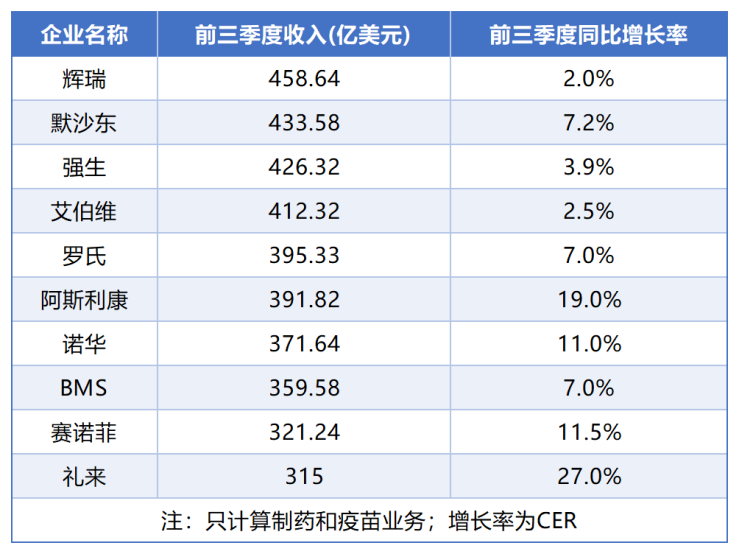

Global Pharma Revenue Top 10 Shakeup: Pfizer Reclaims the Lead, Eli Lilly Surges, GSK Falls Out

GSK

Pharmaceutical R&D Manufacturer

As the third-quarter 2024 financial reports are gradually unveiled, the performance competition among global pharmaceutical giants has once again unfolded, becoming a recent focal point in the industry. Amidst fierce market competition, the rankings of the top 10 global pharmaceutical companies by revenue have undergone another reshuffle.

In the third quarter of 2024, most multinational pharmaceutical companies achieved steady growth in performance driven by the strong sales of innovative products, injecting new vitality into the industry. Among them, Pfizer not only successfully reversed its previous decline in performance with an impressive 32% year-on-year sales increase, making it the fastest-growing multinational pharmaceutical company in the quarter, but also jumped to the top revenue position for the first three quarters of 2024, showcasing its robust recovery and outstanding competitiveness.

At the same time, Eli Lilly also rose to the challenge, successfully surpassing GSK to secure a spot on the TOP10 revenue list for the first three quarters of 2024. Additionally, multinational pharmaceutical companies such as Johnson & Johnson and BMS are struggling to maintain their positions amidst fierce market competition, striving to preserve their market standing.

Looking at major multinational pharmaceutical companies in2024The performance in the third quarter of the year was driven by the rapid uptake of innovative products, effective market expansion, and precise acquisition strategies. With multinational pharmaceutical companies continuously gaining new indications for their products and expanding into emerging markets, these leading companies are expected to maintain steady growth in the future.

However, behind the growth in performance, the intensifying competition in the diabetes and weight-loss drug markets, as well as the impact of generic drugs, cannot be ignored. These challenges will test the innovation capabilities and market adaptability of multinational pharmaceutical companies, adding more uncertainty to their future development path. Nevertheless, the strong performance of multinational pharmaceutical companies in the third quarter has already instilled confidence in the industry and laid the groundwork for future competitive dynamics.

Pfizer Takes the Lead

Lilly's Revenue Surges Significantly

After experiencing a revenue decline in the first quarter and a slight recovery in the second quarter, Pfizer finally made a strong comeback in the third quarter of 2024.

