Over a Dozen Medical Device Companies Report Over 100% Profit Surge Amid Industry Recovery

APT Medical

Cardiac Electrophysiology and Interventional Medical Device R&D Manufacturer

MicroPort EP

R&D Producer of Cardiac Electrophysiology Interventional Medical Devices

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

Jinjiang Electronic

Developer of electrophysiology products

Nuomao

Cardiovascular Innovative Medical Device R&D Manufacturer

Boston Scientific

Medical Device Manufacturer

AccuPulse

Developer of products in the field of cardiac electrophysiology

Endovastec

Developer and Manufacturer of Aortic and Peripheral Vascular Interventional Medical Devices

Lepu Medical

Developer and Manufacturer of Cardiac Interventional Medical Devices and Pharmaceuticals

SINOMED

High-end interventional medical device R&D, production, and sales provider

Snibe

In Vitro Diagnostics (IVD) Product Developer, Manufacturer, and Supplier

Mindray

Medical Device R&D Manufacturer

Since the beginning of the year, the medical device industry has not been doing well.

According to data from SDIC Securities, in the first half of 2024, the scale of bidding and tendering in the medical equipment industry was approximately 55 billion yuan, a year-on-year decrease of about 35%. Among this, the scale of bidding and tendering for medical imaging decreased by around 45% year-on-year, and the scale for the life information field fell by 50% to 60% year-on-year. Particularly, due to the interest-subsidized loan policy in 2023, which led to the early release of demand, hospitals became more cautious in equipment procurement during the first half of the year, resulting in a reduction in the number of tenders.

Medical devices are also a microcosm of the entire medical device industry.

According to the data from the semi-annual reports, among 126 medical device companies, approximately half of the listed medical device companies experienced a decline in performance. The overall revenue increased by only 0.34% compared to the first half of last year. Notably, the quarter-on-quarter data is improving. On a quarterly basis, the Q2 revenue of 126 listed companies increased by 7.73% quarter-on-quarter, and the net profit attributable to shareholders increased by 16.04% quarter-on-quarter.

According to IQVIA statistics, in the first half of this year, excluding obstetric surgery factors, the total number of surgeries in China still maintained a high growth rate of 8%. The volume of surgeries related to sports medicine increased by over 20%, and surgeries in departments such as orthopedics, thyroid, and breast nodules also saw a year-on-year increase of nearly 10%. This indicates that demand has not weakened.

On the other hand, even in such a difficult environment, more than 10 medical device companies reported earnings growth of over 100%, and 45 companies achieved a net profit attributable to shareholders exceeding 100 million yuan. This indicates that with the improvement in procurement and tendering within the medical device industry, the recovery of the device sector is not far off.

Despite the slowdown in performance due to the contraction in procurement scale affecting medical devices, the development of the consumables business remains relatively stable. As long as there is sufficient clinical demand, it is minimally affected by external factors. From the mid-year reports of enterprises, some niche sectors are still experiencing rapid growth.

Vascular Intervention

According to IQVIA statistics, in the first half of 2024, the vascular interventional device market increased by more than 10% year-on-year. The volume of surgeries in its sub-sectors, such as electrophysiology, coronary intervention, and neurointervention, maintained steady growth. At the same time, the scope of surgeries continues to expand, with an increasing number of qualified doctors and hospitals. Domestic brands are covering a larger market during this penetration process.

Taking APT Medical as an example, this enterprise, which focuses on the field of cardiac electrophysiology, has been the focus of the market since the beginning of the year.

At that time, the medical device giant Mindray successfully gained controlling interest at a premium of 25% for a staggering cost of 6.652 billion yuan, sparking heated market discussions: Is premium acquisition a value investment or a financial gamble? With the unveiling of the half-year report, the answer has become clear.

In the first half of the year, APT Medical achieved operating revenue of 1.001 billion yuan, representing a year-on-year increase of 27.03%, demonstrating strong growth momentum. The net profit attributable to shareholders of the listed company reached 343 million yuan, a year-on-year increase of 33.09%. The significant improvement in performance further validates its growth potential and market competitiveness.

Similarly, another Chinese electrophysiology company, MicroPort EP, achieved revenue of 198 million yuan, a year-on-year increase of 39.57%; net profit attributable to shareholders reached 17.0127 million yuan, with an astonishing year-on-year increase of 689.30%.

