Ascletis Submits Dual INDs to FDA for ASC36 and ASC36_35 FDC, Featuring a Next-Gen Amylin Agonist with 91% Superior Weight Loss vs. Competitors

Innovent

High-end Biologics Developer

Ascletis Pharma (01672.HK)July 6Announced that it has been submitted to the U.S.FDA Submits Two Investigational New Drug (IND) Applications for Novel Obesity Therapies——Once monthly to once quarterlySubcutaneous Injectionthe new generation of multi-Peptide Amylin Receptor AgonistASC36, andOnce-Monthly Fixed-Dose Combination (FDC) of ASC36 and the Dual GLP-1R/GIPR Agonist ASC35ASC36_35 FDC。

Both adopt Ascletis' proprietary ultra-long-acting drug development platform.SALD (Self-Assembling Lipid Depot) formulation,Preclinical head-to-head studies showASC36 Monotherapy Weight Loss Effect Compared toPEtrelintide height approximately91%, ASC36_35 FDC showed a relative improvement of approximately compared to eloralintide in combination with tirzepatide51%。

This marks another charge by Chinese biotech firms toward global regulatory authorities in the field of weight loss and metabolism, following the FDA’s IND approval in June 2026 for Ascletis’ ASC35 (a monthly GLP-1R/GIPR dual-target agonist). As the market dominance of the two leading GLP-1 therapies begins to hit a ceiling,Amylin Receptor AgonistwithMulti-Target Combination Long-Acting FormulationIt is becoming the next core battleground for weight loss, where multinational pharmaceutical companies and leading biotech firms are placing their bets.

Frontiers in Weight-Loss Pharmacotherapy: From GLP-1 Dual Agonists to the Race for “Amylin+” and Triple Agonists

Currently, the mainstream weight-loss injections available globally are still dominated by GLP-1 receptor agonists (Novo Nordisk’s semaglutide/Wegovy) and dual GLP-1R/GIPR agonists (Eli Lilly’s tirzepatide/Zepbound). However, existing drugs have approximately25%–40% Weight Regain Rate, some patients experience significant muscle loss and gastrointestinal intolerance, among other limitations; currently, the industry’s R&D focus is iterating in four directions:

■ Multi-Target Synergistic Enhancement

Lilly Retatrutide(GLP-1R/GIPR/GCGR Triple Agonist) Phase III trials demonstrated that the highest dose group achieved an average weight loss of 28.3% over 80 weeks, with nearly half of the participants achieving weight reduction ≥30%. The efficacy approaches that of metabolic surgery, and the New Drug Application (NDA) is expected to be submitted to the FDA in 2026–2027. In ChinaInnovent's Mazdutide(GLP-1R/GCGR dual-target) was approved for weight loss indications in 2025, with clinical data showing an average weight reduction of 18.55% after 60 weeks of treatment in patients with moderate to severe obesity;Hengrui Medicine HRS9531(GLP-1R/GIPR dual-target)Hansoh Pharma's Olepatide(HS-20094) have both entered Phase III clinical trials.

■ Amylin Receptor Agonists

Amylin is co-secreted by pancreatic β-cells and produces weight loss effects independent of GLP-1 by delaying gastric emptying and activating the brainstem satiety center. Eli Lilly’s eloralintide, a selective long-acting AMYR agonist, achieved a mean weight reduction of 20.1% (highest dose group) in a 48-week interim study, and a 29.0% weight reduction when combined with tirzepatide for 32 weeks. Novo Nordisk’s zenagamtide, a GLP-1/amylin fusion molecule, resulted in a 23.9% weight reduction after 36 weeks of subcutaneous injection, while its oral formulation achieved an 11.8% weight reduction over 12 weeks. Ascletis Pharma’s ASC36 and ASC36_35 FDC are among the few candidates with publicly disclosed progress to date."Amylin + Dual-Target Combination Monthly Formulation"Layout.

■ Oral Small-Molecule GLP-1R Agonists

Eli Lilly’s orforglipron (an oral small-molecule GLP-1 receptor agonist) is currently in Phase III clinical trials, with Shuo Di Bio’s aleniglipron and Ascletis’ ASC30 (an oral small-molecule GLP-1 receptor agonist, with Phase III trials expected to commence in Q3 2026) close behind. The oral formulation is regarded asBreaking Through Injectable Production Capacity Bottlenecks and Expanding Penetration into Primary Carekey.

■ Fat Loss and Muscle Preservation

ActRII is an activin receptor expressed in both adipose and muscle cells; activation of the ActRII receptor can lead to fat accumulation and muscle atrophy. By blocking this pathway, it is expected toWhile promoting fat metabolism, it improves muscle composition.During weight loss with GLP-1 receptor agonists, approximately 25%–40% of the loss is lean muscle mass. Combination therapy with a myostatin inhibitor can ensure that 92.8% of the weight loss comes from fat. In Phase II trials, Eli Lilly’s semaglutide combined with bimagrumab achieved an average weight reduction of 22.1%, with near-complete preservation of muscle mass. This approach directly addresses the critical issue of muscle loss associated with GLP-1 therapies, representing the next frontier in the competition for “high-quality weight loss.”

