2026 Weight-Loss Drug Market Set for Major Shake-Up: Lilly’s Tirzepatide Slashes Price by Over 80% Post-NHIR Reimbursement, Domestic Substitutes Accelerate

Qilu Pharmaceutical

Specialty Formulations and Active Pharmaceutical Ingredients (API) Developer

CSPC

Innovative Drug Research and Development, Manufacturer

Innovent

High-end Biologics Developer

China's GLP-1 Drug Market in 2026 is Undergoing an Unprecedented Transformation: Early in the YearQilu Pharmaceutical、CSPCAs domestically produced biosimilars get approved in密集 waves, the era of original drugs' "monopoly" comes to an end;LillyTheTirzepatideIncluded in medical insurance with a reduction of over 80%; price wars sweep through hospitals and beyond;Innovent BioTheMashiduo PeptideThe accelerated entry of differentiated products has intensified the competition in the development of dual- and triple-target drugs, speeding up the restructuring of the market landscape.

However, the current changing situation can be traced, and its root cause can be traced back to the core changes in Q1 of 2025: that quarterTirzepatideFirst Landing in China BreaksSemaglutideExclusive Status, "Blinding Controversy" Shakes Public Trust for the First Time, Deep Market Differentiation in Regional Markets Manifests with Clear Data for the First Time. Three Major Variables Continue to Ferment, Shaping the Market for 2026 and Beyond. Looking Back at Q1 2025, Aimed at Decoding the Logic of the Current Landscape Formation and Predicting Future Evolution, These Variables...(Competitive Impact, Public Sentiment Chain, Regional Differentiation, Pipeline Layout)The sustained impact is precisely the key切入点 for understanding the current competition.

This article is excerpted from the Head Leopard Research Institute's "2026 China Biopharmaceutical Innovation Market Tracking Report:SemaglutideMarket Review of Q1 2025. Anchored in Q1 2025, the report provides a comprehensive market overview with both historical depth and forward-looking perspectives for industry practitioners, investment institutions, and policy researchers through an in-depth analysis of hospital sales data and a full-spectrum scan of R&D pipelines. The report data is sourced from the Mosun Pharma Database - Hospital Sales Intelligence.(The first fine-grained hospital drug sales analysis system developed by MesoEntropy, detailing down to the provincial, city, district and county levels across China as well as hospital grade dimensions), ensuring the reliability and authority of the analysis conclusions, assisting enterprises in optimizing resource allocation, improving operational efficiency, and reducing market risks.

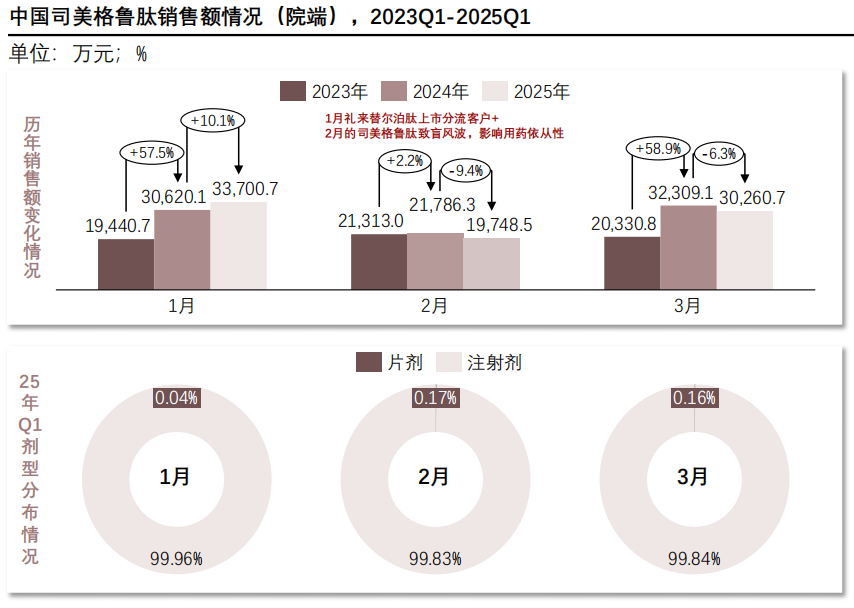

(1) Sales: High start, low dip, then stabilization; initial signs of competitive pressure

The First Quarter of 2025,SemaglutideHospital sales initially surged and then stabilized, influenced by factors such as the product's reputation, tablet pre-marketing, and the launch of competing products. The main dosage form remains injectables, and stronger promotional efforts will be needed in the future to address intense competition.

