Over USD 100 Million! A Zhejiang Pharma Acquires an Analgesic Drug

Conba

Pharmaceutical R&D, Manufacturing, Sales, and Medicinal Herb Cultivation

On July 6, Conba disclosed that its wholly-owned subsidiaries Hangzhou Conba and Hong Kong Conba signed an agreement with Adneuris Therapeutics. The two subsidiaries acquired licensing, development and commercialization rights to the innovative analgesic candidate cebranopadol under development across Greater China including mainland China, Hong Kong, Macao and Taiwan region of China through a license-in transaction.

Under the agreement, Conba will pay an upfront payment of $17.5 million, followed by development and commercial milestone payments totaling no more than $94 million, as well as tiered royalties based on product sales.

Dual-Target Oral Analgesic: Attempting to Solve the Safety Challenge of Opioids

Adneuris Therapeutics, founded in 2019, is a biotechnology company focused on the research and development of innovative drugs in the pain management sector, headquartered in New Jersey, USA. Its parent firm Tris Pharma was founded in 2000. The company’s business covers central nervous system disorders, attention deficit hyperactivity disorder and pain management, with multiple approved products in its portfolio.

Cebranopadol involved in this transaction stands as Adneuris’s core pipeline asset. As an oral small-molecule analgesic, it has completed Phase III clinical studies and the company plans to submit a new drug application to the US Food and Drug Administration. According to public corporate documents, its primary indication is acute postoperative pain relief, and it holds potential for expansion into chronic pain treatment.

To understand why this drug warrants a $17.5 million upfront payment, one must revisit the long-standing clinical paradox associated with traditional opioids.

Currently, strong opioids such as morphine and oxycodone remain the primary choices for treating moderate to severe pain, exerting their analgesic effects mainly by activating MOP (Mu Opioid Receptor). However, the signaling pathways mediated by the MOP receptor are also associated with adverse reactions such as respiratory depression, nausea and vomiting, constipation, tolerance, and dependence.

The challenge of balancing efficacy and safety has long been a key focus in the research and development of analgesics.

Cebranopadol features a dual-target design logic. It activates MOP receptors to produce analgesic effects and meanwhile stimulates NOP receptors to participate in pain regulation. NOP receptors independently mediate pain modulation at spinal and central levels, and are also capable of regulating MOP receptor-related responses, including the rewarding effects caused by opioids. Designed based on this mechanism, cebranopadol aims to retain the analgesic potency of opioids while lowering some safety risks triggered by conventional MOP activation, delivering reduced toxicity without weakened efficacy.

According to public data released by Adneuris and relevant clinical trial findings, cebranopadol demonstrated favorable analgesic efficacy and safety profiles in Phase III clinical trials. Its full clinical benefits remain to be further verified through regulatory review and wider real-world application. Compared with conventional opioid medicines, its dual-target mechanism lays a differentiated foundation for its future market positioning.

Conba Relies on Innovative Drugs for New Growth as TCM Takes Over Half Its Revenue

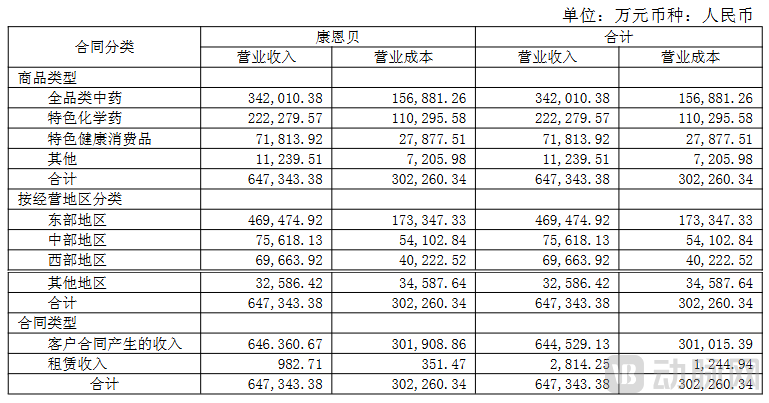

Conba’s 2025 annual report shows that the company achieved an annual operating revenue of RMB 6.473 billion, a net profit of RMB 474 million, and R&D investment of RMB 326 million, including R&D expenses of RMB 262 million, with an R&D expense ratio of 4.04%.

