Sinopharm Biotech Strikes Twice in One Day: $1.9B Out-Licensing Deal with AstraZeneca and In-Licensing of GSK's Blockbuster Respiratory Portfolio Ignites China's $10B+ Respiratory Market

Sino Biopharm

Pharmaceutical R&D Developer

AstraZeneca

Pharmaceutical Technology Research and Development Provider

GSK

Pharmaceutical R&D Manufacturer

On July 8, Sino Biopharm dropped two blockbuster drugs in the respiratory therapeutic area.

First,TQC3721, an Independently Developed Innovative Drug for COPD(PDE3/4 Inhibitors)Up to $1.9 billion in total authorization granted to AstraZeneca, with a $200 million upfront payment received immediately.

Second,Strategic cooperation with GSK further deepened, securing two global blockbuster respiratory products—Fluticasone Furoate/Umeclidinium/Vilanterol Inhalation Powder(Trelegy)、Umeclidinium Bromide and Vilanterol Inhalation Powder(Olezexin)exclusive commercialization rights in mainland China.

Source of screenshot: Announcement by Sino Biopharmaceutical Co., Ltd.

Within a single day, one in-license and one out-license. With just two outbound licensing deals this year, the combined upfront payments have exceeded RMB 2 billion.

China’s $10 Billion Respiratory Market: The Stage Is Set, and a Market Leader Is Poised to Emerge.

01

On the Billion-Dollar Table, Sino Biopharm Plays an Ace Card

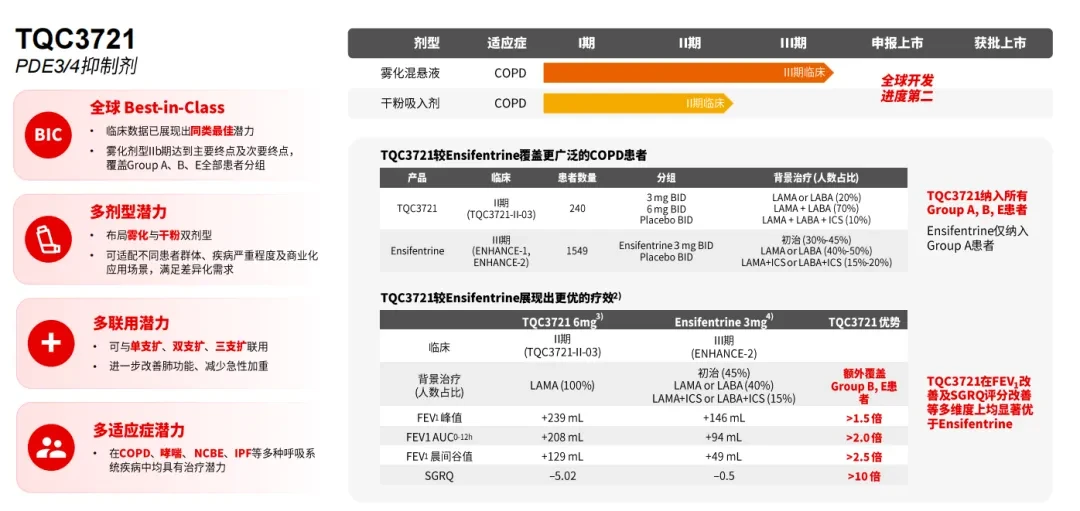

The announcement stated that Sino Biopharm will grant AstraZeneca the rights to develop, manufacture, and commercialize in regions outside China.TQC3721exclusive license. AstraZeneca will also obtain the global (including China) exclusive license for specific development programs of TQC3721. Sino Biopharm is entitled to a $200 million upfront payment, as well as up to $1.7 billion in potential development, regulatory, and sales milestone payments, along with tiered royalties at high double-digit percentages.

PDE3/4 inhibitors represent the first innovative inhaled formulation in the COPD field in the past two decades, with a global market potential reaching tens of billions of yuan. In China, the inhaled formulation sector is equally promising—sales across all terminal hospital markets exceeded RMB 25 billion in 2025.

