Biopharmaceuticals Have No 'Junk Time': A Prospectus on China's Innovation-Driven Drug Development Momentum

Eli Lilly

Global Pharmaceutical R&D and Production Company

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

BeOne

Developer of Molecular Targeted and Immune Anti-Tumor Drugs

In a sluggish market atmosphere, there is a viewpoint: during "historical garbage time," the wise should lie low, watch the show, wait for the garbage time to pass, or seek prosperity elsewhere.

But this does not apply to the biopharmaceutical field. Indeed, many pharmaceutical companies in China have been undervalued and have not returned to normal levels. However, the progress of biopharmaceuticals continues to move forward. At ASCO, EHA, EASL, and ADA, exciting clinical results have emerged one after another. In business history, the first pure pharmaceutical company to break through a market value of 500 billion US dollars has appeared — Eli Lilly. Subsequently, due to achievements in metabolic diseases and neurodegenerative diseases, Eli Lilly's market value has now reached 800 billion US dollars. In the primary market, AI drug discovery has sparked an unprecedented wave of enthusiasm, with a large amount of capital pouring in over the past two years.

Chinese companies are also actively participating in this biopharmaceutical evolution. However, for a period of time, China's innovative drug sector, still a young track, lacked policy support. Now, a nationwide solution to support the development of innovative drugs across the entire chain has finally been introduced: The State Council reviewed and approved the "Full-Chain Support for Innovative Drug Development Implementation Plan." From evaluation and approval, market access, usage, to capital support, especially with international pricing references for innovative drugs and expenditures outside of basic medical insurance, full-chain support for innovative drugs is about to become a reality.

The official full text of the "Implementation Plan for Full-Chain Support of Innovative Drug Development" has not yet been released, but over the past few months—from online leaks to official announcements—the pharmaceutical industry may have already sensed the “policy bottom.” Evaluations from securities firms suggest that the R&D speed of innovative drugs is expected to accelerate, R&D costs are expected to decrease, R&D quality is expected to improve, and return on investment is expected to rise.

A Review of the Development History of China's Biomedical Industry Shows That Bold Reforms Have Paved the Way for the Development of Innovative Drugs. Since 2015, the Release of Milestone Documents Such as the "Opinions on Reforming the Review and Approval System for Pharmaceuticals and Medical Devices" and the "Opinions on Deepening the Reform of the Review and Approval System to Encourage Innovation in Pharmaceuticals and Medical Devices" Have All Activated the Vitality of the Biomedical Industry Chain.

Based on data from the past six months to a year, we want to discuss: Why has the biopharmaceutical industry never entered the so-called "garbage time," and why do we need crucial policy support to "buy time."

Such a contradictory innovative drug

China's pharmaceutical industry, especially in the field of innovative drugs, is both the most vulnerable and the most resilient.

The development of innovative drugs in China has not been going on for a long time. Since its inception, it has been rapidly pushed forward, with relatively weak foundational research. A few years ago, there was a brief phenomenon where the entire market enthusiastically invested money, with both primary and secondary investors contributing, helping innovative drugs to continuously secure funding, which led to breakthroughs for some companies. After a period of rapid growth, there has been a qualitative improvement in the accumulation of talent for innovative drugs, capital investment experience, and biomedical-related infrastructure. However, due to the environment and policy changes, the withdrawal of funding for innovative drugs came too quickly, and the domestic innovative drug companies were also rushed into fulfilling a "people's livelihood" role by making concessions.

Return expectations unmet, financing for innovative drugs hindered, and the entire pharmaceutical industry's capital circulation and development flywheel stalled. According to Wind data, the proportion of loss-making pharmaceutical companies in China has reached a historical high. From January to April, the revenue of large-scale pharmaceutical industrial enterprises nationwide amounted to 807.78 billion yuan, still continuing to decline—although the year-on-year decrease of 0.8% has improved compared to last year’s sharp fall.

But on the other hand, innovative drugs continue to take root, sprout, and bear fruit. According to VCBeat data, in the first half of 2024, Chinese pharmaceutical companies completed 48 cross-border License-out deals, reaching a record high. A significant proportion of these were projects in the preclinical and IND stages.

