FOMO 2026: Global Pharma Innovation Realignment – Few Truly Understand the Shift

Perfuse Therapeutics

Biopharmaceutical Manufacturer

UCB

Biopharmaceutical and Specialty Chemicals Developer

Candid Therapeutics

Developer of Immune Disease Treatment Methods

Biogen

Neuroscience Drug Developer

EyeBio

Ophthalmic Disease Therapeutics Developer

Spark

Medical Insurance Agent

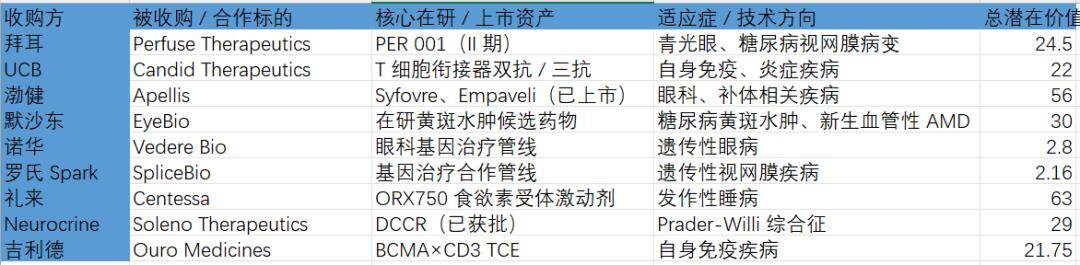

On May 6, 2026, Bayer announced the acquisition of Perfuse Therapeutics for a total potential value of up to $2.45 billion, including an upfront payment of $300 million, with the remaining amount to be paid in installments tied to development, regulatory, and commercialization milestones. Perfuse's lead asset, PER 001, is still in Phase II clinical trials for glaucoma and diabetic retinopathy. This marks Bayer's largest deal since its $63 billion acquisition of Monsanto in 2018.

Five days ago, UCB announced a $2 billion upfront payment and up to $200 million in milestone payments to acquire Candid Therapeutics. This clinical-stage company has multiple T-cell engager bispecific and trispecific antibodies for autoimmune and inflammatory diseases. Candid Therapeutics went public in March 2026 through a reverse merger, and it was acquired less than two years after its establishment.

Now zoom out:

In the same quarter, Biogen acquired Apellis for $5.6 billion at $41 per share in cash, a 140% premium over the previous trading day's closing price, securing two marketed products, Syfovre and Empaveli; Merck completed the acquisition of EyeBio for up to $3 billion, with an upfront payment of $1.3 billion, gaining an investigational drug for diabetic macular edema and neovascular AMD.

Novartis completed multiple ophthalmology deals intensively between 2025 and 2026, including the $280 million acquisition of Vedere Bio and the acquisition of EV06, a presbyopia eye drop from Encore Vision; in April 2026, Spark, the gene therapy unit under Roche, reached a $216 million collaboration with SpliceBio, focusing on inherited retinal diseases.

Table: Core M&A Transaction Amounts of the 2026 Pharma FOMO Wave (Unit: Billion USD)

These transactions are not directly related to each other, but when put together, a clear picture emerges: the big pharmaceutical companies are not sporadically replenishing their pipelines, but rather, with an almost synchronized rhythm, they are simultaneously sweeping through several specific sectors.

This is the FOMO wave of 2026. Its driving mechanism, target characteristics, payment structure, and competitive implications are far more complex than they appear at first glance.

01

The Root of Anxiety: A $236 Billion Hole

FOMO (Fear of Missing Out) is not a new term in the pharmaceutical industry. However, the intensity, pace, and target preferences of this round in 2026 are qualitatively different from any previous wave of mergers and acquisitions in history.

The data speaks for itself: this is no longer a routine cyclical shift, but rather a stress test for the industry's underlying profit model.

In the first quarter of 2026, the total value of global biotechnology M&A transactions reached $84 billion, nearly doubling from $44.4 billion in the same period last year. In just the last 12 days of March, seven deals were completed with a total value of $29 billion, marking the strongest start since 2019.

If the current momentum continues, the total value of biopharmaceutical M&A for the year could exceed $250 billion, second only to the historic peak of $328 billion in 2019 driven by mega-deals such as BMS's acquisition of Celgene.

Table: Comparison of Global Biotech M&A Total Amount in 2025Q1 vs 2026Q1 (Unit: Billion USD)

Driving all of this is a wall of certainty.

