2026 H1 Licensing Landscape: China Secures 8 of the Top 10 Global Licensing Deals

CSPC

Developer of finished drugs and active pharmaceutical ingredients

Hengrui Pharma

Innovative and High-Quality Pharmaceutical Developer

Innovent

High-end Biologics Developer

RemeGen

Biological New Drug Developer

Ribo Life Science

Small Nucleic Acid Drug Developer

Haisco

New Drug Research and Development, Production, and Sales

InSilico Medicine

Intelligent Drug Development Platform and New Drug Research and Development Provider

10 major global pharma license-out deals, 8 Chinese sellers. Unbeknownst to many, Chinese innovative drugs have become a core force in global pharmaceutical innovation.

According to VBInsight statistics, the number of licensing deals for innovative drugs in China in the first half of 2026 has reached 71% of the total number of transactions in 2025, approximately 240 deals; the total transaction amount is approaching the full-year 2025 figure of $135.655 billion, reaching $106.3 billion.

In the first half of the year, total upfront payments for licensing transactions reached $6.158 billion, accounting for 5.8% of the total transaction value—a steady increase from the 5.2% recorded for the full year 2025. Buyers, primarily overseas pharmaceutical companies, have demonstrated steadily growing recognition of and willingness to pay for Chinese innovative assets.

The most striking aspect is that, among the top 10 global licensing deals in the first half of 2026, eight involved Chinese companies, all as sellers. Prior to this, eight of the top 10 global pharmaceutical license-out deals by total value in 2025 also originated from China.

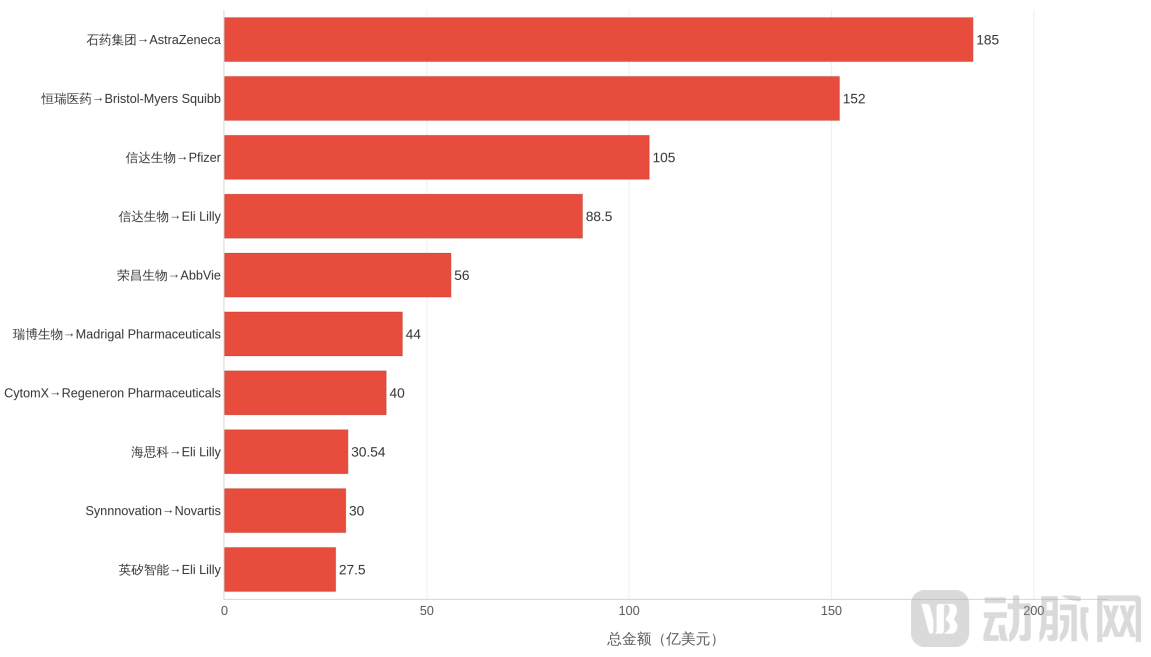

Top 10 Global Licensing Deals in H1 2026

From 2025 to 2026, Chinese innovative drugs secured eight of the top ten global licensing deals for two consecutive years. This serves as a testament to the strength of China's innovative pharmaceutical industry as it transitions from "following" and "keeping pace" to "leading the way."

