On September 2, HeartCare (6609.HK), a pioneer in China's neurointerventional medical device industry listed in Hong Kong, held its 2024 interim results briefing to provide a detailed overview of the company’s performance for the first half of the year.

The following are the key points of HeartCare's mid-term performance in 2024:

Revenue grows steadily, break-even point approaching

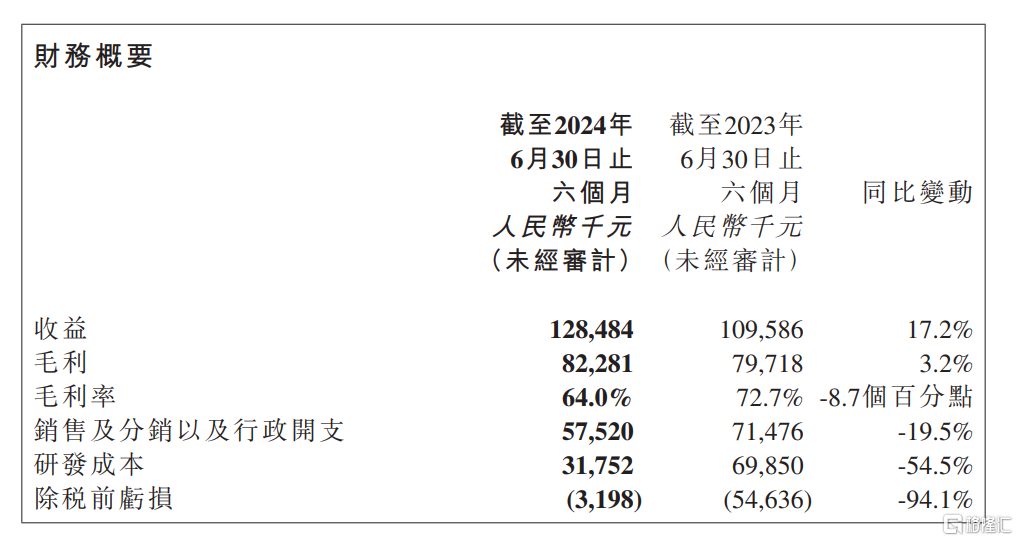

From the core financial indicators, in the first half of the year, the company achieved revenue of 128 million yuan, a year-on-year increase of 17.24%, demonstrating a steady growth trend. This reflects strong market adaptability and business resilience in the face of complex and volatile financial market environments as well as multiple challenges such as centralized procurement policies, laying a solid foundation for the company's continued development within the industry.

In terms of profits, the company's pre-tax loss for the first half of the year further narrowed to 3.2 million yuan, a year-on-year decrease of 94.1%. Significant signs of financial improvement indicate that the company's profitability turning point is approaching, paving the way for a new chapter of profitability. This will undoubtedly further boost the confidence of investors and the market.

The growth momentum of the company's revenue in the first half of the year mainly came from devices for acute ischemic stroke (AIS) thrombectomy, intracranial artery stenosis treatment, and innovative access devices. At the same time, thanks to the registration approval of multiple products by local regulatory authorities, the company's overseas revenue has also seen an effective increase, marking a solid step forward in the company’s global expansion.

In its core business strategy, HeartCare is undergoing a significant transformation from homogeneous channel products to user solutions centered on therapeutic products. This strategic adjustment not only strongly supports the growth of the company’s product sales but also demonstrates its strategic vision of deep cultivation in the neurointervention field and pursuit of differentiated competition.

Since the end of last year, in order to better adapt to the rapidly changing market environment, the company has continuously promoted the transformation and upgrading of its neurointerventional business towards differentiated therapeutic devices. Specifically, neurointerventional therapeutic devices such as stent retrievers, aspiration catheters, dilation balloons, embolic protection systems, and coils contributed 35.6% of sales revenue, reaching 45.8 million yuan. Meanwhile, the sales of neurointerventional access devices and other products achieved a year-on-year growth of 42.1%, with revenue reaching 82.7 million yuan, further solidifying the company's leading position in the industry.

Improved operational efficiency and enriched R&D pipeline create new opportunities

In terms of cost reduction and efficiency improvement, HeartCare has also achieved remarkable results. Despite the pricing adjustment pressure brought by the centralized procurement policy, the company has maintained a good momentum of cost control, efficiency enhancement, and efficient operations that started in the second half of last year.

Data shows that the sales and administrative expenses ratio in the first half of the year decreased by 20.4 percentage points year-on-year, optimizing to 44.8%. In addition, R&D expenses were also effectively controlled, overall reflecting significant progress in the company's R&D efficiency and management optimization, driving the overall operational efficiency of the company.

