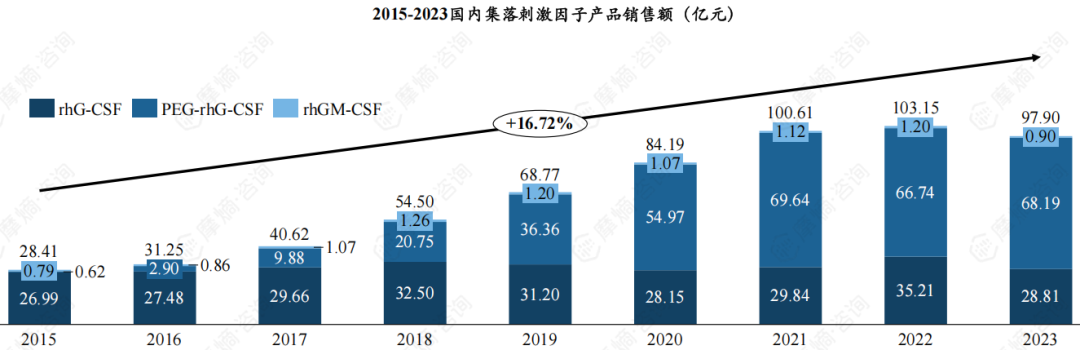

The main market for G-CFS isPEG-rhG-CSFAndrhG-CSFAccording to the database of Mose Pharmaceuticals, the overall market size grew from 2.841 billion yuan in 2015 to 9.790 billion yuan in 2023, with an annual compound growth rate of 16.72%, and the market size increased nearly 3.5 times. The colony-stimulating factor market reached its peak in 2022, with sales of 10.315 billion yuan, and slightly decreased in 2023.

PEG-rhG-CSFDue to its obvious advantages, the market has continued to expand. Sales increased from 0.62 billion yuan in 2015 to 68.19 billion yuan in 2023, and the market share grew from 2.18% to 69.65%, gradually becoming the mainstream in the market. Although the market share of rhG-CSF has been declining, its sales have remained stable at around 30 billion yuan.

rhG-CSFThe market is tending to saturate, as it has not been completely replaced due to its wide range of indications and price advantages.

rhG-CFSThe earliest was by the United StatesAmgenUnited JapanQiluCompany R&D, also known asFilgrastim, which was approved by the FDA for marketing in 1991, is used for neutropenia caused by radiotherapy and chemotherapy. In 1993, the first imported rhG-CSF product entered China, and then was copied and marketed by nearly 25 companies, leading to fierce competition.

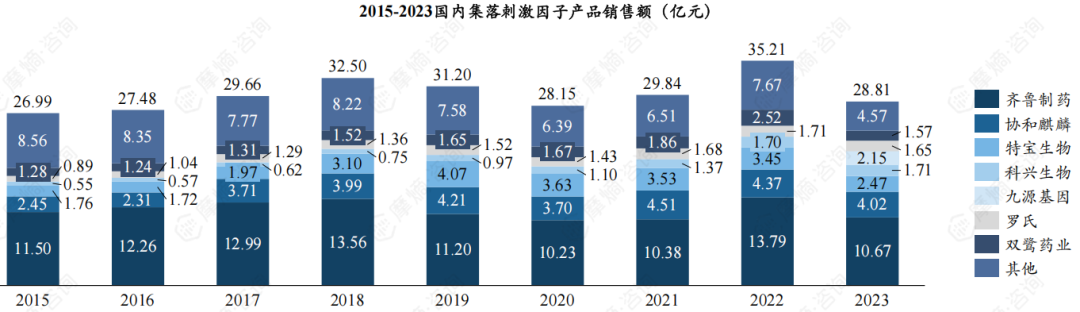

BecauserhG-CFSClinical indications are broader, and the price is lower, so rhG-CSF has not been completely replaced by PEG-rhG-CSF, maintaining a market sales volume of around 3 billion.Qilu PharmaceuticalQilu Pharmaceutical is the leading enterprise in the rhG-CSF market in China, occupying the largest market share with sales reaching 1.067 billion yuan in 2023, accounting for 37.02% of the market. It is followed by Kyowa Kirin, Amoytop Biotech, and Jiuyuan Gene, which occupy 13.95%, 8.59%, and 7.46% of the market respectively.