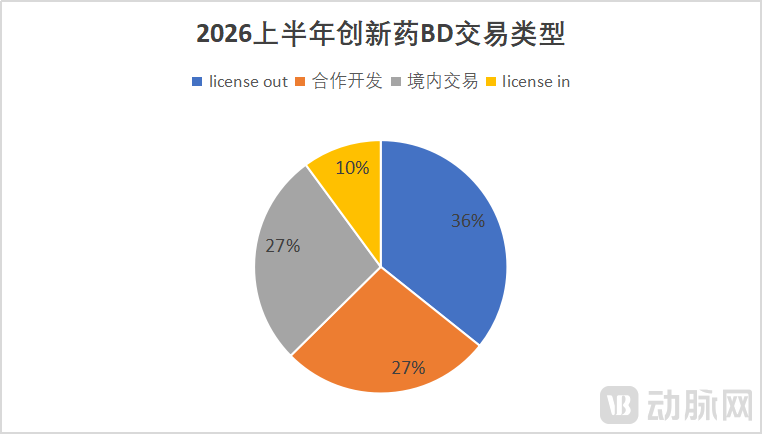

In the first half of 2026, there were approximately 240 licensing deals in China's innovative drug sector, encompassing four types: outbound licensing, domestic deals, collaborations, and inbound licensing from overseas.

Among these, license-out deals were the absolute mainstream, with 85 transactions completed, accounting for 35.5% of the total number of transactions. There were 65 transactions between domestic companies, 64 collaborative development deals, and 24 license-in deals.

Of the 64 collaborative development transactions, domestic enterprises were the dominant force on the seller side, accounting for 59 deals (92%), highlighting China's leading position in the supply of innovative technologies. Buyers such as BASF, HLFM, Ribo Life Science, and Qilu Pharmaceutical collaborated with domestic AI drug discovery companies to leverage their AI technologies for enhancing R&D efficiency and success rates.

From the perspective of transaction amount, in the first half of 2026, the total value of licensing transactions for innovative drugs in China amounted to $106.3 billion, with the disclosed total value of outbound licensing transactions reaching $100.4 billion. Three deals exceeded $10 billion in total value: CSPC Pharmaceutical Group and AstraZeneca's $18.5 billion strategic collaboration on long-acting peptides; Hengrui Medicine and BMS's $15.2 billion multi-area collaborative development; and Innovent Biologics and Pfizer's $10.5 billion licensing deal for oncology pipeline assets.

Top 10 Domestic Licensing Deals by Value in China's Innovative Drug Sector

In addition, the total value of the top 10 licensing deals for innovative drugs in China reached $73.914 billion, accounting for 69.5% of the total amount. The concentration effect is very obvious. Meanwhile, the 230 licensing transactions outside the top ten had a combined transaction value of approximately $32.38 billion, with an average of $140 million per deal, indicating that licensing projects among small and mid-sized innovative pharmaceutical companies are generally smaller in scale.

In terms of upfront payments, the total amount disclosed in the first half of the year reached $6.158 billion, accounting for 5.8% of the overall transaction value, marking a steady increase from the 5.2% upfront payment ratio recorded for the full year 2025.

Notably, the upfront payment for the transaction between CSPC Pharmaceutical Group and AstraZeneca reached as high as $1.2 billion, setting a new record in recent years for upfront payments in the overseas licensing of Chinese innovative drugs. The upfront payments for the deals between RemeGen and AbbVie, and between Innovent Biologics and Pfizer, also each amounted to $650 million.