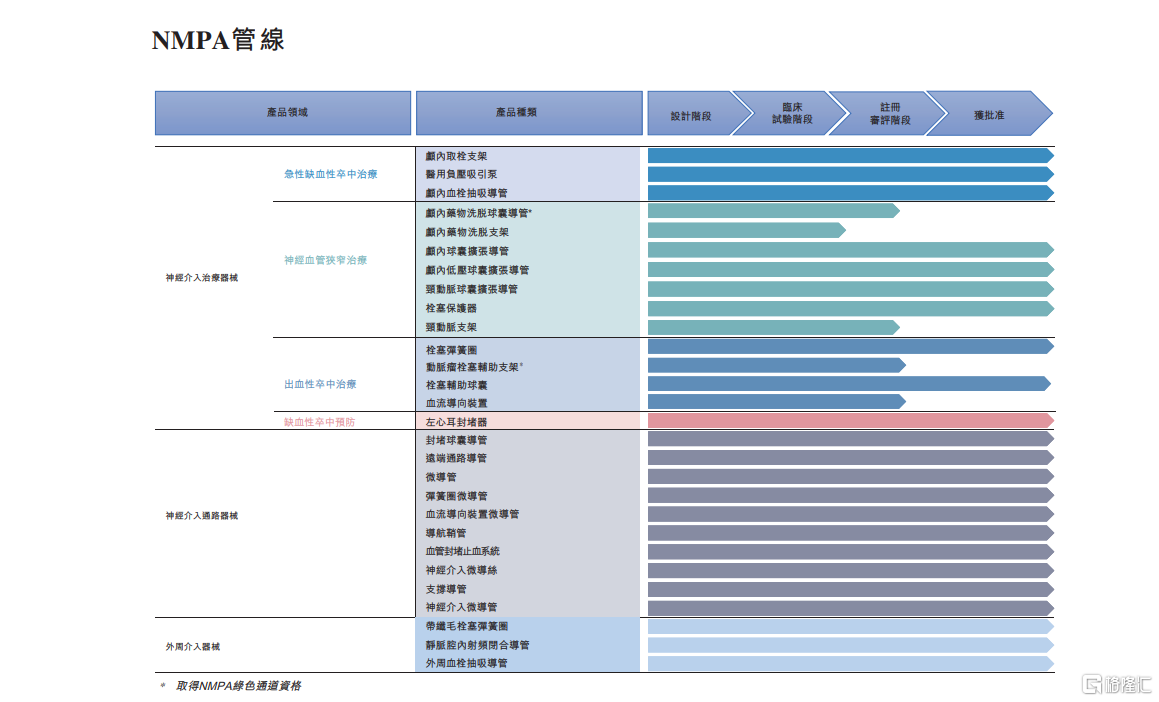

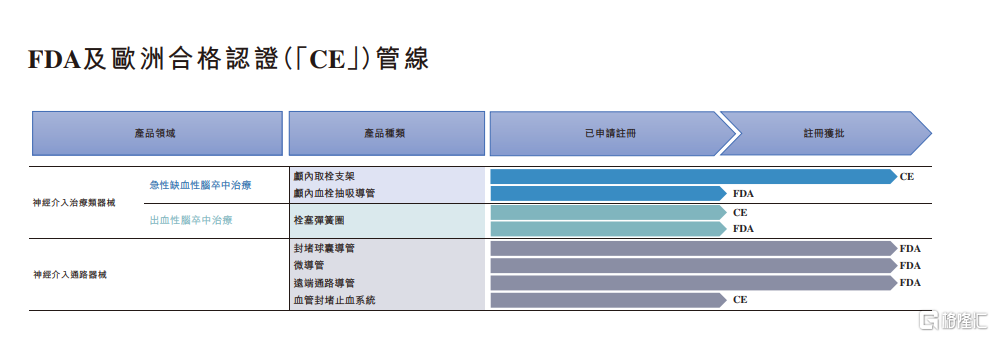

The company has a rich R&D pipeline, which helps to further expand the market growth space in the future. As of the 2024 mid-year earnings announcement date, the company had 29 medical device products approved by the NMPA, three device products approved by the FDA, and one product with a CE mark.

Including approved products and a wide-ranging pipeline in late-stage development, covering treatments for acute ischemic stroke and neurovascular stenosis, hemorrhagic stroke treatment, ischemic stroke prevention, interventional access, and peripheral intervention devices:

In the field of ischemic stroke treatment, the company's core product is the Captor® thrombectomy stent, which is the first domestically produced multi-point imaging thrombectomy stent approved by NMPA in China. In addition, the company also owns an intracranial thrombus aspiration catheter and aspiration pump, both of which have received NMPA approval. This product portfolio can be used for the emergency treatment of different subtypes of acute ischemic stroke.

