Domestic Subunit Influenza Vaccines Rise Amid Import Supply Disruption

Sanofi

Pharmaceutical R&D Developer

This Year's Flu Season Is Unusual.

On August 27, Sanofi announced that it had decided to temporarily halt the supply and sales of its Pasteur influenza vaccine in China due to potency issues. The specific reason is: a declining trend in the potency (reference data related to the expected biological effect of the vaccine) of the inactivated influenza vaccines Fluvax (trivalent) and Flublok (quadrivalent) for the 2024-2025 influenza season has been observed.

As a vaccine giant, Sanofi holds a certain scale in China's influenza vaccine market. In the first half of 2024, Sanofi accounted for 18% of the batch release of trivalent influenza vaccines and 15% of the batch release of quadrivalent influenza vaccines.

"This recall is a rare occurrence in China's vaccine market in recent years," an industry insider told VCBeat. "It can be said that it has caught local disease control centers off guard, and also made community hospitals and vaccination clinics feel challenged. Many people who have been vaccinated with Sanofi have come to inquire about solutions."

This Year's "Flu Surge" Is Fierce: According to the June 2024 national legal infectious disease report, the number of flu cases reached 314,709, a six-fold increase compared to 65,289 cases in the same month last year. Notably, June is not typically a peak season for flu. Generally, the flu vaccination season starts in September each year. However, this year, the flu vaccination schedule has been moved forward significantly compared to previous years.

In addition, this year marks the first year of a general price reduction for flu vaccines. In May this year, Sinopharm Group took the lead in reducing the price of flu vaccines to below 100 yuan, with the bid prices of its quadrivalent influenza virus split vaccines from the Changchun Institute, Wuhan Institute, and Shanghai Institute dropping from 128 yuan per dose to 88 yuan per dose. Subsequently, Hualan Biological Bacterin Co., Ltd., Sinovac Biotech, and Jindike Biotechnology, among other flu vaccine manufacturers, successively announced price cuts in June. Whether voluntary or involuntary, flu vaccine manufacturers have joined this price war.

After the "Battle" of the Flu Season Without Imported Vaccines, Who Will Take the Lead?

After Saying Goodbye to Imported Vaccines

On the day Sanofi Pasteur announced the suspension of supply and marketing of its flu vaccine, Hualan Biological Bacterin Co., Ltd.'s stock price surged to the daily limit. Previously, due to a general price reduction of flu vaccines and possible poor performance, the stock price of Hualan Biological Bacterin Co., Ltd. had once dropped to a historical low before August 26.

Hualan Vaccine stated that it has now entered the peak season for flu vaccine inoculations. The absence of Sanofi's flu vaccine will objectively create a gap in the flu vaccine supply, which is beneficial for other vaccine manufacturers. In the first half of 2024, the batch release of Hualan Vaccine's inactivated flu vaccine accounted for 66.38%, securing an absolutely leading position in the flu vaccine market.

Sanofi Pasteur's trivalent vaccine, Vaxigrip, was introduced to China in 1996, while the quadrivalent VaxigripTetra was approved domestically in February 2023. In 2018, a recall occurred involving certain batches of the trivalent Vaxigrip due to a declining trend in the efficacy of the influenza virus split vaccine. However, at that time, domestic influenza vaccine manufacturers lacked sufficient competitiveness in both production capacity and product quality. The entire influenza vaccine market was still in a very early stage, and the recall incident did not significantly impact Sanofi Pasteur’s subsequent sales in China.

And now, the landscape of China's flu vaccine market has undergone significant changes.

On the one hand, vaccine manufacturers such as Hualan Biological Bacterin Co., Ltd. and Sinovac have dominated the influenza vaccine market. At the same time, there are many domestically produced split quadrivalent vaccine products in China, which have become more cost-effective after price reductions this year. For example, the terminal vaccination cost of Hualan's quadrivalent vaccine is around 100 yuan, while that of Sanofi Pasteur is generally around 150 yuan.

