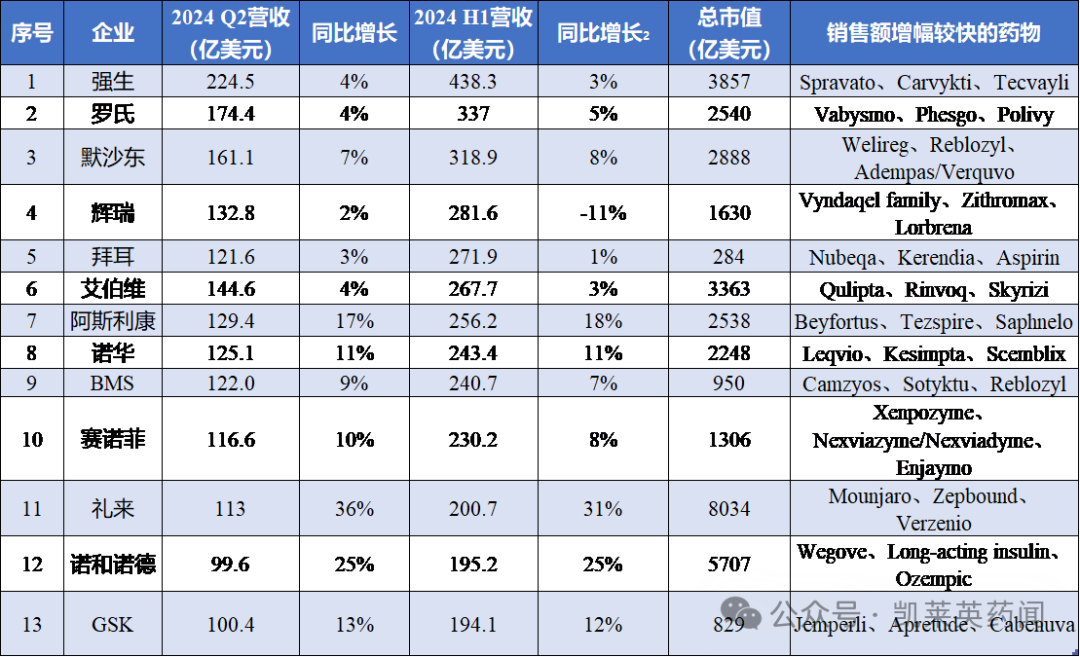

2024 H1 Global Top 10 MNC Pharma Companies: Revenue Highlights and Key Product Performance

Johnson & Johnson

Medical Device R&D and Manufacturer

Welcome to follow Asymchem Pharma News

As global pharmaceutical companies have successively disclosed their Q2 2024 financial reports, the H1 revenue of each company has also shown some changes compared to Q1 2024.

Sorted by the total revenue of pharmaceutical companies,Q2 Revenue Ranking in Order:Johnson & Johnson, Roche, Merck & Co., AbbVie, Pfizer, AstraZeneca, Novartis, Bristol-Myers Squibb (BMS), Bayer, Sanofi.

H1 Revenue Ranking in Order is: Johnson & Johnson, Roche, Merck & Co., Pfizer, Bayer, AbbVie, AstraZeneca, Novartis, BMS, Sanofi.

1

Johnson & Johnson

On July 17, Johnson & Johnson released its 2024 H1 financial results, with total revenue of $43.83 billion, a year-on-year increase of 3.3%; Q2 revenue was $22.45 billion, a year-on-year increase of 4.3%. Innovative pharmaceuticals accounted for $28.05 billion in H1 revenue, a year-on-year increase of 3.3%; medical device revenue reached $15.78 billion, a year-on-year increase of 3.3%. The growth in innovative drug sales was primarily driven by oncology drugs, with oncology drug revenue reaching $9.90 billion in the first half of the year, a year-on-year increase of 16.4%; immunology drug revenue was $8.97 billion, a year-on-year increase of 4.2%; other areas including neuroscience, infectious diseases, cardiovascular, and metabolism experienced varying degrees of decline. Key drugs such as Darzalex (daratumumab), Erleada (apalutamide), Tremfya (guselkumab) and Stelara (ustekinumab) in immuno-oncology, as well as Spravato (esketamine) in neuroscience, contributed significantly to sales. Notably, Carvykti (cilta-cel), a CAR-T therapy developed in collaboration with Legend Biotech, generated $340 million in revenue in the first half of the year, a year-on-year increase of 81.5%; Tecvayli (teclistamab), a bispecific antibody, achieved $270 million in revenue in the first half of the year, a year-on-year increase of 70.2%, showing potential to become the company’s next-generation pillar product in the oncology field.

