Novo Nordisk 2024 Q3 Report: On the Verge of a New Blockbuster Drug?

Novo Nordisk

Insulin Developer and Manufacturer

ToPoint

1

GLP-1 Drugs Cumulative Sales in the First Three Quarters of 2024 Reach $219.67 Billion;

2

Semaglutide's cumulative sales reach $20.585 billion, poised to compete for the top-selling drug title;

3

The U.S. market remains strong, with a growth rate of 32%. In this market, the sales proportion of GLP-1 drugs is as high as 66%.

4

China Market Growth Rate 10%.

Breaking News

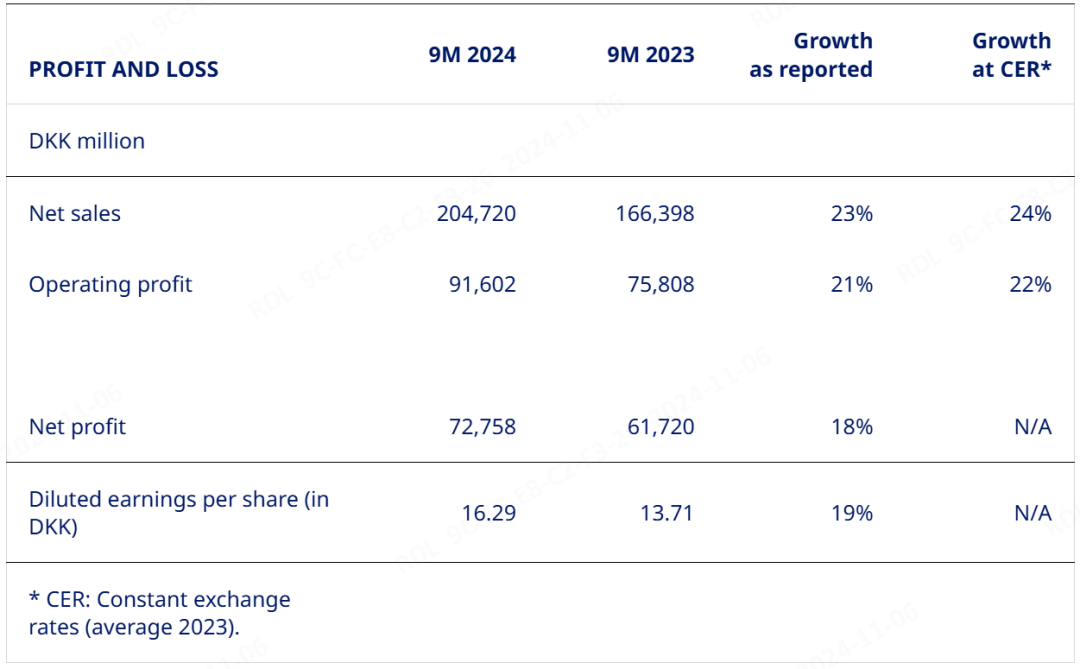

On November 6, 2024, Novo Nordisk announced its financial results for the third quarter of 2024. According to the earnings report, Novo Nordisk's cumulative revenue for the first three quarters reached DKK 204.72 billion (USD 298.43 billion), representing a year-on-year increase of 24%; net profit increased by 18% year-on-year to DKK 72.758 billion (USD 106.06 billion); research and development investment in the first three quarters amounted to DKK 34.26 billion (USD 49.94 billion), marking a year-on-year increase of 56%.