According to Evaluate Pharma's estimates, by 2030, more than $300 billion of brand drug revenue in the global pharmaceutical industry will face the risk of patent expiration. William Blair's independent analysis provides a more precise figure: the total sales of nearly 50 products in 2025 amount to $162.8 billion, which will plummet to $67 billion by 2029.

Fierce Pharma reported that by 2030, more than $200 billion of biopharmaceutical industry revenue will be at risk due to the loss of exclusivity, and by the early 2030s, another $200 billion will face threats.

The problem lies not only in the trigger of patent expiration but, more profoundly, in the extremely unhealthy revenue structure.

Between 2011 and 2020, among the 168 new drugs approved for the world's top 20 pharmaceutical companies by revenue, only 36 blockbuster drugs accounted for 70% of the total sales of new drugs. The seven strongest performers – representing only 4% of the total number of new drugs – contributed 28% of all new drug revenue. Revenue is highly concentrated in single-digit products, and once the patents for these products expire, the entire revenue structure will face collapse.

Moreover, the distribution of risk exposure is not uniform.

Analysts at JPMorgan and William Blair noted that BMS's Eliquis and Opdivo, which together account for over half of the company’s revenue, will both lose exclusivity between 2026 and 2028, leaving the company facing a growth gap of approximately $38 billion. Merck faces a gap of around $23 billion, as its top product Keytruda, which makes up more than half of the company’s income, will lose patent protection in 2028. Pfizer's gap is approximately $21 billion.

This is the underlying logic of FOMO. When half of a company's revenue is at risk of evaporating, what it needs to do is save its life.

Table: Revenue Gap Comparison of Top Pharmaceutical Companies Facing Patent Cliffs (Unit: Billion USD)

02

The Target of the Buying Spree: Three Tracks, Two Logics

The most counterintuitive characteristic of this FOMO wave is not buying, but what to buy.

Logically speaking, big pharmaceutical companies facing a patent cliff should be aggressively acquiring late-stage assets that have been approved or are about to be approved, and the sooner the better. However, the list of deals in the first quarter of 2026 contradicts this assumption. The target assets are not all at the NDA stage where they are almost ready for approval; many are early- or mid-stage products that have just passed the proof-of-concept phase.

In other words, the logic behind M&A in the current cycle is no longer about betting on a molecule that has already crossed the finish line, but rather buying up key biological nodes across the entire track.

Three tracks constitute the core acquisition areas of this round of FOMO: ophthalmology, autoimmune diseases, and细分 diseases within the central nervous system.

The highest density in ophthalmology.

Bayer Acquires Perfuse's Phase II Molecule PER 001 for $2.45 Billion, Merck Re-enters Ophthalmology Market with $3 Billion Acquisition of EyeBio, Biogen Secures Two Commercialized Ophthalmology and Nephrology Drugs in $5.6 Billion Apellis Acquisition, Novartis Strengthens Gene Therapy and Presbyopia Focus through Vedere Bio and Encore Vision Acquisitions, Roche’s Spark Collaborates with SpliceBio.

These five deals share a common technical anchor: rather than competing in the homogenized small-molecule space, they each place bets on differentiated next-generation technological solutions such as gene therapy, long-acting delivery, complement inhibition, and novel mechanisms for presbyopia.

The approach in the autoimmune sector is different.

UCB Acquires Candid, Securing Multiple T-cell Engager Bispecific and Trispecific Antibodies; Gilead to Acquire Ouro Medicines for $2.175 Billion in March 2026, Gaining BCMA×CD3 TCE Assets. Both deals point to the same logic: reconstructing autoimmune treatment strategies using T-cell engagers.

The autoimmune field has been dominated by TNF inhibitors and IL inhibitors over the past decade, while the goal of TCE is to achieve more precise targeted immune resetting, allowing patients to move from "lifelong medication" to "drug-free remission." Big pharmaceutical companies are not just buying a drug; they are purchasing an entirely new generation of treatment paradigms.

The CNS细分疾病领域 is taking a sharper path.

Eli Lilly Acquires Centessa for $6.3 Billion, Aiming for Its Orexin Receptor Agonist ORX750 for Narcolepsy; Neurocrine Acquires Soleno Therapeutics for $2.9 Billion, Securing Its Newly Approved Prader-Willi Syndrome Drug DCCR.

These two tracks have almost no competitors. Prader-Willi Syndrome has not had an approved drug globally for a long time, and Soleno's DCCR reached $190 million in sales in the nine months before its launch.

The commercial model for orphan drugs does not require a large sales force; a specialized drug sales team of several dozen people can cover the main prescription centers across China, while enjoying a 7-year market exclusivity period and high pricing power granted by the FDA's orphan drug designation.