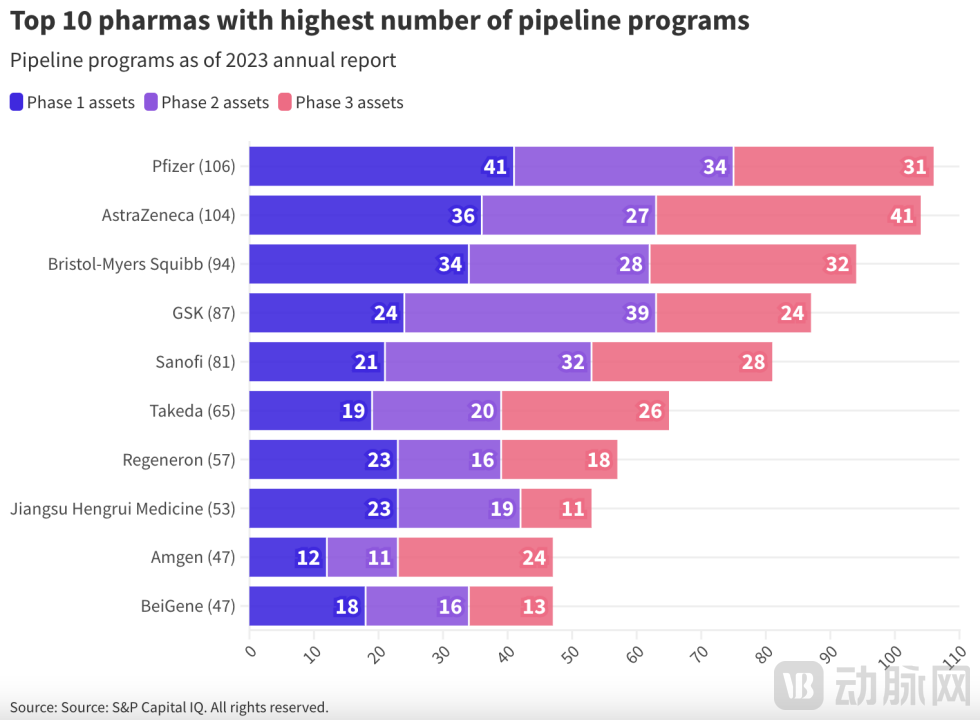

Such a BD boom stems from the rapid growth and massive accumulation in China's innovative drug development. By the end of 2023, in terms of companies developing new drugs, the number of new drug R&D enterprises in China accounted for 16% of the global total; regarding the new drug pipelines under development, China had over 6,000 new drug developments, ranking second globally in both categories. Only in 2023, there were 1,241 IND applications for China’s Class 1 new drugs, marking a year-on-year increase of 31.7%.

Companies like Hengrui Pharma and BeOne Medicines have even ranked among the top ten globally in terms of pipeline quantity.

But paradoxically, behind such a massive pipeline of innovative drugs, the proportion of R&D expenditure has remained relatively low. In 2023, the total R&D expenditure of 486 A-share listed pharmaceutical companies in China was approximately 119.2 billion yuan, accounting for about 4.72% of their investment.

In 2023, BeOne Medicines' total R&D expenditure for the year reached 12.53 billion yuan, accounting for approximately 71%. BeOne Medicines is the most generous pharmaceutical company in terms of R&D investment in China. Before BeOne Medicines went public, Hengrui Pharma was the most generous in R&D investment among A-share pharmaceutical companies. However, by 2023, Hengrui Pharma's R&D investment was only 6.15 billion yuan, which was the result of a tenfold increase in R&D investment over a decade.

In 2023, the average R&D expenditure of the top ten global MNCs was $12.718 billion, with an average R&D spending ratio of 23.7%. According to an analysis by a Nature sub-journal, the return on investment for innovative drugs overseas has hit a 20-year low, with almost no financial returns. However, the substantial investment in R&D by MNCs has never stopped, as the pharmaceutical industry requires continuous heavy investment in innovation to achieve returns.

China's innovative drug industry needs the courage to compete with multinational corporations (MNCs), while also addressing cost constraints typical of the industry's early development stage, and adapting to the payment environment. Despite these challenging "dual demands," China’s innovative drug sector has achieved significant progress. Moreover, given the pharmaceutical industry's close connection to public welfare, the need for reasonable support policies in this sector is arguably more urgent than in any other industry.

Sharing the same fate? Not true.

In the first half of the year, only 45 out of 495 pharmaceutical companies in China's A-share market saw their stock prices rise, meaning that over 90% of pharmaceutical stocks fell. Among the few dozen companies that did see an increase, only four had gains exceeding 50%, compared to as many as 31 companies with similar gains during the same period in 2023.