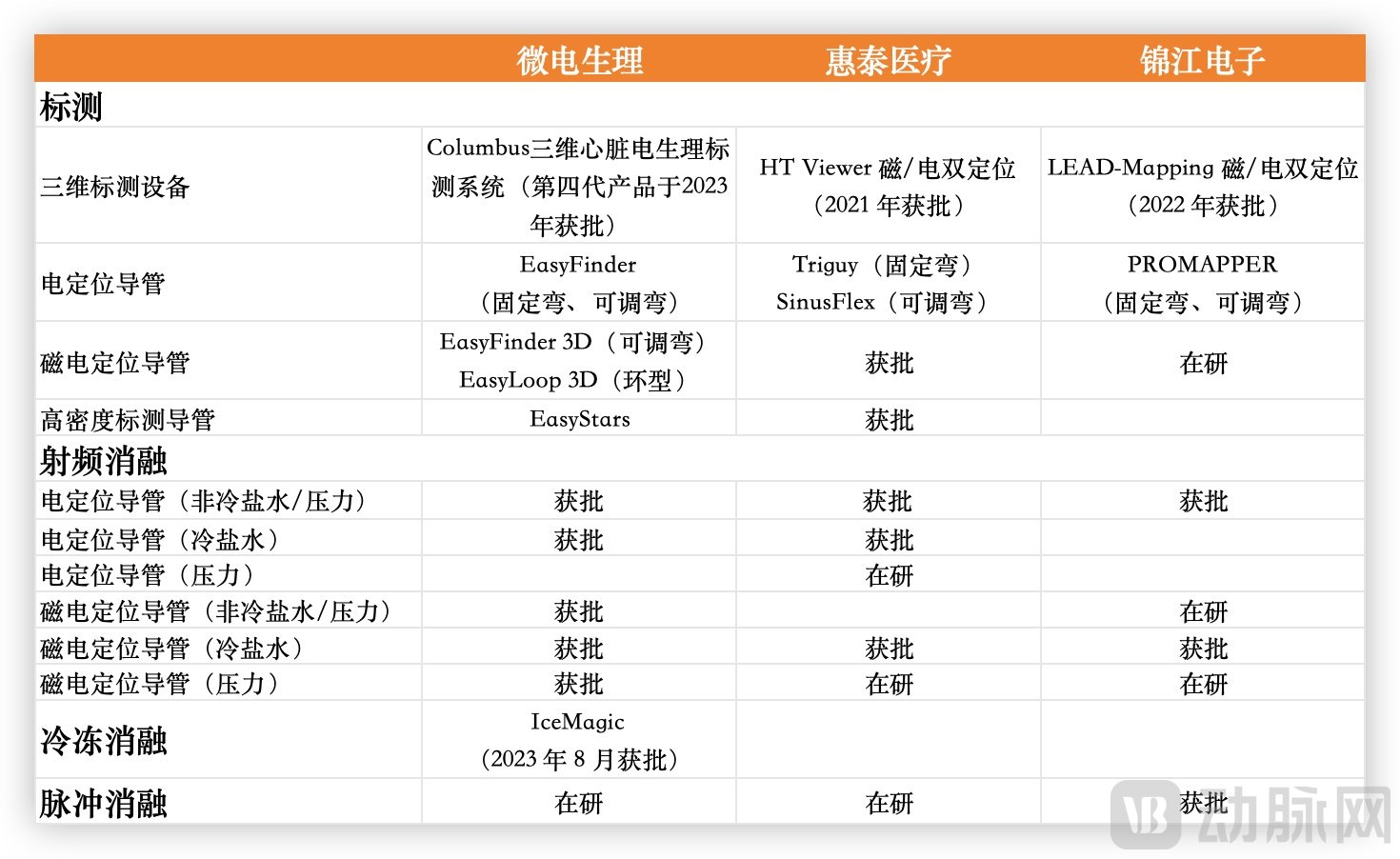

It can be seen that, after years of layout, the market scale of electrophysiology enterprises in China has been growing steadily, with representative companies such as APT Medical, MicroPort EP, and Jinjiang Electronic challenging multinational brands.

In the first half of this year, APT Medical's domestic electrophysiology products were newly implanted in more than 150 hospitals, covering over 1,250 hospitals. In the more technically challenging three-dimensional electrophysiology field, APT Medical has also been making further efforts. In the first half of this year, it completed approximately 7,500 three-dimensional electrophysiology surgeries in more than 800 hospitals, with the number of surgeries increasing by over 100% compared to the same period in 2023. In the non-atrial fibrillation treatment field, APT Medical's three-dimensional cold saline ablation catheter completed about 7,500 surgeries in the first half of 2024. The overall electrophysiology business segment grew by 63% year-on-year.