The First Quarter of 2025,SemaglutideIn China, the only approved products are Novo Nordisk's injectables and tablets. In January, sales reached 337,007,000 yuan, a high level, driven by both the sustained demand from its excellent reputation in blood sugar reduction and weight loss, as well as the market preheating for the full launch of the tablets in January. However, sales plummeted in February, mainly due to two factors: first,LillyTheTirzepatideLaunched officially in China in January, bringing new competitive pressure and diverting some potential customers; secondly, in February...SemaglutideThe blindness controversy has affected patients' medication adherence. Additionally, the market's wait-and-see attitude during the initial launch of the new drug also had a certain impact on sales.

Data Source: Mesentech Pharma Database - Hospital Sales Intelligence

Sales rebounded in March. The impact of Federal Pharmaceutical's liraglutide injection approval in March has yet to fully materialize, while the market gradually stabilized after experiencing fluctuations. Compared with the same period in 2023 and 2024, sales in January 2025 showed significant growth, reflecting the continued expansion of overall market demand. The steady growth during the same period in 2023-2024 also indicates...SemaglutideThe market foundation is continuously being consolidated.

In terms of dosage form structure, injectables still accounted for over 99% in January-March 2025, with tablets holding a very small share. Tablets were fully launched in January, but their market share has not effectively increased. In the future, as market awareness of tablets improves, their convenience advantage will gradually become apparent, potentially attracting some patients who have concerns about injectables. However,SemaglutideIt also faces challenges from competitors like tirzepatide and liraglutide. Companies need to strengthen market promotion and enhance product competitiveness to maintain an edge in the fierce competition.

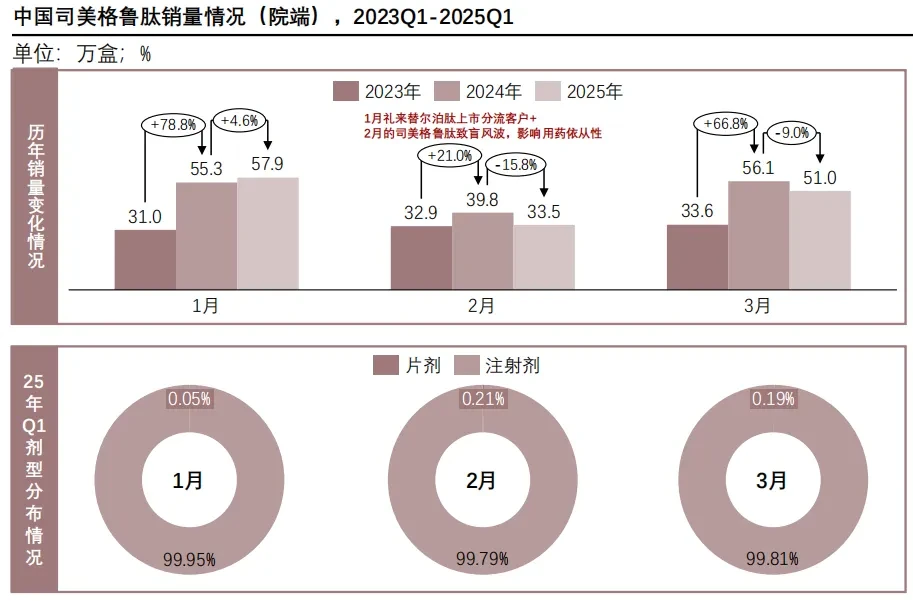

(II) Sales Situation: Market Resilience in Fluctuating Recovery

The First Quarter of 2025, ChinaSemaglutideAfter experiencing fluctuations, hospital sales have rebounded, showing an overall growth trend. Tablets dominate the market, but acceptance of injectables is increasing. Meanwhile, they face intense market competition and require enhanced promotion to improve competitiveness.