Figure 1. Novo Nordisk Earnings Announcement

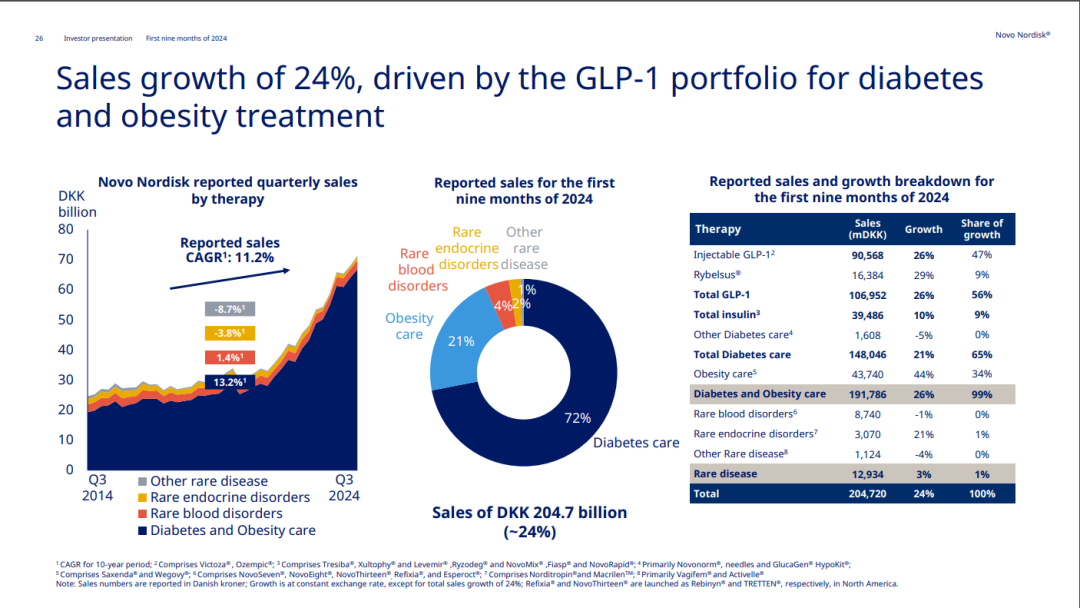

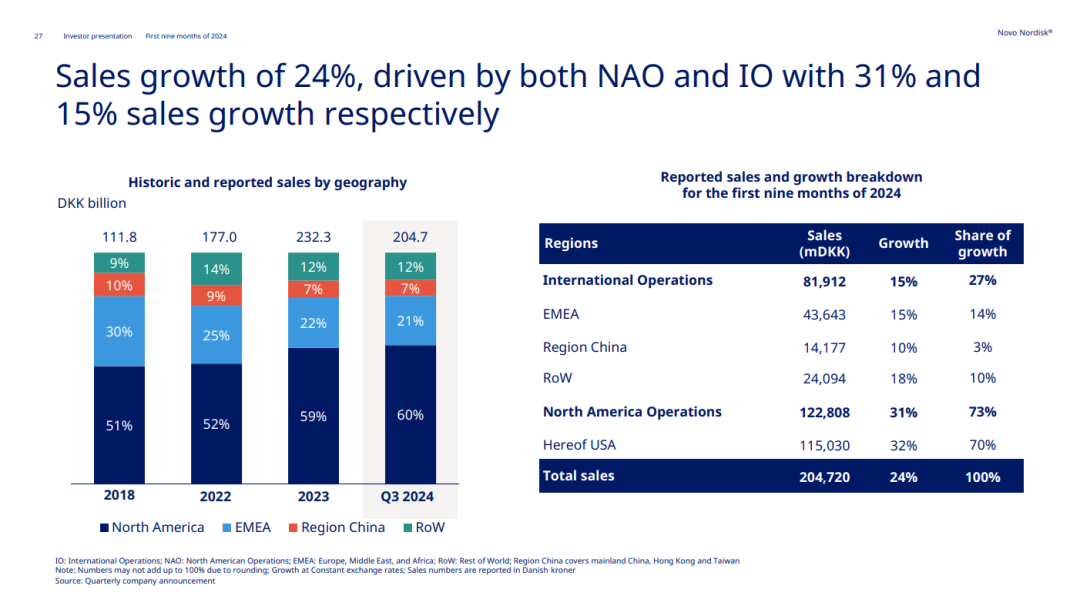

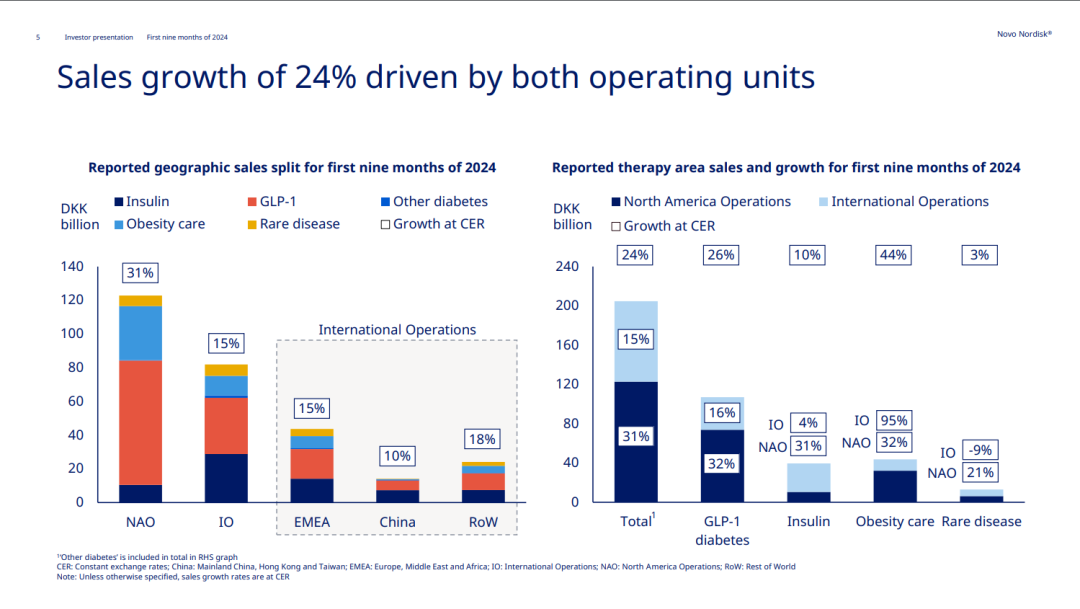

The overall growth of the company's business, from a business perspective, is attributed to the 26% growth in GLP-1 and 44% growth in obesity care; geographically, it is driven by a strong 31% growth in North America. The growth rate of the business in China was 10%, lagging behind EMEA.

As one of the three major insulin monopolies, Novo Nordisk's insulin product series is no longer a strong cash cow or star product. Instead, diabetes and weight-loss drugs led by GLP-1, specifically liraglutide and semaglutide, have taken over, contributing nearly 74% of sales.

North America is the most important market, accounting for 60% of the company's total revenue. The main consumer countries of GLP-1 drugs are also in North America, with the United States being the primary consumer. In this market, revenue from GLP-1 drugs accounts for as high as 66% of the total GLP-1 drug market.

In the third quarter alone, Novo Nordisk achieved revenue of 71.311 billion Danish kroner (10.395 billion US dollars), a year-on-year increase of 21%; net profit increased by 22% year-on-year to 27.301 billion Danish kroner (3.980 billion US dollars).