MicroPort EP has an early layout in the 3D electrophysiology field. Its first-generation Columbus 3D Cardiac Electrophysiology Mapping System entered the Innovative Medical Device Special Approval Process in 2015, and the third-generation product was approved for marketing by NMPA in 2020. To date, MicroPort EP's products have been cumulatively applied in over 70,000 3D cardiac electrophysiology surgeries both in China and internationally. In the first half of this year, the fourth-generation Columbus 3D Cardiac Electrophysiology Mapping System received EU CE certification.

Product Layout of Some China-produced Electrophysiology Manufacturers, Data from Official Websites and Financial Reports

From a product perspective, in the field of 3D mapping equipment, Johnson & Johnson is the absolute leader in the Chinese market and only adapts to its own consumables. Currently, APT Medical, MicroPort EP, and Jinjiang Electronic have all launched their self-developed 3D electrophysiology mapping equipment. Based on this foundation, pulse ablation technology, which needs to be used in conjunction with 3D electrophysiology mapping equipment and is considered to change the landscape of the electrophysiology market, is becoming the next focal point of competition.

In China, Jinjiang Electronic, Nuomao, and Boston Scientific have already been approved. APT Medical, AccuPulse, and others are also striving to catch up. According to the companies' semi-annual reports, APT Medical's research projects, including pulse ablation catheters, pulse ablation instruments, high-density mapping catheters, pressure radiofrequency instruments, and pressure-sensing ablation catheters, have entered the registration review stage. MicroPort EP's renal artery ablation system has officially been approved to enter the National Medical Products Administration’s special review process for innovative medical devices.

Not only in electrophysiology, but the performance of interventional stents in the first half of the year was also commendable.

The increase in demand for coronary implant products has driven the rise in PCI procedures, providing continuous growth for the long-term volume-for-price and scale recovery of the complete set of coronary implant and access products after centralized procurement.

According to data from the National Health Commission, the number of PCI treatment cases in China has been climbing at an annual growth rate of nearly 15% over the past several years. The number of surgeries reached 1.63 million in 2023, a year-on-year increase of 26.44%. With the continuous rise in the number of surgeries, even within the established competitive landscape of a highly mature market, the actual usage of enterprise stents will far exceed the中标level. The process of domestic substitution for high-consumption stent products, pioneered by coronary stents, is still evolving.

In the first half of this year, Endovastec achieved operating revenue of approximately 787 million yuan, representing a year-on-year increase of 26.63%; net profit attributable to shareholders of the listed company was about 404 million yuan, marking a year-on-year increase of 44.36%. The company stated that R&D projects such as the L-REBOA Aortic Occlusion Balloon Catheter, ReeAmber Peripheral Balloon Dilation Catheter, Vewatch Inferior Vena Cava Filter, Vepack Filter Retrieval Device, and Vflower Venous Stent have all been successfully approved as planned. In particular, the Castor Branched Aortic Stent Graft and Delivery System has seen rapid growth in both the number of hospitals adopting the product and terminal implant volumes.

Lepu Medical's cardiovascular implant and interventional business segment achieved a revenue of 1.151 billion yuan in the first half of 2024, representing a year-on-year increase of 16.92%. Among this, the coronary implant and interventional business generated a revenue of 851 million yuan, up 10.21% year-on-year, while the structural heart disease business achieved a revenue of 249 million yuan, marking a significant year-on-year growth of 53.63%. During the earnings briefing, Lepu Medical stated that the growth in coronary implant and interventional revenue was primarily driven by increased sales volumes of cutting balloons and drug-coated balloons under the centralized procurement policy.

Another company, SINOMED, achieved a revenue of 214 million yuan in the first half of 2024, representing a year-on-year increase of 32.5%, with a 125.88% growth in net profit attributable to shareholders. According to the semi-annual report, sales of coronary intervention products continued to rise during the reporting period, with the sales volume of coronary stents surpassing the procurement volume for 2024, showing a significant increase compared to the same period last year. Additionally, in the December 2023 procurement of 28 categories of medical consumables in the Beijing-Tianjin-Hebei region, the company also secured bids for its coronary artery scoring balloon dilation catheters and guiding catheters, which will gradually begin to be implemented across various provinces and cities.

