H&H Healthcare, the Only Company With a Tricuspid Valve Registration Certificate, Files for IPO as Boston Scientific Secures an Option

H&H Healthcare

R&D and Producer of Interventional Medical Devices for Heart Disease

Boston Scientific

Medical Device Manufacturer

In late June 2026, Shanghai H&H Healthcare Technology Company Ltd. submitted its prospectus to the STAR Market, intending to adopt the fifth set of listing criteria.

Despite being only six years old, the company bears two strikingly contrasting labels. It holds a unique global registration certificate for its transcatheter tricuspid annuloplasty system, K-Clip—the only device approved to date in major global markets for tricuspid annulus reduction repair, and the sole product approved in China for transcatheter tricuspid valve intervention. Furthermore, Boston Scientific is willing to provide a RMB 10 million cash deposit solely to secure an exclusive right of first refusal for acquisition by the end of 2027.

Of course, what Boston Scientific is interested in is only H&H Healthcare's IVL business. H&H Healthcare's truly valuable product is the K-Clip tricuspid annuloplasty system. Although multinational giants Abbott's TriClip and Edwards' EVOQUE obtained FDA approval in the United States in 2024, H&H Healthcare's K-Clip had already been commercialized in China by March 2025 and had been adopted in over 100 top-tier tertiary hospitals before the submission of its listing application.

In the field of structural heart disease, competition in the aortic and mitral valve sectors has become fierce. Why did the first domestically produced registration certificate for tricuspid valves not emerge until 2025? What industrial opportunities lie within the tricuspid valve intervention market, known as the last blue ocean in structural heart disease? We can explore these insights through the prospectus.

The evolutionary logic of structural heart disease is straightforward: progressing from the aortic valve to the mitral valve and then to the tricuspid valve, each subsequent stage presents increasing difficulty.

The localization of TAVR for the aortic valve began earliest, with Venus Medtech's 2019 listing on the Hong Kong Stock Exchange serving as a landmark milestone. Companies such as Jiecheng and Peijia followed suit, completing multiple product iterations and navigating the full lifecycle from market launch to centralized procurement and international expansion, thereby solidifying the market landscape. The mitral valve has emerged as the current primary battleground, where companies like Hanyu, Dejin, and Enlight Medical are competing intensely in the edge-to-edge repair and replacement segments. With registration filings and clinical data advancing rapidly, these players are just one step away from a concentrated wave of market entries.

The tricuspid valve sector has long remained a blank slate, representing the industry's recognized final—and most challenging—piece of the puzzle.

The core developmental challenges stem from congenital anatomical structures: the tricuspid annulus exhibits an irregular saddle shape with significant variability in dilation and deformation, while right-sided hemodynamics and anatomical spaces are highly complex. Furthermore, tricuspid regurgitation (TR) has long been regarded as a secondary consequence of left-sided heart disease. Clinically, management has primarily relied on conservative pharmacological therapy and open-heart surgical procedures, leaving a lack of mature minimally invasive interventional solutions for an extended period.

According to data from the "2025 ESC/EACTS Guidelines for the Management of Valvular Heart Disease," the perioperative mortality rate of traditional open-chest tricuspid valve surgery is as high as 8%–10%, with a one-year mortality rate exceeding 30%. This represents a significant clinical gap.

The development of this sector has three distinct milestones: from 2019 to 2021, it was in an exploratory phase, with only a few small-sample clinical trials conducted in China; from 2022 to 2024, it entered a critical period for regulatory approval, during which multiple companies advanced their efforts simultaneously, yet no product obtained NMPA registration certification; in 2025, H&H Healthcare's K-Clip received approval, marking the official start of the commercialization era and serving as a turning point for the sector's development.