Figure 2. Novo Nordisk 2024 Q3 Performance

Figure 3. Novo Nordisk's Performance in Different Regions

Figure 4. Contribution of Regions and Business Segments to Novo Nordisk's Q3 2024 Performance

About the Sales of GLP-1 Drugs

In the first three quarters, Novo Nordisk's diabetes and obesity care division achieved total revenue of 191.786 billion Danish kroner (27.957 billion US dollars), a year-on-year increase of 26%; the rare disease division achieved revenue of 12.934 billion Danish kroner (1.885 billion US dollars), a year-on-year increase of 3%.

Among them, the sales of GLP-1 drugs in the diabetes field reached 106.952 billion Danish kroner (15.591 billion US dollars), and the sales in the obesity field were 43.74 billion Danish kroner (6.376 billion US dollars). This also means that the combined revenue of liraglutide and semaglutide reached 21.967 billion US dollars, of which liraglutide (including Victoza®and Saxenda®) Sales amounted to 9.479 billion Danish kroner (1.382 billion US dollars), Semaglutide (including Ozempic®、Rybelsus®And Wegovy®) Sales amounted to 141.213 billion Danish kroner (20.585 billion US dollars).

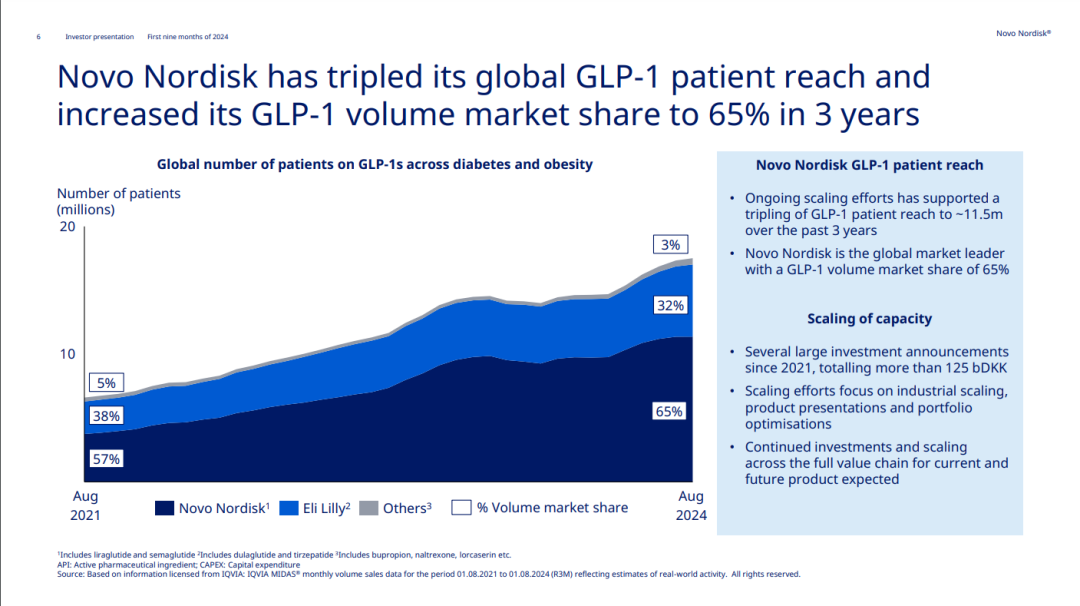

In the past three years, the company's GLP-1 drugs have covered approximately 11.5 million patients, capturing a 65% market share in terms of sales volume, which is twice that of Lilly.

Figure 5. Coverage and Market Share of Novo Nordisk GLP-1 Drugs

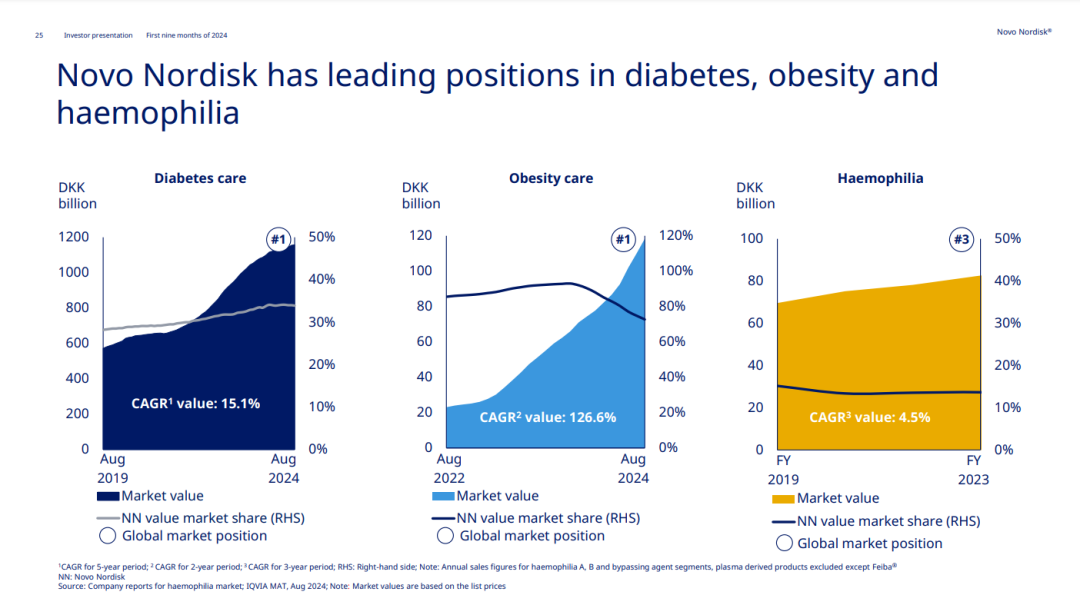

Whether in the diabetes or obesity sector, the company's market share ranks first.

