Xiangxue Pharmaceutical's $930M Restructuring: Is GPC Capital Targeting TCR-T, Not Traditional Chinese Medicine?

Xiangxue

Developer, Producer, and Seller of Traditional Chinese Medicine and Chinese Herbal Pieces

July 3,Xiangxue Pharmaceutical AnnouncementBu, GZPH CapitalSelected as the Successful Reorganization Investor。It has been over a year since it initiated restructuring.Xiangxue rose more than 7% at its peak during today’s opening session.

Xiangxue PharmaceuticalIt is a time-honored Guangzhou-based pharmaceutical enterprise with a 40-year history, over 61% of whose business consists of proprietary Chinese medicines, most of which are “National Protected Traditional Chinese Medicine Varieties.” For instance, products commonly stocked in households.Antiviral Oral Liquid, it is the first national-level new drug; the one you think of when your throat feels uncomfortableJuhong Series(including Juhong Tanke Liquid, etc.), it is an exclusive product in China and a cultural heritage of Lingnan traditional Chinese medicine, originating from the "Er Chen Tang" formula in the Song Dynasty's "Tai Ping Hui Min He Ji Ju Fang."

Guangyao CapitalIt is a capital platform wholly established by Guangzhou Pharmaceutical Holdings Limited in 2026, with a registered capital of RMB 2 billion, focusing on industrial investment and mergers and acquisitions in the pharmaceutical and healthcare sectors.

Winning the bid only means that Guangzhou Pharmaceutical Capital has obtained the priority negotiation qualification. The entry of state-owned assets or central enterprises is not a guarantee either. For example, this year marks the sixth year since the central enterprise Xinxing Jihua Group took control of Hainan Haiyao Co., Ltd.July 6 (Today)Hainan Haiyao Co., Ltd. Issues Announcement on Abnormal Stock Trading Fluctuations: The Company Reports a Half-Year Loss, Projecting Negative Net Assets. According to Shenzhen Stock Exchange regulations, consecutive years of negative net assets will result in delisting. Relying solely on Fengliao Changweikang Granules, developed in the 1970s, has failed to drive the company’s forward development.

Xiangxue Pharmaceutical reported an audited net assets attributable to shareholders of the listed company of -360 million yuan for 2025, meaning that if the figure remains negative in 2026, it will be the first to trigger a "delisting" alert.

01

The Open Cards of Listed Traditional Chinese Medicine Companies

For valuable private traditional Chinese medicine enterprises, state-owned capital takes over when they fall into distress,There have also been many related cases in the past three years. For example, in August 2024,China Resources SanjiuProposed AcquisitionTasly28% equity stake, with a total transaction value of approximately RMB 6.2 billion. In December 2025,TaiLong PharmaceuticalDisclosure, with a background in Jiangxi State-owned AssetsJiangsu Pharmaceutical HoldingsThrough a combination of "agreement transfer + private placement," with an investment of over RMB 1 billion to take control, the company's actual controller has changed to the State-owned Assets Supervision and Administration Commission of Jiangxi Province.

The main problem with Xiangxue Pharmaceutical is that,Declining revenue from traditional Chinese medicine operations, high debt levels, and non-compliant corporate governance.

Actually,Since 2020, Xiangxue Pharmaceutical has been under continuous operational pressure, with debt risks gradually emerging.As of the end of 2025, its total liabilities amounted to approximately RMB 6.7 billion, with an asset-liability ratio of 99.35%. The company has reported losses for five consecutive years, with the net loss in 2025 further widening to RMB 1.392 billion. The primary reasons for the losses were intensified market competition coupled with a liquidity crisis, which led to underperformance in the sales of traditional Chinese medicine (TCM) proprietary products.

Furthermore, governance and compliance risks have emerged. In 2024, the company was fined RMB 1 million by the Guangdong Provincial Medical Products Administration and had its illegal gains confiscated for producing Banlangen Granules that failed to meet standards, severely damaging its brand reputation. In 2025, it was collectively fined RMB 6 million by the China Securities Regulatory Commission (CSRC) and the Guangdong CSRC Bureau for false records in its 2019 annual report and failure to disclose misappropriation of funds by related parties; Wang Yonghui, the actual controller, was subjected to a market entry ban.

As of February 2026, in addition to the disclosed litigation, Xiangxue Pharmaceutical and its subsidiaries were defendants in a total of 22 undisclosed cumulative lawsuits over a consecutive twelve-month period, with the total amount involved reaching RMB 92.2656 million, primarily concerning contract disputes.

In January 2025, the creditor Guangdong Jinglong Construction submitted an application for pre-restructuring to the Guangzhou Intermediate People's Court, citing Xiangxue Pharmaceutical’s inability to repay due debts and its obvious lack of solvency, thereby formally embarking on the path of restructuring.

Subsequently, the pre-restructuring period was extended four times and has now been extended to July 11, 2026.

In February 2026, Guangzhou Xiangxue Pharmaceutical Co., Ltd. applied to Guangdong Nanhai Rural Commercial Bank Co., Ltd. for a one-year loan facility totaling RMB 437.4 million. In April 2026, the company decided to publicly solicit restructuring investors, and after more than two months of selection,Guangzhou Pharmaceutical Capital ultimately prevailed.

This is not the first time Guangzhou Pharmaceutical Holdings Limited has restructured local pharmaceutical enterprises.

In 2021, Kangmei Pharmaceutical entered bankruptcy reorganization proceedings due to financial fraud. Led by Guangzhou Pharmaceutical Holdings Limited, a consortium including multiple financial investors contributed a total of RMB 6.5 billion to participate in the reorganization, becoming the controlling shareholder of Kangmei Pharmaceutical. This case ranks among the largest listed company reorganizations in the history of China’s A-share market.

