Beijing TRT Healthcare, a TCM Service Leader With a 300-Year Pharmaceutical Heritage, Goes Public on the Hong Kong Stock Exchange

Beijing TRT Healthcare

TCM Medical Service Provider

On July 7, Beijing TRT Healthcare was listed on the Hong Kong Stock Exchange, with an issue price of HK$5.5.

Beijing TRT Healthcare is the fourth listed entity under the Tongrentang Group. Unlike the other three, which focus primarily on pharmaceutical manufacturing and distribution, it fills the Group's gap in offline clinical medical services. Together, the four entities establish a complete closed loop encompassing drug R&D, production, domestic and international distribution, and TCM diagnosis and treatment services, with their businesses forming complementary upstream and downstream relationships.

Since its initial filing in June 2024, the company underwent two rounds of updates in late 2024 and June 2025. After launching its IPO in March 2026, it temporarily suspended the offering due to lukewarm subscription interest. Following the final update to its prospectus in June, the company proceeded with its listing.

It is not new for time-honored brands to operate chain outpatient clinics, but Goodsangtang has paved the way by taking a TCM clinic chain to an IPO on the Hong Kong Stock Exchange, with Beijing TRT Healthcare becoming the second to do so. In particular, a comparative review of the various prospectuses filed by Tongrentang clearly reveals the true fluctuations in policy and capital cycles within the private TCM sector, while also reflecting the real challenges faced by time-honored brands as they cross over into healthcare provision.

Traditional Chinese Medicine (TCM) healthcare services represent a vast market, yet the landscape is highly fragmented.