Figure 6. Novo Nordisk's Market Share

Diabetes Business

Q3, Ozempic®Performance was outstanding, achieving 29.804 billion Danish kroner (4.345 billion US dollars) in sales, ranking first on the best-selling products list, with a year-on-year increase of 24.64%. The largest contribution came from the North American market, reaching 22.841 billion Danish kroner (3.330 billion US dollars), at least three times that of other markets, with a year-on-year growth of 35.85%.

Rybelsus®Revenue in the third quarter reached 5.453 billion Danish kroner (795 million USD), increasing by 21.29% year-on-year. Of this, the North American market contributed 2.509 billion Danish kroner (366 million USD), representing a year-on-year decrease of 3.65%.

Victoza®(Liraglutide) reported a loss of 322 million Danish kroner ($47 million) in the third quarter, a year-on-year decrease of 114.46%.

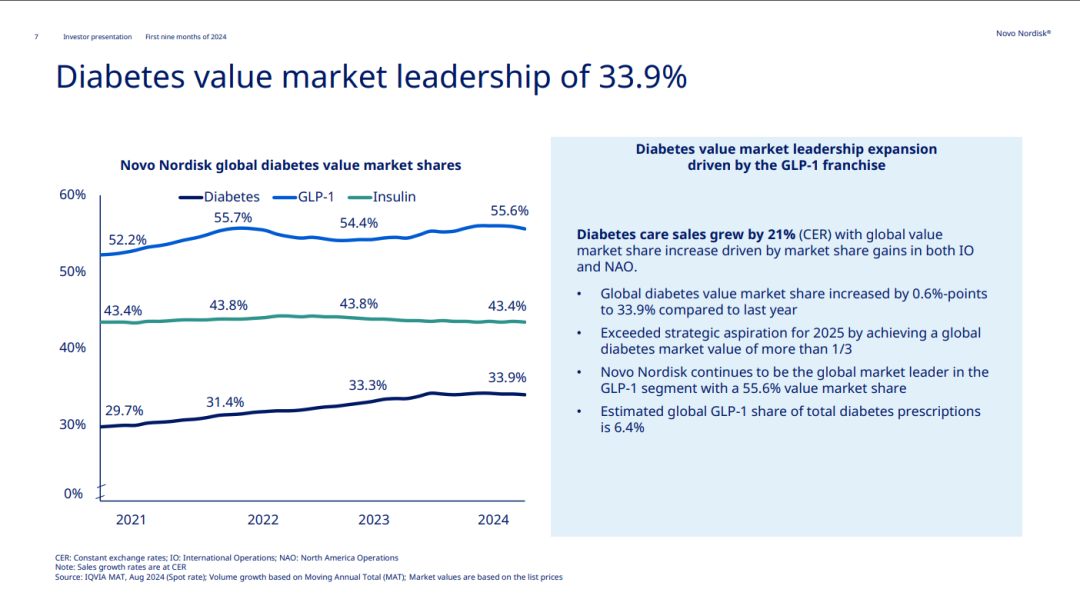

Driven by the GLP-1 drugs in the North American market, the diabetes care business grew 21% to 148.046 billion Danish kroner (21.581 billion US dollars). In the past 12 months, the global market share of Novo Nordisk's diabetes drugs increased from 33.3% to 33.9%. Products for treating type 2 diabetes centered on GLP-1 (Rybelsus®, Ozempic®and Victoza®) Increased from 54.4% to 55.6%.

Figure 7. Market Share of Novo Nordisk's Various Diabetes Drugs

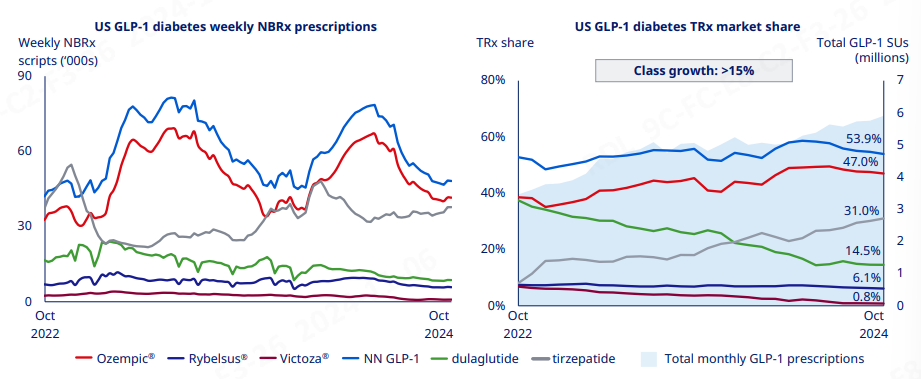

In terms of new and total prescriptions in North America, the market competition still centers around semaglutide (Rybelsus).®And Ozempic®) and tirzepatide as the main players, but it is clear that semaglutide is entering the declining phase of its lifecycle, while tirzepatide is at its peak. As older-generation GLP-1 drugs, the decline of liraglutide and dulaglutide is irreversible.

