Author:Drunken Breeze Editor: VitaminWhy can重磅 products like Brukinsa (zanubrutinib), Aidifang (ivorasimab), and Carvykti (ciltacabtagene autoleucel) emerge from the fertile ground of innovative drugs in China, but the country cannot cultivate top-tier companies like Regeneron, Genentech, Vertex, or Gilead that grow from Biotech to Biopharma? This question is deeply thought-provoking amid the current investment chill in the innovative drug sector.China’s innovative drug environment boasts good products, advanced technologies, and strong teams, yet these favorable factors combined still fail to form a great enterprise. In fact, even well-known biopharmaceutical companies like Regeneron, Vertex, and Gilead experienced significant growing pains during their development phases. Under the influence of multiple factors — such as the determination of management, the support of investors, favorable policies, and the advanced nature of core technologies — they finally entered a harvest period in the 21st century: Regeneron’s Eylea (aflibercept) took a decade to develop, Vertex achieved dominance in the field of cystic fibrosis, and Gilead became a leader in antiviral therapies…Objectively speaking, the success of Regeneron, Vertex, and Gilead has an element of randomness and luck, but the extraordinary tenacity and indomitable spirit behind it are worth learning from for China's Biotech industry. Of course, we are also pleased to see that many Biotech companies in China have the courage to burn their boats and the determination to move forward, bravely facing challenges in an unfavorable market environment and actively seeking a transformation path that suits them. Since different Biotech companies specialize in different disease subfields, develop different types of modalities, and differ in terms of fundraising and capital efficiency, there is no one-size-fits-all solution. The best approach is the one that fits them.Big Moves in Equity Financing to Expand Pipelineeg:BeOne Medicines, Innovent Biologics, Junshi BiosciencesAs representatives of the "PD-1 Four小龙" in China, BeOne Medicines, Innovent Biologics, and Junshi Biosciences are key beneficiaries of the relaxed environment in both the primary and secondary markets within the country.- BeOne Medicines: Listed on the US stock market in 2016, raising $147 million; listed on the Hong Kong stock market in 2018, raising HK$7.085 billion; listed on the A-share market in 2021, raising RMB 22.16 billion.

- Innovent Biologics: Listed on the Hong Kong Stock Exchange in 2018, raising HKD 3.304 billion.

- Junshi Biosciences:Listed on the Hong Kong Stock Exchange in 2018, raising HKD 3.08 billion;Listed on the A-share market in 2020, raising 4.836 billion RMB.

The financing boom that BeOne Medicines, Innovent Biologics, and Junshi Biosciences encountered back in the day now seems unattainable.,Sufficient funds enable the company to confidently weather the winter, while other Biotechs are fretting over their tight cash flows.BeOne MedicinesRepresenting the well-funded Biotech, BeOne Medicines can expand against the market trend and enrich its clinical pipeline under research. The methods of self-research + external introduction + licensing cooperation have helped the company own multiple marketed products and products under research. In terms of going overseas, BeOne Medicines is also one of the few Biotechs that has built its own commercial team to carry out product sales locally. Compared with the strategy of most Biotechs in China seeking BD transaction cooperation with foreign MNCs for commercialization, this move by BeOne Medicines has its pros and cons. Sufficient funds can help the company seek autonomy in commercialization.Back to the essence, Biotech still needs to rely on high-quality products to speak for itself.In 2018,Junshi BiosciencesThe approval and market launch of Tuoyi (Toripalimab) ushered in a new era for innovative drugs in China. Products such as BeOne Medicines' Baizean (Tislelizumab) and Daboshu (Sintilimab) followed soon after, marking the first wave of returns on years of investment. As a phenomenal product, PD-1 has already delivered certain returns to some investors. What will be the next wave of phenomenal products—ADCs, small nucleic acids, or radiopharmaceuticals? Let us wait and see.Table 1. Sales of China-produced PD-(L)1 antibody products in the first half of 2024Source: Semi-Annual Reports of Listed Companies