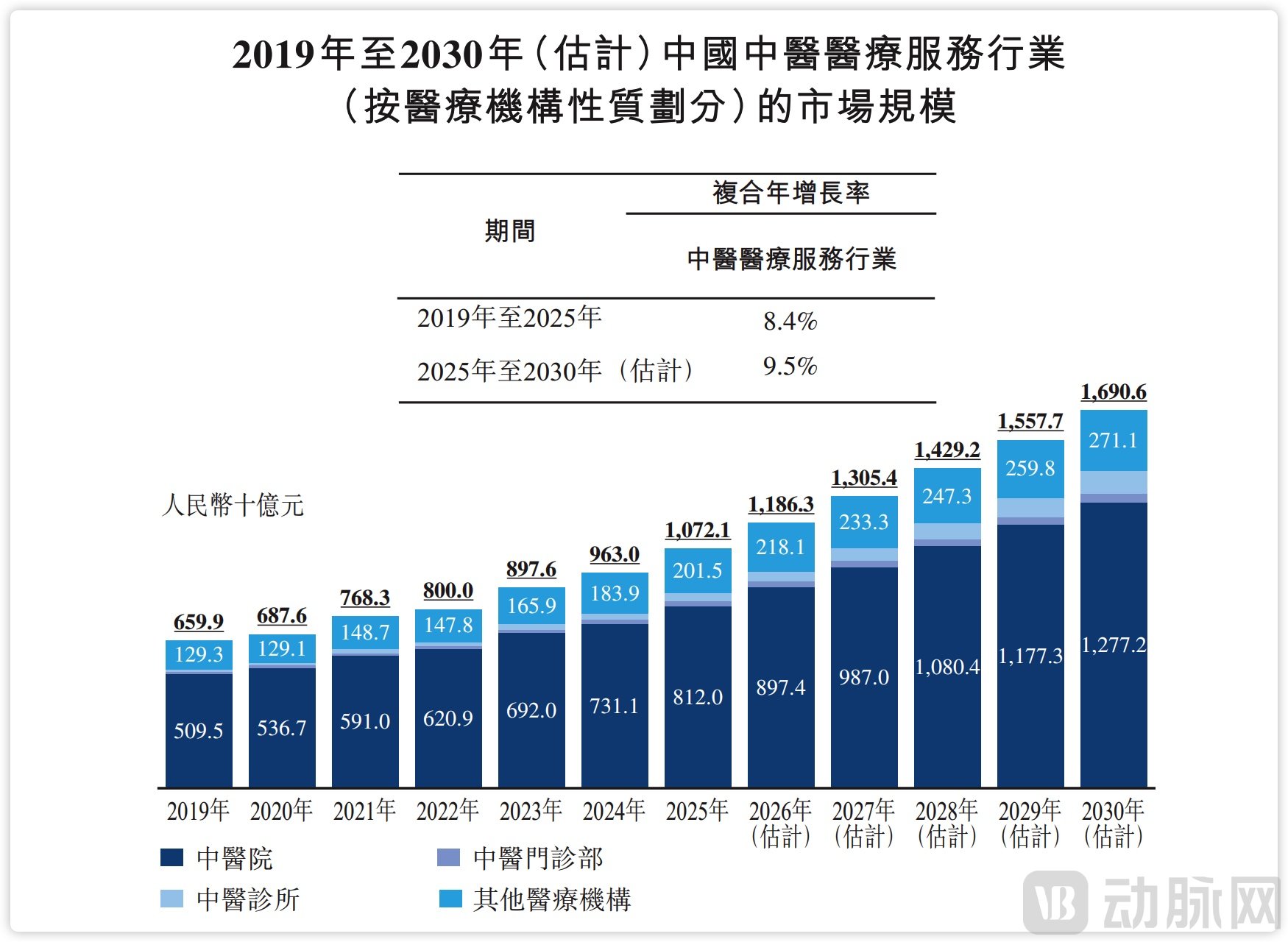

The TCM healthcare services industry is undergoing a phase of rapid expansion. According to Frost & Sullivan data, the market size of China's TCM healthcare services exceeded RMB 1 trillion in 2025, accounting for approximately 14% of the country's overall healthcare services market. This growth is driven by the rising demand for chronic disease management due to population aging, the expansion of medical insurance coverage, and a wellness trend spearheaded by the newer generation.

Market Size of Traditional Chinese Medicine (TCM) Medical Services, Source: Prospectus

Market size is not equivalent to corporate size.

In this trillion-yuan market, industry concentration is surprisingly low. The combined market share of the top five non-public TCM hospital groups amounts to approximately 5.4% by number of patient visits and merely 0.8% by revenue. Beijing TRT Healthcare ranks first by patient visits with a 1.5% market share, but second by revenue with only a 0.2% share. Even the industry leader has yet to achieve significant economies of scale.

The fragmentation of the industry has deep-rooted causes. As of 2024, there were a total of 6,497 TCM hospitals in China, accounting for less than 0.6% of all medical institutions. Among these, public TCM hospitals hold an absolute advantage in terms of quantity, designation as medical insurance providers, patient trust, and physician resources.

Although there are 3,614 non-public TCM hospitals, most are characterized by their small scale, fragmented distribution, and limited competitiveness. They face operational challenges such as high barriers to medical insurance reimbursement eligibility, scarcity of resources from renowned and experienced TCM practitioners, and strong community-based attributes that hinder cross-regional replication.

This gap is even more pronounced when compared to the mature development path of Western medicine chains.

Aier Eye Hospital achieved rapid expansion through standardized surgical procedures and heavy investment in asset-intensive equipment, while TC Medical established brand premium through deep regional cultivation. However, the capitalization level of TCM medical services remains relatively low. Although Goodsangtang listed on the Hong Kong Stock Exchange in 2021, becoming the first privately owned TCM chain company to do so, pure TCM medical service targets remain scarce in both the A-share and Hong Kong stock markets.

With Beijing TRT Healthcare's recent listing, a duopoly has formed alongside Goodsangtang. Though their paths differ, they face the same challenges.

As of the end of 2025, Goodsangtang operated approximately 101 medical institutions, with revenue exceeding RMB 3.2 billion and adjusted net profit of around RMB 390 million in 2025. Its business model focuses on the asset-light replication of TCM clinics, characterized by small store sizes and low capital investment. By leveraging a physician partnership system to secure resources from renowned TCM practitioners, the company has achieved rapid expansion.