The rise in absolute upfront payments and payment ratios confirms the continuously improving bargaining power of Chinese innovative drug assets.

From the perspective of clinical stage distribution, licensing transactions in the first half of 2026 exhibited a "bimodal activity" pattern. Marketed products and preclinical projects collectively accounted for over 60%, while clinical projects in other stages (such as Phase I/II and Phase III) comprised nearly 40%.

This distribution pattern reflects two mainstream licensing logics:

First, the overseas commercial licensing of mature products, i.e., the "fruit-picking" model, represented by the Rovadicitinib deal between Sino Biopharmaceutical and Sanofi, the Felzartamab deal between TJ Bio and Biogen, and the Serplulimab injection deal between Henlius Biotech and Eisai, with total transaction values of $1.53 billion, $850 million, and $388 million, respectively.

Second, the bulk licensing of early-stage platforms or pipeline portfolios, i.e., the "sowing seeds" model, exemplified by CSPC Pharmaceutical Group's partnership with AstraZeneca on a peptide platform and Innovent Biologics' bundled licensing of 12 early-stage oncology projects to Pfizer.

Notably, platform-based collaborations and multi-project bundled licensing are becoming the dominant form of large-scale transactions. Among the top five deals in the first half of the year, four were multi-asset or platform-based collaborations, while the proportion of large-scale single-product transactions declined. This indicates that MNCs' procurement logic is shifting from "acquiring blockbusters" to "establishing a long-term pipeline of innovative assets." By forging deep partnerships with Chinese biotech firms, MNCs are continuously securing early-stage innovative assets to supplement their own R&D pipelines.

Amid the industry backdrop of the U.S. FDA's proposed restrictions on the use of Chinese clinical data in 2026, this structural shift in the clinical development phase carries profound strategic implications. In April 2026, the U.S. House Appropriations Committee introduced new regulations requiring the FDA to limit its reliance on clinical trial data originating from China when reviewing IND applications and marketing authorization applications for new drugs. The market widely believes that this move will impact the global expansion of innovative drugs developed in China.

As Das Kapital states, once there is adequate profit, capital becomes emboldened.

In China, leveraging policy support, talent pools, and supporting infrastructure, the comprehensive R&D costs for projects with identical targets are 30%–50% lower than in Europe and the United States, while clinical recruitment speed and early target validation efficiency have increased by more than 50%. "Cost savings translate directly into profits." Therefore, driven by the pursuit of lower costs and higher efficiency, overseas capital continues to increase its investment in licensing for Chinese innovative drug assets, with licensing focus increasingly shifting toward preclinical and early-stage projects.

In the long run, the shift of licensing projects toward earlier stages signifies that Chinese pharmaceutical companies will evolve from "product export" to "export of innovation capabilities." They will deliver value by leveraging source innovation capabilities and foundational technology platforms as their core, thereby integrating more deeply into the global innovative drug R&D ecosystem.

In the first half of 2026, the AI drug discovery sector emerged as a dark horse, driving incremental growth in the licensing market.

In the first half of the year, Chinese AI-driven drug discovery companies completed a total of seven outbound licensing transactions. As a leader in the AI pharmaceutical sector, Insilico Medicine finalized five major overseas licensing deals during this period, partnering with top-tier global MNCs including Eli Lilly, Servier, SK Biopharmaceuticals, and Takeda. The total potential value of these collaborations approaches $7 billion, covering multiple high-profile therapeutic areas such as oncology, neuroimmunology, anti-aging, and metabolic diseases. This makes Insilico Medicine the company with the highest transaction frequency and the most prestigious partnerships in the global AI drug discovery field during the first half of the year.

In addition to Insilico Medicine, other leading Chinese AI drug discovery companies such as XtalPi and METiS TechBio have also continued to exert their influence, successively closing multiple overseas technology collaborations and platform licensing deals. For instance, XtalPi entered into a strategic AI drug discovery partnership worth over $400 million with a renowned international pharmaceutical company, focusing on the development of innovative small molecules targeting GPCR targets.