In terms of sales performance, January reached a high of 579,000 boxes, a result that was due toSemaglutideThe brand accumulation in the field of blood sugar reduction and weight loss continues to attract consumers to choose; it also benefits from the market preheating before the full launch of the tablets, prompting some consumers to pay attention and purchase in advance, injecting momentum into sales growth. In February, sales plummeted to 335,000 boxes, with the core cause consistent with the decline in sales: the launch of Eli Lilly's Tirzepatide diverted customers.SemaglutideThe blindness controversy affected medication adherence, and combined with market观望情绪, led to a significant sales decline.

Data Source: MaxEntropy Pharma Database - Hospital Sales Intelligence

Sales volume rebounded to 510,000 boxes in March, echoing the upward trend in sales revenue. Comparing the same periods, the January 2025 sales volume showed significant growth compared to the same period in 2023 and 2024, aligning with the year-on-year increase in sales revenue, fully demonstrating that ChinaSemaglutideThe overall market size is continuously expanding, which is consistent with the increase in sales reflecting the growing market demand.

In terms of dosage forms, injectables accounted for over 99% from January to March, while tablets had a smaller share. Tablets were launched in January, but market acceptance still needs improvement. In the future, the convenience advantage of tablets may attract specific patients, butSemaglutideFacing fierce competition, enterprises need to strengthen promotion and enhance competitiveness.

(III) Key Area Comparison: Resource Aggregation and Economic Development Determine Market Structure

2025Q1SemaglutideMarket regional differences are significant, with Beijing leading at 5.9 yuan per capita in sales, while Chongqing's per capita sales are only 0.6 yuan due to economic factors. Regional development is uneven, and unleashing potential requires coordinated multi-measures.

Data Source: Mosentropy Medicine Database - Hospital Sales Intelligence

Among the municipalities directly under the central government, Beijing stands out with a population of 21.832 million contributing sales of 127.874 million yuan, ranking first in per capita sales at 5.9 yuan per person and per capita volume at 95.9 boxes per 10,000 people in representative regions. This advantage is attributed not only to Beijing's resource concentration effect as the medical center of China – with a high density of top-tier hospitals and leading diagnosis and treatment levels for obesity-related diabetes – but also to the in-depth academic promotion of GLP-1 drugs in first-tier cities, as well as the concentration of cross-regional patient medical needs by early 2025.SemaglutideThe approval of obesity indications in China has further amplified the demand potential in the Beijing market.

Shanghai's population of 24.803 million is slightly higher than Beijing's, but its sales of 65.443 million yuan account for only 51.3% of Beijing’s, with per capita sales of 2.6 yuan/person significantly lagging behind. The core reason lies in the more intense competition in the local GLP-1 class drug market.TirzepatideThe dense layout of similar products, coupled with a dispersed population distribution, has led to the market demand not being highly concentrated in core medical resources, resulting in...SemaglutideThe market share is being squeezed.

Chongqing's population is 31.905 million, the largest among the four direct-administered municipalities, but its per capita GDP is only 24,000 yuan.(Only 42.1% of Beijing), corresponding to sales of 19.731 million yuan and per capita sales of 0.6 yuan per person at the lowest level. This is due not only to economic constraints, such as the non-inclusion of obesity indications in medical insurance, resulting in a heavy financial burden on patients paying out-of-pocket, but also to the concentration of medical resources in urban centers, with insufficient accessibility to diagnosis and treatment in regional areas, further limiting the market size.

In provincial regions, Shandong Province, with a population base of 100.802 million people and a GDP total of 2,346.6 billion yuan, achieved sales revenue of 39.805 million yuan. However, the per capita sales revenue was only 0.4 yuan/person, and the per capita sales volume was 7.1 boxes per 10,000 people, which were relatively low. The core reason lies in the dispersed distribution of medical resources within the region. The promotion of GLP-1 class drug prescriptions at the grassroots level is still in its early stages, and the coverage of medical insurance for new hypoglycemic and weight-loss drugs is weaker than in first-tier cities, resulting in market volume being supported but insufficient per capita penetration.