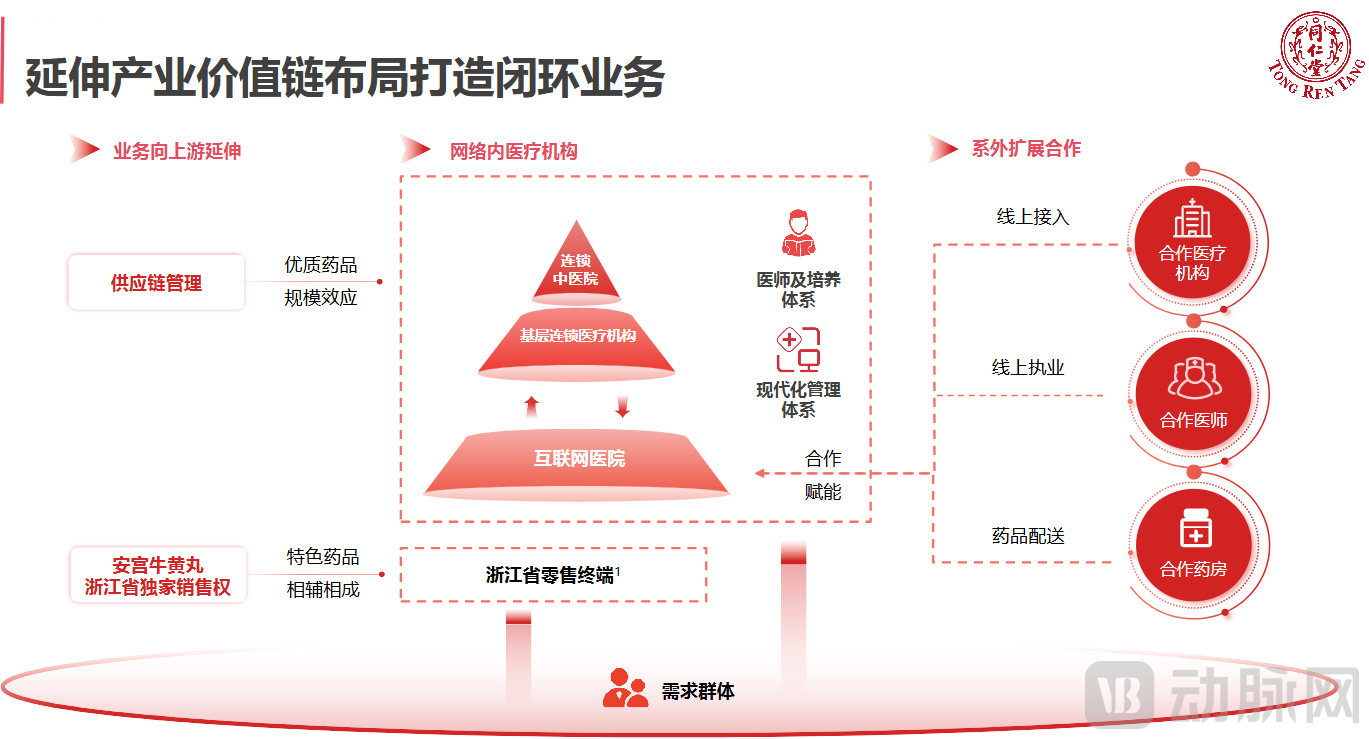

Beijing TRT Healthcare operates seven self-owned hospitals, three outpatient departments, and three clinics, in addition to managing 12 medical institutions and one internet hospital. Its business model is anchored by TCM hospitals, featuring a heavier asset structure and stronger specialization. The company aims to achieve deep regional penetration through a tiered diagnosis and treatment network. However, the integration, acquisition, and operation of hospitals involve high complexity, requiring a strategy grounded in deep operational expertise.

Asset-light renowned physician clinics offer rapid expansion and higher gross margins, but lack the capacity to admit critically ill patients, face a hard ceiling on average revenue per user (ARPU), and incur persistently high costs due to the need for high revenue-sharing arrangements to retain top physicians. In contrast, self-built comprehensive TCM hospitals can meet full-spectrum diagnostic and treatment needs, but require heavy asset investment that prolongs the payback period and makes nationwide replication extremely costly.

Neither TCM clinics nor TCM hospitals can escape the talent bottleneck plaguing the TCM industry. Beijing TRT Healthcare employs 2,732 licensed physicians, including 30 nationally honored physicians. While renowned physicians can be acquired, they are difficult to replicate; however, the brand effect of Tongrentang plays a significant role in healthcare service scenarios.

Beijing TRT Healthcare's Business Structure Closed Loop

Amid industry-wide constraints, the strategic adjustments made by this time-honored brand can be observed through the differences in Beijing TRT Healthcare's four-stage progression.