Only Five Pharma Companies with Over 100 Billion Market Cap Remain: Mindray Medical, Hengrui Pharma, BeOne Medicines, Pien Tze Huang, and WuXi AppTec. The Combined Market Cap of the Top 20 Pharma Stocks Totals 1.9 Trillion Yuan, Down 20.8% from 2.4 Trillion Yuan in the First Half of 2023.

Innovative Drug ETF

Since the establishment of the Innovative Drug ETF four years ago, its peak (1.638 yuan) occurred in August 2020, and by June 2024, it had fallen to only a fraction of its highest point.

And due to the particularity of innovative drug companies — likely being in a state of continuous losses before product commercialization, the number of newly listed innovative drug companies in the first half of this year was directly 0 in the face of the strict listing thresholds of the STAR Market.

By contrast, the situation in the Hong Kong stock market is slightly better, with four pharmaceutical companies successfully obtaining tickets to the capital market, raising a total of approximately HK$1.9 billion. These include "China's first autoimmune stock" Quanxin Biotech and the first company to be listed under Rule 18C, "AI Pharma First Stock" XtalPi.

The second half of the year may see more biopharmaceutical IPOs in the Hong Kong stock market. George Chan, EY's Global IPO Leader, recently revealed in an interview with the media that his company’s Hong Kong capital team is extremely busy at present. It is expected that the number of new stocks will increase in the second half of the year, and the Hong Kong IPO market will significantly improve in the next five years. The Hong Kong Stock Exchange is currently processing 89 IPO applications, among which 16 have been approved by the Listing Committee and are awaiting listing, with biopharmaceutical companies forming the main force.

Hong Kong-listed pharmaceutical companies, especially many Chapter 18A companies, have successively turned profitable since last year. However, even so, 20 companies under Chapter 18A have seen their market value drop by over 90%. Overall, among Hong Kong-listed pharmaceutical enterprises, only Kelun-Biotech, Innovent Biologics, and Akeso Biopharma have experienced growth in market value.

But across the ocean, they have gradually emerged from the cold winter.

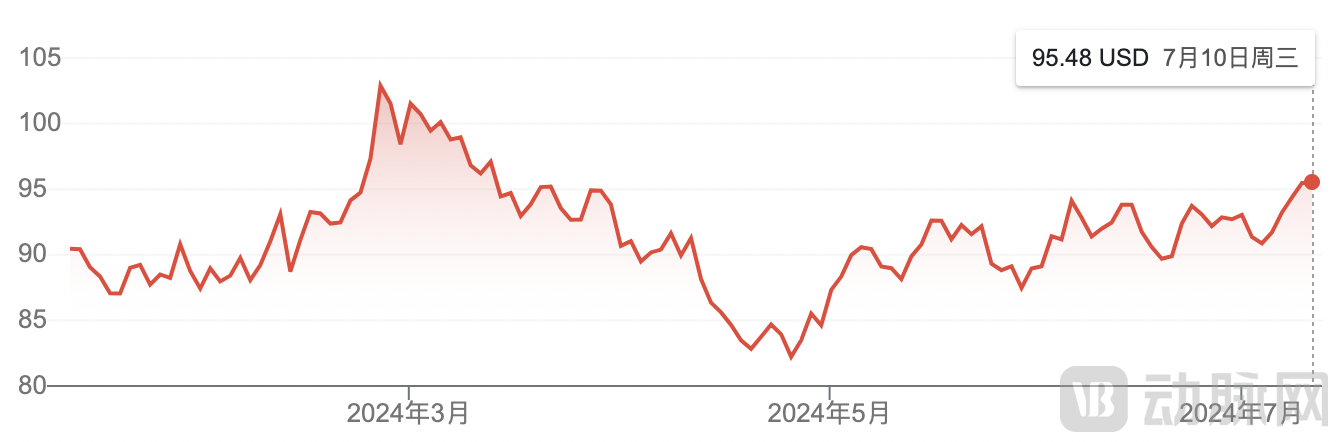

XBI Index

From the perspective of the secondary market, the XBI index is around $93, lower than the recent high of $103.52 at the end of February 2024, but still higher than the low of $65 when the rebound began in October 2023.

