Major Pharma Companies Implement Strategic Pipeline Cuts to Optimize R&D Resources: Johnson & Johnson, Pfizer, Shanghai Pharmaceuticals, and Huadong Medicine Lead Industry-Wide Restructuring

Johnson & Johnson

Medical Device R&D and Manufacturer

SPH

Pharmaceutical R&D and Manufacturing

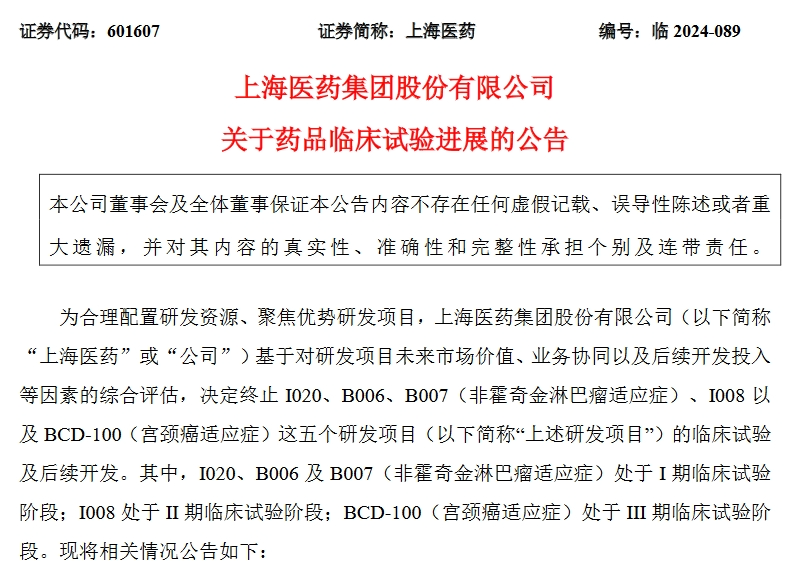

Recently, SPH announced the termination of clinical trials and subsequent development for five R&D projects at one go, marking the third batch of pipeline cuts this year for the state-owned pharmaceutical company.A total of 12 projects have been terminated, with accumulated sunk costs nearing 700 million yuan.

Although pipeline adjustments as intensive and extensive as those of SPH are rare, in the innovative drug R&D sector — where the cost is typically "ten years, ten billion dollars" with a success rate of only about 10% — blockbuster drugs remain a rarity. For most innovative pharmaceutical companies, apart from selecting competitive R&D pipelines, it is also crucial to adjust product pipelines in a timely manner based on their development strategies and market changes, balancing resource allocation or cutting losses promptly.

As Johnson & Johnson, a multinational pharmaceutical giant that released its Q3 2024 earnings report on October 15, reported that the sales of some core products increased by more than 80% year-on-year, it also quietly disclosed in its latest R&D pipeline update within the same quarter that...The development of three early- and mid-stage candidate drugs has been discontinued.

Johnson & Johnson's partner, Legend Biotech, a leading innovator in China's pharmaceutical industry, successfully developed Caryvkti (Ciltacabtagene Autoleucel), a blockbuster drug. However, in 2022, the company also experienced the termination of a significant clinical trial for one of its key research pipelines.

Since 2024, both foreign and domestic pharmaceutical companies, such asPfizer, AstraZeneca, BeiGene, Huadong Medicine, etc.No fewer than 10 companies have terminated ongoing projects due to internal or external reasons, resulting in financial losses ranging from tens of millions to billions.

The hardest hit was undoubtedly Pfizer, which had to terminate all clinical trials and globally recall the related drug after a product pipeline, acquired two years ago for $5.4 billion, showed significant risks in clinical trials.

700 Million Cost Reduced to Zero

If the R&D cycle for an innovative drug is 10 years, the clinical trial phase will likely take around 6 to 7 years, which is often the most costly stage with a relatively high failure rate.

SPH Latest Announcement of Termination of Five ProjectsHave already entered the clinical trial stage, with a total R&D investment of approximately 257 million yuan., three of which have completed Phase I clinical trials, one has completed Phase II clinical trials, and one is even in the final stage of Phase III clinical trials.

The project pipeline with the least cumulative R&D investment is I020, a selective inhibitor intended for the treatment of non-small cell lung cancer (NSCLC) and other malignant tumors. It is currently at the end of Phase I clinical trials. More than five years have passed since it was approved for clinical trials in May 2018, with a total investment of 41.4507 million yuan accumulated to date.