Figure 8. New and Total Prescriptions of GLP-1 Diabetes Drugs in the United States

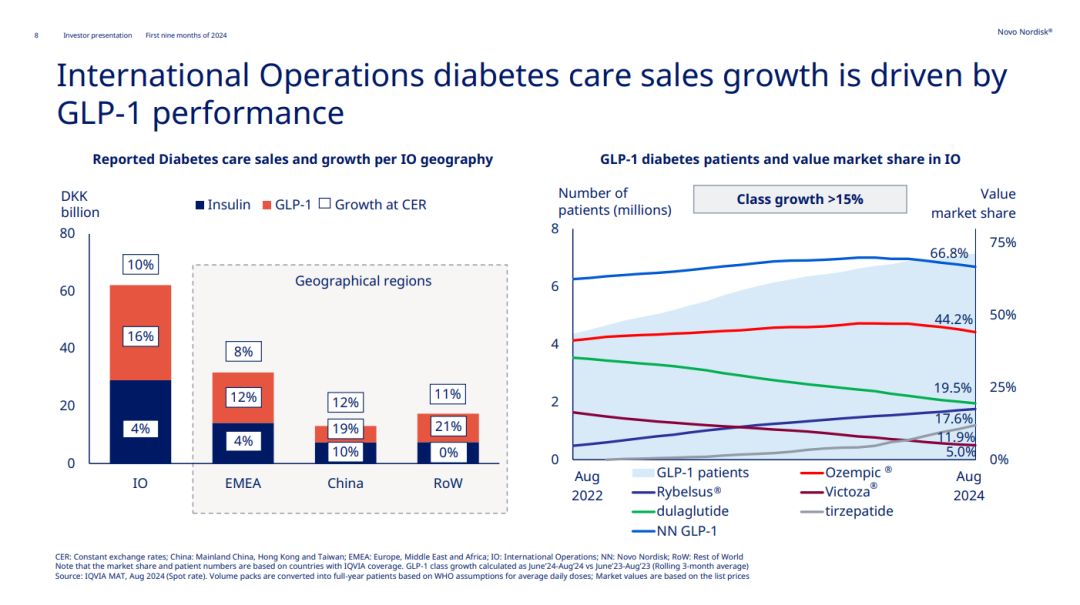

The performance in international markets outside North America also benefited from the growth of GLP-1 (16%). Whether in EMEA or China, a certain proportion of insulin products are holding their own against it. In terms of patient coverage and market share, semaglutide injection (Ozempic®) are the best-performing varieties. In terms of growth potential, the most competitive product is Novo Nordisk's own semaglutide tablets (Rybelsus).®) and Lilly's tirzepatide, with the former performing much better in the international market than in the North American market, while the latter's main market is in North America.

Figure 9. New and Total Prescriptions for GLP-1 Diabetes Drugs in the International Market

Obesity Business

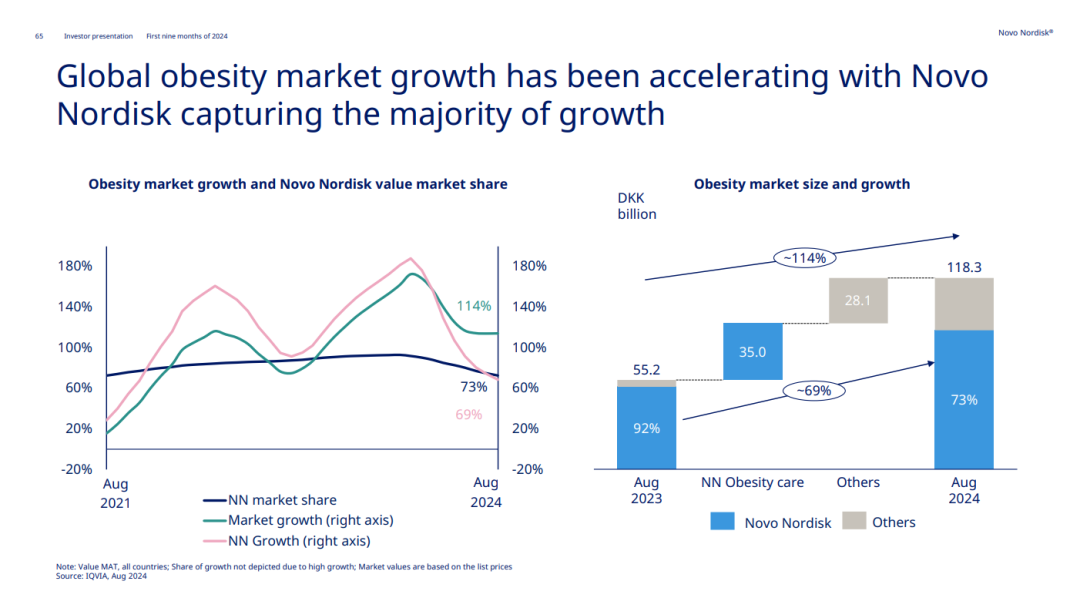

Obesity care business grew by 44% to DKK 43.74 billion (USD 6.376 billion). Although Novo Nordisk remains the market leader in the obesity sector with a 73% market share, the company's market share and growth rate have been significantly impacted by the launch of competing products, with its growth rate once dropping from 180% to 60%.