On the other hand, there are options available for domestically produced vaccines beyond split-virus vaccines, such as Baik Biotechnology's nasal spray trivalent vaccine and Zhonghui Biotechnology's subunit quadrivalent vaccine. The nasal spray live attenuated vaccine can induce a broader immune response, with better immune responses observed in young children and school-age children compared to adults, potentially offering greater advantages. Subunit vaccines, belonging to the third generation of inactivated vaccines, further remove internal viral proteins and have been clinically proven to offer better safety compared to the first two generations.

"This flu season, Sanofi has exited, and it's hard for us to judge the impact on Sanofi’s sales or market access for next year." The aforementioned industry insider believes that imported vaccines may face increasing challenges in participating in China's flu vaccine market competition going forward.

It is undeniable that, before the recall, Pasteur, as an imported vaccine, was still favored by many vaccine recipients, especially as the first choice for many parents to vaccinate their children against influenza.

But the market share yielded by Sanofi may not necessarily fall to domestically produced split vaccines. On social platforms, it can be observed that many people who originally planned to get the Sanofi vaccine have started inquiring about the inoculation details of subunit flu vaccines.

Outpatient institutions have a similar perception. A person in charge of a chain medical outpatient brand said: "After the Pasteur recall, we did not find a significant increase in the vaccination of Hualan, Sinovac and other vaccines in our channels. What has significantly increased is actually the subunit quadrivalent vaccine from Zhonghui Biotechnology. Just on the 27th, one of our outpatients completed more than 100 doses of the subunit quadrivalent vaccination."

The 4-valent subunit vaccine is currently the most expensive influenza vaccine in China. Huierkangxin, developed by Zhonghui Biotechnology, is the first and only product of its kind in China, approved for marketing at the end of 2023. It is specifically classified as a 1.4-type vaccine — a multivalent vaccine containing new antigen forms, differing from previously marketed 4-valent split influenza vaccines in terms of antigen form. The supply price from Zhonghui Biotechnology is 319 yuan, with terminal vaccination costs around 350 yuan, and in some regions or channels, the cost approaches 400 yuan.

"People who choose Pasteur won't think there is a significant difference in cost between a 100-yuan flu vaccine and a more than 300-yuan flu vaccine," the person in charge said. "Based on our direct feedback from users, they care more about the effectiveness and safety of the flu vaccine. After introducing the characteristics of various flu vaccines, users often quickly and naturally decide to get the subunit quadrivalent vaccine."

"Nasal spray vaccines also have certain advantages in terms of administration, and many users opt for them; however, the current vaccination population is limited to ages 3 to 17. Therefore, I personally believe that the most notable beneficiary this year might be the subunit quadrivalent influenza vaccine."

Incremental Market: Perhaps Price Wars Should Be Avoided

After Pasteur's "accidental exit," users' reactions and choices revealed a potential issue: in the influenza vaccine market, which is mainly self-paid and growing, a low-price, high-volume strategy might not be the best approach.

Influenza vaccines belong to Category II vaccines, which require individuals to pay out-of-pocket for vaccination. Some products can be paid for using medical insurance, and certain regions may introduce policies, such as offering free vaccination slots for the elderly to encourage immunization.

Although the need for out-of-pocket payment is considered one of the reasons for the consistently low penetration rate of flu vaccines in China, users cultivated in the self-paid market are unlikely to be overly price-sensitive.

The relevant person in charge of the above-mentioned outpatient institutions said: "When many users choose influenza vaccines, they don't pay attention to who has reduced the price more, but rather whether there is a more effective product available. In other words, a considerable number of people will pursue the latest and most expensive influenza vaccine products, rather than the so-called products with the best cost performance."

Currently, the production capacity of influenza vaccines in China is not an issue. Hualan Biological Bacterin Co., Ltd. has a production capacity of 100 million doses of quadrivalent influenza vaccine. Jindik has a production capacity of 10 million doses of quadrivalent influenza vaccine and is constructing a new workshop for 30 million doses. Baike Biotech has a production capacity of 14.4 million doses of freeze-dried nasal spray influenza vaccine and is awaiting acceptance of a workshop for 10 million doses of live attenuated influenza vaccine (liquid formulation).