PEG-rhG-CSF solves the short half-life problem of rhG-CSF, with 7 products currently on the market.

In 2002,AmgenThe first long-acting white blood cell booster, pegfilgrastim, was obtained by linking the N-terminal amino acid of filgrastim with a single linear 20kD PEG, solving the problems of filgrastim's short half-life and the need for daily injections, making it more convenient to use while improving efficacy.

In 2011, the first PEG-rhG-CSF product in China,Shiyao Baik Pharmaceutical Co., Ltd.TheJinyouliApproved for marketing, filling the gap in such products in China. As of October 2024, seven PEG-rhG-CSF products have been approved for marketing in China, among which Jinyouli, Xinruibai, Shenlida, and Jiuli belong to the first generation of PEG-rhG-CSF.

Hengrui PharmaceuticalTheSulperfigrastim、Yifan BiologicsOfAibegstim α、Xiamen TebaoTheTobefigstimRespectively, the original research was restructured and upgraded, further expanding the market pattern of long-acting white-blood-cell-boosting injections.

The bonus of the first-generation PEG-rhG-CSF's inclusion in the medical insurance has been mostly realized.

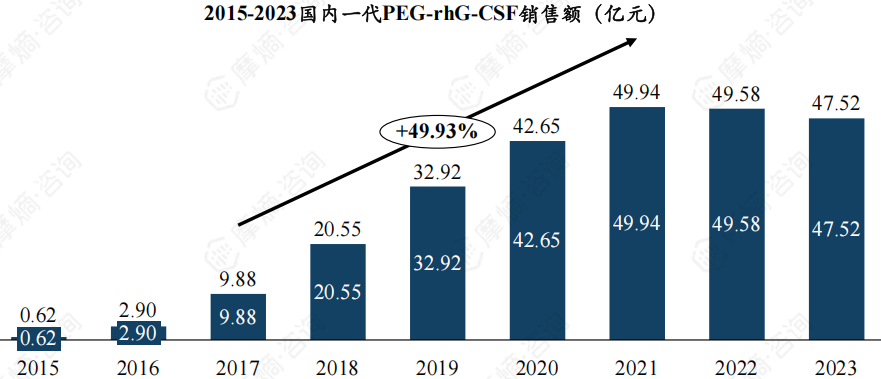

2011PEG-rhG-CSFAfter its market launch, due to the ongoing market education phase and the product not being included in the medical insurance, the high price led to a relatively small market scale. In 2017, PEG-rhG-CSF was included in the national medical insurance directory, leading to a rapid increase in product sales.

