Hefei-Backed Biotech Jingze Files Third Hong Kong IPO Bid Amid Commercialization Push

Jingze Bio

New Drug Developer

On July 3, Jingze Bio submitted its prospectus to the Hong Kong Stock Exchange for the third time.

As early as June 2025, the company had submitted its IPO application, followed by a second filing at the end of the year. Three submissions have become the norm for many Chapter 18A innovative biopharmaceutical companies with pipelines nearing commercialization as they race to go public.

Jingze Bio is headquartered in Hefei, with its shareholder list prominently featuring Hefei state-owned capital platforms such as Hefei Industrial Investment, Hefei New Economy, and Hefei Shuangchuang. However, compared to star projects like BOE and NIO, Jingze Bio’s story is far more subdued.

How Can This Biotech Firm, Yet to Commercialize Its Products, Bear the Expectations for Hefei’s Biopharmaceutical Industry’s Hong Kong IPO?

Jingze Bio traces its history back to 2014 and has grown since establishing its presence in Hefei in 2018.

It has chosen two fields that appear to be quiet but actually have enormous demand: assisted reproductive technology, addressing the challenge of infertility; and ophthalmology, addressing the problem of vision loss.

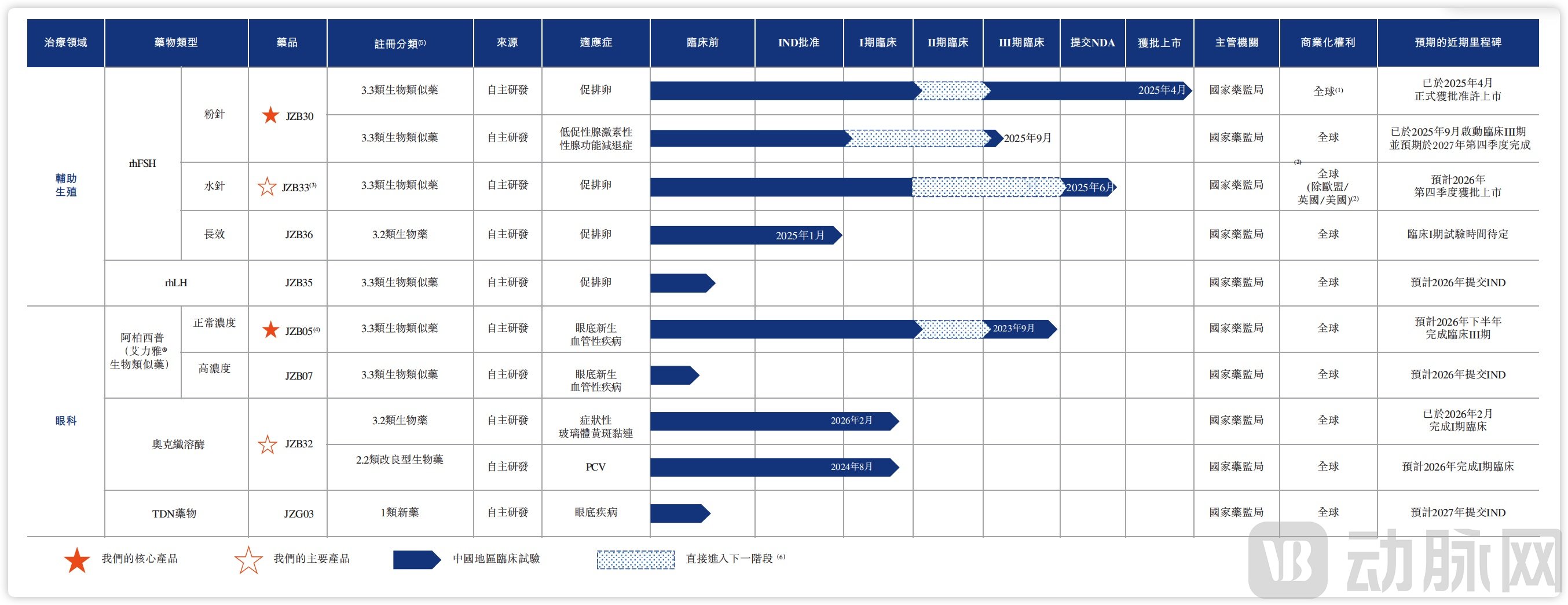

Corporate Pipeline Portfolio, Source: Prospectus

JZB30 is a lyophilized powder for injection of recombinant human follicle-stimulating hormone (rhFSH). It received marketing approval from the National Medical Products Administration in April 2025, marking Jingze Bio’s first commercialized product. JZB33 is an aqueous solution formulation containing the same active ingredient; its New Drug Application (NDA) was submitted and accepted in June 2025. The transition from lyophilized powder to aqueous solution addresses the need for greater convenience in patients’ home administration.

Jingze Bio does not intend to engage in head-to-head competition with first-movers in any single dosage form. Instead, it leverages a product portfolio covering diverse usage scenarios to meet the varied needs of institutions ranging from top-tier tertiary hospitals to grassroots reproductive centers.

For a long time, core assisted reproductive technology drugs such as follicle-stimulating hormone (FSH) have been monopolized by the imported original drug Gonal-f, resulting in high prices. The approval of JZB30 adds a new option to domestically produced recombinant human FSH (rhFSH). This not only reduces the cost of in vitro fertilization (IVF) cycles but also aligns, to some extent, with national policy directives on fertility support. However, although JZB30 has been approved, its production side is still undergoing pre-commercialization production line modifications and acceptance procedures.