The project with the highest investment is I008, which has already cost 62.1875 million yuan. This pipeline is also one of the core R&D projects first introduced after SPH began emphasizing R&D and technological innovation as a development focus in 2009. It is a patented compound derived from the active ingredient triptolide found in the traditional Chinese medicine Lei Gong Teng, through purification, processing, and chemical structural modification, intended for the treatment of rheumatoid arthritis.

Now, the pipeline that has taken 15 years and tens of millions in funding to advance to the end of Phase II clinical trials has come to an abrupt halt, which is truly lamentable. However, SPH has also stated that the clinical trial and subsequent development for the HIV chronic abnormal immune activation indication of the I008-A project are still proceeding as normal.

In May and June prior to this, SPH also successively terminated the clinical trials and subsequent development of two batches comprising seven R&D projects.Since 2024, SPH has terminated a total of 12 project pipelines, with cumulative R&D investment amounting to approximately 6.94 billion yuan, accounting for 23.59% of the company's 29.42 billion yuan attributable net profit in the first half of 2024.

(SPH 2024 R&D Pipeline Termination Status, Source: Corporate Announcement)

For such intensive and large-scale pipeline adjustments, SPH's rationale is the rational allocation of R&D resources, focusing on advantageous R&D projects. This decision is also based on a comprehensive evaluation of factors such as the future market value of R&D projects, business synergy, and subsequent development investments.

New Health Insights has learned that over the past nearly 10 years, SPH had a concentrated investment akin to the "Great Leap Forward" in its innovative drug R&D pipeline. This led to a steady increase in R&D investment, but the R&D outcomes have been few and far between.

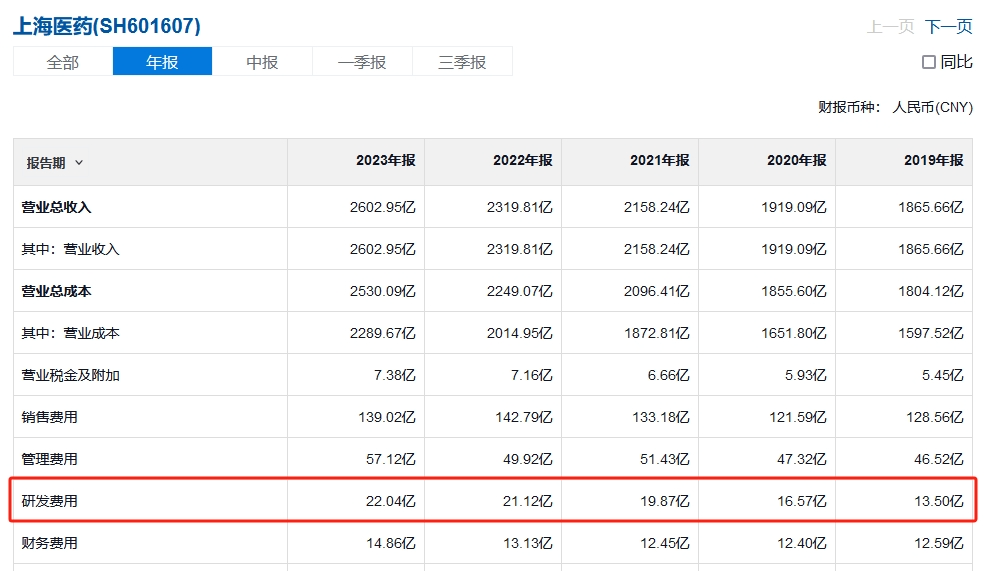

In 2017, SPH's R&D expenditure was still in the single digits at 7.90 billion yuan, breaking 10 billion yuan in 2018, exceeding 20 billion yuan in 2022, and reaching 22.04 billion yuan in 2023.R&D investment exceeds 11.1 billion yuan over the past seven years。

(Recent R&D expenses of SPH, source: Xueqiu)

As of June 30, 2024, SPH has already reached 50 innovative drug pipelines that have been accepted for clinical applications and entered subsequent clinical research stages.(Three of which are in Phase II clinical trials in the United States), with R&D expenses reaching 1.105 billion yuan in the first half of the year, representing a year-on-year increase of 7.67%.

But behind the heavy investment, there is a serious imbalance in R&D results. Statistics from some self-media have found that,SPH has failed to have any new innovative drugs approved for marketing from 2006 until now., only three innovative drugs have been launched in China so far: Oncorine (Recombinant Human Adenovirus Type 5), Kallicon (Urokinase), and Bifico (Triple Live Bifidobacterium), which were launched in 2005, 2005, and 1995, respectively.

Whether it's due to inefficiency in R&D or overexpansion leading to resource waste, as a leading pharmaceutical commercial enterprise, SPH’s experience of “large-scale investments and withdrawals” in the transition to innovative drugs serves as a reminder to many peers that the innovative drug business not only tests a company’s pipeline management capabilities but also requires timely insights into market changes and industry trends. Especially under the capital winter, timely loss-cutting may not be a bad thing.