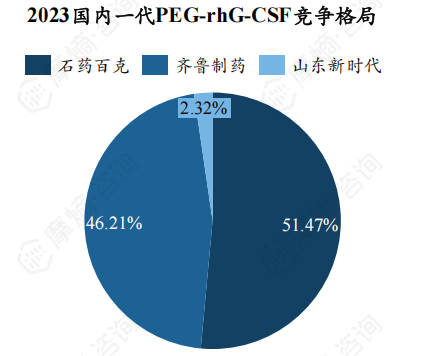

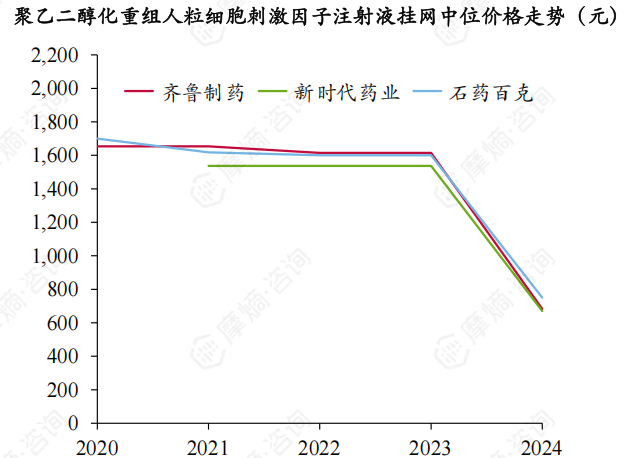

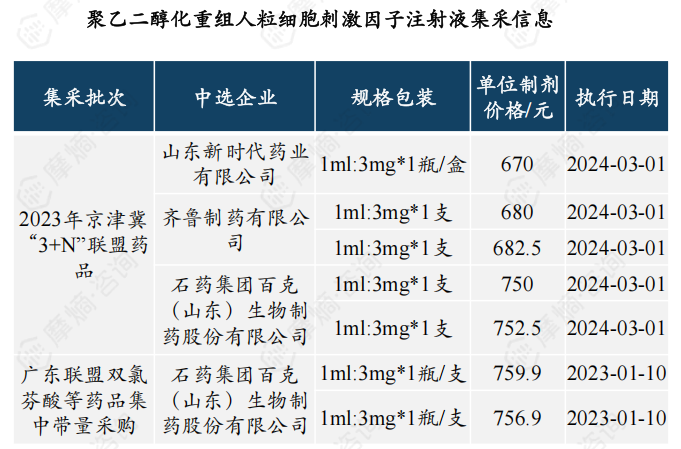

In 2021, the sales revenue of the first-generation PEG-rhG-CSF reached 4.994 billion yuan, with a compound annual growth rate of 49.93% from 2017 to 2021. After 2021, due to the release of the benefits from the expansion of medical insurance coverage, the market size slightly decreased.Shiyao Baik PharmaceuticalAndQilu PharmaceuticalThe product, due to its early market launch, has seen the two split the market evenly, occupying 51.47% and 46.21% respectively. AsShandong New Era and Shuanglu PharmaceuticalThe product launch will bring a certain impact on the current market landscape.

Market Analysis of Jinyouli in Hospitals at All Levels (Taking Harbin City as an Example)

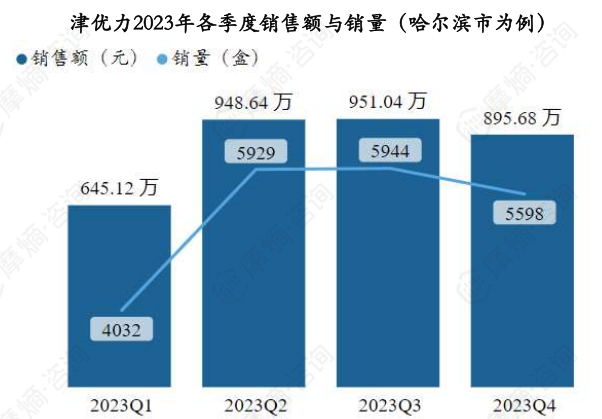

According to the drug distribution data from Mose Pharm, taking Harbin City as an example,JinyouliThe sales volume and sales revenue for each quarter of 2023 are shown in the figure below:

JinyouliTop 3 Hospitals in Sales Revenue for 2023(Taking Harbin as an example)The Third Affiliated Hospital of Harbin Medical University, The Sixth Affiliated Hospital of Harbin Medical University, and The First Hospital of Harbin City.