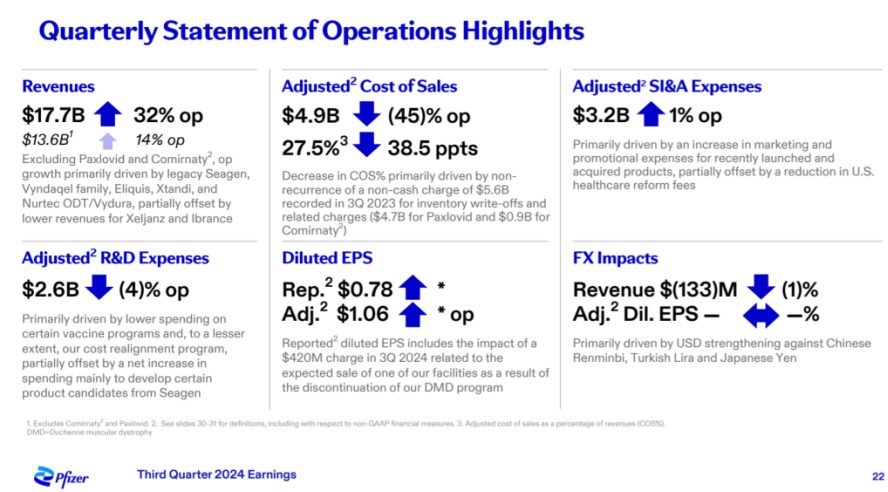

According to the financial report, Pfizer's revenue in the third quarter reached $17.702 billion, a year-on-year increase of 32%, far exceeding the market expectation of $15.08 billion. This made Pfizer the fastest-growing multinational pharmaceutical company in the quarter, breaking the six-month dominance of the two GLP-1 "powerhouses," Eli Lilly and Novo Nordisk. Meanwhile, net profit soared to $4.465 billion, a stark contrast to the net loss of $2.382 billion in the same period last year. Earnings per share were $0.78, and adjusted earnings per share reached $1.06, fully demonstrating the company's strong and robust financial outlook.

Pfizer's performance growth is mainly attributed to the joint contribution of multiple products. Among them, the COVID-19 oral drugPaxlovidRevenue reached in the third quarter27billion dollars, with significant year-on-year growth, mainly due to globalCOVID-19Strong demand in the U.S. during the new wave of the pandemic, along with a one-time contract delivery to the U.S. Strategic National Stockpile100Ten thousand courses of treatment. In addition,ComirnatyVaccines also contributed14Billion USD in revenue, year-on-year growth9%, which is mainly attributed to2024The early approval of the new variant vaccine in the United States led to an early stockpile.

In terms of oncology business, Pfizer has also performed outstandingly. In the third quarter, Pfizer's oncology business grew by 31% year-over-year, partly due to the acquisition of Seagen, a leading company in antibody-drug conjugates, and the efficient operation of the newly established Pfizer Oncology division. In its earnings report, Pfizer also highlighted new research achievements in areas such as breast cancer, genitourinary tumors, hematological malignancies, and thoracic tumors, further solidifying its leadership position in the oncology field.

In addition to the strong growth in performance, Pfizer has also raised its revenue guidance for the full year of 2024: it is expected that the total annual revenue will be between $61 billion and $64 billion, an increase of $1.5 billion compared to the previous guidance. The adjusted earnings per share guidance range has also been raised to $2.75 to $2.95, reflecting Pfizer's continued confidence in its business and its strong performance since the beginning of the year.

In terms of cost control, Pfizer has also achieved significant results. It is expected to realize net cost savings of at least $5.5 billion from previously announced cost-cutting measures, with at least $4 billion anticipated to be achieved by the end of 2024 through cost restructuring plans. Additionally, the first-phase manufacturing optimization plan is projected to save approximately $1.5 billion by the end of 2027.

While revenue highlights were abundant, Pfizer particularly emphasized in its financial report that it would continue to increase investment in R&D. In the first half of 2024, Pfizer's R&D-related expenses amounted to $5.189 billion, a year-on-year increase of 1%. As of July 2024, Pfizer had a total of 113 projects under research globally, covering all stages from Phase I clinical trials to registration submissions, involving multiple fields such as oncology, internal medicine, vaccines, inflammation and immunology, and rare diseases.