Source: Menet Pharmaceutical Full-Terminal Hospital Sales Database (Check Data. Find Menet)

Last yearIn July, Merck & Co.$10 billionAcquisitionVerona secured the global first-in-class PDE3/4 inhibitor Ensifentrine, instantly igniting fervor in the therapeutic arena. Subsequently, Hengrui Medicine and HaiSiKe made their moves, but it was not until a year later that TQC3721—ranking second globally and first domestically in clinical development—reached its moment in the spotlight.

Why now? Because what Sino Biopharm wants is not"First to market" is "best."

Clinical data show that,TQC3721 enrolled patients with more severe COPD and outperformed competitors on key endpoints, including FEV₁ improvement and SGRQ quality-of-life scores.

SameTimeTQC3721Established a dual-formulation portfolio comprising nebulized inhalation suspension and dry powder inhaler, with the nebulized inhalation suspensionDemonstrated best-in-class potential in Phase IIb studies,in ChinaIIIPhase clinical stage,The dry powder inhaler is also advancing synchronously to Phase II clinical trials, with the potential to become the first domestically produced inhaled PDE3/4 dual inhibitor approved for marketing in China.Nebulization for severe cases, dry powder inhalation for mild to moderate cases, adapting to different scenarios and expanding treatment boundaries.

$200 million upfront payment + up to $1.7 billion in milestones + double-digit tiered royalties—Whether in terms of the upfront payment or the total contract value, this transaction has set a new record for out-licensing deals in China’s respiratory sector.

And choosing AstraZeneca was an even more astute move.

AstraZeneca is a global respiratory/The leading pharmaceutical company in immunology revenue, with over 15 respiratory product pipelines and four blockbuster products each generating annual sales exceeding $1 billion.

Sino BiopharmAlsoIt is one of the few leading companies in China with a deep footprint in the respiratory field. In the area of inhalation preparations, where domestic substitution is extremely challenging, Sino Biopharm was the first to achieve domestic substitution of budesonide suspension, with annual sales exceedingRMB 500 million, with multiple products such as Tiotropium Powder for Inhalation (Tianqing Sule®) and Methacholine Chloride Nebulizer Solution for Inhalation (Tianqing Suxin®) approved for market launch.

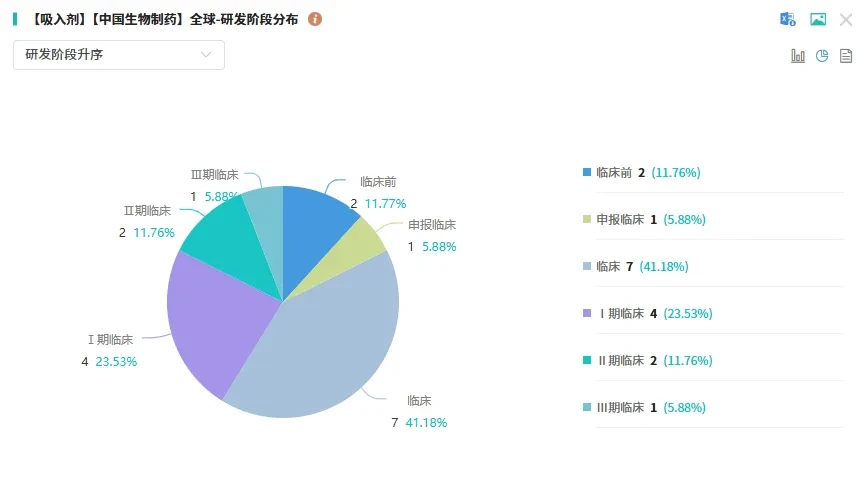

Except for TQC3721,Data from Mosent Pharma shows that,Sino BiopharmGlobally, more than 10 inhaled formulation pipelines have entered clinical stage and beyond,Its pipeline depth and tiered completeness are unique in China’s respiratory sector.