Figure 10. Novo Nordisk's Market Share in the Obesity Field

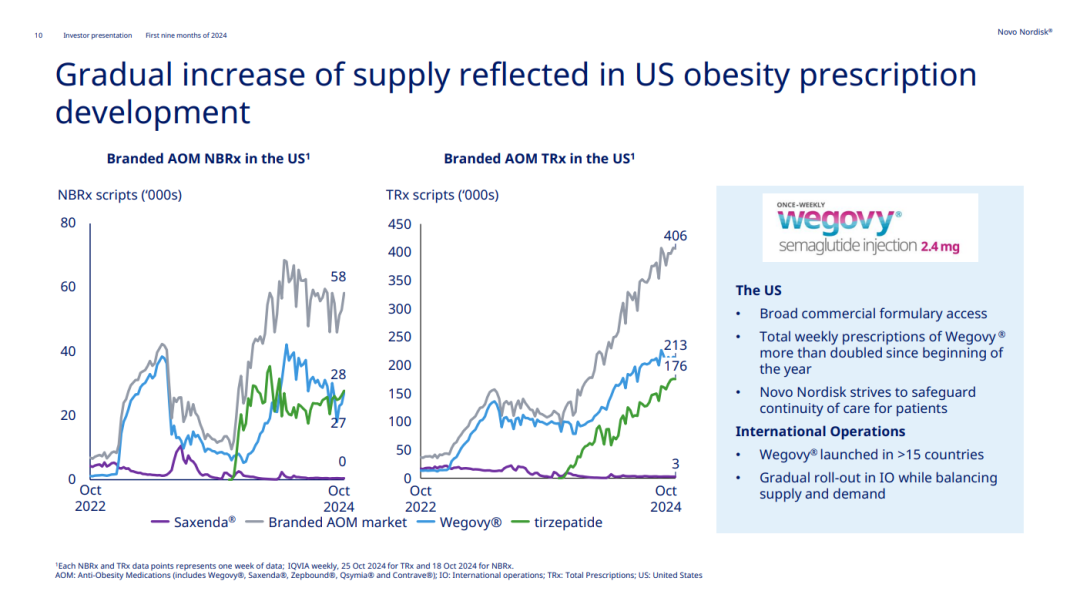

In North America, the competition in weight-loss drugs is mainly between semaglutide and tirzepatide, with remarkable growth, while liraglutide has gradually been phased out of the market.

Wegovy®Revenue in the third quarter was DKK 17.304 billion (USD 2.522 billion), a year-on-year increase of 79.35%. Of this, the North American market contributed DKK 12.827 billion (USD 1.870 billion), which is 2.9 times that of other markets, with a year-on-year increase of 39.41%.

Saxenda®Revenue in the third quarter was DKK 1.497 billion (USD 218 million), a year-on-year decrease of 42.58%.