From the perspective of transaction models, licensing in the AI drug discovery sector during the first half of 2026 primarily focused on technology platform exports and co-building AI-driven R&D systems. Unlike the overseas expansion of single-asset pipelines typical for small molecules and antibody-based innovative drugs, Chinese AI pharmaceutical companies centered their collaborations on exporting AI-powered drug discovery platforms, multimodal data systems, intelligent target screening, and automated lead optimization capabilities. These efforts aim to help MNCs address industry pain points such as prolonged traditional R&D cycles, difficulties in target validation, and high failure rates.

For example, Insilico Medicine's AI foundation model for longevity science and its intelligent small-molecule R&D system, as well as the AI-driven peptide drug discovery platform under CSPC Pharmaceutical Group that has attracted AstraZeneca's interest, are all typical representatives of the "selling technology, selling capabilities, and selling systems" business model.

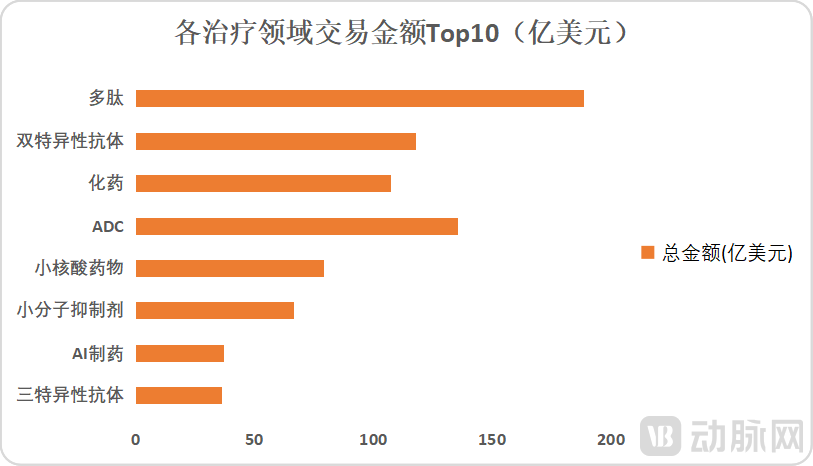

From the perspective of licensing, sectors such as peptides, bispecific antibodies, ADCs, small nucleic acid drugs, and immunotherapy are experiencing significant momentum, with deal closures also occurring in emerging fields like cell and gene therapy. Notably, the siRNA therapy transaction between Ribo Life Science and Madrigal Pharmaceuticals, with a total value of $4.4 billion, has become a benchmark case in the field of nucleic acid therapeutics. Additionally, the licensing agreement for AAV capsid technology between VectorBuilder and Ikarovec reached a scale of $1 billion, highlighting the growing value of platform technologies in gene therapy.

Overall, the landscape of licensing deals for innovative drugs in China is continuously expanding, evolving from a singular structure dominated by oncology into a multidimensional framework covering multiple modalities and therapeutic areas.

In the first half of 2026, the competitive landscape for high-end licensing deals in global innovative drugs became clearly defined. Among the Top 10 blockbuster licensing deals, which comprehensively cover all pharmaceutical companies worldwide, Chinese enterprises strongly secured eight spots, while the remaining two were claimed by leading overseas MNCs.

From the buyer's perspective, Eli Lilly was the most active overseas acquirer in the first half of the year, completing four licensing deals for innovative Chinese drugs, spanning multiple areas including small molecules and AI-driven drug discovery. Other MNCs, such as Novartis, AbbVie, GSK, and Boehringer Ingelheim, each closed more than two deals. Meanwhile, industry giants like AstraZeneca, BMS, and Pfizer distinguished themselves by deal size, ranking top three in terms of individual transaction value.