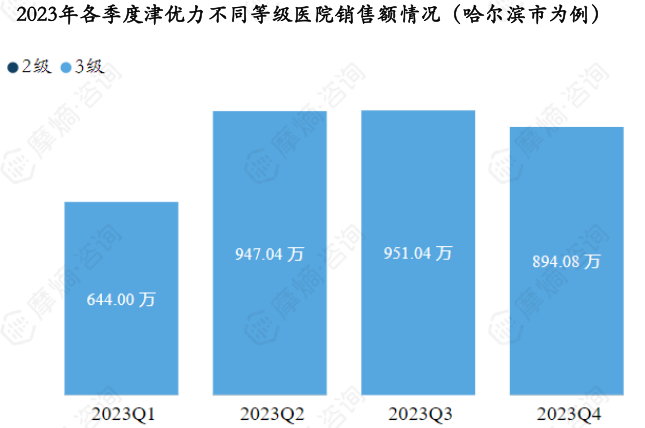

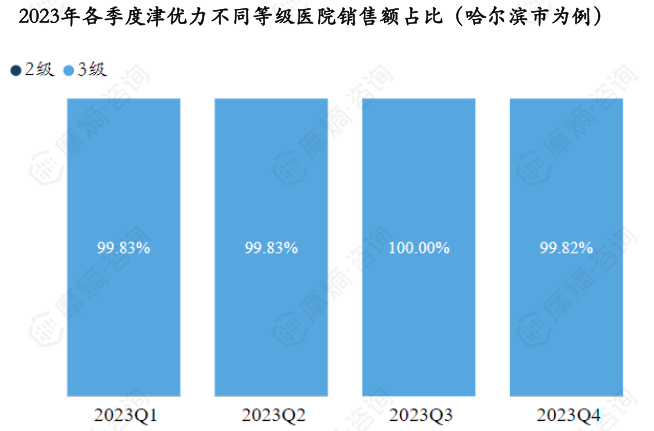

JinyouliIn 2023, the main sales market was distributed in tertiary hospitals, where all sales in the third quarter came from tertiary hospitals, and the sales proportion from secondary hospitals in other quarters was less than 1%.

First-generation PEG-rhG-CSF saw a certain degree of price reduction in 2023, with expectations for a second wave of increased sales.

Sulperfigrastim Addresses the Issue of Unstable Binding Between First-Generation PEG and G-CSF Receptor, with Sales Breaking Through 2 Billion Yuan in 2023

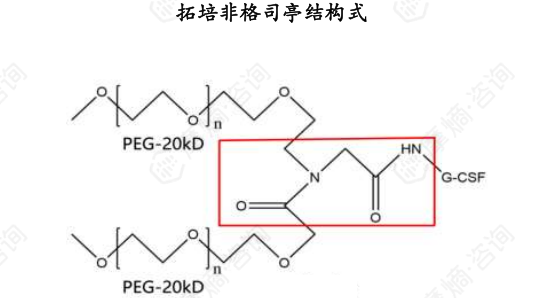

SulperfigoceptIt is the first domestically developed long-acting white blood cell booster in China, which was approved for marketing in 2018.SulperfigrastimThe overall structure is similar to the first-generation long-acting white blood cell booster, but the researchers introduced a thiol group at the N-terminus of G-CSF. Through a Michael addition reaction, a 19kDa linear PEG was attached to G-CSF. With this technical improvement, the modification efficiency of the product is higher, and the purity has also significantly increased, effectively addressing the issue of unstable binding between the first-generation PEG and the G-CSF receptor.

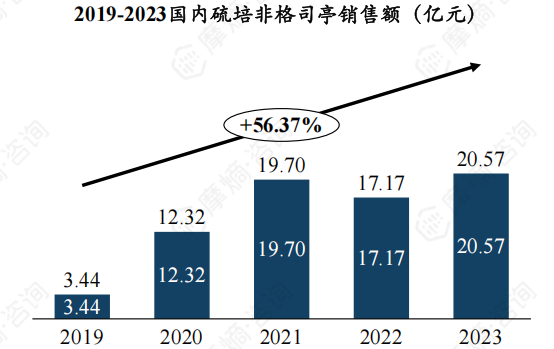

SulperfigoceptThe launch price was 6,800 yuan per vial. In 2019, to be included in the medical insurance, the price dropped to 3,680 yuan per vial. By 2024, the median online price further decreased to 2,547.78 yuan per vial, but it is still relatively higher compared to the price of first-generation PEG-rhG-CSF.Sulperfigo StimulantSince its launch, sales have continued to rise, with a compound annual growth rate of 56.37% from 2019 to 2023, reaching 2.057 billion yuan in sales in 2023.

Tebio and Fosun Pharma Join Hands to Boost the Sales of Torepefigstim

TopegfilgrastimProduced byTebio BiotechDeveloped and approved for marketing in 2023, and included in the medical insurance catalog in the same year.TopegifstimIt is a long-acting white blood cell boosting agent with a novel structure, composed of Y-shaped polyethylene glycol with a molecular weight of 40kD.(PEG)A new generation of PEG-rhG-CSF combined with rhG-CSF.