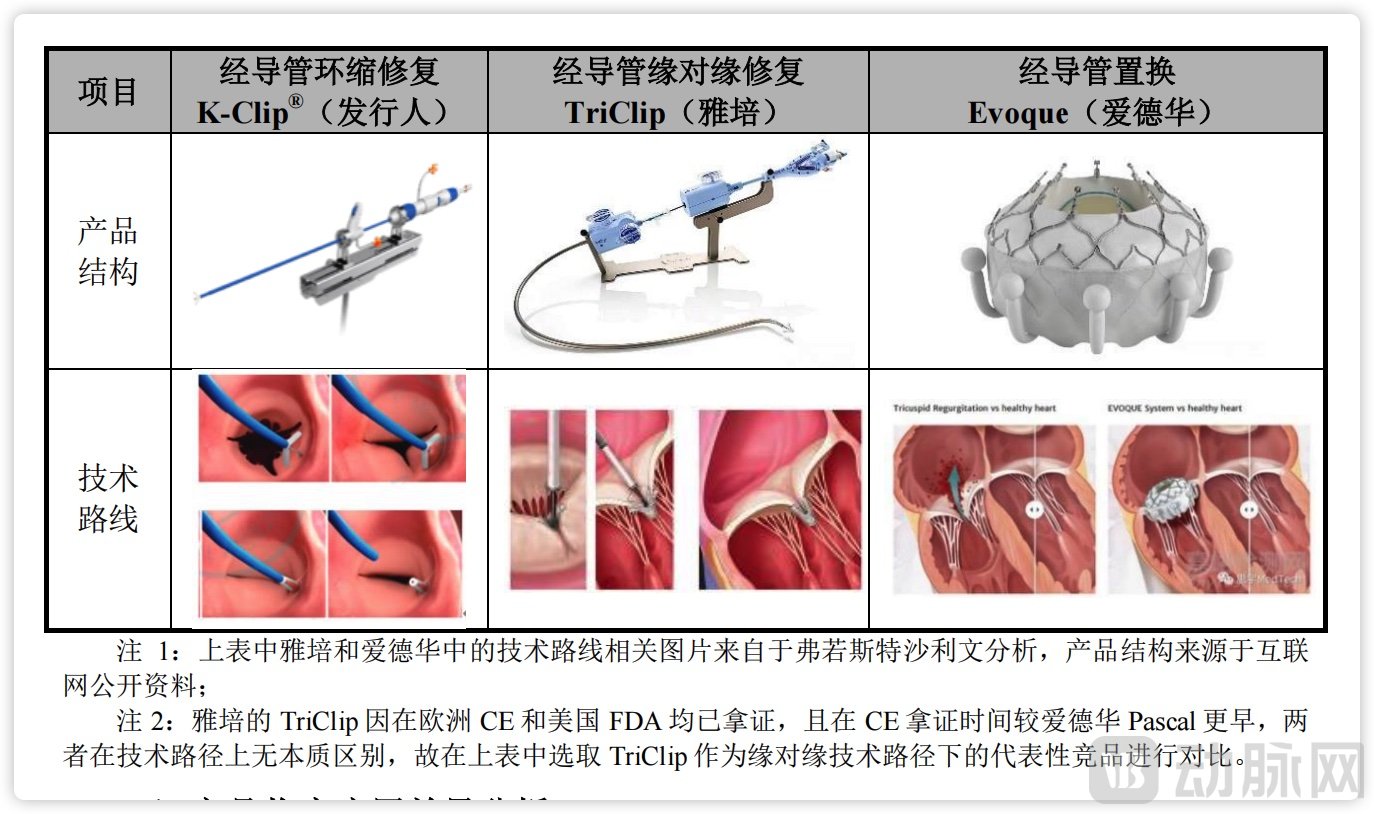

Among the major global regulatory markets (China, the United States, and Europe), only four adult transcatheter tricuspid valve intervention products have been approved.

Abbott's TriClip follows the transcatheter edge-to-edge repair (T-TEER) approach, receiving European approval in 2020 and U.S. FDA approval in 2024; Edwards' Evoque adopts the transcatheter tricuspid valve replacement (TTVR) approach, obtaining CE marking in 2023 and FDA approval in 2024; Edwards also offers Pascal, another T-TEER device, which was approved in Europe in 2022.

Comparison of Three Products, Source: Prospectus

H&H Healthcare's K-Clip is the only approved product worldwide utilizing the transcatheter tricuspid valve annuloplasty (TTVA) approach.

None of the three technical approaches is absolutely superior or inferior; they simply correspond to different anatomical indications. Edge-to-edge repair has strict limitations regarding leaflet coaptation gaps, valve replacement requires lifelong anticoagulation, whereas annuloplasty targets functional tricuspid regurgitation (accounting for over 80% of cases), theoretically covering a broader patient population.

In addition to H&H Healthcare, several other domestic companies have related products in clinical trials, with technologies largely benchmarked against overseas edge-to-edge repair and valve replacement approaches. These products are expected to receive centralized regulatory approval for market launch between 2027 and 2029, at which point competition in this sector will intensify rapidly.

H&H Healthcare's bold foray into the uncharted territory of annuloplasty is largely attributable to its founding team.

Founder Lin Lin is a former cardiologist at Ruijin Hospital; Chief Technology Officer Xu Jun served as General Manager of R&D at 3M China, spending 17 years in the multinational corporation's central laboratory; and Chief Operating Officer Liang Tao previously held sales responsibilities at multiple foreign medical device companies.

This is not a typical scientist-led startup, but rather a combination of clinical need insight, engineering implementation, and industrial resource integration. One understands pathology and knows that the real pain point of tricuspid regurgitation lies in annular dilation; one excels in engineering translation and can transform the surgical Kay's annuloplasty into an interventional device; and one is well-versed in channels and markets, knowing how to get the product into hospitals.

While many companies have chosen to follow Abbott's or Edwards' edge-to-edge repair or valve replacement pathways, H&H Healthcare has opted to restore the classic surgical approach. This strategic choice gives K-Clip several advantages: it reduces procedural time, features a short average device operation time, and has a shallow learning curve, making it physician-friendly for training; it preserves the native valve, eliminating the need for lifelong anticoagulation; and the procedure is reversible, allowing for repeated position adjustments before final deployment, thereby significantly reducing intraoperative difficulty.