In the past week, CSPC and Baiyu Pharma have successively announced the authorization of drug-related rights to MNC giants. The former granted AstraZeneca the exclusive rights to a preclinical small-molecule lipid-lowering drug candidate for a total amount exceeding 2 billion US dollars, while the latter signed an exclusive licensing agreement with Novartis for a small-molecule anti-cancer drug, with a potential transaction value surpassing 1.17 billion US dollars.

Relevant media statistics show,So far this year, the number of commercial licensing deals for innovative drugs in China has exceeded 50, with a potential total transaction value of over 36 billion yuan.

Behind the ongoing wave of innovative drug exports, it not only signifies the recognition of the R&D capabilities of local innovative enterprises but also implies that the market will place higher demands on pharmaceutical companies in terms of actual innovation in their pipelines and expectations for market transformation. Especially during a downturn in the market environment, the allocation and optimization of resources in the R&D pipeline are particularly crucial for companies.

Therefore, some industry insiders pointed out,As the market environment changes and the development of China's innovative drug industry enters a new stage, it will become a常态化 choice for innovative drug companies to terminate pipelines with poor prospects and adjust the allocation of funds and resources for their pipelines. This may even gradually lead to a wave of pipeline optimization.

A senior executive of a listed pharmaceutical company once indicated that after more than a decade of vigorous development, China's innovative drug sector has now moved from a phase of extensive growth towards industrial structural upgrading and optimization, triggering a wave of pipeline refinement.

Zhang Yi, CEO and Chief Analyst of iiMedia Research, emphasized in an interview with the media,In the current market environment, companies will be more inclined to allocate resources and funds to projects that are close to the market, have high returns, and strong certainty when adjusting their R&D pipelines.

Since the beginning of this year alone, more than ten pharmaceutical companies, including leading and small-to-medium-sized enterprises, have optimized their R&D pipelines. Reasons range from adjustments in corporate strategies to unfavorable clinical data, low R&D returns, and unremarkable competitive advantages.

(2024 Partial Cessation of R&D Pipelines by Some Innovative Drug Companies in China, Source: Corporate Announcements, Media Information Compilation)

As Huadong Medicine announced in mid-August that the subsequent development of the TTP273 project, an oral small molecule GLP-1 receptor agonist introduced from the US vTv Therapeutics at the end of 2017, will be terminated due toAnother GLP-1 targeted product under development by Huadong Medicine has shown significantly greater efficacy and higher market potential for weight loss indications.

Therefore, Huadong Medicine decided to cut losses in time and focus its energy and resources on promoting the research of other innovative products with more obvious advantages. Previously, Huadong Medicine's total direct R&D investment in the TTP273 project amounted to approximately 1.97 billion yuan (including a 10 million US dollar upfront payment and registration milestone payments).

Similar to Huadong Medicine, BeiGene and Tiantan Biologics have also proactively ceased further R&D investment in related pipelines during internal optimization adjustments, based on market competition dynamics and their own strategic considerations. In February this year, BeiGene announced the termination of four allogeneic NK cell therapy programs targeting specific antigens, which were acquired from Shoreline Biosciences in June 2021, with a prepayment of $45 million made in 2022.

Athenex and Laekna discontinued their product pipelines due to clinical trials not meeting expected outcomes, while Probiomed's Phase III clinical trial of Sofalcone Injection for treating acute ischemic stroke was abandoned because the trial coincided with widespread pandemic lockdowns across China, which could have led to potential quality risks in the clinical study data.

It is worth mentioning thatWalvax Biotech Terminates Five Vaccine Developments in Q2, Four of Which Are COVID-19 VaccinesDue to the focus on earlier virus mutations, continuing investment would be hard to yield further commercial benefits, thus the decision to terminate was made.

Moreover, affected by the underperformance of two core products—the bivalent HPV vaccine and the 13-valent pneumococcal conjugate vaccine—in 2023, Walvax Biotechnology experienced a dual decline in revenue and net profit during the year. This downward trend persisted into the first half of 2024, with revenue and net profit falling by 33.88% and 62.53%, respectively. In light of overall operational development considerations, pipeline optimization has become inevitable.

By contrast, Zai Lab, which saw a significant slowdown in overall revenue growth and cut three drug pipelines in 2023, decided to terminate the development of Margetuximab, Odronextamab, and BLU-945 after evaluating the developmental potential of their research projects and the competitive landscape of the disease areas involved. Notably, two of these drugs were nearing market launch and commercialization.