In terms of transactions, the company acquired several products in the first half of the year through the acquisition of Ambrx, including the PSMA-targeted ADC drug ARX517 (JNJ-8177). Additionally, through the acquisitions of Proteologix and Yellow Jersey, the company obtained products such as the IL-13/TSLP bispecific antibody PX128, the IL-13/TSLP bispecific antibody PX130, and the IL-4Rα/IL-31 bispecific antibody ND026. Apart from innovative drugs, the company also completed the acquisition of Shockwave for $13.1 billion. Shockwave is a company that provides intravascular lithotripsy (IVL) for coronary arteries, focusing on offering innovative solutions for the treatment of calcified lesions in coronary artery disease (CAD) and peripheral artery disease (PAD). With this transaction, Johnson & Johnson has regained its top position in the cardiovascular field and topped the list in the medical device sector.

The company forecasts adjusted earnings per share of $9.97 to $10.07 for 2024, down from the prior estimate of $10.57 to $10.72; projected sales are $88 billion to $88.4 billion.

2

Roche

On July 25, Roche released its 2024H1 financial results, with total revenue of 29.848 billion Swiss francs, a year-on-year increase of 5% (calculated at constant exchange rates, CER); excluding COVID-19 related products, the growth was 8%. Specifically, pharmaceutical business revenue reached 22.637 billion Swiss francs, a year-on-year increase of 5%, while diagnostics business revenue was 7.211 billion Swiss francs, also with a year-on-year increase of 5%. Within the pharmaceutical segment, oncology revenue amounted to 9.619 billion Swiss francs, a year-on-year increase of 4%, driven by products such as Perjeta (pertuzumab), Alecensa (alectinib), and Avastin (bevacizumab). Notably, the combination drug Phesgo (trastuzumab + pertuzumab) achieved sales of 799 million Swiss francs in the first half of the year (a year-on-year increase of 60%), and Polivy, a CD79b-targeted ADC drug, recorded sales of 513 million Swiss francs in the first half of the year (a year-on-year increase of 54%), making them among the products with the highest sales growth in this field. Additionally, ophthalmology revenue reached 1.891 billion Swiss francs, a year-on-year increase of 54%, largely due to the significant sales increase of Vabysmo (faricimab) which grew by 93% year-on-year.

In addition, Roche also disclosed updates on the company’s R&D pipeline in its financial report: Since Q2 of 2023, the company has terminated 25% of its new molecular entity pipelines under research; this includes abandoning two Phase III studies of the TIGIT monoclonal antibody tiragolumab in combination with atezolizumab for the treatment of non-small cell lung cancer (NSCLC), the Phase II/III SKYSCRAPER-06 study of tiragolumab as a first-line treatment for NSCLC, and the GOLDEN study of complement factor B antisense therapy RG6299 for geographic atrophy.

The company raised its full-year 2024 profit forecast, expecting total revenue to achieve mid-single-digit growth.

3

Merck & Co.

On July 30, Merck released its 2024H1 performance, with total revenue of $31.887 billion, a year-on-year increase of 8%; Q2 revenue was $16.112 billion, a year-on-year increase of 7%. Among this, H1 revenue in China was $3.534 billion, pharmaceutical business revenue was $28.415 billion, a year-on-year increase of 9%; R&D investment was $7.492 billion, a year-on-year decrease of 57%.

In the pharmaceutical business segment, Keytruda (Pembrolizumab) generated revenue of $14.217 billion, representing an 18% year-over-year increase. According to statistics, Keytruda has now been approved for 40 indications, with additional indications still under exploration. The market is expected to continue growing and may achieve a sales record of $30 billion this year. Aside from Keytruda, the HPV vaccine Gardasil/Gardasil 9 reported revenue of $4.727 billion, marking a 7% year-over-year increase. The main growth driver was higher sales in the U.S., attributed to premium pricing, strong demand, and public sector purchasing patterns. In contrast, sales in the Chinese market declined compared to the same period last year.