Below is the complete list of the top 10 global licensing deals in the first half of 2026, including eight benchmark deals from China and two major overseas deals:

Total Transaction Value: $18.5 billion; Upfront Payment: $1.2 billion

On January 30, 2026, CSPC Pharmaceutical Group and AstraZeneca announced a strategic collaboration with a total value of up to $18.5 billion, making it the largest global licensing deal by value in the first half of the year. The $1.2 billion upfront payment also set a new record for the highest upfront payment in recent years for Chinese innovative drugs going global.

Under the agreement, both parties will engage in comprehensive strategic collaboration in the discovery of innovative peptide molecules and the development of long-acting delivery products. In addition to continuously advancing its existing preclinical pipeline of long-acting peptides, CSPC Pharmaceutical Group will also discover and develop other innovative long-acting peptide products for AstraZeneca.

Total Transaction Value: $15.2 billion; Upfront Payment: $600 million

On May 12, 2026, Hengrui Medicine and Bristol Myers Squibb (BMS) announced a landmark strategic collaboration with a total transaction value of $15.2 billion. BMS secured exclusive overseas rights to four oncology and hematology assets from Hengrui, as well as five innovative co-developed programs leveraging Hengrui's platform. In return, Hengrui obtained exclusive rights to four immunology assets from BMS within the Greater China region.

This transaction has evolved from the previous "asset pipeline sale" to an "exchange of R&D capabilities."

Total Transaction Value: $10.5 billion; Upfront Payment: $650 million

On May 29, 2026, Innovent Biologics and Pfizer entered into a collaboration valued at up to $10.5 billion, covering 12 early-stage innovative oncology drug projects. These include eight early-stage assets from Innovent's proprietary pipeline and four entirely new projects proposed by Pfizer, spanning cutting-edge areas such as novel payload ADCs and differentiated multispecific antibodies. The two parties will adopt a tiered rights model for global development and commercialization.

The scale of 12 projects signifies that Pfizer effectively regards Innovent Biologics as a key external supplier for its early-stage oncology pipeline.

Total Transaction Value: $8.85 billion; Upfront Payment: $350 million

On February 8, 2026, Innovent Biologics and Eli Lilly once again joined forces to reach a collaboration agreement on innovative drugs in the fields of oncology and immunology, with a total transaction value of $8.85 billion. This marks another deep partnership between the two companies following their collaboration on sintilimab, and represents the second mega licensing deal completed by Innovent in the first half of the year.

Securing two multi-billion-dollar deals consecutively within six months has made Innovent Biologics one of the biggest winners in the licensing market in the first half of the year.

Total Transaction Value: $5.6 billion; Upfront Payment: $650 million

On January 12, 2026, RemeGen and AbbVie reached a global exclusive licensing agreement for RC148, with a total transaction value of $5.6 billion and an upfront payment of $650 million. RC148 is a novel bispecific antibody drug independently developed by RemeGen that targets PD-1 and VEGF, aiming to simultaneously activate anti-tumor immune responses and inhibit tumor angiogenesis.

RC148 was sold for a high price of $5.6 billion during its Phase II clinical stage, achieving value realization.

Total Transaction Value: $4.4 billion; Upfront Payment: $60 million

On February 11, 2026, Ribo Life Science entered into a collaboration with Madrigal Pharmaceuticals, granting the latter an exclusive global license to leverage Ribo Life Science's RiboGalSTAR and siRNA chemical modification platforms for the development of preclinical siRNA assets targeting MASH. The total value of the transaction amounts to $4.4 billion.

This transaction represents another major overseas licensing deal in China's nucleic acid drug sector to date, holding significant benchmarking importance for the industry.

Total Transaction Value: $3.054 billion; Upfront Payment: $87 million

On June 1, 2026, Haisco Pharmaceutical entered into a collaboration with Eli Lilly to conduct candidate drug discovery and early-stage R&D leveraging Haisco's small-molecule innovation technology platform, while Eli Lilly will be responsible for subsequent IND applications, clinical development, and commercialization. The partnership covers up to five small-molecule innovative drug projects, with a total potential value of $3.054 billion.