AndAfter halting R&D investment in the aforementioned three drugs, Zai Lab's R&D expenditure decreased by 7.12% to US$266 million in 2023, while its net loss for the same period narrowed by more than 20%.By the middle of 2024, the company's revenue growth exceeded that of 2023, increasing by 42.35% year-on-year to 188 million yuan, while the net loss narrowed further by 20% year-on-year to 134 million yuan.

Industry insiders pointed out that when a company decides to cut its pipeline, it needs to comprehensively consider factors such as investment, development prospects, and market changes. In the current environment, innovative pharmaceutical companies optimizing their asset pipelines based on cost-effectiveness is actually a positive phenomenon.From the perspective of the entire industry, including investment and financing, industry regulation, and other aspects, every facet of China's biopharmaceuticals sector is currently undergoing a process of optimization and restructuring.

Moreover, the changing market environment not only impacts domestic companies but also the multinational corporations (MNCs), who, while heavily investing in acquiring promising pipelines, are simultaneously "phasing out" products with low return on investment or poor prospects to cut losses in a timely manner.

For example, Johnson & Johnson, which has just disclosed its Q3 earnings report, saw its innovative drug business revenue grow by 4.9% year-over-year to $14.58 billion during the period, thanks to strong sales growth of products such as Darzalex (daratumumab), Erleada (apalutamide), and Carvykti (cilta-cel). However, it also quietly...Kicked three early- and mid-stage candidate drugs in the field of neuroscience out of the research pipeline.

(2024MNCs in some yearsEnterpriseTermination of R&D Pipeline Status, Source:Corporate Announcements, Media Information Compilation)

Wave Life Sciences, Takeda's partner, also disclosed in a document that Takeda had decided on October 11 to abandon the option for Huntington's disease therapies, including WVE-003. The two parties signed a related strategic cooperation agreement in February 2018 to jointly develop nucleic acid drugs for the treatment of central nervous system disorders, and so far, Takeda has paid Wave Life Sciences approximately $260 million.

On October 15, Pfizer announced a strategic collaboration and licensing agreement worth over $1.5 billion with TRIANA Biomedicines to discover novel molecular glue degraders for multiple targets. Just half a month ago, Pfizer had drawn industry attention due to a failed drug clinical trial.

Pfizer's sickle cell disease treatment drug Oxbryta (also known as Voxelotor), which was acquired for $5.4 billion in 2022, has been found to have serious complications and death risks according to the latest clinical data. As a result, all production batches for this indication have been recalled, and all ongoing clinical trials and expanded access programs for the drug have been halted.

It is reported that Oxbryta's global sales reached US$328 million in 2023, but Pfizer said it did not believe the market withdrawal would affect the company’s financial guidance for 2024.

But this is not the first time Pfizer has terminated a pipeline this year. In May, the company also halted the development of three drugs that had reached Phase I or II clinical trials, in order to focus its efforts and resources on advancing the research progress of superior products already in the clinical study stage.

Outside Pfizer,BMS, Gilead, Novartis, AstraZeneca, Roche, Sanofi, and others have also announced pipeline adjustments and optimization plans.

As BMS CEO Christopher Boerner announced mid-year, the company will cut 12 R&D pipelines to save funds for investing in potential blockbuster products, such as the cell therapy Breyanzi. Previously, the company had already halted 12 projects, including the next-generation version of the immunotherapy Yervoy, SIRPα-targeted drugs, and BET-targeted drugs.

Gilead also terminated two cell therapy projects in the first half of the year, as well as six trials related to the CD47 antibody magrolimab, including studies on magrolimab combination therapies for squamous cell carcinoma of the head and neck, triple-negative breast cancer, colorectal cancer, and other solid tumors.

This project, acquired by Gilead for $4.9 billion, is a potential first-in-class anti-CD47 immunotherapy, but its clinical development has not been ideal, leaving no choice but to abandon it.

—END—

Highlights:

18A Innovative Drug Companies "Selling Shells": A New Path for Biotech Transformation?

The 10th Batch of National Collection Initiates! Scale Exceeds 40.7 Billion, Including Multiple Heavyweight Products

Nearly 8 Billion in Four Years! Akeso Biopharma Secures Another Major Round of Financing

The World’s First Oral Formulation! Targeting the Billion-Dollar Gastric Cancer Market

◆Xinkejie widely solicits contributions, which can cover topics related to the pharmaceutical industry such as pharmaceutical policies, R&D trends, and the capital market. Please send your submissions to (hejing@sinohealth.cn) and include your contact information.

◆ For business cooperation/reprint, please contact 18823242014 (same number on WeChat).