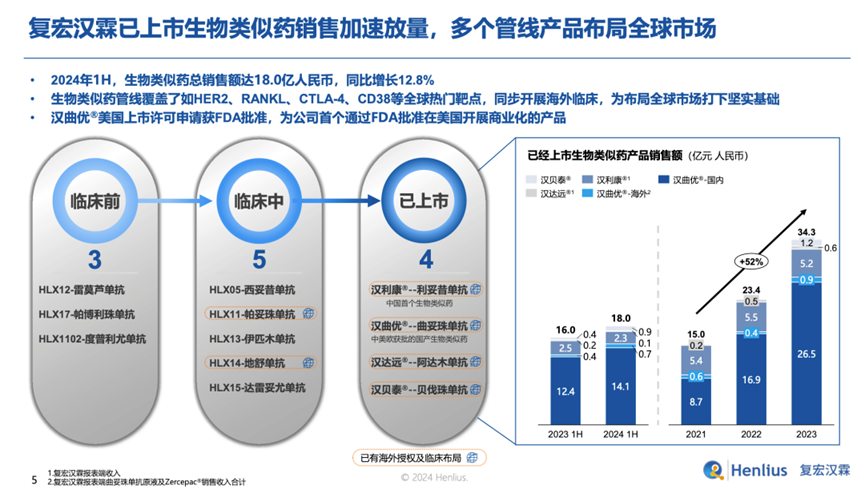

Combination of Imitation and InnovationWhen rumors of Fosun Pharma privatizing Henlius Biotech surfaced in the market, it also indirectly validated the value of Henlius Biotech. As one of the earliest China-based Biotechs listed under Hong Kong's Chapter 18A to achieve profitability,HenliusRelying on the "innovation through imitation" strategy to be the first to break out of the commercialization dilemma.Biosimilars + Innovative drugs with differentiated competitive advantages + Global commercial perspective are the reasons why Henlius Biotech stands out from a group of loss-making Biotechs.Henlius' biosimilars focus on blockbuster products, such as Hanquyou.®(Trastuzumab) has been approved for marketing in more than 40 countries and regions, including China, Europe, and the United States. In the first half of 2024, it generated revenue of 1.474 billion yuan, with sales growing by 15.4% year-on-year. Hanbeitai®(Bevacizumab), Hanlikang®(Rituximab), Handayan®(Adalimumab) has been launched and is already on the market, while actively expanding into overseas markets. Although Hansizhuang (Seriplimab) was not among the first batch of PD-1 inhibitors to be marketed, it quickly captured a significant share of the domestic market in China by focusing on differentiated indications (small cell lung cancer), later becoming a "RMB billion molecule." In the future, as Henlius continues to explore new markets and new indications with multiple products, the company’s growth potential is worth anticipating.

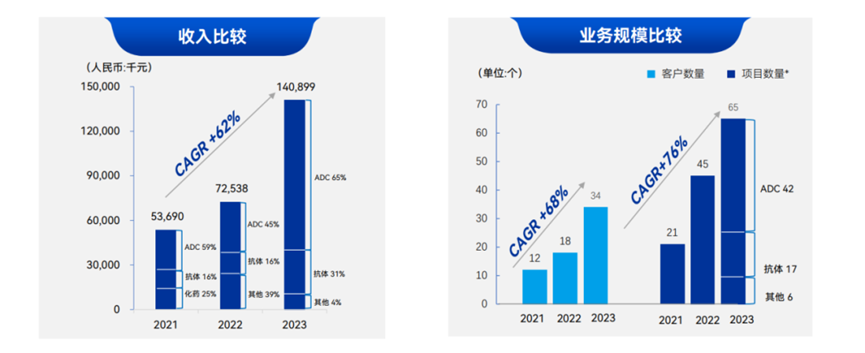

Figure 1. Accelerated Sales of Henlius’ Marketed Biosimilars, Source: Henlius 2024 Interim Report

