Fertility-Related Companies Rush to IPO Amid Survival Crisis: 'List or Perish'

Jingze Bio

New Drug Developer

Recently, Saint Bella, known as the "Hermes" of confinement centers, officially went public on the Hong Kong Stock Exchange, with its stock price surging 33.74% on the first day of trading, and its market value skyrocketing to HK$5.366 billion at its peak.

However, in the eyes of industry insiders, this IPO seems more like a desperate gamble. According to the financial report, although Saint Bela's revenue has been continuously increasing in recent years,But the net profit continues to be negative, with the total loss now reaching 773 million yuan. Under the immense financial pressure, going public has become the only option for relief.. Coincidentally, the Hong Kong Stock Exchange launched the "Tech Enterprise Express" policy in May 2025, which gave Saint Bela an opportunity. The company then integrated its confinement center with medical care and technology as valuation support points, eventually leading to a successful listing.

Figure 1. Some fertility companies that are in the process of going public (Chart by VCBeat)

Figure 1. Some fertility companies that are in the process of going public (Chart by VCBeat)

In fact, it is not only Saint Bella that wants to seize the lifeline of going public. According to incomplete statistics from VCBeat,So far this year, 11 "fertility"-related companies have launched IPO attempts., including infant monitor R&D providerPolyIntel Technology, China's largest special medical food group for infantsSaintonge Special Medicaland assisted reproductive drug research and development enterprisesJingze Bioetc. If we add the ones submitted earlier that are still pending listing,VitaTech Biologics, Dongyun Healthcare, Aivia Medical, Newman's Health, etc. Currently, there are over 30 "fertility" companies in the queue for going public.

This is absolutely a rare scene to behold, but behind the bustling facade lies, more often than not, a sense of helplessness:For the vast majority of "fertility" enterprises, the next two years will be their last chance to stay afloat. If they miss it, the only fate awaiting them will be elimination by the market or a complete transformation.. This is absolutely not an exaggeration.

Not going public, out of the game?

Just the day after Shengbela's IPO, Jingze Bio officially submitted its prospectus to the Hong Kong Stock Exchange. This biopharmaceutical company, which focuses on two major fields—assisted reproduction and ophthalmic drugs—currently has eight drug candidates in its pipeline. Among them, the recombinant human follicle-stimulating hormone lyophilized powder injection JZB30 has been approved and is about to move into commercialization. Additionally, JZB33 (recombinant human follicle-stimulating hormone water injection) and JZB05 (anti-VEGF intravitreal injection) are currently in the NDA and Phase III clinical stages, respectively, with market launches imminent.

But behind the glossy pipelines, Jingze Bio still cannot hide the embarrassing reality of continuous losses and having no commercial revenue at all. According to the prospectus,Net Loss Exceeds 500 Million Yuan in the Past Two Years, which is mainly due to expenditures such as R&D costs and administrative expenses.Due to the lack of commercialized products, Jingze Bio's cash flow mainly relies on financing. However, by the end of 2024, the company's cash equivalents were only 68.586 million yuan.。

To make matters worse, Jingze Bio's redeemable liabilities have now reached 1.33 billion yuan, with a staggering debt-to-asset ratio of 486%.If the conditions such as going public or completing a full qualification sale are not met by December 31, 2025, it will trigger the investor's redemption right.。Therefore, for Jingze Bio, this attempt to go public on the Hong Kong stock market is a desperate leap in dire straits.