JZB05 is an anti-VEGF intravitreal injection, benchmarked against aflibercept, the world’s best-selling ophthalmic drug. It is currently in Phase III clinical trials, with completion of the trials and submission of a marketing application expected in the second half of 2026.

Also noteworthy is JZB32, which targets symptomatic vitreomacular adhesion (sVMA). The traditional treatment for this condition is vitrectomy, which causes significant trauma to the eye. JZB32 aims to spare patients from surgery by employing an enzymatic injection approach. Currently, it is the only sVMA drug under development in China. Additionally, a therapy targeting polypoidal choroidal vasculopathy (PCV) is in Phase I clinical trials.

Rather than competing in the saturated anti-VEGF market, Jingze Bio’s future prospects lie in the differentiated development path of JZB32. In contrast, JZB05 (an aflibercept biosimilar), currently in Phase III clinical trials, is positioned as a follower in a mature market. To control costs and ensure production capacity, Jingze Bio has established GMP-compliant manufacturing facilities in Chengdu and Xuzhou, with a total planned capacity exceeding 5,000 liters. The company has also completed head-to-head clinical trials comparing JZB05 with Eylea.

In addition, candidate drugs such as JZB36 (long-acting rhFSH), JZB35 (rhLH), and JZB07 (high-concentration aflibercept) are in earlier stages of development, collectively forming a pipeline portfolio that spans from biosimilars to improved biologics.

On the eve of commercialization, Jingze Bio has opted for an asset-light strategy combining independent R&D with collaborative promotion. The domestic commercialization rights for JZB05 have been assigned to Kangzhe Pharmaceutical, while the exclusive commercialization rights for JZB33 in the United States, the European Union, and the United Kingdom have been licensed to Nanjing Jianyou. Meanwhile, the company is collaborating with overseas partners to simultaneously advance the overseas registration of its reproductive health and ophthalmic drugs, thereby sharing the costs of international clinical development and market entry.

The two sectors chosen by Jingze Bio are both undergoing a transition period of domestic substitution.

The market size of assisted reproductive drugs in China was approximately RMB 5.8 billion in 2025 and is projected to reach RMB 11.3 billion by 2030, with a compound annual growth rate (CAGR) exceeding 12%. Ovulation induction drugs account for the largest proportion of costs throughout the entire assisted reproductive cycle. In the domestic recombinant follicle-stimulating hormone (rFSH) segment, recombinant human follicle-stimulating hormone (rhFSH) holds over 70% of the market share due to its higher bioactivity and safety profile.