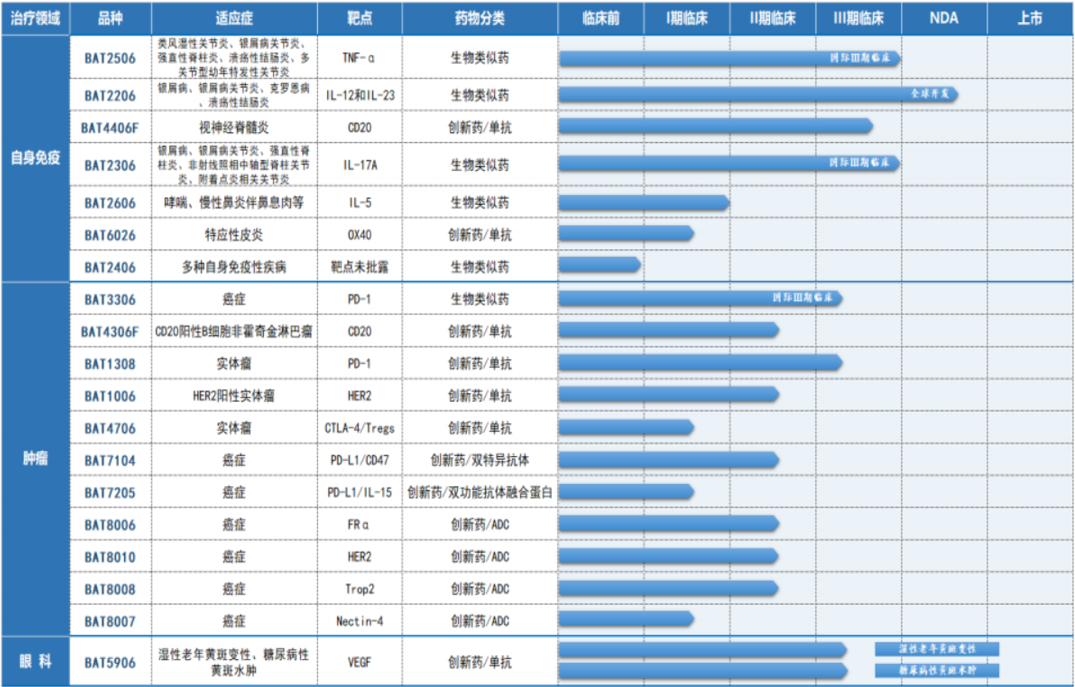

Compared to relying solely on self-developed innovative drug businesses, the strategy of developing biosimilars has its unique advantages — well-established market education, controllable R&D and production costs, and the ability to capture market share through competitive pricing during commercialization...Bio-TheraIt is also a practitioner of the "biosimilar + me better" strategy.Bio-Thera Builds Seven Core Technology Platforms, Covering the Entire Process of Antibody Drug Development. The company has three biosimilars on the market: Adalimumab (launched in China), Bevacizumab (launched in both China and the US, received positive opinion from EMA in June 2024), and Tocilizumab (launched in China, the US, and Europe). One innovative drug, Bavituximab, was approved for marketing in June 2024.At the same time, it actively engages in commercial collaborations, having reached 13 license-out agreements globally for five varieties, including Bevacizumab, with partners such as BeOne Medicines, Sandoz, and Biogen. Moreover, its R&D pipeline is well-stocked: Ustekinumab has submitted an application for market approval to the NMPA, Bevacizumab has submitted an application for market approval to the EMA, six products are in Phase III clinical trials, and multiple products are in the clinical research stage.