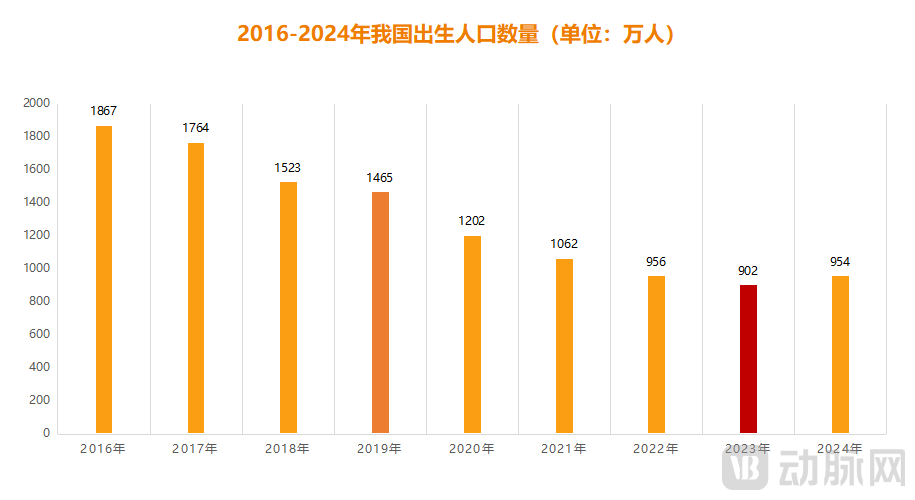

Figure 2. The number of births in China from 2016 to 2024 (Data source: National Bureau of Statistics)

Figure 2. The number of births in China from 2016 to 2024 (Data source: National Bureau of Statistics)

In addition to the pressure at the repurchase level,The Gradually Shrinking Market Makes the Path to IPO More Urgent for More Fertility EnterprisesAccording to data released by the National Bureau of Statistics, the number of newborns in China in 2024 was 9.54 million. Although this halted an eight-year decline, it still represents a decrease of nearly 5 million compared to 14.65 million in 2019. The direct impact of this is a further downturn in the market, and accordingly, a significant reduction in companies' revenue and profits.

Taking Newman Health as an example, this enterprise specializing in maternal and infant nutrition products has seen its net profit drop significantly from 338 million yuan in 2021 to 45 million yuan in the first half of 2024, nearing a shift from profit to loss. In order to curb losses as soon as possible, Newman has been striving for an IPO since 2019.It has already submitted its listing application to the Hong Kong Stock Exchange for the sixth time in a row, and its urgent desire for an IPO is evident.。

HaiPaKe is no exception. As the largest vertical e-commerce platform for maternal and infant products in China, its total annual transaction volume exceeds 11 billion yuan. However, even so, its financial report data remains alarming:Over the past two years, HaiPaKe's net profit has continued to decline. The company now has accumulated losses of 1.854 billion yuan and carries a net debt of up to 2 billion yuan, indicating significant financial pressure.Therefore, Haipaike, which has only the IPO path left, has no choice but to go public as soon as possible before the situation worsens.

In this regard, a senior investor commented, "In recent years, in order to control some 'problematic' listed companies, major exchanges have regarded 'sustained profitability' as the key criterion for subsequent listing eligibility.Therefore, for the vast majority of fertility companies, they all want to seize the last wave of demographic dividend and go public as soon as possible when they can deliver a good 'report card', otherwise it will only become increasingly difficult later on.。”

After listing, it still needs to "overcome challenges"

In recent years, under the market dividend of the "three-child policy," the fertility sector has also given rise to a number of listed companies, such as the "first in vitro fertilization stock."Jinxin Fertility"The First Postpartum Care Center Stock"Aidigongand "the first stock in auxiliary reproductive genetic testing"Beikang Medicaletc.

Figure 3. Performance of Some Listed Fertility Companies (Chart by VCBeat)

Figure 3. Performance of Some Listed Fertility Companies (Chart by VCBeat)

But from the current performance, its days after the listing have not been easy. Take Jinxin Reproductive as an example. According to the annual report, its revenue in 2024 was 2.812 billion yuan, a mere 0.8% year-on-year increase.This is the first time its revenue growth has slowed to single digits since 2021.Not only that, but Jinxin Fertility's net profit has also turned into negative growth. In 2024, the company achieved a net profit of 274 million yuan, a year-on-year decrease of 21.2%.

Beikang Medical is also deeply mired in performance woes. Although its revenue grew against the trend by 43.8% in 2024, losses continue to widen, with the total deficit exceeding 700 million yuan over the four years since its listing. As a result, Beikang Medical's market value has now fallen to less than 900 million Hong Kong dollars, a sharp decline of nearly 90% compared to the closing market value of 7.4 billion Hong Kong dollars on its first day of listing.