In terms of transactions, the company acquired the rights to three ADC drugs—HER3-DXd, I-DXd, and R-DXd—from Daiichi Sankyo for $22 billion in the first half of the year, exploring the therapeutic potential of ADC monotherapy and its combination with PD-1. Additionally, the company announced a $10.8 billion acquisition of Prometheus, a clinical-stage company focused on developing treatments for ulcerative colitis (UC), Crohn's disease (CD), and other autoimmune diseases; this acquisition will further strengthen the company’s presence in the autoimmune field.

4

Pfizer

On July 30, Pfizer released its 2024 H1 financial results, with total revenue of $28.162 billion, a year-on-year decrease of 11%; net profit was $3.156 billion, a year-on-year decrease of 60%. The performance was still affected by the COVID-19 vaccine Comirnaty and the oral medication Paxlovid. In Q2, revenue was $13.283 billion, representing a year-on-year increase of 2%. Excluding Comirnaty and Paxlovid, revenue increased by 14% year-on-year. In the first half of the year, R&D expenses amounted to $5.189 billion, a year-on-year increase of 1%. Based on confidence in further recovery in H2 performance, Pfizer raised its 2024 guidance to $59.5 billion - $62.5 billion.

Among them, H1 oncology business revenue reached 7.505 billion USD, increasing by 23% year-on-year; this was mainly driven by the contributions of Xtandi (enzalutamide) and ADC products acquired from Seagen. In the vaccine field, the H1 revenue of Prevnar series products was 3.05 billion USD, growing by 1% year-on-year; Abrysvo revenue amounted to 201 million USD; furthermore, the company’s next-generation PCV candidate products, RSV vaccine, and combined COVID-19/influenza vaccine are proceeding steadily. In other fields, the growth of Vyndaqel (tafamidis) in the cardiovascular sector was primarily propelled by strong demand in international developed markets such as the United States; the growth of Eliquis (apixaban) was mainly due to the continuous adoption of oral anticoagulants and an increased market share for non-valvular atrial fibrillation indications in certain markets in the US and Europe; global operational growth of migraine drug Nurtec ODT/Vydura (rimegepant) reached 44%, mainly driven by robust demand in the US market and momentum in international markets.

5

Bayer

On August 6, Bayer released its 2024H1 financial results, with total revenue of 24.909 billion euros, a year-on-year increase of 1%, and net profit of 1.123 billion euros. In the second quarter of 2024, sales reached 11.144 billion euros, a year-on-year increase of 3%. Among them, pharmaceutical business revenue in the first half of the year was 8.963 billion euros, a year-on-year increase of 4%, with the best-selling drugs being Xarelto (rivaroxaban) and Eylea (aflibercept); Nubeqa (darolutamide) and Kerendia (finerenone) contributed to significant sales growth. Strategically, the company terminated the Phase II study of zabedosertib for the treatment of atopic dermatitis, as well as the development of the soluble guanylate cyclase (sGC) activator runcaciguat.

In terms of transactions, BlueRock, a subsidiary of Bayer, obtained the exclusive license for OpCT-001 in January of the first half of the year. OpCT-001 is an induced pluripotent stem cell (iPSC)-derived cell therapy candidate for the treatment of primary photoreceptor diseases. Additionally, the company invested $310 million to acquire the exclusive commercialization rights for acoramidis in Europe from BridgeBio. Acoramidis is an oral transthyretin (TTR) small molecule stabilizer used to treat transthyretin-mediated amyloidosis with cardiomyopathy (ATTR-CM). Bayer also entered into a strategic collaboration with Aignostics, aiming to create a new target identification platform by deeply integrating AI machine learning with biological, chemical, and clinical data, thereby advancing the development of precision oncology treatment solutions. Furthermore, Bayer partnered with Evotec to leverage Evotec's human-induced pluripotent stem cell disease models for developing innovative therapies.

6

AbbVie

On July 25, AbbVie announced its 2024H1 financial results, with total revenue reaching $26.772 billion, a year-on-year increase of 3.7% (at constant exchange rates). Breaking it down by segment, the company's main businesses include immunology, oncology, aesthetics, neuroscience, and ophthalmology. The respective revenues for the first half of the year were $12.342 billion (+0.6%), $3.177 billion (+11%), $2.639 billion (+0.3%), $4.127 billion (+15.6%), and $1.071 billion (-10.6%).