Haisco Pharmaceutical has emerged as a dark horse in the licensing market during the first half of the year, completing a total of four outbound licensing deals with partners including MNCs such as Eli Lilly and AbbVie.

Insilico Medicine is the benchmark enterprise in the global AI-driven drug discovery licensing sector in the first half of 2026. Within six months, it successfully closed five high-quality overseas licensing deals, with a cumulative potential collaboration value nearing $7 billion. Its partnership portfolio covers top-tier global pharmaceutical companies including Eli Lilly, Servier, SK Biopharmaceutics, and Takeda Pharmaceutical, ranking first among global AI drug discovery companies in both transaction frequency and deal size.

The $2.5 billion SK Biopharm collaboration project featured on this list focuses on AI-driven small-molecule drug development in the field of neuroimmunological diseases. Leveraging Insilico Medicine's end-to-end AI drug discovery platform, it achieves intelligent acceleration across the entire chain—from target identification and molecular design to druggability validation—significantly reducing R&D costs and the risk of failure.

Reviewing the licensing market in the first half of 2026, three core trends clearly define the new characteristics of China's innovative drug licensing 2.0 era.

First, large-scale transactions have surged in a concentrated manner, significantly driving up valuations and further strengthening market concentration. In just the first half of 2026, the total transaction value reached $106.3 billion, approaching the historical high of $135.655 billion recorded for the full year of 2025. This growth was primarily driven by the batch closure of major deals valued at over $10 billion and $5 billion.

Compared to 2025, the first half of this year witnessed a higher density of large-scale transactions and greater value per individual deal, thoroughly achieving the transition from "volume growth" to "value expansion."

Meanwhile, the competitive advantage of industry leaders continues to widen. A small number of leading pharmaceutical companies, through platform-based and bundled mega-deals, account for the majority of transaction volume in the sector. Resources and capital are increasingly concentrating in these top-tier enterprises that possess core technologies and platform capabilities.

Second, AI-driven drug discovery is leading the upgrade of technological modalities, with emerging sectors fully realizing their value. The most significant industrial transformation in the first half of 2026 has been the elevation of AI-driven drug discovery to a core pillar supporting the global expansion of innovative drugs. Beyond AI-driven drug discovery, the proportion of licensing transactions in emerging technical fields such as small nucleic acid drugs, gene therapy, and peptides is rapidly increasing.

Third, the transaction structure continues to be optimized, and a new pattern dominated by Chinese technologies with global synergy has taken shape. From the perspective of transaction structures, license-out deals continue to solidify their mainstream position, while co-development models are rapidly rising. Notably, in the co-development arena, technology output is entirely led by Chinese enterprises, with overseas companies playing more supportive roles in capital provision and commercialization synergy. As a result, Chinese pharmaceutical companies have completely shed the label of mere "pipeline suppliers."

The upfront payment ratio increased from 5.2% in 2025 to 5.8%, while asset premium capability and transaction quality steadily improved. Coupled with the widespread adoption of deep collaboration models such as bidirectional licensing, co-development, and profit-sharing, Chinese innovative drugs have achieved a qualitative leap in their voice and participation within the global innovation value chain, officially entering the mature "licensing 2.0" phase characterized by "strategic symbiosis and shared value."

Notably, a significant volume of licensing transactions in the first half of the year were concentrated in the preclinical and early clinical stages. While this reflects MNCs' recognition of China's early-stage innovation capabilities, it also implies a relatively higher failure rate for these traded assets. As licensing deals for early-stage projects increase, the industry may see more instances of "deal reversals" or project terminations in the coming years. The industry should view the growth in licensing deal volume and value rationally, placing greater emphasis on the ultimate success rates and value realization of the transacted assets.

Looking ahead to the second half of 2026, the momentum in licensing transactions for China's innovative drugs is highly likely to continue. The value proposition of licensing deals will further deepen. New models such as platform-based collaborations, technology licensing, and co-development will become more prevalent, enhancing Chinese companies' participation and influence in the global innovation value chain.