Biotech Fundamentals Show Clear Improvement, Follow-up Market and M&A Activities at Record Levels. Brian Gleason, Managing Director of Raymond James, revealed that the current financing scale in the U.S. secondary equity market has exceeded $22 billion, reaching an all-time high; the closest comparison is $18.8 billion from 2021 during the same period.

This means that companies with good clinical data performance can secure funding, and the number of companies with improved cash flow is increasing. The original innovation in Biotech is very active, which forms the basis for capital inflow into the industry. These strong fundamental factors, combined with lower interest rates, will likely lead to an even better performance for Biotech later this year.

In terms of primary market financing, more than 50 American Biotech companies completed financings of over 100 million US dollars in the first half of this year. These include Xaira, an AI protein design company that raised 1 billion US dollars in a seed round, Mirador, a precision immunology company that secured 400 million US dollars, and Formation Bio, an AI pharmaceutical company highly favored by Sam Altman, among others.

Endpoints News pointed out that if this pace continues, the scale of biotech financing in 2024 may surpass the peak levels of 2020 and 2021.

Accordingly, American venture capital firms are also actively raising funds to prepare for investment projects. Among them are new funds, such as Goldman Sachs' first life sciences fund, which raised $650 million. Meanwhile, established Biotech investors are also busy: Arch Venture outlined plans in February to raise $3 billion, while Canan Partners recently added $100 million to its 13th fund.

China and the United States are among the few countries globally capable of supporting a complete Biotech ecosystem. However, the distinctive feature of the U.S. Biotech ecosystem is that even during industry downturns, new waves of innovation and companies can quickly emerge. A notable characteristic is the continuous supply of market funding, which remains active even during market slumps. Particularly, multinational corporations (MNCs) with substantial financial strength continue to create value and opportunities for Biotech through business development (BD) activities.

The U.S. Biotech Winter is More Like a Bubble Clearance, Making Room and Resources for Valuable Innovations; After the Market Purification Process Ends, Companies and Projects with Real Strength Will Regain Funding Support. This Mechanism Ensures Continuous Innovation and Development Momentum in the Industry.

When the innovation highland of life sciences is once again gathering momentum for a new round of Biotech development, it would be a pity if China's innovative drug sector were to pause and hesitate at this moment.

What to Expect Next?

In fact, economist Mises did not provide a definition for "the garbage time of history." On the contrary, he pointed out: the occurrence of historical events depends on the choices and actions of individuals and groups at specific moments. Every individual's choice will have an impact on history, even if the influence appears to be small.

Every link in China's biopharmaceutical industry chain is making choices that advance the industry. For instance, companies and founders who have adhered to their original aspirations of drug development over the years, innovative explorations by financial institutions, as well as investment organizations willing to support the growth of China's innovative drugs.

For instance, we can see that the accessibility of innovative drugs in China is also continuously improving. In terms of approvals, in the first half of 2024, a total of 44 new drugs were approved for the first time in China, among which Class I innovative drugs accounted for a significant proportion, reaching 23. In addition, nearly 50 new drugs received approval in China for new indications or new formulations.

In terms of payment, recent policies have been introduced in various regions. According to the "Several Measures of Beijing Municipality to Support High-Quality Development of Innovative Pharmaceuticals (2024)," eligible expenses for new drugs and technologies will not be included in the DRG payment standard but will be paid separately. Meanwhile, Guangzhou has proposed establishing a directory of major innovative pharmaceutical products in Guangzhou and setting up a procurement incentive mechanism for products listed in the directory.

It was generally believed that the development dilemma of innovative drugs focused on the payment process, which involved several key issues: how to be included in the medical insurance system, how to enter the hospital system, how to obtain doctors' prescriptions, and how to ensure patients could access these drugs at a reasonable price. These challenges formed a complex path for innovative drugs from research and development to ultimately benefiting patients.

We are highly anticipating the official full text of the "Implementation Plan for Full-Chain Support of Innovative Drug Development." If the plan can be implemented, this predicament is very likely to improve. Although the situation may not be immediately and comprehensively resolved through a single high-level policy document, the emphasis on innovative drugs undoubtedly conveys a positive signal. This indicates that at the national strategic level, innovative drugs are regarded as an essential component of new productive forces and will receive substantial support and development.

China's biomedicine should never have a "garbage time." On the contrary, this is a period worthy of disrupting old models, surpassing current limitations, and achieving new breakthroughs.