Screenshot source: PharmCube Global Drug R&D Database (Search Data. Find PharmCube)

02

GSK’s Two “Cash Cows” Make a Grand Entrance:Respiratory Leader Adds Two More Moats

If we sayTQC3721If the "going global" strategy represents a long-term layout, then the deep cooperation with GSK is the immediate realization of the "bringing in" strategy.

Under the agreement, Sino Biopharm’s subsidiary, Chia Tai Tianqing, will be fully responsible for the importation, distribution, hospital access, and promotion of Trelegy and Anoro in mainland China. GSK will continue to serve as the Marketing Authorization Holder (MAH), overseeing registration, quality, pharmacovigilance, and global brand strategy.

How competitive are these two products?

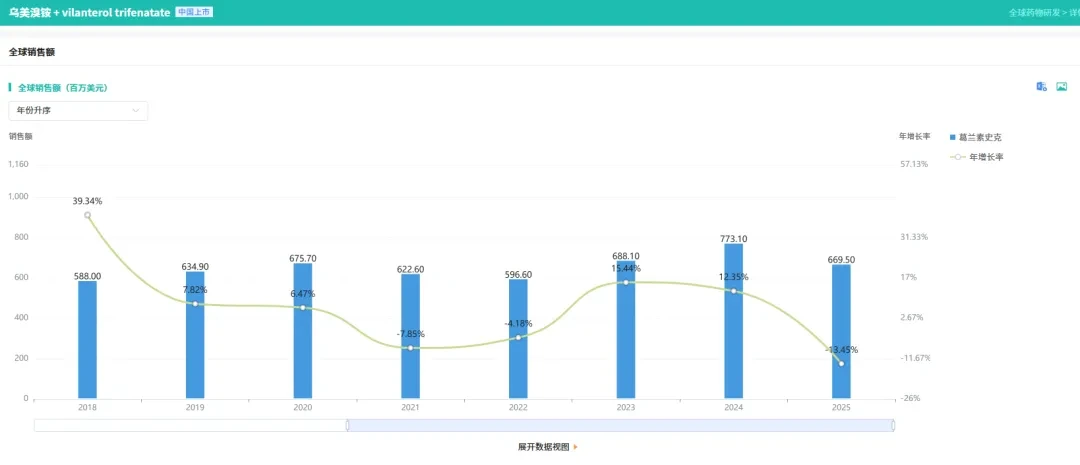

Trelegy Ellipta is currently the only single-inhaler triple therapy in China approved for maintenance treatment of both asthma and COPD. With global sales of approximately $4 billion in 2025, it ranks as the top-selling inhalation product worldwide. Anoro Ellipta is a core dual-bronchodilator regimen for COPD recommended by the GOLD guidelines, with annual global sales of approximately $700 million.

Screenshot source: PharmCube Global Drug R&D Database (Search Data. Find PharmCube)

The two products have achieved cumulative global sales of over US$23 billion.

By entrusting them to Sino Biopharm, GSK is betting on Sino Biopharm’s commercialization capabilities—its respiratory-focused academic promotion team of nearly 2,000 members, distribution channels covering more than 9,000 medical institutions across China, and its leading market share in the respiratory sector, consistently ranking first domestically. In the field of inhalation preparations, where domestic substitution faces significant challenges, Sino Biopharm was the first to successfully develop budesonide suspension, achieving annual sales exceeding RMB 500 million.

This is not the first time GSK has entrusted a blockbuster product to Sino Biopharm. Two months ago, the commercialization rights in China for the star liver disease drug bepirovirsen were also awarded to Chia Tai Tianqing. Prior to that, Sino Biopharm and BI had already established a comprehensive collaboration in the oncology field over many years.

MNCs’ trust in Sino Biopharm is on an upward spiral. The progression from single-product to multi-product collaborations, and the deepening of partnership from oncology to respiratory diseases, essentially constitutes a continuous validation of Sino Biopharm’s “end-to-end capabilities spanning R&D to commercialization.”