Jilin Province has the lowest per capita GDP of 14,000 yuan among all regions, but its sales revenue of 12.655 million yuan and per capita sales volume of 9.7 boxes per 10,000 people are slightly higher than those of Fujian Province, which has a per capita GDP of 32,000 yuan.(Sales 12.449 million yuan, per capita sales volume 5.4 boxes/10,000 people)The core difference lies in the fact that medical resources in Jilin are concentrated in core cities like Changchun, where market demand is relatively aggregated, whereas in Fujian, medical resources are dispersed across multiple cities, and patients' awareness and acceptance of novel weight-loss drugs is progressing more slowly.

Overall, 2025Q1SemaglutideRegional market differences are a comprehensive reflection of factors such as the concentration of medical resources, economic levels, medical insurance policies, and competitive landscapes. First-tier cities have significant resource and demand advantages, while the potential release in lower-tier regions and provincial markets still relies on the decentralization of medical education, support from the payment side, and optimization of the competitive landscape.

Note: Except for the population data which is at the end of 2024, all other data are calculated based on the first quarter of 2025.

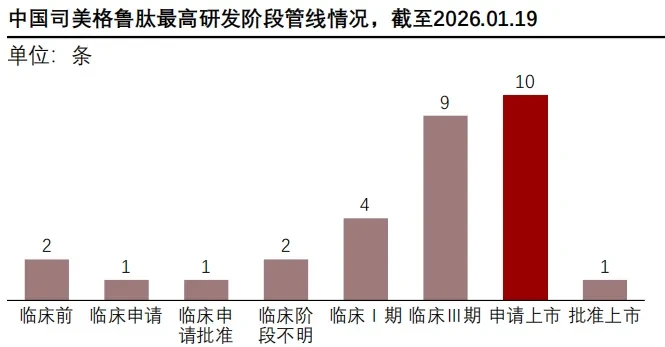

If sales data reveals the "current state" of the market, then the R&D pipeline points to the "future direction" of the market. As of early 2026, ChinaSemaglutideThe R&D pipeline has shown a gushing trend, indicating that the market pattern is about to undergo a dramatic change.

(1) R&D Pipeline: More Than Ten Companies "Waiting in the Wings," 2026 to See Peak of Approvals

ChinaSemaglutideAs the R&D process accelerates and numerous companies' products are nearing market entry, generic drugs will enter the market after the expiration of original drug patents. This will lead to intensified competition in the short term and market differentiation in the medium to long term. The policy environment will also play a crucial role in shaping the future development of the industry.

According to the MaxEntropy pharmaceutical database, as of January 19, 2026, in ChinaSemaglutideThe layout of related R&D pipelines is becoming increasingly complete, with multiple corporate products nearing market launch. In terms of the distribution of R&D pipeline stages, there are 2 pipelines in the preclinical stage, 1 in the clinical application stage, 1 in the clinical application approval stage, 4 in Phase I clinical trials, 9 in Phase III clinical trials, 10 in the application for marketing stage, and only 1 has been approved for marketing.(Novo Nordisk products)Among them, the manufacturers applying for listing include well-known domestic pharmaceutical companies such as Qilu Pharmaceutical and CSPC. Their initial application times are concentrated between September 2024 and September 2025, indicating that a large number of domestically produced products will be available in China within the next 1-2 years.SemaglutideProducts Gradually Enter the Market.

Data Source: Mesentech - Global Drug R&D Database

SemaglutideBranded drugs currently dominate the market, but the approaching patent expiration is driving changes in the landscape. After the patents expire, generic drugs will enter the market in an orderly manner, and based on the R&D progress, the number of products expected to launch in the next two to three years may significantly increase. Branded drug companies might consolidate their positions by improving dosage forms or expanding indications before the patents expire, while generic drug companies need to accelerate R&D and approval processes to capture market share. Currently, multiple companies are in Phase III clinical trials or applying for market entry, and subsequent competition will focus on production cost control and marketing effectiveness.