For a long time, this market has been dominated by imported products. Gonal-f has captured half of the market share, with prices once reaching several thousand yuan. While there is significant potential for domestic substitution, the entry barriers remain high. As the first domestically produced recombinant human follicle-stimulating hormone (rhFSH), Jin Sai Heng from Changchun GeneScience Pharmaceuticals has gained a foothold in the market after years of gradual growth. An Xin Bao, developed by Qilu Pharmaceutical, was approved in 2021 but currently holds a low market share.

For patients, imported products are expensive, and there is still a clear demand for lower-priced domestically produced alternatives.

The ophthalmic anti-VEGF drug market is also showing a growth trend, with the market for anti-VEGF drugs targeting fundus neovascular diseases (FND) valued at approximately RMB 6.4 billion in 2025 and projected to reach RMB 12.6 billion by 2030.

The domestic ophthalmic anti-VEGF market is characterized by a "one dominant player, several strong competitors" landscape alongside a transition between older and newer therapies. Kanghong Pharmaceutical’s Conbercept, the sole domestically developed original drug, firmly holds the top position with annual sales exceeding RMB 2.4 billion. Among imported products, Bayer’s Aflibercept remains in the second tier, while Novartis’s Ranibizumab has suffered a significant decline in market share due to pressure from both domestic biosimilars and Conbercept. The key variable is Roche’s Faricimab, approved in 2024, which is rapidly gaining volume thanks to its extended-duration mechanism and reshaping the market landscape.

In the niche segment of aflibercept biosimilars, Qilu Pharmaceutical has secured the first approval, followed closely by Boan Biotech. Maiwei has also submitted its New Drug Application (NDA), while Jingze Bio’s JZB05 is still in Phase III clinical trials, expected to be completed in the second half of 2026. By the time it officially launches, two similar products will already have been commercialized in China. Meanwhile, the next generation of competition is shifting toward dual-target and even multi-target therapies, with Kanghong, InnoCare, and Rongchang all making strategic moves. The window of opportunity for pure biosimilars is narrowing.

The commonality between the two sectors is that the market education phase has passed, patient demand is genuine and sustained, yet high-end biologics have long relied on imports, leaving clear room for domestic substitution and product upgrades.

The corporate financing process also reflects capital’s optimism about the future development of the sector.

Since 2018, Jingze Bio has completed six rounds of equity financing, from Pre-A to C+, with a cumulative total of approximately RMB 1.041 billion. In terms of capital structure, the investors are categorized into industrial capital (Tigermed, CMS Pharmaceutical, Nanjing Jianyou), local state-owned capital (industrial funds in Hefei, Xuzhou, Chengdu, Anhui, and other regions, deeply tied to the establishment of production bases), and venture capital (including Yifeng Capital, Yinglianxi, and Donghai Venture Capital, which have continuously participated in multiple rounds).