This reveals a new rule that big pharmaceutical companies have gradually figured out in the FOMO game: instead of competing for market share in broad, generic oncology targets with dozens of competitors, enter a niche field that is narrow enough, deep enough, and has a clean competitive landscape, securing certainty at an acceptable price.

This is also the core source of premium.

03

The Other Side of FOMO: Structural Upheaval in the Global Competitive Landscape

If the patent cliff is the push driving big pharmaceutical companies to buy pipelines, then the structural changes in the global competitive landscape are the accelerators of this round of FOMO.

In the global BD deals of the first quarter of 2026, one signal that cannot be ignored is: Chinese assets are being systematically included in the shopping lists of major pharmaceutical companies.

CSPC Pharmaceutical Group signed a R&D collaboration with AstraZeneca worth up to 18.5 billion US dollars, RemeGen entered into a licensing collaboration with AbbVie valued at 5.6 billion US dollars, Innovent Biologics reached its seventh collaboration with Eli Lilly with milestone payments of up to 8.5 billion US dollars, China Biologic Products authorized Sanofi to develop Rofacitinib for 1.53 billion US dollars, and Hengrui Medicine established a strategic collaboration with BMS potentially worth 15.2 billion US dollars.

Table: Key Collaboration Deals between Multinational Pharmaceutical Companies and Chinese Biotech in 2026 (Unit: Billion USD)

Multinational pharmaceutical companies, facing the patent cliff, must find new sources of supply. China, on the other hand, has just completed its positioning on a new generation technology platform.

ADC, bispecific antibodies, and cell therapy—these next-generation technology platforms are gradually replacing the central role of traditional small molecule drugs. Chinese companies, without the heavy asset burden from the small molecule era, have been able to directly enter the cutting-edge track from the start. Globally, there are over 300 ADC projects in clinical development, with more than 50% originating from China.

This structural shift on the supply side is fundamentally altering the flow of global innovative drug transactions.

At the same time, another variable is exacerbating the tension.

Morgan Stanley's forecast for the end of 2025 shows that by 2040, the proportion of drugs originating from China approved by the FDA will increase from the current approximately 5% to 35%, generating about 220 billion US dollars in income in markets outside of China.

This figure itself explains why some people are getting restless. In April 2026, the U.S. House Appropriations Committee slipped an amendment into an expenditure bill report, proposing to ban the FDA from accepting or reviewing clinical trial data from China – this happened precisely during the busiest trading window driven by FOMO, which is no coincidence.

In this dimension, FOMO is no longer just about "the fear of missing out on a good molecule," but rather "the fear of missing out on an entire emerging supply system." The former can be remedied by a single transaction, while the latter represents a strategic level of anxiety.

However, not all big pharmaceutical companies are going with the flow in this FOMO.

Roche Clearly Stated It Won’t Participate in This Round of Acquisition Frenzy. During the Q1 2026 earnings call, Roche CEO Thomas Schinecke told Fierce Biotech: This is not about being conservative or lacking funds, but a strategic decision based on financial discipline and pipeline confidence. Roche anticipates that nearly 20 new drugs will be launched by the end of 2030, with 16 having blockbuster potential, and nine expected to exceed $3 billion in peak sales.

Roche's calmness precisely confirms a fact from the opposite perspective: the intensity of FOMO is directly proportional to the extent of the patent cliff exposure faced by large pharmaceutical companies. The emptier the pipeline, the deeper the anxiety, and the more urgent the actions. Conversely, those companies busy acquiring assets everywhere have anxieties that are not without foundation.

04

The Secret in the Payment Structure: Risk Pricing and Chip Transfer

A key signal hidden behind the transaction amount lies in the payment structure.

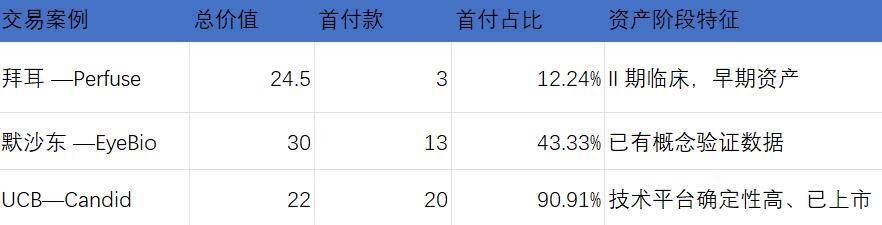

Bayer's $2.45 Billion Acquisition of Perfuse: Only $300 Million as Upfront Payment, Accounting for About 12%. Merck’s $3 Billion Acquisition of EyeBio: $1.3 Billion as Upfront Payment, Accounting for About 43%. In UCB's $2.2 Billion Total Acquisition of Candid, the Upfront Payment Reached $2 Billion, Accounting for About 91%.