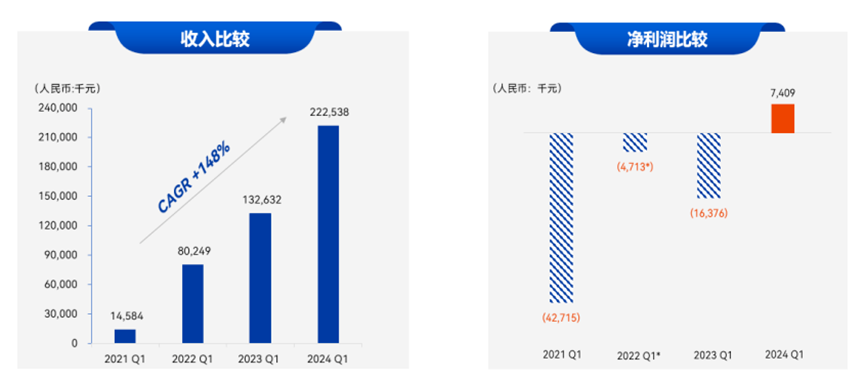

Figure 2. Bio-Thera’s R&D Pipeline Progress, Source: Bio-Thera 2024 Half-Year Reporteg:Zai Lab, Everest MedicinesWhen it comes to the License-in model, the representative companies are Zai Lab and Everest Medicines. As exemplary models of "capital + international vision," Zai Lab and Everest Medicines have extraordinary considerations in selecting products for introduction, advancing subsequent clinical trials, and commercial promotion after product launch. The products licensed in by Zai Lab and Everest Medicines generally avoid traditionally highly competitive targets such as EGFR, VEGF, BTK, CD19, and BCMA… It is undeniable that although the introduced products hold significant clinical value, there remains a certain gap before this translates into extremely high commercial value.

In essence, the License-in business model is like an investment. For a pharmaceutical company to make money from a deal, it must introduce products with sufficient market potential.After deducting the down payment, milestone payments, subsequent R&D expenses, and commercialization expenses, the remaining money is the pharmaceutical company's profit. However, in China, the license-in model does not necessarily allow pharmaceutical companies to make money because when drugs are introduced from high-price regions overseas to low-price regions, the pricing of the drugs is often subject to a significant discount.

For exampleZai LabThe drug Veiglivo, which costs about $6,000 per 400mg vial in the U.S., is expected to result in annual treatment costs as high as $200,000 for patients. In China, after Efgartigimod entered the medical insurance system, its price dropped to 5,608 yuan per vial. Insufficient payment ability leads to limited returns for pharmaceutical companies introducing the drug. Moreover, continuous investment is required for subsequent drug development and building sales teams. This presents a significant challenge for innovative pharmaceutical companies that are not yet self-sustaining.

Perhaps it is precisely because of seeing these shortcomings that Zai Lab has started to engage in CSO business. In 2024, Zai Lab acquired partial Greater China sales rights for the blockbuster PD-1 drug Nivolumab (Opdivo, or "O Drug") from BMS. It will obtain the sales rights for Opdivo in 10 provinces: Yunnan, Guizhou, Guangxi, Inner Mongolia, Xinjiang, Gansu, Ningxia, Qinghai, Hebei, and Shanxi. The purpose of doing so is to maximize the efficiency of the marketing team and spread out the cost of the marketing team. The gap in payment capability within the local pharmaceutical market means that pharmaceutical companies cannot rely on simple and crude "ready-made solutions." As a pioneer of the license-in model in China, Zai Lab and Everest Medicines continue to explore this approach to this day.After relying on an advanced BD transaction strategy to "return" Sacituzumab Govitecan,Everest MedicinesDecided to focus on three areas: anti-infective, nephrology, and autoimmune. In July 2023, Yijia®(Eravacycline) commercially launched in China; In November, Nefukang®Approved in China, becoming the only causative treatment drug for adult primary IgA nephropathy in China, and successfully commercially launched in May this year.The consecutive launches of two major products have not only solidified the company’s certainty but also built confidence among all sectors of the market. In the first half of 2024, total revenue reached RMB 3.02 billion, a significant increase of 158% compared to the second half of 2023, marking the company's first-ever commercial profitability in its history. Meanwhile, the company maintains robust financial health, with cash reserves amounting to RMB 19.3 billion in the first half of 2024, providing assurance for future business development and sustained growth.