40kD PEG isTopegfilgrastimAs a hallmark feature of the new generation of long-acting G-CSF. Compared with 20kD PEG, the 40kD PEG structure contains more ethylene oxide units, has a larger volume, and exhibits greater mobility. Therefore, when the PEG molecule forms a protective structure around the drug, it can provide more comprehensive protection for rhG-CSF. Meanwhile,TobefigstimIt also has a unique branched chain structure, which further enhances the protection of PEG molecules on rhG-CSF, making the drug less susceptible to enzymatic degradation or clearance, with stronger stability and a milder white blood cell boosting effect.

TopefigrastimIn 2023, the sales revenue was 406,700 yuan,Tebio BiotechAlreadyTopegfilgrastimThe exclusive promotion and sales rights in mainland China are granted toFosun Pharma, receiving an upfront payment and milestone payments totaling 73 million yuan. Fosun's strong commercialization capabilities are beneficial.TopefigrastimThe rapid increase in volume.

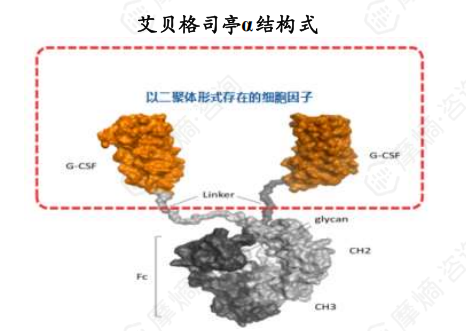

Aibegstimα is the first Fc-fused G-CSF, with excellent efficacy and high safety.

Aibegstim α(Ebilux)Produced byYifeng BioDeveloped and approved for marketing in 2023. Unlike other PEG-rhG-CSF, it contains G-CSF at the N-terminal and a human Fc fusion protein at the C-terminal, with each Fc fragment conjugating two G-CSF molecules, leading to stronger activation of downstream signaling pathways. In contrast, the PEG-G-CSF structure contains only one G-CSF molecule, which may also be shielded by PEG around its active functional clusters, reducing its leukocyte-boosting efficacy. In terms of production cost,AibegstimαFewer production steps, significantly lower than PEG-G-CSF.

Aibegstim αIt is the only long-acting G-CSF to date that has conducted head-to-head Phase III studies with both original short-acting and original long-acting formulations, achieving non-inferiority results in both, and has now been approved for marketing in the United States and Europe.

AibegstimαSuccessfully included in the medical insurance at the end of 2023, with a medical insurance price of 2388 yuan per vial, slightly lower thanHengrui MedicineSulperfigrastimIn 2023, the sales revenue was 9.4613 million yuan. As the first Fc fusion-type G-CFS, it has demonstrated good efficacy and excellent safety, with expectations for successful market expansion.

The market competition landscape for colony-stimulating factor drugs is complex and ever-changing.PEG-rhG-CSFAndrhG-CSFDifferent enterprises have their own advantages in the market and compete for market share through product innovation, market strategies, and other means. With continuous technological advancements and changes in the market environment, the competitive landscape of the colony-stimulating factor drug market will continue to evolve in the future. Enterprises need to constantly innovate and improve product quality and service levels to address market changes and challenges.

Copyright Statement: This article is reproduced fromAPI Intelligence Bureau,Media or individuals who do not wish to be reproduced can contact us, and we will delete it immediately.

Rooted in Shanghai and radiating globally, PharmaCircle, as a strategic platform for the biopharmaceutical industry, is on a mission to "enable the borderless flow of intelligence and connections." It has established an empowering system that covers the entire pharmaceutical industry chain, including R&D, production, distribution, and commercialization. Through four core engines—intelligent cloud services, precise resource linking, industrial think tanks, and ecosystem communities—it is building the infrastructure for the flow of pharmaceutical value in China.

Under the dual waves of globalization and digitalization, PharmaCircle is redefining the circulation paradigm of pharmaceutical resources — it is not only a hub for information and networking but also a catalyst for industrial transformation. With China as the origin, we are weaving a global network of pharmaceutical intelligence, making every precise connection a catalyst for enterprises' leapfrog growth.