In the immunology field, although Humira (adalimumab) dropped to $5.084 billion with a decline of approximately 32%, Skyrizi (risankizumab) and Rinvoq (upadacitinib) generated revenues of $4.735 billion (+46.6%) and $2.523 billion (+60.4%), respectively, offsetting the losses caused by the expiration of Humira's patent. In the oncology sector, the continuous growth of Venclexta (venetoclax), the approval of Epkinly (epcoritamab) in May of last year, and the acquisition of ImmunoGen’s targeted FRα ADC drug Elahere (mirvetuximab soravtansine) contributed to the sustained increase in sales within this field. In the neuroscience area, products such as Ubrelvy (ubrogepant), Qulipta (atogepant), and Vraylar (cariprazine) also demonstrated strong performance.

In terms of transactions, the company invested in three promising drugs in the inflammatory bowel disease (IBD) field in the first half of the year, including: (1) acquiring Landos for $137.5 million to obtain the NLRX1 agonist NX-13; (2) signing a licensing agreement with Mingji Biotech to co-develop the preclinical TL1A antibody FG-M701; (3) acquiring Celsius, a clinical-stage company, to obtain the TREM1 antibody CEL383.

7

AstraZeneca

On July 25, AstraZeneca announced its 2024 H1 financial results, with total revenue of $25.6 billion, representing an 18% year-over-year increase; Q2 revenue reached $12.9 billion, up 17% year-over-year. In the first half of the year, revenue in China amounted to $3.4 billion, a 15% year-over-year increase; R&D investment was $5.8 billion, marking a 10% year-over-year growth.

The company's main revenue drivers stem from sales growth in the fields of oncology, cardiovascular, renal, and metabolic (CVRM), respiratory, and rare diseases (R&I). In the oncology sector, revenue for the first half of the year reached $10.4 billion, representing a 22% year-over-year increase, with major growth momentum driven by Tagrisso (osimertinib), Calquence (acalabrutinib), Imfinzi (durvalumab), Lynparza (olaparib), and Enhertu (trastuzumab deruxtecan). In the CVRM sector, dapagliflozin generated $3.8 billion in sales in the first half of the year, marking a 38% year-over-year increase, primarily due to its widespread use among patients with heart failure and chronic kidney disease. In the R&I sector, Symbicort and Fasenra have promoted broad market application as innovative respiratory drugs. In the rare disease sector, C5 complement inhibitors eculizumab and ravulizumab contributed $3.243 billion, alfaelosulfase injection contributed $653 million, and the new NF1 drug selumetinib added $410 million.

In the transactions, the company introduced Pinetree's preclinical EGFR degrader candidate for a total price of $540 million, and acquired Fusion for $2.4 billion to obtain multiple RDC drugs, strengthening its oncology portfolio.In 2024, AstraZeneca's full-year performance is expected to achieve a mid-teens growth (previously estimated at low double digits).

8

Novartis

On July 18, Novartis released its financial results for the first half of 2024, reporting total revenue of $24.3 billion, a year-on-year increase of 11% (at constant exchange rates); net profit reached $5.9 billion, up by 43%. Revenue in China amounted to $2.1 billion, marking a year-on-year growth of 29%. The company primarily focuses on four therapeutic areas: cardiovascular and renal metabolism, immunology, neuroscience, and oncology. In the cardiovascular and renal metabolism segment, Entresto achieved sales of $3.8 billion, increasing by 32%, driven by deeper penetration in heart failure and hypertension markets; RNAi therapy Leqvio generated sales of $300 million, surging by 137%. In the immunology segment, drugs such as Cosentyx (secukinumab), Xolair (omalizumab), and Ilaris (canakinumab) fueled market expansion. In the neuroscience segment, Kesimpta (ofatumumab) for multiple sclerosis and Zolgensma, a gene therapy for spinal muscular atrophy, recorded sales of $1.4 billion (+66%) and $600 million (+6%), respectively. In the oncology segment, Kisqali achieved first-half sales of $1.3 billion, growing by 52%, benefiting from recognition of its overall survival benefits in HR+/HER2- advanced breast cancer; two radiopharmaceuticals, Pluvicto and Lutathera, reported first-half sales of $700 million (+45%) and $300 million (+16%), respectively.