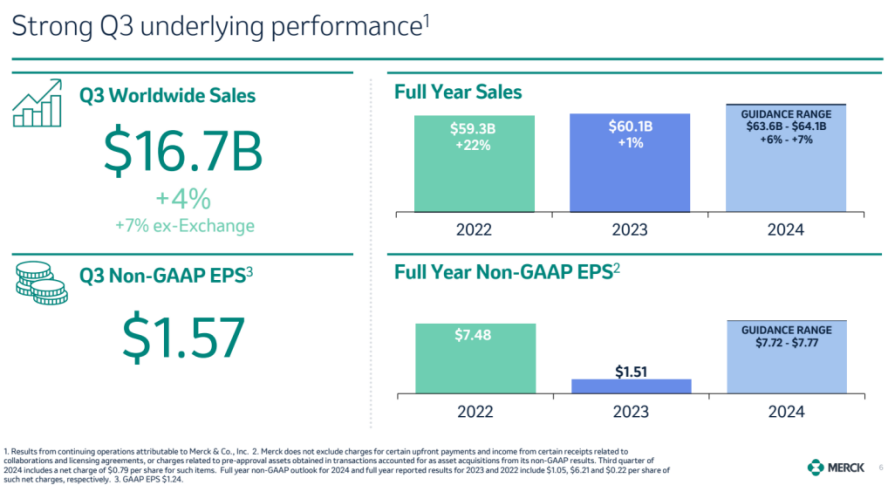

Similarly, Merck also achieved steady growth in the third quarter of 2024. The financial report shows that Merck's total revenue in the third quarter was $16.657 billion, a year-on-year increase of 7%. Among this, pharmaceutical business revenue reached $14.943 billion, growing by 8% year-on-year. Notably, Merck’s revenue from its China operations was $996 million, accounting for 6.7% of global pharmaceutical business revenue. Merck also pointed out that despite the overall good performance of its business, considering the uncertainties in the market environment, it has decided to lower its full-year revenue guidance, with an expected annual revenue between $63.6 billion and $64.1 billion.

Specifically,MSD's flagship productPD-1Monoclonal AntibodyKeytruda(Pembrolizumab, commonly known as“KMedicine”) Continue to maintain a strong growth momentum. In the third quarter,KDrug sales reached74.29Billion USD, year-on-year growth21%In the first three quarters,KThe cumulative sales of the drug have reached216.46Billion USD, year-on-year growth18%MSD expects,KDrug's annual sales in China may exceed290Billion US dollars, and is even expected to exceed300Billion-dollar mark.

Moreover, Merck's 15-valent pneumococcal vaccine Vaxneuvance (V114) also performed well, with revenue reaching $239 million, a year-on-year increase of 13%. Meanwhile, the 21-valent pneumococcal conjugate vaccine Capvaxive (V116), approved in June this year, has also achieved an encouraging market start. However, the demand for Merck’s HPV vaccine in the Chinese market has decreased somewhat, with the sales of Gardasil 9 (9-valent HPV vaccine) in Q3 amounting to $2.306 billion, a year-on-year decrease of 10%.

In the cardiovascular field, Merck's new drug Winrevair has continued its growth momentum since its launch, achieving global sales of $149 million and steadily penetrating the U.S. pulmonary arterial hypertension market. In the third quarter, approximately 1,700 new patients began treatment with Winrevair, bringing the total number of patients treated since the drug’s launch to over 3,700.

Regarding Merck's performance in the third quarter of 2024, analysts believe that despite a slight reduction in the full-year revenue guidance, the strong performance of Keytruda (K药) and the company’s continued investment in R&D still provide solid support for Merck's future development.