Global and China Weight Loss Market Size and Competitive Landscape

1. Global Market: Duopoly with a Hundred-Billion-Yuan Opportunity Yet to Be Unleashed

Annual report data shows that in 2025, Eli Lilly’s tirzepatide achieved global sales of approximately $36.5 billion (with the weight-loss version, Zepbound, contributing $13.54 billion), while Novo Nordisk’s semaglutide reached a combined total of around $36.1 billion (with the weight-loss version, Wegovy, accounting for $12.5 billion). Together, these two companies captured nearly 97% of the global GLP-1 weight-loss market. According to forecasts from institutions such as Jefferies, the total market size for GLP-1 receptor agonists (GLP-1 RAs) is expected to exceed $150 billion by 2031.

2. China Market: The "Tripartite Game" of Originator Drugs, Domestic Innovations, and Biosimilars

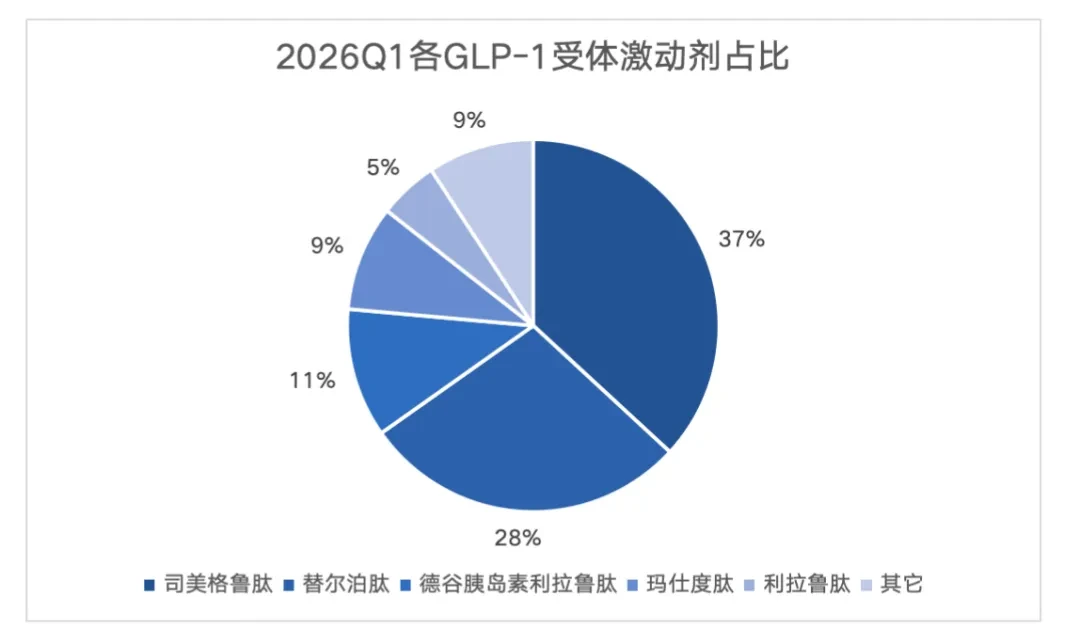

According to multi-channel data from Sinopharm CHIS, the omni-channel market size for GLP-1 receptor agonists in 2025 was approximately RMB 14.6 billion., a year-on-year increase of 34%, with growth rates in both the retail market and B2C exceeding 100%. In Q1 2026, the combined share of these two channels surpassed 50%, higher than that of the hospital-based channel.

In terms of the competitive landscape, semaglutide held the highest market share (37%) in Q1 2026, followed by tirzepatide (28%), with originator drugs demonstrating a clear advantage; domestically produced innovative drugs—Innovent's MazdutideRanked fourth (9%) after only one year on the market, with astonishing growth.

Regarding biosimilars, the core compound patent for semaglutide in China will expire in March 2026,Jiuyuan Gene, Huadong Medicine, Livzon Group, Qilu PharmaceuticalMore than 10 domestic companies have submitted marketing applications for their biosimilars or completed Phase III clinical trials. However, the originator company, Novo Nordisk, has successfully extended its market exclusivity until around April 2027 through a combination strategy of "patent + data protection," creating substantial barriers to the market entry of domestically produced biosimilars.

Directions for Breakthroughs and Prospects for New Targets

Although the GLP-1 therapeutic area appears crowded, significant unmet clinical needs remain. Beyond the aforementioned multi-target synergy and fat loss with muscle preservation, the next-generation breakthrough directions widely recognized by the industry include:

Source: Nature Rev Drug Discov 2026, Clinicaltrials.gov

Analysts point out that over the next 3–5 years, competition in the weight-loss drug market will evolve from a simple contest of “who achieves greater weight loss” toEfficacy、Compliance(Oral/Long-acting),Muscle Protection、Improvement in Complications(Fatty liver/MASH, OSA, cardiovascular risk) andCost-effectivenessa multidimensional competition. In the Chinese market, although the patent cliff for semaglutide has been delayed, its market share is already being challenged by new multi-target drugs. In the field of novel mechanisms of action, the differentiated strategies of domestically developed innovative drugs—such as Ascletis’ recent deployment of a monthly amylin + GLP-1R/GIPR combination formulation—are poised to secure a foothold for Chinese biotech companies in the amylin therapeutic arena.

In your opinion

What Characteristics Must the Next Generation of “Blockbuster” Weight-Loss Drugs Possess?

Ultimate Efficacy / Ease of Use / Muscle Protection?

Industry peers are welcome to exchange and discuss in the comments section~

This article synthesizes data from Sinocare CHIS, company announcements, NMPA and FDA public disclosures, and publicly available market research reports.