In Vitro Diagnostics

IVD Companies First to Shake Off the Impact of High Pandemic Baseline Begin to "Shine" in Niche Markets.

As routine diagnostic services recover, some companies in the IVD industry have begun to see steady growth in performance. For instance, the performances of SaintDx Biotech, Pulnovo Medical, Snibe, and YHLO in the first half of the year increased by 70.93%, 27.78%, 20.42%, and 22.25% respectively. The top five companies by revenue are Mindray, Dian Diagnostics, Runda Medical, KingMed Diagnostics, and Snibe.

From the breakdown of performance, chemiluminescence has become an important engine driving performance growth, with companies like Mindray, Snibe, and YHLO relying on chemiluminescence to achieve rapid performance growth. In addition, respiratory testing has also driven the growth of related companies, such as the outstanding performance of Sansure and Innovita.

Specifically, Snibe increased the number of tertiary hospitals it served by 101 in H1 2024 compared to the end of 2023, continuously promoting the domestic expansion of chemiluminescence. AccuPulse's self-produced chemiluminescence business revenue reached 720 million yuan in H1 2024, a year-on-year increase of 48.46%. It achieved the installation of 1,170 new chemiluminescence instruments, bringing the cumulative total to 9,430 as of the reporting period, with a cumulative total of 129 assembly lines installed. Nearly 40% of these assembly lines were installed in tertiary hospitals.

In China, the in vitro diagnostics segment of Mindray, the domestic medical device leader, also saw a year-on-year revenue increase of 28.16%. Among this, chemiluminescence, as a traditional advantage business, grew by over 30%. Notably, with the gradual implementation of the Anhui chemiluminescence reagent alliance procurement, Mindray estimates that its chemiluminescence business's market share in China could surpass another imported brand, ranking third, only behind Roche and Abbott.

Other companies such as Chemclin Diagnostics, Pumen Technology, Wondfo Biotech, Getein Biotech, and Hotgen Biotech have also achieved performance growth by relying on the rise of chemiluminescence businesses. Overall, chemiluminescence has become the main driver for core performance growth among IVD enterprises and an important factor in overseas expansion. Additionally, this year's industry exhibitions indicate that automated流水lines have become mainstream, which will further compress the market space for standalone chemiluminescence machines in the future. Competition will shift from individual machines to流水line competition and eventually to competition in smart laboratories.

Performance of the chemiluminescence sector of some IVD companies, data sourced from financial reports

Besides, some companies have achieved rapid growth in niche markets by virtue of comprehensive product layouts and overall solutions. For instance, Mindray's minimally invasive surgery business grew by over 90% year-on-year in the first half of 2024, particularly its core product in minimally invasive surgery, the rigid endoscopy system, which doubled its performance.

According to IQVIA data, the surgical field market grew by 4.6% year-on-year in the first half of 2024. With the continuous increase in the volume of surgical procedures and minimally invasive surgeries, the usage of related products is also expected to rise. For the entire consumables sector, growth is expected to continue upward for some time in the future.

Of course, in addition to the continuous refinement of products, we also see that many companies have made great efforts in exploring emerging markets, bringing new increments to their revenue.

Exporting overseas has become an important measure for medical device companies to stabilize their performance.

According to customs statistics, in the first half of 2024, China's total exports of medical devices amounted to 22.976 billion US dollars, increasing by 3.1% year-on-year. Overall, despite a nearly 10% decline in the export value of low-value consumables such as medical dressings, categories including disposable consumables, hospital diagnostics and treatment equipment, health rehabilitation products, dental equipment and materials all achieved positive growth.

In terms of the export market, the United States remains China's largest export market for medical devices, accounting for 23.7% of export value, with a slight year-on-year increase of 4.5%. In the first half of the year, China's medical device exports to the 27 EU countries amounted to $4.26 billion, a year-on-year increase of 6.6%. Except for a year-on-year decline in exports to Greece, exports to the other nine major EU markets including Germany, the Netherlands, France, and Italy all showed varying degrees of growth.

In addition to traditional European and American markets, emerging markets represented by countries along the "Belt and Road" have also shown good performance. In the first half of the year, the cumulative export volume to 152 countries along the route reached 8.82 billion U.S. dollars, a year-on-year increase of 4.3%. By August, the export volume reached 886 million U.S. dollars, accounting for 24.64% of the total export volume, with a month-on-month increase of 2.8%. Among them, Russia, South Korea, Vietnam, Singapore, and Malaysia ranked high in exports. Additionally, significant export growth was seen in markets including Venezuela, Iraq, Kyrgyzstan, and the United Arab Emirates.