Figure 11. New and total prescriptions for weight-loss drugs in North America

Pipeline Progress

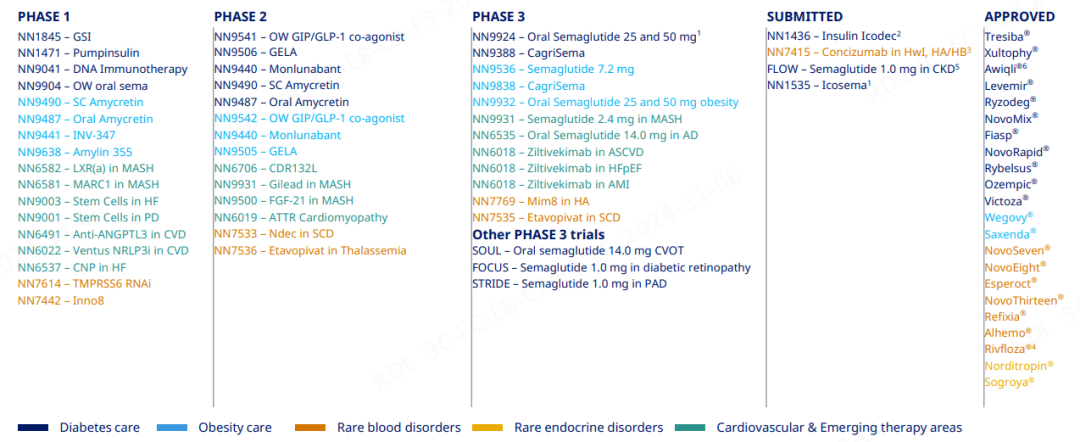

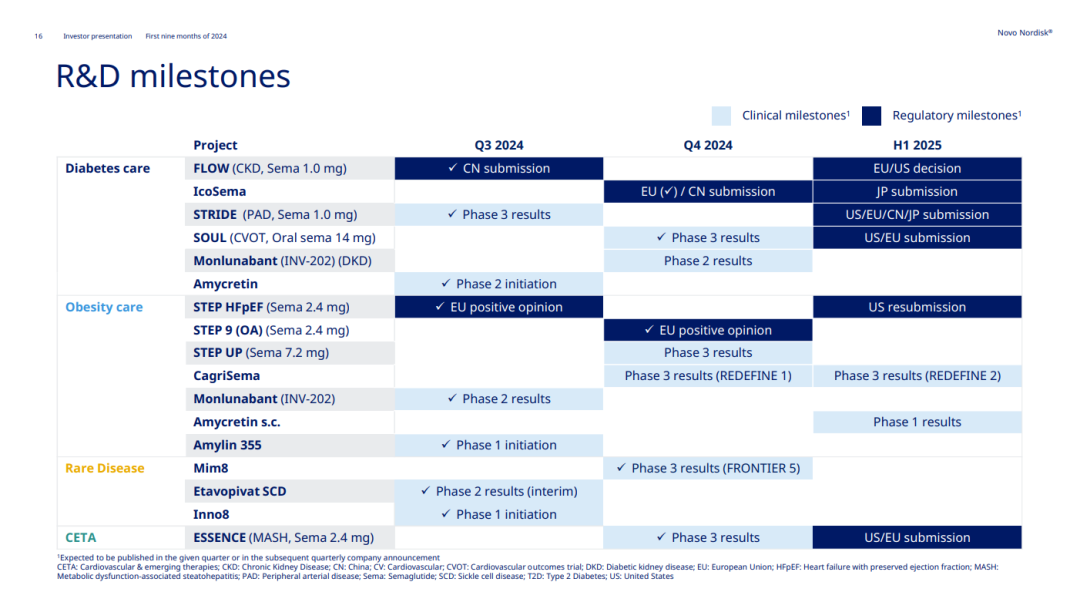

As of 2024 Q3, Novo Nordisk has 17 Phase I pipelines, 14 Phase II pipelines, 15 Phase III pipelines, and 4 pre-registration drugs. Among them, there are 17 pipelines for diabetes care, 10 for obesity management, 7 for rare blood disorders, and 16 for cardiovascular and emerging therapeutic areas. Key milestones in Q3 include the submission of a 1.0mg semaglutide application for chronic kidney disease in China.

Figure 12. Novo Nordisk Pipeline

Figure 13. Novo Nordisk Key R&D Milestones

At the same time, Novo Nordisk announced several clinical results:

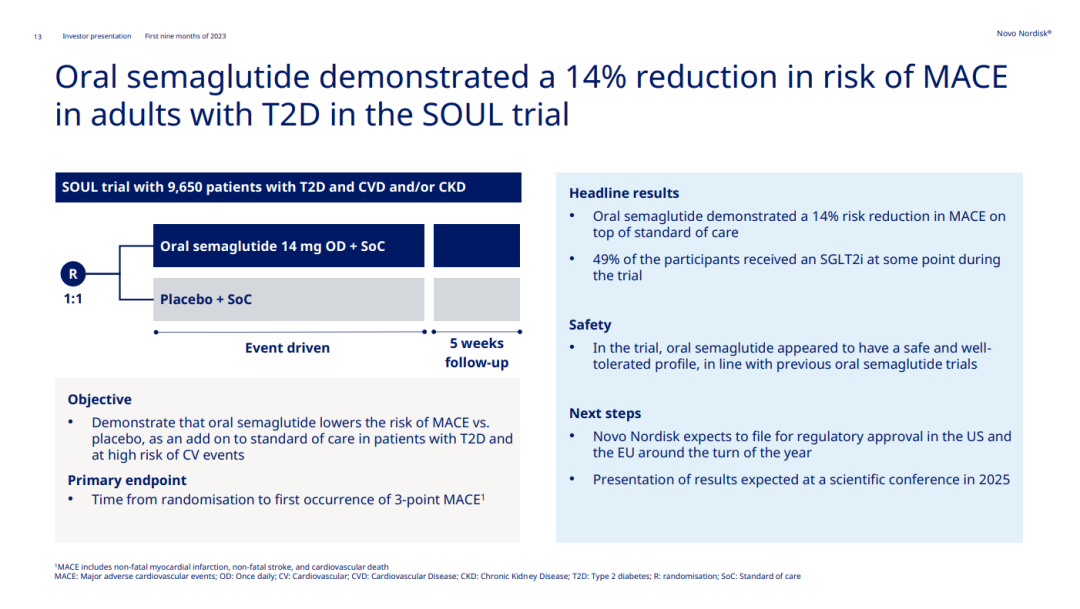

SOUL Cardiovascular Trial Shows Oral Semaglutide Reduced MACE Risk by 14% in Adults with Type 2 Diabetes.