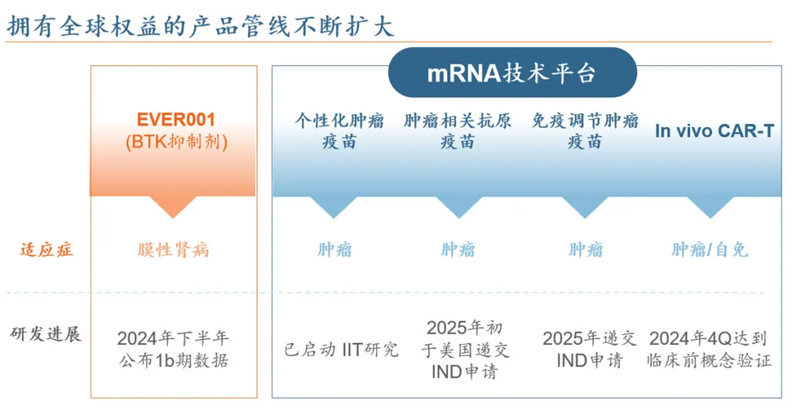

Figure 3. Everest Medicines’ R&D Pipeline,Source:Everest Medicines

eg:Akeso, Legend, Ascentage, HutchmedFrom "License in" to "License out," China's Biotech industry has fully demonstrated the competitiveness of its flagship products in the past two years.Two years ago,Akeso BiopharmaThe BD deal between Summit and Akeso regarding Idafornib welcomed success two years later. In December 2022, Akeso announced that it had licensed partial commercial rights of its bispecific antibody to Summit Therapeutics for up to 5 billion US dollars. Summit Therapeutics obtained exclusive development and commercial rights for Ivonescimab in the United States, Canada, Europe, and Japan.At that time,The reason why Kangfang's License out deal has attracted much attention is that both the upfront payment (500 million US dollars) and the highest transaction amount have broken the record for the largest outbound licensing deal for an unlisted new drug.; At that time, the externally authorized product Yivoki had entered Phase III clinical trials for NSCLC, including a monotherapy head-to-head challenge against Keytruda as a first-line treatment and a combination therapy with chemotherapy for EGFR TKI-resistant second-line treatment, supported by breakthrough therapy designation, with the potential to become a major blockbuster in the bispecific antibody field.In September 2024, Ivolitinib became the world's first and only drug to demonstrate significantly superior efficacy compared to Keytruda in a Phase III monotherapy "head-to-head" clinical trial.At the 2024 World Lung Cancer Conference, Akeso announced the data from the registrational Phase III clinical study (HARMONi-2) comparing its self-developed, world's first PD-1/VEGF bispecific antibody drug, Ivonescimab (AK-112), as a monotherapy versus K-drug (Pembrolizumab) as a monotherapy for first-line treatment of locally advanced or metastatic non-small cell lung cancer (NSCLC) with positive PD-L1 expression (PD-L1 TPS≥1%). In the intent-to-treat (ITT) population, Ivonescimab monotherapy significantly prolonged patients' progression-free survival (PFS) compared to K-drug monotherapy. The median progression-free survival (mPFS) was record-breaking, nearly doubling that of the K-drug group (11.14 months vs. 5.82 months), and significantly reduced the risk of disease progression/death by 49%.Cilta-cel (Chinese trade name: Carvykti, English trade name: Carvykti) is produced in NanjingLegend BiotechA CAR-T therapy targeting BCMA. The drug was first approved for marketing in the United States in February 2022, followed by a conditional marketing authorization granted by the EU EC in May of the same year, and approval from Japan's MHLW in September, for the treatment of adult patients with relapsed or refractory multiple myeloma. In August 2024, the drug was finally approved for marketing in China, for the treatment of relapsed or refractory multiple myeloma in patients who have progressed after receiving at least three prior lines of therapy (including at least one proteasome inhibitor and one immunomodulatory agent).Adult Patients。

As early as 2017, Cilta-cel caught the attention of Johnson & Johnson with early clinical data showing an ORR (Overall Response Rate) of 100%. J&J paid Legend Biotech an upfront payment of $350 million along with subsequent milestone payments to co-develop and commercialize cilta-cel, setting a record for the largest upfront payment in a patent licensing deal by a Chinese pharmaceutical company at that time, as well as offering the best terms of cooperation. Objectively speaking, the commercial performance of CGT products within China has been less than ideal. If Cilta-cel had not expanded overseas and chosen a multinational partner like J&J, it might not have become the blockbuster product it is today.

In 2023, the sales of Cilta-cel reached 500 million US dollars, and in the first half of 2024, the sales were 343 million US dollars (2.4 billion RMB), increasing by 82% year-on-year. Johnson & Johnson expects that the peak sales of this drug will exceed 1 billion US dollars.HutchmedThe reason why fruquintinib was acquired by Takeda for over $1.1 billion in total (with an upfront payment of $400 million) lies in the solid support of global multi-center clinical data, enabling it to enter the U.S. market with a faster uptake than in the Chinese market. Fruquintinib is the first and only small-molecule targeted drug approved in the U.S. in the past 10 years for third-line mCRC, and its excellent efficacy has been included in the NCCN guidelines.