However, this is not the worst; the worst is Aidi Palace. On February 21, 2025,Aidigong Officially Announces Trading Halt; the Reason is that Aidigong's Financial Officer, Mr. Zhu, Refused to Cooperate with the Auditor, Resulting in the Inability to Disclose the 2024 Annual Results on TimeAccording to the latest public financial report of Aidi Palace, in the first half of 2024, Aidi Palace achieved a revenue of 275 million Hong Kong dollars, a year-on-year decrease of 10.58%, and a net profit loss of 39 million Hong Kong dollars, a year-on-year decrease of 65.68%. As of now, Aidi Palace has not yet resumed trading, but under long-term losses, its path to resuming trading is obviously bleak.

It is not difficult to see that even if they are successfully listed, fertility enterprises currently have their own difficulties. So, what are the reasons? Apart from the previously mentioned market contraction, what other key factors have caused this group of companies to fall into a growth bottleneck, or even face survival difficulties?

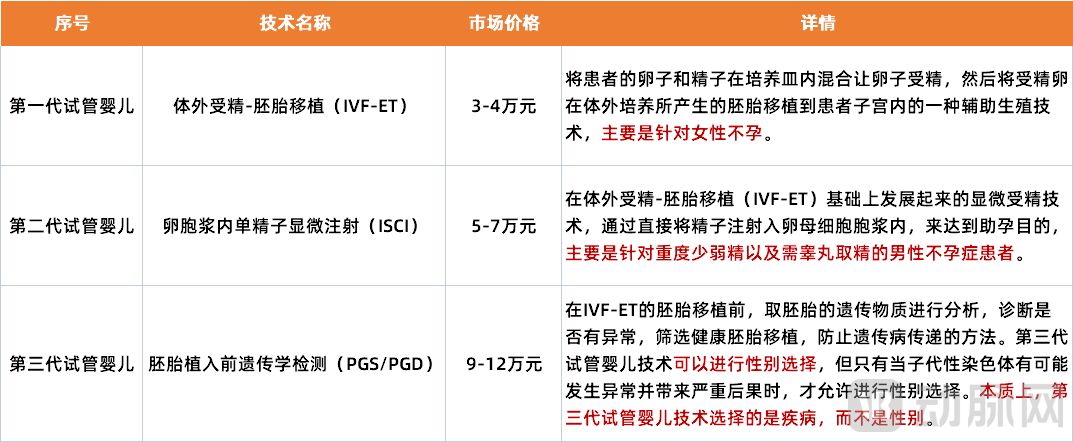

Through expert interviews and case analysis, VCBeat believes that there are mainly three points:The first point is the low market penetration rate.According to data from Frost & Sullivan,In 2023, the penetration rate of China's assisted reproductive market was 9.2%., although it increases slightly every year, the gap is still large compared with the market penetration rate of about 30% in developed countries in Europe and America.

Figure 4. Details and Market Pricing of the Third-Generation IVF Technology (Data Source: Frost & Sullivan, Chart by VCBeat)

Figure 4. Details and Market Pricing of the Third-Generation IVF Technology (Data Source: Frost & Sullivan, Chart by VCBeat)

The reasons for this are complex, but the key factor lies in technology. Currently, global assisted reproductive technology has evolved to the third generation, which focuses on Preimplantation Genetic Testing (PGT). The success rate of this technology in China is generally around 50% to 70%, while in countries like the United States and Thailand, it reaches as high as 60% to 80%. This inevitably drives some Chinese patients to seek medical treatment abroad. Indeed, it is reported that Thailand performs over 30,000 IVF cycles annually, with Chinese clients accounting for 80%.

In addition to technical differences, price is also an important reason for the low penetration rate, as the "astronomical" cost of services keeps many people out.Taking postpartum care centers as an example, most of them are associated with high prices. For instance, the starting price for a 28-day package at Saint Bella is 138,000 yuan, while the highest-end "Queen Package" can exceed 500,000 yuan. This determines that their services are mainly targeted at high-income groups, with extremely limited coverage.