9

Bristol-Myers Squibb

On July 26, Bristol-Myers Squibb ("BMS") released its 2024H1 financial results, with total revenue of $24.066 billion, a year-on-year increase of 7%; Q2 revenue was $12.201 billion, a year-on-year increase of 9%. In the first half of the year, R&D investment reached $5.594 billion, a year-on-year increase of 22%. The company's performance growth was mainly driven by sales in the fields of oncology, hematology, and cardiovascular diseases, contributing $6.633 billion, $6.860 billion, and $7.359 billion in revenue respectively, accounting for 87% of BMS's total revenue in the first half of the year. In the field of oncology, three key drugs—Opdivo (nivolumab), Opdualag (nivolumab + relatlimab), and Yervoy (ipilimumab)—generated $6.119 billion in revenue. Additionally, the subcutaneous injection formulation of nivolumab is expected to receive regulatory approval by the end of the year, which could provide new momentum to the oncology sector. In the field of hematological diseases, two CAR-T cell therapies, Breyanzi and Abecma, generated revenues of $260 million (+52%) and $177 million (-37%), respectively, in the first half of the year. Since its market approval, BMS has been continuously expanding the indications for Breyanzi, including accelerated FDA approval in March this year for the treatment of relapsed/refractory chronic lymphocytic leukemia (R/R CLL) or small lymphocytic lymphoma (SLL), and approval in May this year for the treatment of relapsed or refractory mantle cell lymphoma. In the cardiovascular disease field, the oral anticoagulant Eliquis performed the best, with H1 revenue exceeding $7.1 billion.

In the first half of the year, BMS also adjusted its pipeline, terminating Alnuctamab, a BCMA/CD3 bispecific T-cell engager that had already entered Phase 3 clinical trials. In terms of deals, BMS reached an $1.865 billion collaboration with Repertoire to jointly develop vaccines targeting up to three autoimmune diseases. At the beginning of the year, BMS acquired RayzeBio, a radiopharmaceutical company, for $4.1 billion, gaining access to a differentiated radiopharmaceutical platform based on alpha-emitting radionuclides and several innovative drug candidates under development.

10

Sanofi

On July 25, Sanofi released its 2024H1 financial results, with total revenue of €21.209 billion, representing an 8.4% year-on-year increase; Q2 revenue reached €10.745 billion, a 10.2% year-on-year growth. In the first half of the year, the company's pharmaceutical business revenue was €16.059 billion (+9.6%), vaccine revenue was €2.319 billion (+0.3%), and consumer healthcare business revenue was €2.831 billion (+9.2%). Among these, the core product Dupixent (dupilumab) generated revenue of €6.138 billion in the first half. In July 2024, the European Medicines Agency (EMA) approved dupilumab as an add-on maintenance treatment for adult patients with chronic obstructive pulmonary disease (COPD) characterized by blood eosinophilia and who remain uncontrolled. The company is expected to achieve several key milestones in the second half of the year, including the U.S. market application for COPD (PDUFA date: September 27), the U.S. market application for adolescent patients with chronic rhinosinusitis with nasal polyps (CRSwNP) (PDUFA date: September 15), EU indication expansions for pediatric patients with eosinophilic esophagitis (EoE) and chronic spontaneous urticaria, among others. Additionally, as one of the largest vaccine suppliers, total vaccine sales in H1 2024 amounted to €1.348 billion, with increased sales across meningitis vaccines, travel vaccines, endemic disease vaccines, RSV vaccines, and influenza vaccines.

In addition, the company has made some adjustments to its product pipeline, cutting two pipelines, including terminating the Phase II study of complement C1s monoclonal antibody riliprubart for cold agglutinin disease, and terminating the Phase I study of quadrivalent influenza mRNA candidate vaccine SP0273.And deprioritize the clinical development of three products: the Phase II study of FGFR3 antibody SAR442501 for the treatment of achondroplasia, the Phase I study of TGF-β antibody SAR439459 for osteogenesis imperfecta, and the Phase I study of PH4H-targeted gene therapy SAR444836 for phenylketonuria.