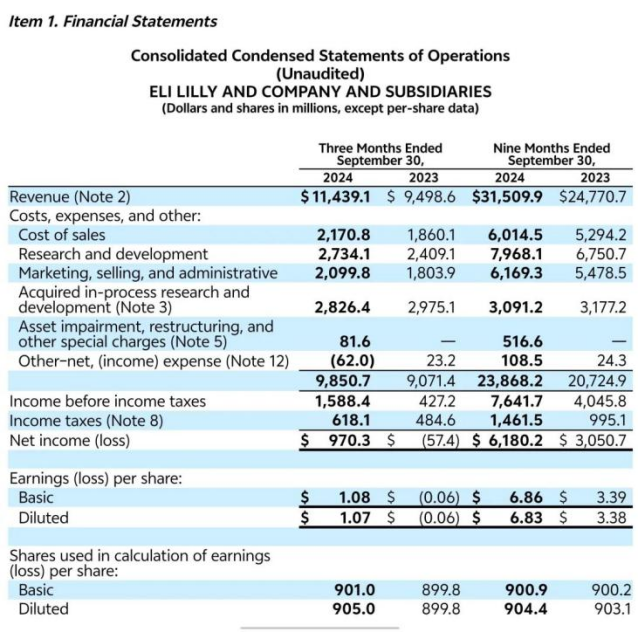

Eli Lilly's financial performance in the third quarter of 2024 was equally remarkable: third-quarter revenue reached $11.44 billion, achieving a 20% year-over-year increase, with a net profit of approximately $970 million. Looking at the first three quarters of 2024, Eli Lilly's total revenue reached $31.5 billion, marking a substantial 27% year-over-year growth, with a net profit of $6.18 billion. This growth was primarily driven by the strong sales performance of several innovative drugs, especially star products like tirzepatide, which continued to gain significant traction in the global market.

As a blockbuster product launched by Eli Lilly in recent years,GIP/GLP-1The receptor dual agonist tirzepatide has gained widespread recognition for its outstanding efficacy in weight loss and diabetes treatment.2024YearIn the first three quarters, the cumulative sales of tirzepatide have reached a high of110billion dollars, not only solidified Eli Lilly's leading position in the diabetes treatment field but also significantly increased its market share in the weight loss sector, becoming the core engine of the company's performance growth.

But Eli Lilly's innovative pace did not stop at tirzepatide. The company has launched innovative drugs in multiple therapeutic areas such as cardiovascular, immunology, and oncology, successfully achieving market entry and scale-up, providing strong support for the company's performance growth.

In addition to Pfizer, Eli Lilly, and Merck, multinational pharmaceutical companies such as Novartis, Sanofi, and AstraZeneca also achieved double-digit growth in the first three quarters. Industry insiders noted that unlike the widespread trend of weak growth year-on-year last year, multinational pharmaceutical companies this year seem to be emerging from a growth slump, showing strong momentum for development. The revenue growth of these companies is mainly driven by the continued increase in sales of innovative drugs, market expansion, and effective cost control measures.

Johnson & Johnson, AbbVie Secure Positions

GSK Regrets Falling Out of the Top Ten

In the third quarter of 2024, the competitive landscape of the global pharmaceuticals industry once again presented a diversified trend.Despite the fact that most companies have achieved revenue growth, single-digit growth and the subpar performance of some pharmaceutical enterprises have also drawn widespread attention and in-depth discussion in the industry.Among them, Johnson & Johnson, AbbVie, and BMS secured their positions in the top ten with slight growth, while GSK was unfortunately edged out of the list by Eli Lilly, a change that undoubtedly highlights the fierce competition in the industry.

Recently, Johnson & Johnson announced its financial report for the first three quarters of 2024, revealing the company's latest performance dynamics in the pharmaceutical field. Despite a slight slowdown in overall growth, Johnson & Johnson has still demonstrated considerable strength in its innovative pharmaceuticals business.

According to the financial report,Johnson & Johnson ThirdQuarterly sales were225Billion USD, year-on-year growth5.2%. By business division, pharmaceutical sales146Billion USD, year-on-year growth4.9%. Medical Device Business Sales79USD billion, year-on-year growth5.8%Among them, core products such as Daratumumab, Apalutamide, and Guselkumab all achieved double-digit growth, demonstrating strong market competitiveness and patient recognition.