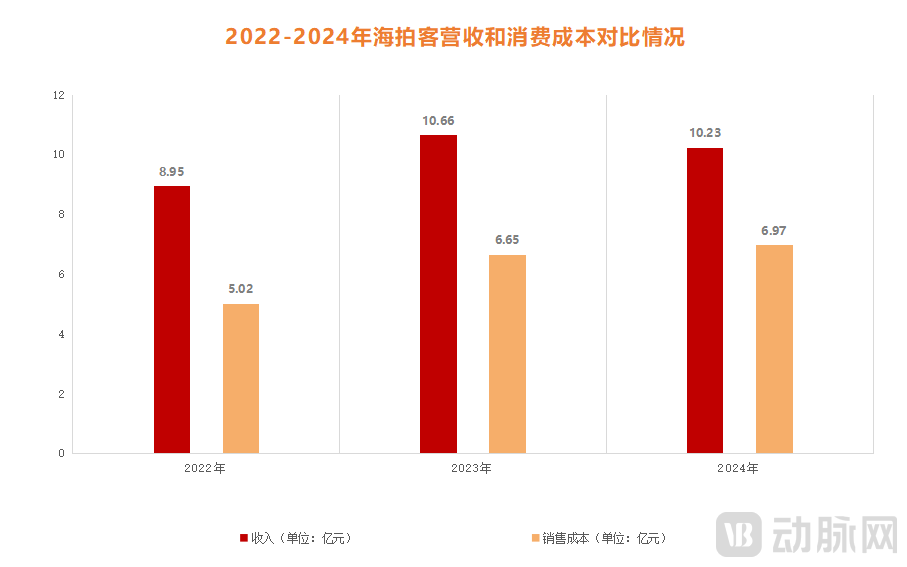

Figure 5. Comparison of HaiPaKe's Revenue and Cost of Sales (Data Source: Company Prospectus)

Figure 5. Comparison of HaiPaKe's Revenue and Cost of Sales (Data Source: Company Prospectus)

The second key reason is the persistently high sales costs, which have significantly eroded corporate profit margins.Take Hippo Baby as an example. As the largest maternal and infant B2B platform in China, its revenue reached 1.032 billion yuan in 2024. However, despite this, it still cannot escape the embarrassing situation of "selling more but losing more." The main reason lies in the extremely high cost spent on marketing. According to the prospectus, Hippo Baby's sales expenses in 2024 were close to 700 million yuan, accounting for over 60% of its total revenue. Adding other fixed costs, the profit margin left for the company is minimal.

The last point is the break of the capital chain caused by blind expansion, leading to a sharp increase in market risks.In fact, the technical barriers of fertility-related enterprises are generally not high, so homogenization is relatively serious. In order to quickly capture market share, companies have no choice but to choose aggressive expansion in the early stage. However, the negative impact brought by this is that it will not only generate a large amount of costs, but also once the market performance is not ideal and does not reach a certain realization rate, it is very easy to cause a profit gap for the enterprise, or even a break in the capital chain.

In this regard, a senior figure who has long been concerned about the fertility field mentioned, "Fertility enterprises are actually easy to fall into the vicious circle of increasing revenue but not increasing profit."On the one hand, this is because most of them are directly consumer-facing, so their service models are generally more resource-intensive, with relatively high costs; on the other hand, it’s because they are mostly in the early stages of development, thus requiring significant market investment. In this process, if the balance between cost and profit is not well-maintained, it can easily lead to losses, which may in turn affect the normal development of the enterprise."

Where is the future path? Entering the下沉市场or going overseas

Although the number of newborns in China is decreasing year by year, the large population base and low penetration rate still determine that this is a huge market. Taking the assisted reproduction field as an example, according to Frost & Sullivan data,The scale of China's assisted reproductive market is expected to reach 108.9 billion yuan by 2029, with a compound annual growth rate of 12.9% from 2024 to 2029.. This shows that its market potential is still relatively large.

So, how to cash in on the future? This needs to be viewed from multiple dimensions.