The launch of these two products comes at an opportune time. The domestic market for inhalation preparations is approximately74.8 billion yuanAsthma and COPD indications account for over 60%. High-end combination inhalers, such as triple therapy and dual bronchodilators, are the fastest-growing category. With COPD included in the National Basic Public Health Services Program, policy benefits are rapidly unlocking penetration potential in the primary care market.

As the leading player with the most comprehensive portfolio in China’s respiratory sector, Sino Biopharm has established a product cluster featuring multi-technological modalities and diverse dosage forms, including three major inhalation platforms—nebulized solutions, dry powder inhalers (DPI), and soft mist inhalers (SMI)—alongside four innovative technology platforms for small molecules, antibodies, siRNA, and transdermal patches.

GSK provides the products, Sino Biopharm provides the channels—leveraging a time-tested commercialization network to unlock the most certain incremental market.

03

# With Inflows and Outflows, Sino Biopharm’s Valuation Formula Is Being Rewritten

Two deals closed on the same day, one acquisition and one divestment, outlining Sino Biopharm’s clear strategic product portfolio.

"Bringing In": By securing two blockbuster respiratory products from GSK, in addition to its previous deep collaborations with multinational corporations (MNCs) such as BI, Sanofi, and Merck & Co., Sino Biopharm has become one of the few domestic pharmaceutical companies in China capable of consistently undertaking the commercialization and launch of global blockbuster products across multiple therapeutic areas.

"Going Global": TQC3721The licensing deal with AstraZeneca marks Sino Biopharm’s second outbound licensing transaction of the year. In February this year, rovatirelinib was licensed to Sanofi for $1.53 billion. To date, Sino Biopharm has completed a total of four outbound licensing deals, with upfront payments exceeding $1 billion and a total transaction value surpassing $7 billion.

This year, the upfront payments from just two outbound licensing deals have already exceededRMB 2 billion, providing a considerable and better-than-expected boost to 2026 performance. AsTQC3721As clinical development of the products advances, subsequent milestone payments will provide sustained contributions.

Industry consensus holds that collaborations between multinational corporations (MNCs) and Chinese pharmaceutical companies typically evolve from superficial to deep, progressing step by step. Sino Biopharm has successively established in-depth partnerships with multiple MNCs, including Boehringer Ingelheim, Sanofi, Merck & Co., GSK, and AstraZeneca, signifying that its comprehensive capabilities across commercialization, R&D, and platform development have gained substantial recognition from leading global pharmaceutical companies. As one of the preferred partners for MNCs in China, Sino Biopharm is continuously expanding the scope of its collaborations, entering a rapid “snowballing” phase.

Behind these collaborations, Sino Biopharm has become the only pharmaceutical company in China to successfully implement a “dual circulation” strategy across multiple therapeutic areas—bringing “China-born innovations” to the global market and introducing “global innovations” to the Chinese market. This has established a clear and sustainable second growth curve: leveraging the rapid scale-up of mature, blockbuster products worldwide to solidify its domestic market share as a stabilizing anchor, while relying on global licensing partnerships to unlock profit elasticity and consistently deliver high-value returns. These two pillars are mutually synergistic and supportive.

As the scale of two-way business development (BD) continues to expand, the second growth curve will provide stable and sustained incremental profits, and the valuation formula is being recalculated.

Over the past decade, China’s respiratory medication market has undergone a protracted transition from import monopoly to domestic substitution. Sino Biopharm was the first to successfully develop budesonide suspension, breaking the stranglehold on inhaled formulations and establishing itself as the undisputed pioneer in China’s respiratory sector.

Today, armed with two blockbuster products, TQC3721 and GSK’s offerings, Sino Biopharm has made the critical leap from “follower” to “leader.”

END

This article is an original work. Please leave a message to obtain authorization for reposting.