Rather, from the perspective of various products, there is an oversupply of influenza vaccines in China. Currently, nearly 20 companies in China are involved in the influenza vaccine market, including Hualan Biological Bacterin Co., Ltd., Jindike, Baik Biotechnology, Zhifei Biotechnology, and Kangtai Biotechnology. In its 2023 annual report, Hualan Biological also mentioned that the number of competitors for the quadrivalent influenza vaccine continues to increase, and intensified competition may lead to higher sales expenses for enterprises, with the possibility of a further decline in gross profit margins.

Tao Li纳, former chief physician of the Immunization Program at the Shanghai Municipal Center for Disease Control and Prevention, previously told the media that competition for the quadrivalent influenza virus split vaccine is extremely intense, and price cuts are to be expected. However, China's influenza vaccination rate has remained below 4% for years, and "price reductions are unlikely to significantly expand the market."

China's influenza vaccine market is an undisputed incremental market. According to estimates by Huaxing Securities, the scale of China's influenza vaccine market will increase from 6.4 billion yuan in 2020 to 19.7 billion yuan in 2025.

However, the expectation for market size ultimately depends on the increase in vaccination rates. During the 2022-2023 flu season in China, the vaccination rate was 3.84%, far lower than the average market penetration rate of about 50% in European and American developed countries. In the United States during the 2021-2022 flu season, 57.8% of children aged 6 months to 17 years received ≥1 dose of the flu vaccine, the flu vaccine coverage rate for adults aged ≥18 was 49.4%, and the flu vaccine coverage rate for elderly people aged ≥65 reached 73.9%.

The centralized price reduction of flu vaccine manufacturers in the first half of the year is widely considered by the industry to not be entirely voluntary. This wave of price cuts was not a "thunderclap" in the flu vaccine market, but rather an exacerbation of the homogenization and internal competition that has been quietly intensifying within the industry.

"The scale of China's influenza vaccine market is still limited by penetration rate, and there is a significant gap in accessibility compared to developed markets," a person engaged in vaccine marketing told VCBeat.

For example, in the United States, most chain pharmacies and many independent pharmacies offer flu vaccination services. Common chain pharmacies include CVS, Walgreens, Rite Aid, etc., and the vaccination service does not require an appointment, making it convenient for users to get vaccinated at any time. Although the flu season is usually in the autumn and winter, many pharmacies provide vaccination services all year round, without waiting for the "start of the flu vaccination campaign."

Moreover, the vast majority of commercial health insurance plans in the United States cover influenza vaccines. This is because the Affordable Care Act (ACA) requires most insurance plans to cover certain preventive services, including influenza vaccines. Additionally, most commercial insurance plans can achieve 100% coverage for influenza vaccines without copayments.

The promotion of influenza vaccines also significantly boosts vaccination rates. In May, Vaccine published a transient intervention study conducted in China involving 3,138 elderly individuals who initially were unwilling to receive the influenza vaccine. Transient intervention refers to flexible communication with those who are recommended but unwilling to vaccinate at the vaccination clinic, aiming to make them perceive the benefits of receiving the influenza vaccine and encouraging the elderly to get vaccinated. This transient intervention increased willingness to vaccinate from 18.5% to 79.8%, and the actual vaccination rate rose from 13.5% to 53.9%.

Of course, faced with the growth dilemma in the influenza vaccine field, what is most needed might still be innovation in research and development. The supplementation of Pasteur's subunit quadrivalent vaccine this time indicates the diversification of market demands, indirectly proving the promising future of China's influenza vaccine market while pointing out the current lack of innovative products.

According to CICC Research data, in the 2022 overseas influenza vaccine market, Fluzone High-Dose influenza vaccine and Flublok recombinant influenza vaccine accounted for 31% of the market share, while Flucelvax cell-culture influenza vaccine occupied 10% of the market share. Compared with traditional inactivated vaccines, high-dose influenza vaccines typically contain four times the antigen of standard-dose vaccines, offering better protection; recombinant vaccines provide enhanced protection through more precise antigen design and higher purity, with safety equivalent to or better than traditional vaccines, representing a significant direction for vaccine innovation and upgrade; cell-culture vaccines have advantages in production flexibility and potential virus matching. However, there are no such vaccine products currently available in China.