The first step is to focus heavily on the下沉market and rapidly increase penetration. According to reports,In 2024, 9.54 million newborns, 85% were contributed by the county market., and the spending power of this group is relatively limited, so there needs to be significant focus on pricing. Take Jinxin Fertility as an example. In recent years, it has specifically targeted low-income groups and even launched the "Jinbao Plan 2.0" with "0 yuan IVF, full refund if unsuccessful." The aim is to attract more users and accelerate coverage in lower-tier markets.

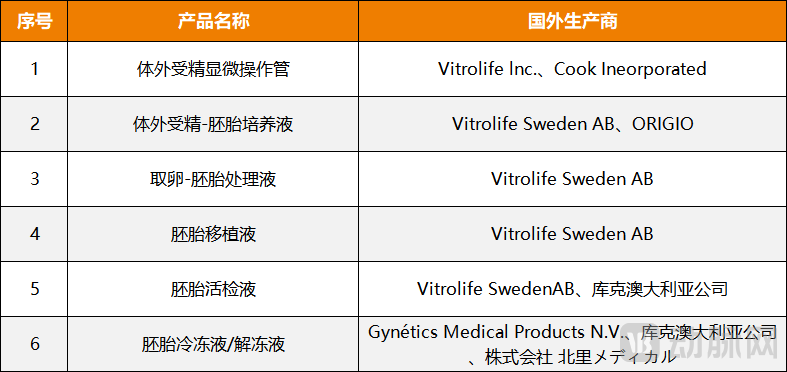

Figure 6. Major instruments for assisted reproduction are monopolized by foreign-funded products (Source: Huachuang Securities)

Figure 6. Major instruments for assisted reproduction are monopolized by foreign-funded products (Source: Huachuang Securities)

Secondly, it is necessary to accelerate the substitution of domestically produced products to gain more control over pricing.According to a report released by Frost & Sullivan in 2022, the import monopoly of equipment and consumables in China's assisted reproductive industry is relatively high.The import ratio is as high as 95%., involving approximately 40 to 60 categories, most of which are high-value consumables. This means that the profit margins of domestic companies will be further compressed, and to reverse this situation, technological innovation must be continuously pursued to achieve the replacement with Chinese-produced alternatives.

Then, at the promotion level, we should target our efforts and try to "achieve big results with small investments."Specifically, on the one hand, the focus is to create a group of star doctors or star teams, utilizing their market influence for brand promotion and quickly attracting a group of precise users. On the other hand, diversified services are used to drive traffic. Taking Jin Xin Reproductive as an example, it has opened reproductive restoration and anti-aging clinics targeting women's needs, and also covers areas such as insomnia and psychology. This type of consumer service can enhance customer stickiness.

The final goal is to open up broader markets, actively go global and expand overseas.In recent years, riding the wave of overseas expansion, a group of fertility enterprises have also reaped considerable returns in foreign markets. For instance, Jinxin Fertility reported overseas business revenue of 604 million yuan in 2024, marking a 6% year-on-year increase, with growth significantly outpacing that of the domestic market. Similarly, Zhuhai Beikang Zeen Health Management Co., Ltd. generated sales revenues of 58.431 million yuan, 21.328 million yuan, and 17.453 million yuan in Europe, North America, and the Asia-Pacific regions, respectively, in 2024. The total income from these regions accounted for over 30% of its total revenue, reflecting the remarkable success of its global strategy. From a long-term perspective, overseas markets are undoubtedly a blue ocean, offering vast development space and opportunities for Chinese enterprises.

Objectively speaking,The decline in fertility rates is an established fact, but this is not something that companies can control. What they can truly influence is how to reduce costs and increase efficiency, and improve market penetration through services with a higher cost-performance ratio, thereby increasing revenue and profits. This is the key to their successful listing.。

1. "The Boss of the Postpartum Center Flees, Has the Sky Fallen for the Wealthy Housewives?" — Chinese Research Lab;

2. "Jinxin Fertility Faces Short-term Funding Gap of 700 Million! 'First IVF Stock' Loses Luster" — VCBeat;

3. "Backed by Hengrui, Jingze Bio Enters Hong Kong Stocks with 486% Debt Ratio: How to Navigate the Red Ocean of Biosimilars?" — VCBeat.