Notably, the BCMA CAR-T therapy Cilta-cel, developed in collaboration with Legend Biotech, achieved a staggering $629 million in sales in the third quarter, representing an 84.3% year-over-year increase. This remarkable performance undoubtedly added significant momentum to Johnson & Johnson's oncology business. Meanwhile, the EGFR bispecific antibody Amivantamab is fiercely competing with AstraZeneca's Osimertinib in the market, showcasing Johnson & Johnson's profound expertise in the field of cancer treatment.

However, behind the overall positive performance, Johnson & Johnson also faces some challenges. Its growth rate for the first three quarters was only 3.9% (CER), and the growth rate of its proud autoimmune business has dropped to 1%. The core product, ustekinumab, although still maintaining sales of $8 billion, has shown a negative growth of 1.2%, with sales in the third quarter declining by 6.6%. This change undoubtedly sounds an alarm for Johnson & Johnson, reminding it that it needs to work harder to find new growth points in the autoimmune field.

In sharp contrast, Johnson & Johnson's oncology business has emerged as a standout, becoming a new engine for the company’s performance growth. In the first three quarters, the overall sales of the oncology business reached $15.284 billion, with a growth rate of 17.2%. Apart from Ciltacabtagene Autoleucel, developed in collaboration with Legend Biotech, Johnson & Johnson's long-standing product Daratumumab also performed exceptionally well, achieving sales of $8.586 billion and a growth rate of 19.3%. Additionally, products in the oncology pipeline such as ERLEADA and Amivantamab have also achieved rapid growth, injecting new vitality into Johnson & Johnson's oncology business.

Notably, amid the wave of BD activities by multinational pharmaceutical companies such as Merck and AstraZeneca (AZ), Johnson & Johnson's ADC strategy stands out as particularly remarkable. As early as 2022, Johnson & Johnson collaborated with biotech firms like Mersana Therapeutics and DAC Biotech to jointly develop novel-targeted ADCs. This year, Johnson & Johnson made a multibillion-dollar acquisition of Ambrx, successfully gaining several ADC products with first-in-clinical potential. These moves not only expanded Johnson & Johnson’s product pipeline but also laid a solid foundation for its competitive edge in the future pharmaceutical market.

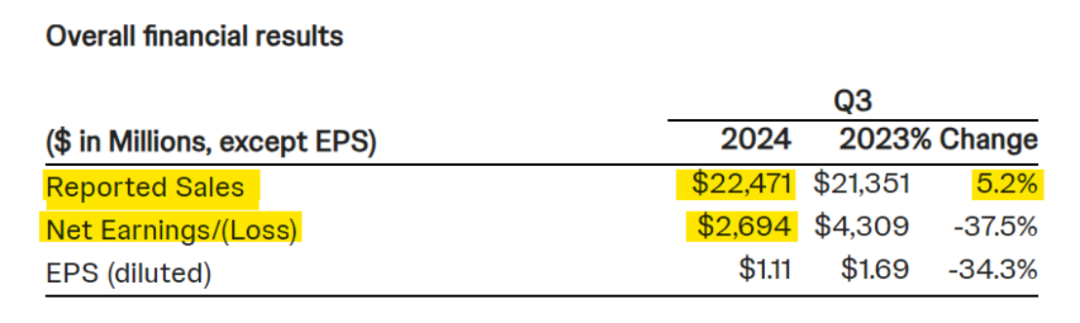

Similar to Johnson & Johnson, AbbVie's third-quarter financial report also demonstrated its resilience. The report shows that AbbVie’s revenue for the first three quarters reached $41.232 billion, a slight year-on-year increase of about 3%. In the third quarter, the company achieved total revenue of $14.460 billion, representing a year-on-year growth of 3.83%. However, it is worth noting that AbbVie's net profit attributable to shareholders in this quarter was $1.551 billion, a year-on-year decrease of 12.22%. Behind this change lies the main challenge currently faced by AbbVie.