The亮眼 performance of the aforementioned companies in the first half of the year was also inseparable from the contribution of their overseas businesses.

Taking the cardiovascular business as an example, APT Medical's international business grew by 19.73% overall in 2024H1. Among this, the performance in the CIS region was particularly outstanding, with a year-on-year increase of 124%; the European region increased by 51% year-on-year; and other regions such as the Asia-Pacific, Latin America, Middle East, and North Africa also showed significant growth. MicroPort EP has intensified its overseas market expansion efforts thanks to a comprehensive product layout, with the number of three-dimensional surgeries achieving rapid growth, already covering 36 countries and regions worldwide. Additionally, the total trade volume of IVD instruments has seen a large increase. Taking August data as an example, the export value was 253 million yuan, showing a month-on-month increase of 42.7%.

For some sub-sectors with slower profit growth in the first half of the year, such as orthopedics, overseas markets have become an important driver for maintaining performance.

Chunli Medical, which focuses on artificial joints as its core product, reported that export revenue accounted for 40.7% of its total revenue in the first half of the year, becoming an important pillar for the company's continuous development. Aikon Medical successfully entered countries such as Malaysia, Japan, and Spain in the first half of the year. Relying on a personalized customization service strategy, it quickly opened up overseas markets. Its overseas revenue increased by 8.7% year-on-year in the first half of the year, accounting for 18.8%.

Overseas Revenue of Some Orthopedic Companies, Data from Corporate Financial Reports

In addition, WEGO Orthopaedics is actively promoting the construction of key channels in the Southeast Asian market. It increases brand exposure and improves market coverage through meticulous management of channels and customers in Indonesia and Thailand. Product registration has been initiated in 11 countries including Brazil, Saudi Arabia, Dubai, and Thailand. Dabo Medical has exported its products to more than 60 countries and regions such as Australia, Ukraine, and Chile. Meanwhile, Sanyou Medical's ultrasonic bone scalpel has expanded its market to regions such as the Netherlands, Spain, and Australia.

The sluggishness in medical device bidding and tendering has dragged down the growth of the equipment track, and a recovery will require a boost from the equipment sector.

According to data from Guotou Securities, the medical imaging industry (excluding ultrasound) saw a bidding scale decline of 50%-60% from January to March this year, with the decline narrowing to 25%-35% from April to July. In the life information support sector (including monitoring, respiratory, anesthesia, defibrillation, etc.), the bidding scale fell by about 70% from January to March, dropped by approximately 40% in April, and narrowed to a decline of 20%-30% from May to July.

The scale of medical ultrasound tenders and bids declined by 40%-50% from January to March this year, decreased by about 10%-20% from April to June, and grew by 13% in July compared to June. The scale of endoscope tenders and bids fell by 40%-50% from January to March this year, narrowed to a decline of 20%-30% from April to June, with an increase of about 40% in June compared to May, and grew by approximately 5% in July compared to June. It can be seen that the tendering activity in these two major sectors has begun to recover.

According to statistics from Ping An Securities, some provinces in China have already released pre-approval announcements or approvals for medical equipment upgrade projects. The disclosed amount has exceeded 20 billion yuan, and it is expected that there may be an increase of hundreds of billions of yuan in equipment upgrades nationwide. Mindray also revealed at an investor meeting that although the bidding and procurement activities in the first half of this year were continuously delayed, which slowed the growth of domestic segments across multiple business lines, the total volume of pent-up procurement demand was not affected, and the delayed procurement projects will still be fully released in the future.

On the other hand, data from the primary market also shows some differences. As of August this year, the IVD field saw 9 more financing events compared to last year, the medical imaging field had 4 more, and the surgical treatment equipment field had 20 more. All sub-tracks’ financing events leaned towards Series A or earlier rounds, with IVD and medical imaging having the highest numbers at 28 and 25 times respectively. Notably, surgical robots still garnered significant attention this year, with 9 financing events occurring. Additionally, two subsidiaries under Blue Sail Medical collectively experienced 4 investment and financing events, securing over 2 billion RMB in total.

The coldest season has passed, and the medical device industry is not as fragile as the market feared. Consumables continue to grow, and medical equipment has seen marginal improvement. The industry's recovery is only awaiting the implementation of a medical equipment renewal policy.