Ascentage PharmaAurora Borealis (Nirik) reached a licensing cooperation agreement with Takeda worth $1.3 billion in total, setting the highest record for China-produced small-molecule oncology drugs in external BD, and also received an investment from Takeda, thanks to its original innovative thinking.Nelike is the first and only third-generation BCR-ABL inhibitor approved for marketing in China. It has addressed the clinical gap and demonstrated better efficacy and safety compared to Takeda's Ponatinib.After introducing Nulast, Takeda has gained the confidence to compete with Novartis' Asciminib and solidify its dominance in the CML market.eg:Tomei Pharmaceuticals, Harbour BioMedThe research and development of innovative drugs is highly uncertain, with risks such as long R&D cycles, high investment, and slow returns. Given that the company has a strong technical platform and production capacity, why not transition to a CXO model, relying on "technical services" to generate cash flow first, helping the company survive through cycles. Examples of this approach include TOT Biopharm and Harbour BioMed.Tomeison PharmaceuticalsFounded in 2010, the company initially built its own drug R&D pipeline, pilot plant, and began constructing a commercial production base. In addition to the already initiated Bevacizumab biosimilar (TAB008), in 2013, TOT Biopharm initiated the development of the T-DM1 ADC (TAA013) drug, being one of the earliest pharmaceutical companies in China to research ADCs.With the continuous improvement of global biosimilar-related regulations and changes in the industrial environment, after 11 years, in 2021, TOT Biopharm's self-developed monoclonal antibodyProduct Puxinting®(Bevacizumab Injection) has been successfully launched and is currently in ongoing commercial production.ADC drugs, composed of three key elements—antibodies, linkers, and highly potent molecules—differ in development from antibody drugs due to the presence of more technical barriers. Each step of the development strategy is closely tied to numerous regulatory standards, posing challenges that require communication and confirmation. In 2023, after conducting a comprehensive and cautious analysis and evaluation of the future commercial value and market sales of TAA013, and aligning with the company’s strategic planning, TOT Biopharm announced the termination of the Phase III clinical trial and development of TAA013 in China.In the R&D of ADC drugs, TOT Biopharm integrates its past experience into ADC CDMO services, providing partners with robust and efficient product development acceleration. Its integrated platform for antibody/ADC/XDC research and production highlights the company’s differentiated competitive edge and service characteristics among similar companies. In H1 2024, TOT Biopharm achieved profitability and demonstrated counter-cyclical growth amidst the downturn affecting China's Biotech and CXO sectors, a feat that is truly commendable.

Figure 4. Revenue and Business Scale Details of TOT Biopharm, Source: TOT BiopharmHBM PharmaAchieved a net profit of $1.397 million in the first half of 2024, equivalent to nearly RMB 10 million. Harbour BioMed based on Harbour Mice®...and other core technology platforms, while advancing its self-developed pipeline, considering the lengthy clinical phase of innovative drugs, adopted a more pragmatic approach to explore profit models: establishing the subsidiary Nona Biologics to provide global pharmaceutical companies with one-stop solutions from target identification (I) to investigational new drug (IND) enabling studies (ITM), covering comprehensive services from discovery to preclinical development.From a business model perspective, NanoBiologics is not a traditional CRO but rather a monetization of core innovation capabilities: In addition to generating profits through conventional service models, NanoBiologics can also earn substantial milestone-based revenues through licensing and other models.It is precisely because of the outstanding performance of Nona Biologics that HBM continues to be profitable.On one hand, Nanor Biotech reached a deal worth up to $604 million with AstraZeneca in the first half of the year, including a $19 million upfront payment and a $10 million near-term milestone payment. The company has already received the $19 million upfront payment in the first half, contributing significantly to its revenue. On the other hand, a stable service model is also one of Nanor Biotech's core sources of profit. In H1 2024, Nanor Biotech’s research service fees increased by 167.4% compared to the same period last year, reaching $2.326 million, equivalent to over 16 million RMB.