In terms of business structure, the company currently operates five divisions covering over-the-counter medicines, prescription drugs, health consumer goods, API products, and Chinese herbal decoction pieces. Its full-spectrum traditional Chinese medicine business generated revenue of RMB 3.420 billion, accounting for 52.83% of total revenue and ranking as its largest business segment. The specialty chemical medicine segment brought in RMB 2.223 billion, making up 34.34% of total revenue. Together, these two segments contribute more than 87% of the company’s core operating income.

Conba’s 2025 Revenue and Cost of Sales Details (Source: Conba 2025 Annual Report)

A key consideration for Conba’s introduction of cebranopadol is to add innovative drug assets to its established traditional business lines.

Meanwhile, the analgesia sector offers substantial market potential. According to industry data cited in Conba’s announcement, the size of China’s acute postoperative pain management market was approximately RMB 20.5 billion in 2019 and is projected to exceed RMB 32 billion by 2030.

Against this backdrop, whether a product can address unmet clinical needs stands as the core competitive factor for innovative analgesics. For a long time, conventional opioid analgesics deliver clear therapeutic effects yet are constrained by safety concerns such as dependence and respiratory depression. Clinicians still demand novel pain management solutions that balance robust efficacy and favorable safety profiles. Featuring a dual MOP/NOP target mechanism, cebranopadol is engineered to mitigate certain limitations of classic opioids, aligning with mainstream innovation trends in the analgesic field.

Heightened Regulatory Barriers Raise Entry Hurdles, First-Mover Products Poised to Gain Competitive Advantage

China implements strict classified management of narcotic drugs and psychotropic substances, covering multiple aspects including the drug catalog, production and operation, circulation and distribution, and clinical use, with joint administration by drug regulatory, public security, and health authorities. Compared with ordinary pharmaceuticals, narcotic analgesics face higher requirements in research and development registration, production qualifications, and commercial promotion.

This regulatory attribute, on the one hand, raises market entry barriers for enterprises in this field. On the other hand, it means enterprises that take the lead in obtaining product approval and building a clinical application system are likely to gain notable first-mover advantages.

Differences in control classification will further boost the commercial flexibility of cebranopadol. As disclosed in the transaction announcement, if cebranopadol obtains approval in the United States, the Drug Enforcement Administration is expected to classify it as a Schedule IV or V controlled substance. It carries far lower abuse control restrictions than traditional potent opioids such as morphine and oxycodone, which fall under Schedule II. From China’s regulatory perspective, the 2025 edition of the Catalogue of Medicinal Psychotropic Substances has already categorized cebranopadol as a Class II psychotropic substance in advance.

More importantly, no oral dual NOP/MOP-targeted analgesic has yet been filed for approval in China. If cebranopadol successfully completes bridging trials, it will become the first-in-class candidate in this domestic track.

This first-mover advantage translates into three layers of moats built ahead of competitors: physician academic recognition, medical insurance reimbursement access, and nationwide channel coverage, which late entrants can hardly catch up with in the short run. Combined with lower controlled-substance classification and accelerated regulatory review timelines, the cycle from product approval to robust sales expansion will be shortened, delivering a more predictable timeline for the realization of investment returns.

License-in Deals Heat Up as Traditional Pharma Companies Target Late-Stage Clinical Assets

From a broader industrial perspective, the cebranopadol licensing deal is not an isolated case. In recent years, license-in transactions have become a vital approach for Chinese pharmaceutical companies to enrich innovative pipelines, and established integrated pharmaceutical enterprises with mature commercialization systems are particularly active in seeking late-stage clinical assets.

This trend reflects the evolving division of labor within China’s innovative drug industry chain. In the past, pharmaceutical companies largely relied on their own capabilities to manage the entire process from R&D to commercialization. As competition in innovative drugs intensifies, different types of enterprises are increasingly collaborating based on their respective strengths. Biotech firms are focusing more on early-stage innovative exploration, while traditional pharmaceutical companies leverage their capabilities in clinical development, manufacturing, and commercialization to acquire mature assets. The license-in model has become a key mechanism for connecting the capabilities of these two types of enterprises.

Nevertheless, license-in deals do not eliminate innovation risks. The ultimate value of a product hinges on multiple factors including regulatory approval, clinical positioning, physician acceptance and reimbursement landscape. For cebranopadol, it has not yet secured FDA approval. Its long-term value derived from this transaction will be shaped by its subsequent registration progress in China, commercialization strategies and real-world clinical feedback.

The postoperative analgesia market is in urgent clinical need of more high-efficacy and low-toxicity treatment options. However, it remains to be seen whether such unmet clinical demand can translate into profits for Conba.