First and foremost is AbbVie's star productHumira(The patent cliff effect of Adalimumab). With the influx of generic drugs,HumiraThe market share and sales volume have suffered a serious impact. The financial report data shows,HumiraRevenue in the third quarter was only22.27Billion USD,同比下降37.2%. This significant decline has put considerable pressure on AbbVie's overall performance and is directly reflected in the drop in net profit attributable to shareholders.

In addition to the challenges posed by Humira, the uncertainty of the global economic environment and the overall volatility of the healthcare industry have also impacted AbbVie's performance. Despite AbbVie maintaining growth momentum in multiple areas, changes in the overall market environment still present significant challenges to its profitability.

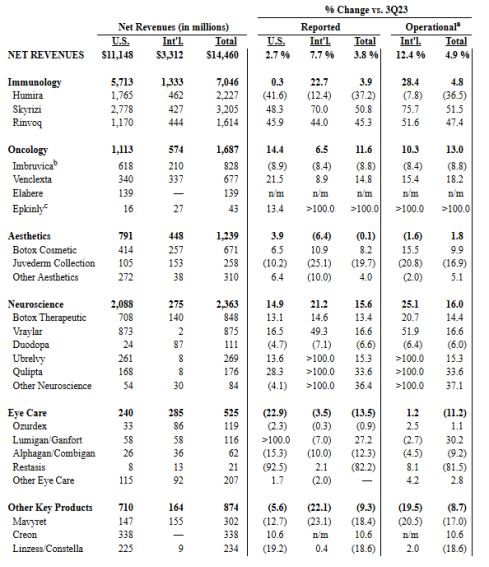

However, in the face of these challenges, AbbVie has not stood still. On the contrary, AbbVie's growth in new business areas has brought positive signals to the market. The financial report shows that Skyrizi (risankizumab) and Rinvoq (upadacitinib), as successors to Humira, are rising at an astonishing rate. Skyrizi's sales in the third quarter reached $3.205 billion, a year-on-year increase of 50.8%, with annual revenue expected to exceed $11 billion. Meanwhile, Rinvoq also performed strongly, with third-quarter sales of $1.614 billion, a year-on-year increase of 45.3%, and annual revenue projected to surpass $5 billion. The excellent performance of these two products not only partially offset the gap caused by the decline in Humira sales but also became an important support point for AbbVie's performance.

Moreover, AbbVie has made significant progress in the fields of oncology and neuroscience. The net revenue of the oncology drug Venclexta (Venetoclax) reached $677 million in the third quarter, representing a year-over-year increase of 14.8%, demonstrating strong market potential. In the field of neuroscience, AbbVie further expanded its product portfolio through the acquisition of Cerevel, showing new growth potential in therapeutic areas such as schizophrenia and Parkinson's disease, laying a solid foundation for the company’s future development.