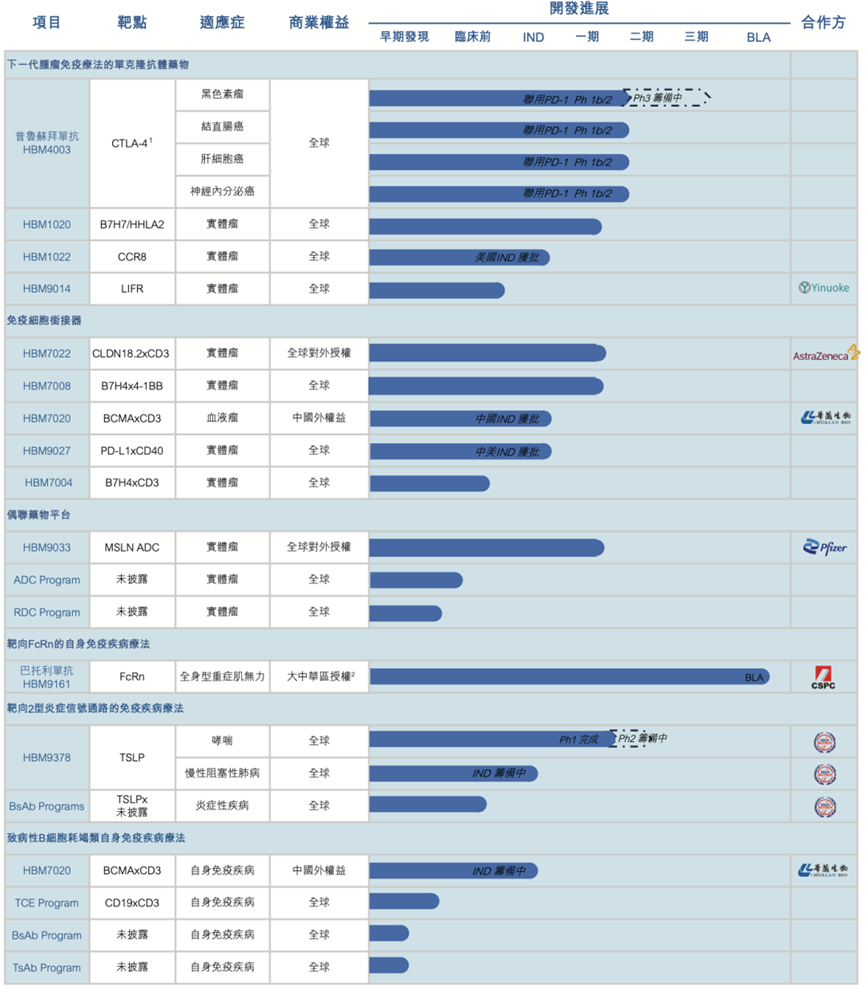

Figure 5. Progress of HBM’s R&D Pipeline, Source: HBM

"If Heaven Had Feelings, It Would Grow Old; The Right Path of Humanity Is Change and Suffering." Biotech, tempered by time, will prove their worth. Traditional growth logic and winning formulas no longer apply to the new era. The key lies in shifting from following trends and rapid replication to meticulous cultivation, leveraging genuine technological advantages and differentiated strategies to seek new growth and opportunities.

Survival of the fittest. At any time, enterprises should not complain about the market environment. Every drastic change in the environment also brings new opportunities.

[1] Biotech VS Pharma: A Comprehensive Exploration of Commercialization Pathways. Written by the Same Author[2] Efficiency Determines Biotech's Survival: The Enlightenment from Everest Medicines' Two-Year Journey Through the "Darkest Hour". E Drug Manager[3] Where is the future of China's innovative drugs? Insights[4] Head-to-Head Win Over K Drug! Akeso's Next Mission: Creating the Second Chinese "Billion-Dollar Molecule". E Drug Manager[5] Strive for Annual Revenue to Breakthrough 1 Billion Yuan: Unveiling the Dark Horse CDMO, TOT Biopharm. BIG Biotech Innovation Hub[6] Achieve sustainable profitability and initiate the "flywheel effect" in platform-based Biotech. Amino Observation*Disclaimer: This article only introduces the research progress in the pharmaceutical and disease fields, briefly describes the research overview, or shares pharmaceutical-related information. It does not recommend any treatment or diagnostic plans, nor does it constitute any advice on related investments.If there are any omissions, please feel free to communicate and point them out!