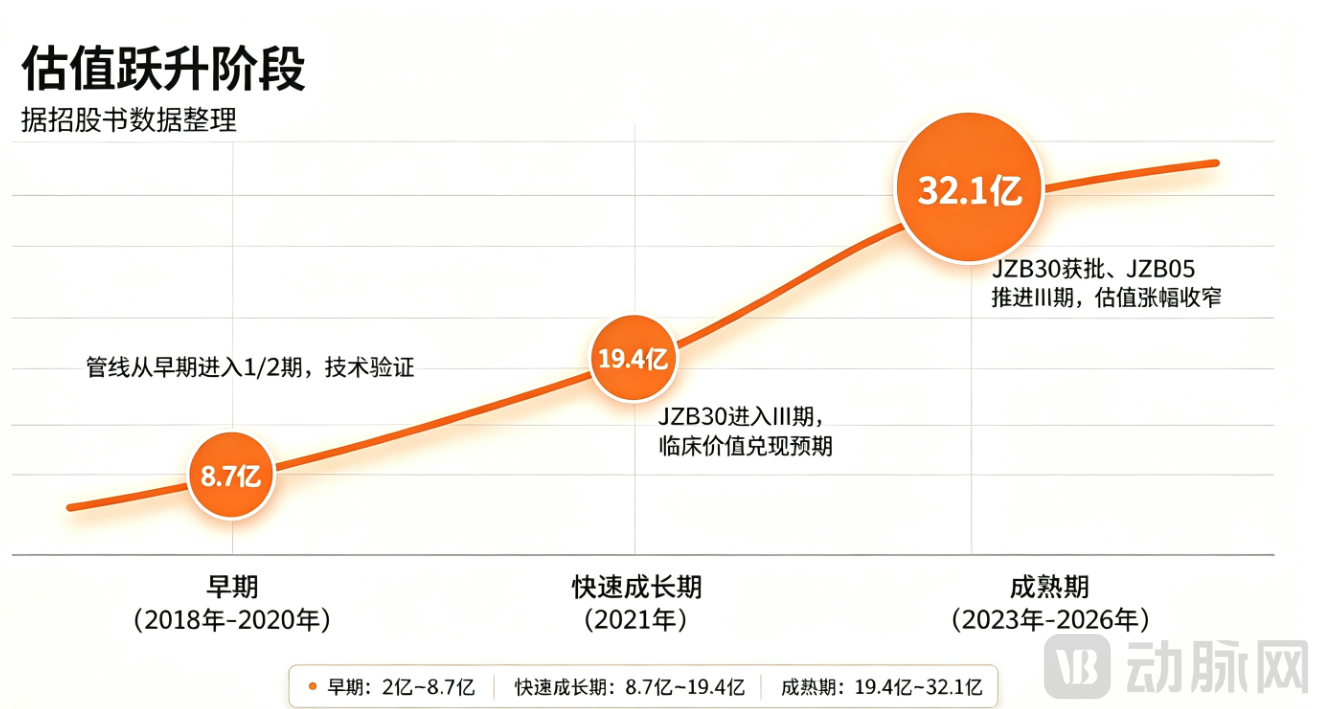

From the perspective of the financing process, Jingze Bio has gone through three important stages.

Valuation Surge Phase, Compiled from Prospectus Data

From the Pre-A round to the B+ round, the valuation gradually climbed from RMB 200 million to RMB 870 million, marking the early stage of R&D validation. In January 2021, the Series C financing raised RMB 240 million, with the valuation jumping to RMB 1.94 billion. This milestone coincided with the official launch of the Phase III clinical trials for JZB30, where reduced risk led to a doubling of the valuation.

The C+ round, spanning from late 2023 to early 2026, corresponded to multiple milestones: the completion of Phase III clinical trials for JZB30, the entry of JZB05 into Phase III trials, and the filing for market approval of JZB33. During this period, industrial capital and local state-owned assets also successively invested in the company. Despite the capital winter in the primary market, the valuation still climbed to RMB 3.21 billion.

The prospectus discloses that all funds raised will be used to advance the product pipeline and establish production capacity. The core allocation is divided into four major segments: advancing JZB05 through Phase III clinical trials, expanding new indications for JZB30, and commercializing proprietary production lines; supporting clinical trials for the innovative drug JZB32; investing in the R&D of multiple pipelines under development, including JZB33, JZB36, and JZB07; and supplementing working capital to cover R&D personnel salaries, raw materials, and daily operational expenses.

Jingze Bio’s three consecutive listing applications are, in fact, a microcosm of the Chapter 18A sector. Many biotech firms like Jingze are stuck in a critical transitional phase where substantial R&D investments have been made and products have received regulatory approval, but commercial scale-up has yet to materialize. These companies do not lack technology or clinical value; what they lack is time and capital.