From the market trend, the listing of generic drugs in the short term will intensify competition and driveSemaglutidePrices are falling, and market penetration is increasing. In the medium to long term, the market will become more differentiated, with companies that have scale and brand advantages capturing the majority of the market share. R&D innovation remains a key variable; if companies achieve breakthroughs in developing new formulations or new indications for semaglutide, they will seize new development opportunities. Additionally, changes in the external environment, such as medical insurance policies and drug approval regulations, will also have an impact.SemaglutideWill have a significant impact on the future direction of the market.

(II) Competition from Substitutes: From "Two-Power Rivalry" to "Multi-Player Race"

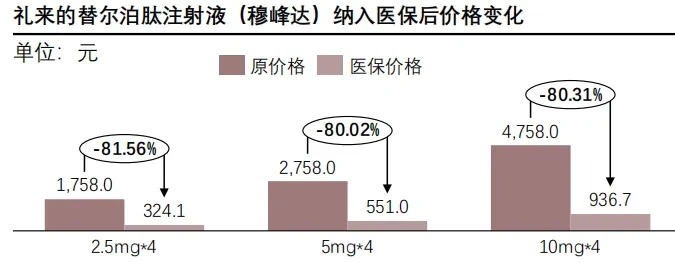

By early 2026, Eli Lilly and Novo Nordisk will engage in fierce price competition in China's weight-loss drug market. Factors such as patents and the entry of new players have led both companies to cut prices. Meanwhile, Chinese pharmaceutical companies are also highly competitive, and future market competition is expected to intensify further.

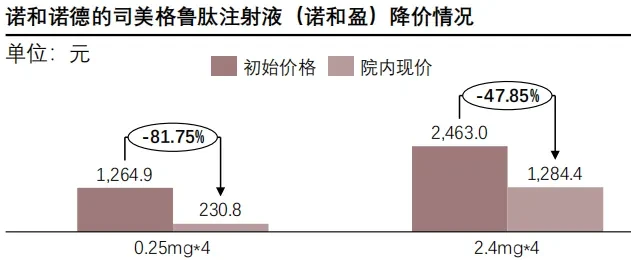

Early 2026,LillyAndNovo NordiskTwo Major Pharmaceutical Giants Launch Intense Price Competition in China's Weight-Loss Drug Market.LillyTheTirzepatide InjectionAfter being included in the medical insurance, the price reduction for all specifications exceeds 80%;Novo NordiskOfSemaglutide InjectionPrices within hospitals have also significantly dropped, with retail outlets and e-commerce platforms simultaneously following suit with price reductions.

Data Source: Mosentropy Medical Database - Hospital Sales Intelligence

The intensification of external competition stems from the叠加 of multiple factors: First,SemaglutideAs the expiration of core patents approaches, China-produced biosimilars are poised to enter the market; secondly, new players such as Innovent Bio are entering the field with novel dual-target drugs, diversifying the main competitors in the market; thirdly, latecomers such as...Tirzepatide, it is necessary to adopt a more competitive pricing strategy in the alreadySemaglutideRapidly capture market share in mature markets.

In terms of market development trends, the weight-loss drug market has enormous potential but is far from saturated. Companies are seeking differentiated advantages through innovation, such as developing dual-target drugs and creating oral formulations. Chinese pharmaceutical companies possess certain competitive strengths, including cost advantages, familiarity with the domestic medical environment and patient needs, flexible strategies in market penetration, and a gradually narrowing gap in cutting-edge research compared to international giants. In the future, competition in China’s weight-loss drug market will become even more intense. Companies will need to adopt comprehensive strategies in pricing, R&D innovation, and marketing to address the fierce competition.

The first quarter of 2025 is in ChinaSemaglutideA Key Turning Point in the Market. It signifies the market's transition from a period of rapid growth dominated by original research to a new phase characterized by multi-product competition, increasing price pressures, uneven regional development, and innovation-driven R&D. To succeed in the intensely competitive landscape of the future, companies must rely on powerful intelligence tools like the Mosentropy pharmaceutical database to敏锐 capture market dynamics, anticipate R&D trends in advance, and strategically focus their efforts while tactically achieving precise impact.

END

This article is original. Please leave a message to obtain authorization for reprint.

More RecentlyMoxie ConsultingPopular Reports

Scan the QR code below to claim