Table: Details of Payment Structures for Key M&A Transactions (Amount Unit: Billion USD)

Three payment structures, corresponding to three risk perceptions.

Bayer dares to place the main payment later because Perfuse's PER 001 is still in Phase II, and the data has not been fully locked yet. The essence of the delayed payment is to allow Perfuse's early investors to share the subsequent development risks with Bayer.

MSD's ratio is in the middle, and EyeBio's assets in the AMD field are already supported by concept validation data.

UCB paid 91% of the upfront payment to Candid because the technical certainty of the T-cell engager platform was higher. Additionally, Candid had already accumulated substantial cash reserves after going public through a reverse merger, eliminating the need for a large pharmaceutical company to bear the front-end risk.

This divergence in payment structure sends a clear signal to the acquired party: the seller of early-stage assets no longer receives just an initial payment check, but a composite pricing mechanism of "initial payment anchor + milestone multiplier." The setting and release of each milestone represent an independent, non-blurring risk pricing.

For the global licensing deals that Chinese Biotechs are participating in, the transposition of this logic is very straightforward: the earlier the pipeline stage, the more it requires meticulous milestone design to achieve risk transfer and interest lock-in during valuation negotiations. The collaboration between Hengrui and BMS, which exchanged 13 preclinical projects for a $600 million upfront payment, is a concentrated embodiment of this logic.

This also means that FOMO isn't about endlessly paying high prices for deals. Big pharmaceutical companies act out of anxiety, but they maintain precise control over every penny spent. The real gamble isn't on the upfront payment but on whether the milestones can be achieved. And that depends on the data.

05

Direction: The game has just begun.

Lifting the gaze from single transactions, this round of FOMO is pushing the entire industry's chessboard in three directions.

First, early assets are being systematically repriced.

Candid Therapeutics was acquired in less than two years after its establishment; Soleno was acquired at a premium just one year after DCCR was approved for marketing; the checkbooks in the hands of companies like Eli Lilly, Neurocrine, and Gilead are tilting towards mid-to-early stage pipelines at an unprecedented rate.

This means that the M&A activities of large pharmaceutical companies are no longer purely about "buying certainty," but rather about "buying into a field" and "buying time" — securing differentiated mechanisms, shortening internal R&D cycles, and filling every critical gap before the arrival of the patent cliff. When internal R&D cycles are too long, buying becomes the only accelerator.

Second, the track competition is shifting from a "large target point war of attrition" to a "non-consensus precision battle."

Over the past decade, the major targets in tumor immunology have been crowded with pipelines of PD-1, ADC, and CAR-T, leading to such severe homogenization that even commercial teams couldn't push them forward. However, the FOMO list for 2026 clearly points in another direction: orphan indications, rare endocrine disorders, specific sleep diseases, and ophthalmic gene therapy.

These tracks, though small in patient numbers, feature a clean competitive landscape, extremely high pricing power, and deep policy barriers. Big pharmaceutical companies are beginning to realize: instead of competing with dozens of rivals for a slice of the same pie in a red ocean, it's better to enjoy the entire pie in a blue ocean. The premium that Neurocrine paid to acquire Soleno essentially reflects paying for scale.

Third, the supply landscape of global innovative assets is being reshuffled.

Chinese companies are no longer merely "authorized sellers" but are becoming indispensable structural nodes in the pipeline puzzle of major pharmaceutical firms. The valuation curves of pipelines held by Hengrui, BeiGene, and Innovent, when presented to the same buyers in the U.S. market, are being re-anchored by figures such as Bayer's $2.45 billion, UCB's $2.2 billion, and Biogen's $5.6 billion.

Regardless of whether Chinese Biotechs accept this logic, it is already in operation within the financial models of Merck, Bayer, Biogen, and others. The chessboard has been reset, and the question is no longer about whether it's worthwhile, but rather when and in what capacity Chinese Biotechs will take their seat at the table.

Half of 2026 has passed, but the music hasn’t stopped, and there are still a few chairs left. Everyone must keep dancing amid the wave of FOMO.

This article is based on publicly available information and is intended solely for informational exchange. It does not constitute any investment advice.

This article is from the WeChat Official Account"MediShine", Author: Uncle Yao, 36Kr authorized publication.