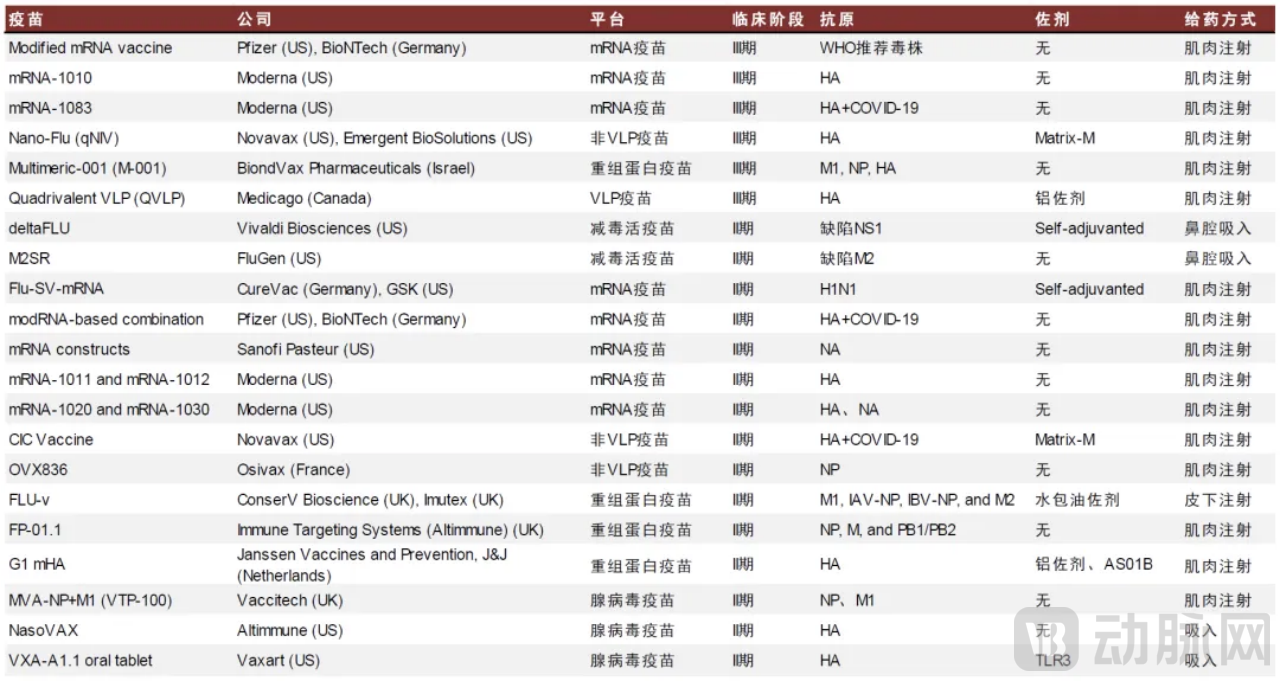

In fact, the influenza vaccine is a highly complex product. Overseas, various innovative influenza vaccines are reshaping the influenza vaccine market and continuously expanding its scale. Vaccine companies such as Sanofi, CSL, and Moderna have shifted their focus in influenza vaccine development to non-egg-based manufacturing technologies like recombinant protein and mRNA. In the Chinese market, inactivated influenza vaccines still dominate, with a few companies developing cell-cultured influenza vaccines. However, most products in clinical phases 2 and 3 are crowded in the inactivated split-virus vaccine category.

Global Universal Influenza Vaccine Progress (Phase II/III, as of the end of 2023), Source: Gates Universal Influenza Vaccine Foundation, CICC Research Department

"The way forward for China's flu vaccines is to develop platforms with updated routes and better antibody effects, rather than fiercely competing in the split flu vaccine market, and there is no need to pursue a low-price strategy."

References

CICC | Vaccine Industry Series Report: Innovative Flu Vaccines Reshape Overseas Competitive Landscape: https://mp.weixin.qq.com/s/Z-gyi4oOlrtgFBLXbbJfIg

Influenza Vaccine Coverage Rate: Where Exactly Lies the Problem? : https://mp.weixin.qq.com/s/09ikGUtEZGxlt_yuXYg7Hw