Figure 14. SOUL Trial

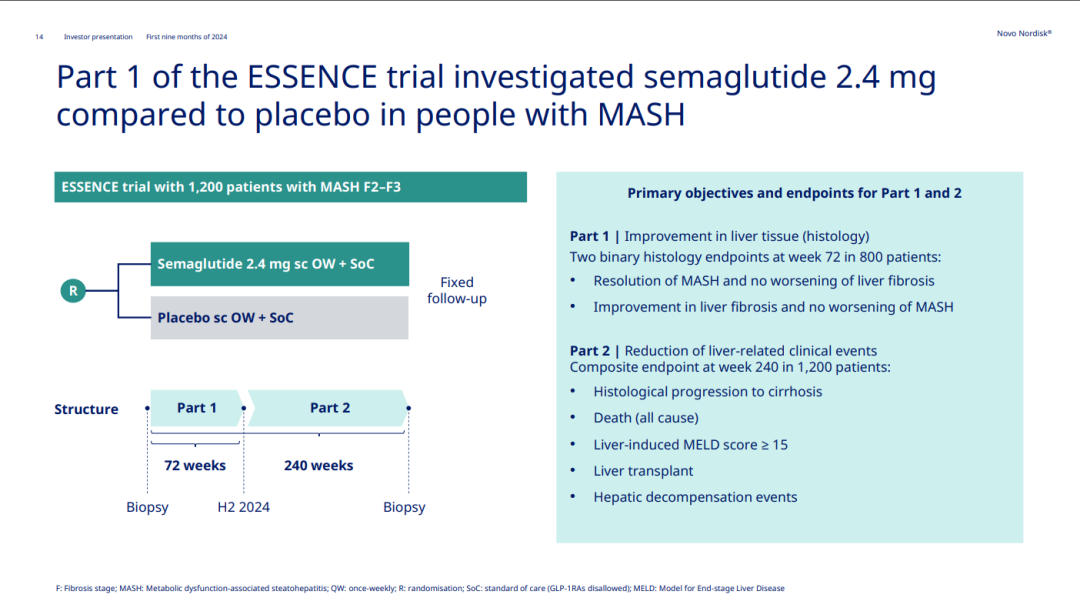

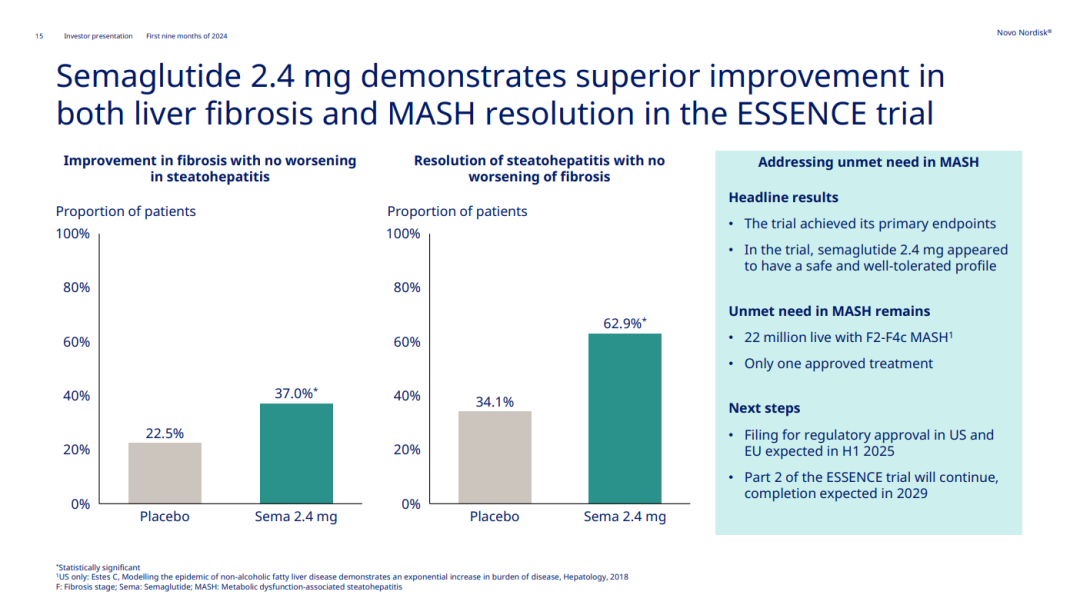

ESSENCE Trial Shows Primary Results of 2.4 mg Semaglutide in Adults with MASH and Liver Fibrosis, Demonstrating Significant Improvements in Liver Fibrosis and MASH Resolution Compared to Placebo.

Figure 15. ESSENCE Trial 1

Figure 16. ESSENCE Trial 2

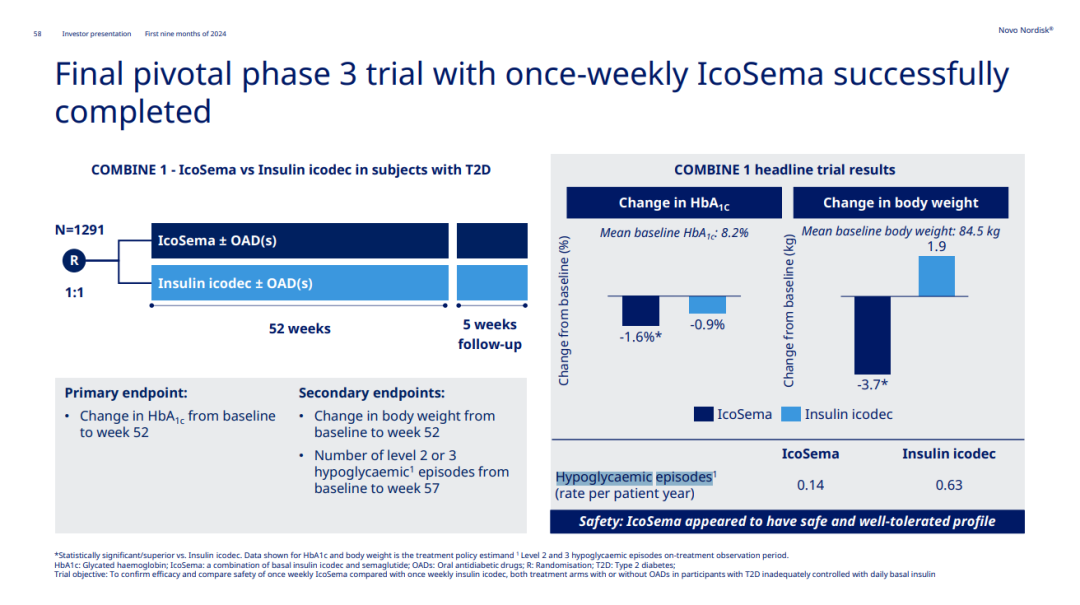

COMBINE 1 Trial Shows: The Blood Sugar Lowering Effect of Icodec Insulin and Semaglutide Combination is Better Than Icodec Insulin Alone, with Hypoglycemia Events as Low as 0.14 Compared to 0.63 for Monotherapy; the Study Also Indicates That Icodec Insulin Does Not Have Weight Loss Effects.

Figure 17. COMBINE 1 Trial

| References

[1] Novo Nordisk.website.

- END -

Flagship Report

Column Recommendation

Peptide Research Society

Biopharmaceuticals · Beauty & Personal Care · Nutrition & Health

Animal Health · Green Agriculture · Biomaterials

Professional Focus | Customer Success | Co-growth