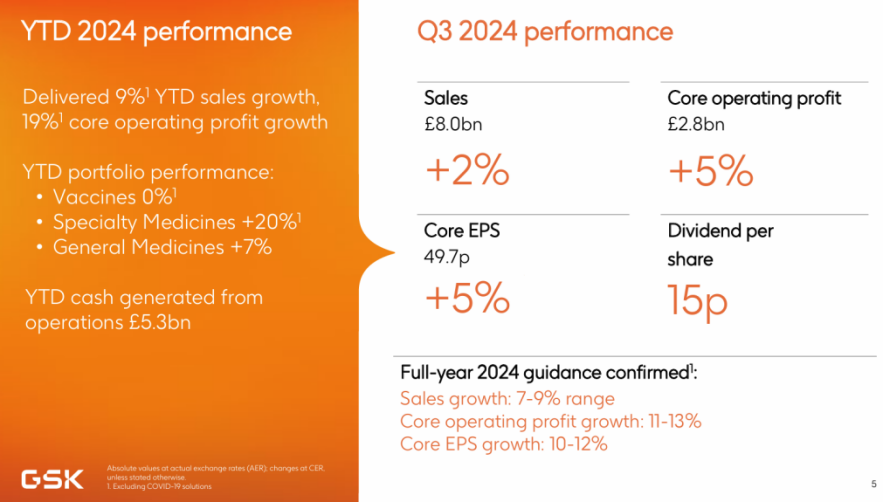

Compared with multinational pharmaceutical companies experiencing single-digit growth, the decline in GSK's performance and its drop out of the top ten global pharmaceutical companies by revenue is regrettable. In the third quarter of 2024, GSK's revenue was £8.012 billion (approximately $10.2 billion), compared to £8.147 billion in the same period last year. The quarterly operating profit was £189 million, compared to £1.949 billion in the same period last year. The net loss attributable to shareholders for the quarter was £58 million, compared to a net profit of £1.464 billion in the same period last year.

It is reported that,Performance Decline“Culprit”Directly PointingGSKTwo Key VaccinesProduct——Respiratory Syncytial Virus (RSV)VaccineArexvyAnd Shingles VaccineShingrix. According to the financial report,ArexvyVaccine Sales in Q3 Plummet Year-on-Year74%To1.88Billion pounds (2.44Billion US dollars), andShingrixVaccine sales also declined.10%To7.39Billion pounds (9.56billion dollars). The sluggish sales of these two vaccines have impactedGSKhas severely impacted overall performance.

GSK CEO Emma Walmsley admitted that the third quarter was "challenging" for GSK, especially in the vaccine sector. The decline in vaccine sales was due to a variety of complex reasons: on one hand, the U.S. Centers for Disease Control and Prevention narrowed its immunization recommendations, leading to a significant drop in demand for the Arexvy vaccine; on the other hand, the prioritization of COVID-19 vaccines had a crowding-out effect on RSV vaccine uptake; furthermore, the seasonal low incidence of RSV also exacerbated the difficulties in vaccine sales.

Despite the poor performance of the vaccine sector, GSK's specialty medicines segment has emerged as a standout, becoming a key pillar for the company’s performance. In the third quarter, sales in the specialty medicines division (covering oncology, HIV, and respiratory/immunology) increased by 19%, with oncology sales surging 94% year-on-year, marking it as a major highlight. This clearly demonstrates that GSK's investments and innovations in the specialty medicines field are gradually paying off.

However, the sluggish vaccine sales still caused GSK to be overtaken by its competitor Eli Lilly in terms of revenue for the first three quarters, missing out on a spot in the top ten global pharmaceutical companies by revenue. This shift not only reflects the intense competition within the global pharmaceutical industry but also highlights the dynamic changes in market structure.

GSK States Continued Investment and Innovation in Specialty Medicines, Aiming for Breakthroughs in Oncology and HIV. Meanwhile, GSK Is Actively Pursuing Recovery Opportunities in Vaccines, Expressing Confidence in Achieving Over £3 Billion Peak Sales for the Arexvy Vaccine and Planning to Launch More Innovative Vaccine Products in the Coming Years. Additionally, GSK Is Expanding Its Collaboration Network, Recently Partnering with Companies Such as BioVersys, Wave Life Sciences, and Pfizer to Advance New Drug Development and Market Expansion. These Collaborations Will Not Only Broaden GSK's Product Portfolio but Also Enhance Its Market Competitiveness.

Overall, the performance of the global pharmaceutical industry in the third quarter of 2024 showed a diversified trend, with some underperforming companies drawing widespread attention and deep reflection within the industry. Facing the current competitive landscape of the global pharmaceutical market and future development opportunities, pharmaceutical companies need to continuously strengthen their innovation capabilities, seek international cooperation and merger integration opportunities, and enhance marketing and channel development to ensure long-term stable growth. Against this backdrop, the performance of companies such as Pfizer, Johnson & Johnson, and AbbVie has undoubtedly set an example for the industry, while adjustments and transformations by companies like GSK have also provided valuable insights.

Editor: Vanilla

www.yyjjb.com.cn

Insight into Industry Trends

"Pharmaceutical Economy News"

Academic Official Account

Focus on the Frontier of Oncology Academia

Terminal Official Account