The story of Beijing TRT Healthcare began in 2015. In that year, Beijing Tongrentang Investment Development Co., Ltd. was established, with its initial positioning serving merely as an internal investment platform for the group. It was not until 2019, when it was renamed Beijing Tong Ren Tang Healthcare Investment Co., Ltd., that its strategic direction shifted toward TCM medical services. In June 2024, the company completed its joint-stock restructuring and began filing its application with the Hong Kong Stock Exchange.

From an investment platform to a healthcare services group, the transformation was driven primarily by mergers and acquisitions, with four rounds of prospectuses fully documenting the company's expansion trajectory.

First, acquire for-profit TCM medical institutions. The first version of the document only incorporated Zhejiang Sanxitang, with 10 self-owned medical institutions; the second submission completed the acquisitions of Shanghai Chengzhitang and Zhonghetang, establishing high-end outpatient clinics in the Yangtze River Delta region; the third version fully integrated the annual performance of Shanghai stores; the final draft for 2026 stabilized the existing asset scale, featuring 13 self-owned institutions paired with one internet hospital and 13 managed public institutions, adding new off-site management projects, while continuously enhancing digital business layout.

Mergers and acquisitions-driven expansion directly altered the companies' fundamental financial profiles. During the first two IPO filing cycles, the inclusion of newly consolidated entities boosted revenue, signaling rapid scale growth to the market. However, after the disclosure of complete annual data in the subsequent two filings, revenue growth began to slow, with the medical services segment—accounting for 84.94% of total revenue—reporting a gross profit margin of 17.2%.

The company's external positioning has begun to shift. Its first two IPO filings closely followed the elder-care trend, emphasizing the integrated model of medical and elderly care. In its subsequent prospectus, it candidly disclosed that revenue from its health-and-wellness segment accounted for a relatively small proportion, with all core revenue derived from TCM clinical services. Consequently, the narrative focus has shifted to a tiered diagnosis and treatment model combining asset-heavy hospitals with public-hospital trusteeship.

On the other hand, in addition to its asset-heavy operations, Beijing TRT Healthcare has begun developing asset-light business lines, namely medical institution management services. By exporting a comprehensive standardized operational system, it charges management fees equivalent to 3%–4% of total revenue without bearing any costs, achieving a gross profit margin as high as 71.9%. The partnership targets public and community-based non-profit TCM hospitals and healthcare institutions, leveraging brand influence to rapidly penetrate lower-tier markets.

Currently, this business segment is in its early stages, with annual revenue at the tens of millions level. However, its costs are limited to management personnel and digital system maintenance, excluding heavy-asset rigid expenditures such as depreciation, rent, and equipment procurement. As a result, its cash conversion cycle is significantly more efficient than that of the company's self-owned hospital operations. The company plans to expand its management service offerings in the future, which may serve as the key to overcoming the challenges of asset-heavy models and slow scalability by leveraging brand equity.

The fundraising plan limits the number of newly built and acquired institutions to five each over the next five years, with resources concentrated on deepening presence in the two core markets of Beijing and Zhejiang.

The objectives are clear: control the pace of mergers and acquisitions to optimize single-store profitability; continuously expand high-margin managed services to balance the profit structure; increase investment in AI-driven TCM and internet hospitals to tap into online growth opportunities; and address sector challenges through a differentiated model that combines asset-light and asset-heavy approaches with industrial chain synergy.

Public awareness of Tongrentang is largely confined to its nationally recognized products, such as Angong Niuhuang Wan (a TCM remedy for emergency stroke treatment) and Wuji Baifeng Wan (a TCM remedy for gynecological health). With a brand history spanning over 300 years, the company has accumulated substantial trust capital. This trust is also reflected in its financial data: the company's annual sales and promotion expenses account for only 0.2% of its revenue, significantly lower than the industry average of 0.5% to 2%.

The brand brings its own traffic, maintaining customer flow without the need for high-cost advertising, resulting in extremely low customer acquisition costs.

With over 300 years of brand history, Beijing TRT Healthcare has established a foundation of trust that is difficult for other enterprises to match. However, the true test for Beijing TRT Healthcare has only just begun following its listing. While the time-honored brand's pharmaceutical expertise has created a century-long legacy, the future challenge lies in transforming this product-based trust into trust in its services.