In the interim results announcement for 2024, the company disclosed that in the next 18 months, it expects at least five major neurointerventional treatment devices to be launched. These include an intracranial drug-eluting balloon catheter for stenosis treatment (with NMPA innovative device designation), a self-expanding drug-eluting stent, and a carotid artery stent, as well as an aneurysm embolization assist stent (with NMPA innovative device designation) and a flow diverter for hemorrhagic stroke treatment.

At the same time, the company is enhancing the competitiveness of its key thrombectomy products (aspiration catheters and stent retrievers) and one-stop medical device solutions to meet the growing demand for stroke treatment in China amidst an aging population, addressing the needs for emergency surgery in different subtypes of cerebral infarction.

In the overseas market, the company's thrombectomy stent, occlusion balloon catheter, remote access catheter, and microcatheter have obtained CE or FDA certification, and have completed registration and initiated commercialization in countries or regions such as Thailand. Meanwhile, the company is also conducting product registration in more than 10 other countries or regions, expanding sales channels, and laying the foundation for achieving long-term goals in overseas sales.

Looking ahead, the company is committed to becoming a leader in China's neurointerventional medical device market and securing a competitive edge in the domestic innovative medical device market. To achieve this goal, the company has formulated three core strategies: First, enhance brand awareness, expand the commercial sales of existing products, and accelerate the market entry of products under development; second, strengthen manufacturing capabilities to ensure highly reliable product supply; third, focus on emerging therapeutic areas with high growth potential, drive the development of innovative medical devices, and aim to build a second competitive commercial product portfolio business unit beyond the neurointervention business.

The following is a partial transcript of the Q&A session between investors and management during this earnings meeting:

Q1: What is the company's view on the recent pricing issues of innovative medical device products? What are the subsequent impacts on the market and the company’s response strategies?

A1: Regarding the pricing of innovative devices, the cycle for innovative devices is now shorter than before, unlike in the past when a product enjoyed a long period of exclusivity after its launch. As for our strategy, we still firmly believe that innovative products are crucial. The country has many supportive policies that allow for rapid scaling. The price of innovative products can maintain an advantage for a certain period. In the future, we will continue to leverage innovative products, enhance academic and hospital promotions, and lay a solid foundation for future volume and centralized procurement. At the same time, we also need to continuously optimize product performance and iterate on innovation.

Q2: What is the company's outlook for future revenue and profits?

A2: Starting from 2024, the next 2-3 years will be a test for all China-produced medical device companies engaged in neurointerventional business. The competition for access products is fierce due to homogeneity, and they will become the basic source of income in the future. Companies need to manage costs effectively and enrich their therapeutic product pipelines. Over the next three years, the revenue structure will gradually shift towards therapeutic products, with expected gross margins and pre-tax profit rates both set to increase progressively.

Q3: What are the research and development progress and existing data on intracranial stents for treating stenosis and drug-eluting stents?

A3: The intracranial drug-coated stent has just completed patient enrollment in the first half of this year and is currently in the follow-up stage, with the final data yet to be released. The intracranial thrombectomy stent was submitted for registration last year, showing good results, and specific approval is currently under discussion with the NMPA.

Q4: What is the company's strategic thinking for the subsequent development of the hemorrhagic product line, and what are the growth prospects?

A4: The company places great importance on the hemorrhage business and has established a dedicated sales team to take charge. In the next 1-3 years, with the launch of blockbuster products such as embolic assist stents and coated flow-diverter stents, the hemorrhage business line will provide strong growth momentum, with a growth rate higher than the company's overall growth rate.

Q5: What is the current status and future plan of the company's overseas market?

A5: Overseas market revenue in the first half of the year exceeded 3 million, with sales or registration already established in multiple countries and regions. The future focus will be on developing an agent network and local registration, with expectations to achieve long-term sales in over 10 countries or regions by next year, and the growth rate will continue to accelerate.

Q6: How does the company balance the promotion strategy and volume expansion approach for high-end treatment products under the DRG context?

A6: Therapeutic products are the company's future focus, with an emphasis on specialized promotion. By integrating product differentiation innovation and clinical value, customer awareness will be enhanced. Collaborate with key clients for innovation and deepen cooperation.

Q7: What are the company's cost reduction and efficiency improvement plans for the second half of the year? What is the possibility of turning the full-year profit positive and reducing the pre-tax profit loss?

A7: The policy of cost reduction and efficiency enhancement continues to advance, including personnel cost control and expense management. The company aims to stabilize the scale of expenses while maintaining revenue growth and gradually improve the team's level. It is expected to achieve break-even this year. The goal for the next few years is to control the expense ratio within 45-50% and achieve a pre-tax profit margin of around 20%.

Q8: Does the company have other potential blockbuster products for overseas markets in the future?

A8: The company has multiple access and treatment products, including vascular occluders, distal access catheters, thrombectomy stents, and coils, all actively undergoing international registration. Once approved, these products will quickly gain traction overseas, supporting the growth of international business.