11

Eli Lilly

On August 8, Eli Lilly released its 2024 H1 financial results, with total revenue of $20.071 billion, representing a year-on-year increase of 31%; Q2 revenue reached $11.303 billion, marking a year-on-year growth of 36%. The net profit for the first half of the year was $5.210 billion, reflecting a 74% year-on-year increase. Based on the performance in the first half of the year, Eli Lilly raised its full-year revenue forecast to $45.4–46.6 billion. The company's revenue growth was mainly driven by increased sales of Mounjaro, Zepbound, Verzenio, Taltz, and Jardiance. In the diabetes and weight loss sectors, total revenue for the first half of the year reached $13.008 billion, showing a 42% year-on-year increase. Revenue from Mounjaro (tirzepatide for glycemic control) was $4.897 billion, while Zepbound (tirzepatide for weight loss) generated $1.761 billion, bringing cumulative revenue to $6.658 billion. Jardiance (empagliflozin) achieved revenue of $1.456 billion, reflecting a 17% year-on-year increase. In the oncology field, Verzenio (abemaciclib) reported revenue of $2.382 billion for the first half of the year, with a year-on-year growth of 42%. Regarding the pipeline, the company removed several studies, including Phase III trials of abemaciclib (a CDK4/6 inhibitor) for hormone-sensitive prostate cancer and empagliflozin for post-myocardial infarction treatment; a Phase II study of GBA1 gene therapy for type 2 Gaucher disease; as well as Phase I studies of an NRG4 antagonist for heart failure, a PI3K selective inhibitor for cancer treatment, a GITR antagonist, and an undisclosed molecule for autoimmune diseases.

12

Novo Nordisk

On August 7, Novo Nordisk released its 2024 H1 financial results, with total revenue of 133.4 billion Danish kroner, representing a year-on-year increase of 24%. Of this, revenue from the China region in the first half of the year reached 9.5 billion Danish kroner, a year-on-year increase of 10%. In the diabetes and obesity care business unit, revenue for the first half of the year was 125 billion Danish kroner, a year-on-year increase of 27%. Specifically, the injectable semaglutide for diabetes, Ozempic, generated revenue of 56.7 billion Danish kroner, a year-on-year increase of 36%; the oral semaglutide for diabetes, Rybelsus, achieved revenue of 10.9 billion Danish kroner, a year-on-year increase of 32%; the weight management injectable Wegovy brought in revenue of 21 billion Danish kroner, a year-on-year increase of 74%. The combined total revenue from these products was 88.7 billion Danish kroner, with an estimated annual revenue expected to comfortably exceed $25 billion. Revenue from insulin products amounted to 27 billion Danish kroner, a year-on-year increase of 10%. In the rare disease sector, revenue for the first half of the year was 8.4 billion Danish kroner, a year-on-year decrease of 3%.

On the pipeline, the company completed the Phase III FRONTIER 2 trial of Mim8, a bispecific antibody targeting FIXa and FX. Additionally, the Phase III CLARION-CKD trial of ocedurenone, an MR antagonist for treating advanced chronic kidney disease (CKD) with refractory hypertension, was halted as ocedurenone failed to meet the primary endpoint.

13

GSK

On July 31, GlaxoSmithKline ("GSK") released its 2024H1 financial results, with total revenue reaching £15.247 billion, a year-on-year increase of 12%; Q2 revenue was £7.884 billion, up 13% year-on-year. The company's vaccine, specialty medicine, and oncology businesses performed strongly in the first half of the year. Vaccine sales in the first half amounted to $4.276 billion, an 8% increase, driven primarily by meningococcal vaccines (Meningitis), the shingles vaccine Shingrix, and the RSV vaccine Arexvy. In the specialty medicines segment, HIV products (including Dolutegravir products, Dovato, Tivicay, Triumeq, and Cabenuva) contributed £3.370 billion (+14%). Revenue from respiratory/immunology reached £1.546 billion (+15%) in the first half, with steady growth maintained for products like Nucala, Benlysta, and Trelegy. Oncology revenue also reached £629 million.

References

1. Official Websites of Various Companies

2. PharmaResearch, PharmSnap, PharmaCube, PharmData, 21st Century Economic Report, Oreo Daily, Every Day Economic News, Pharmaceutical Economy News, Biopharma Times, BiG Biotech Innovation Community, Insight Data, MedClub

"Views"Click once