Clinical data also demonstrate these design advantages.

One-year follow-up data from the TriStar study demonstrated that 94.2% of patients maintained at least a one-grade improvement in tricuspid regurgitation (TR) severity, with 82.5% achieving TR reduction to moderate or less. The heart failure rehospitalization rate decreased by 64.6%. Furthermore, 97.7% of followed-up patients attained NYHA functional class I or II status. The mean KCCQ score improved from 67.9 to 74.9, representing an approximate 10% increase.

Of course, a single product cannot sustain an entire company. Beyond the tricuspid valve, H&H Healthcare has also entered two additional fields: intravascular lithotripsy (IVL) and radiopaque tumor embolization microspheres.

Traditional imported microspheres cannot be visualized in real time during surgery, making it difficult to intuitively assess the embolization effect. H&H Healthcare Vispearl is China's first drug-eluting microsphere with imaging capability. It has successfully been included in and won bids for provincial alliance centralized procurement programs across 24 provinces, leveraging these procurement channels to rapidly penetrate grassroots hospitals and establishing a certain degree of differentiated competitive advantage.

In the field of intravascular lithotripsy (IVL), imported products are prohibitively expensive. H&H Healthcare's C-Wave is the first domestically produced IVL catheter in China to secure approvals for both peripheral and coronary indications, having been successively launched in 2023 and 2024. It addresses critical clinical challenges in PCI for severe vascular calcification, offering substantial potential for domestic substitution.

More importantly, in April 2026, Boston Scientific and H&H Healthcare signed an agreement, appointing Boston Scientific as the exclusive national distributor of H&H Healthcare's shockwave catheters in China. Meanwhile, Boston Scientific paid a RMB 10 million option fee to secure the right to acquire 100% equity interest in Suzhou Zhonghui, a subsidiary of H&H Healthcare, for a consideration of RMB 225 million by December 31, 2027.

Suzhou Zhonghui serves as the vehicle for H&H Healthcare's IVL catheter business. Boston Scientific not only assists H&H Healthcare in marketing its IVL products but may also directly acquire this business segment.

As a global giant in minimally invasive interventional procedures, Boston Scientific did not develop its own IVL technology but instead chose to partner with H&H Healthcare, indicating that H&H Healthcare's capabilities in this field have gained recognition. Meanwhile, Johnson & Johnson's Shockwave has long dominated the market, while numerous Chinese manufacturers are emerging, accelerating the trend of domestic substitution. By entrusting its IVL business to Boston Scientific in exchange for channel resources and cash, H&H Healthcare is concentrating its efforts on penetrating the tricuspid valve market.

From a commercialization perspective, K-Clip entered more than 100 end-user hospitals within nine months of its launch, including top-tier medical institutions such as Fuwai Hospital, Zhongshan Hospital, Ruijin Hospital, Anzhen Hospital, and Xiangya Hospital. However, insurance coverage remains limited, with reimbursement currently available only in select cities. This means that H&H Healthcare's short-term priority is not to defeat competitors, but to rapidly complete procedural education, physician training, and insurance market access to cultivate the market.

A look at H&H Healthcare's shareholder list reveals a clear relay of capital investment.

In the early stage, market-oriented institutions such as Oriza Holdings and BioTrack Capital supported the company through its technology validation phase. In the mid-stage, state-backed funds like Lingang Fund joined in. By December 2025, amidst a capital winter, Taiping Healthcare made a counter-trend additional investment and simultaneously acquired part of the equity from existing shareholders.

The entry of insurance capital warrants attention. Transcatheter tricuspid valve interventions target an elderly, high-risk patient population with multiple comorbidities, which aligns naturally with insurance payment scenarios. If future multi-tiered payment systems, including commercial insurance, can cover transcatheter tricuspid valve procedures, early strategic positioning will hold significant value. Furthermore, H&H Healthcare's innovation capabilities—particularly the originality of the K-Clip in pioneering a novel procedural approach, along with its platform-based capabilities in the pan-vascular intervention field—are key factors attracting such investment.

H&H Healthcare's revenues from 2023 to 2025 were RMB 2.8037 million, RMB 26.9882 million, and RMB 101.5448 million, respectively, marking explosive revenue growth; however, the company is not yet profitable.

The proposed fundraising amount is RMB 1.11 billion, of which RMB 430 million will be used to build a new production center and expand the production capacity for K-Clip, shockwave catheters, and microspheres; RMB 250 million will supplement working capital to support the promotion of K-Clip, thereby rapidly increasing revenue scale in the short term. RMB 210 million will be allocated to new product development, advancing the mid-term strategic plan to establish a comprehensive portfolio of structural heart intervention products, including K-Plus, Tri-Cap, and the two major components of the mitral valve system: L-Clip and D-Clip. Additionally, RMB 220 million will be invested in overseas clinical trials and regulatory registrations to prepare for long-term international market entry.

All four investment directions converge on a single objective: to convert first-mover advantage into revenue scale within the window period, while laying the groundwork for medium- to long-term strategic initiatives.