Following the completion of its restructuring, Kangmei Pharmaceutical gradually emerged from its operational crisis. The company successfully turned a profit in 2023, with revenue further increasing to RMB 5.252 billion in 2025 and net profit attributable to shareholders reaching RMB 10.328 million.

The successful restructuring of Kangmei has provided Guangzhou Pharmaceutical Holdings Limited (GPHL) with relevant experience. However, what differs in this case is that the entity taking over Xiangxue is GPHL Capital, a wholly-owned subsidiary of GPHL, with the Guangzhou Municipal People’s Government as the ultimate actual controller.Positioned as an industrial investment platform that “serves the Group’s strategy and empowers industrial development,”The goal is to achieve a merger and acquisition investment scale of no less than RMB 20 billion by the end of the "15th Five-Year Plan" period, with the scale of funds under management being no less than RMB 10 billion.

The market generally believes that Guangzhou Pharmaceutical Holdings Limited’s recent move is not merely to support Xiangxue’s dwindling traditional Chinese medicine foundation, but may also be driven by its TCR-T cell therapy pipeline.

02

The True Intentions of Guangzhou Pharmaceutical Holdings Limited

In 2024, the U.S. FDA approved the world’s first and currently only T-cell receptor (TCR) gene therapy—Adaptimmune’s Tecelra (afamitresgene autoleucel)—for the treatment of adults with unresectable or metastatic synovial sarcoma who have previously received chemotherapy.

Compared with CAR-T, TCR-T equips T cells with a “molecular microscope,” enabling them to scan and recognize tumor signals within cells, thus achieving more rapid breakthroughs in the field of solid tumors. Following the approval of the first TCR-T product, a global investment surge in the TCR-T sector was immediately triggered.Xiangxue’s stock price once climbed to a five-year high of RMB 16.5 per share in October 2024, but has since fallen by nearly half from that peak.

According to incomplete statistics, there are more than 17 companies in China that have laid out TCR-T cell therapy, most of which have already entered the clinical research stage;However, Xiangxue is making the fastest progress.

Currently, all three of its products have obtained Investigational New Drug (IND) approval in China. TAEST16001 injection is poised to become the first TCR-T cell therapy product approved for marketing in China and the second globally.

It primarily relies on Xiangxue Life Sciences’ comprehensive TCR-T technology platform and manufacturing processes, supporting the research and development of high-specificity, high-affinity TCR-T cell immunotherapy products for malignant solid tumors.

In 2026, Guangyao Capital made frequent moves after its establishment.MayAcquired a controlling stake in Da An Gene for approximately RMB 2.418 billion, completing the layout of the in vitro diagnostics segment;JulySelected as the restructuring investor for Xiangxue Pharmaceutical.Within just six months, it successively acquired controlling stakes in two listed companies, completing its industrial layout from diagnosis to treatment.

Da An Gene holds over 70% of the domestic PCR diagnostics market share in China and was acquired by Guangzhou Pharmaceutical Holdings Limited, a state-owned enterprise, when its valuation was at a low point following consecutive years of losses. Therefore, from a macro perspective, this move may also represent a strategic step by Guangzhou’s state-owned assets to build a pharmaceutical industry cluster.

Revitalizing distressed listed pharmaceutical companies through restructuring not only avoids the series of negative impacts associated with delisting, but also enables the acquisition of high-quality industrial assets at a relatively controllable cost.

03

# Innovation and Compliance Are Essential for the Survival of Traditional Chinese Medicine Enterprises

There is still significant demand for traditional Chinese medicine, particularly proprietary Chinese medicines, in China's pharmaceutical market.According to data from Menet, in the first three quarters of 2025, Chinese patent medicines still accounted for nearly 36.30% of sales in urban physical pharmacies in China;Urban communities: Chinese patent medicines account for over 40%; In urban public hospitals, the proportion of Chinese patent medicines has remained stable at around 15%.

The operational difficulties faced by Xiangxue Pharmaceutical are also common issues in the transformation of traditional Chinese medicine enterprises.

To seek new growth drivers, many traditional Chinese medicine enterprises have chosen to transform into the innovative drug sector, such as cell therapy and biologics. However, the high investment required for innovative R&D conflicts with the traditional profit models of these Chinese medicine companies.

Traditional businesses of Chinese herbal medicine enterprises often rely on high-volume, low-margin sales, resulting in relatively stable cash flows that are insufficient to sustain the substantial, continuous investment required for innovative drug R&D. Should issues arise in internal controls or financing, the capital chain is prone to rupture, plunging the company into a predicament where “innovation remains unfinished while the core business has already declined.”

Furthermore, compliance issues have become increasingly prominent. The National Audit Office released the “Report of the State Council on the Audit Work Regarding the Implementation of the Central Budget and Other Fiscal Revenues and Expenditures for 2025,” which included investigations into 66 traditional Chinese medicine (TCM) production and distribution enterprises across 10 provinces and 28 medical institutions. Issues involving a total amount of RMB 4.652 billion were identified, with the main problems including:

Some pharmaceutical companies are driving up drug prices.By fabricating procurement information to falsely issue purchase invoices totaling RMB 2.281 billion, thereby inflating costs; additionally, RMB 2.25 billion in sales expenses with no underlying genuine business transactions were paid to promoters and subsequently funneled back to the company;

A Small Number of Pharmaceutical Companies Still Engage in "Kickback-Driven Sales" Practices. By inflating costs and fabricating expenses to embezzle RMB 4.25 billion, part of which was used for kickback-driven sales;

Some medical institutions erode the benefits of medical insurance and policy dividends.Six institutions engaged in high-priced procurement by leveraging the 25% markup rule on the purchase price of traditional Chinese medicine (TCM) decoction pieces, collectively imposing an additional burden of over RMB 150 million on patients and the medical insurance fund.

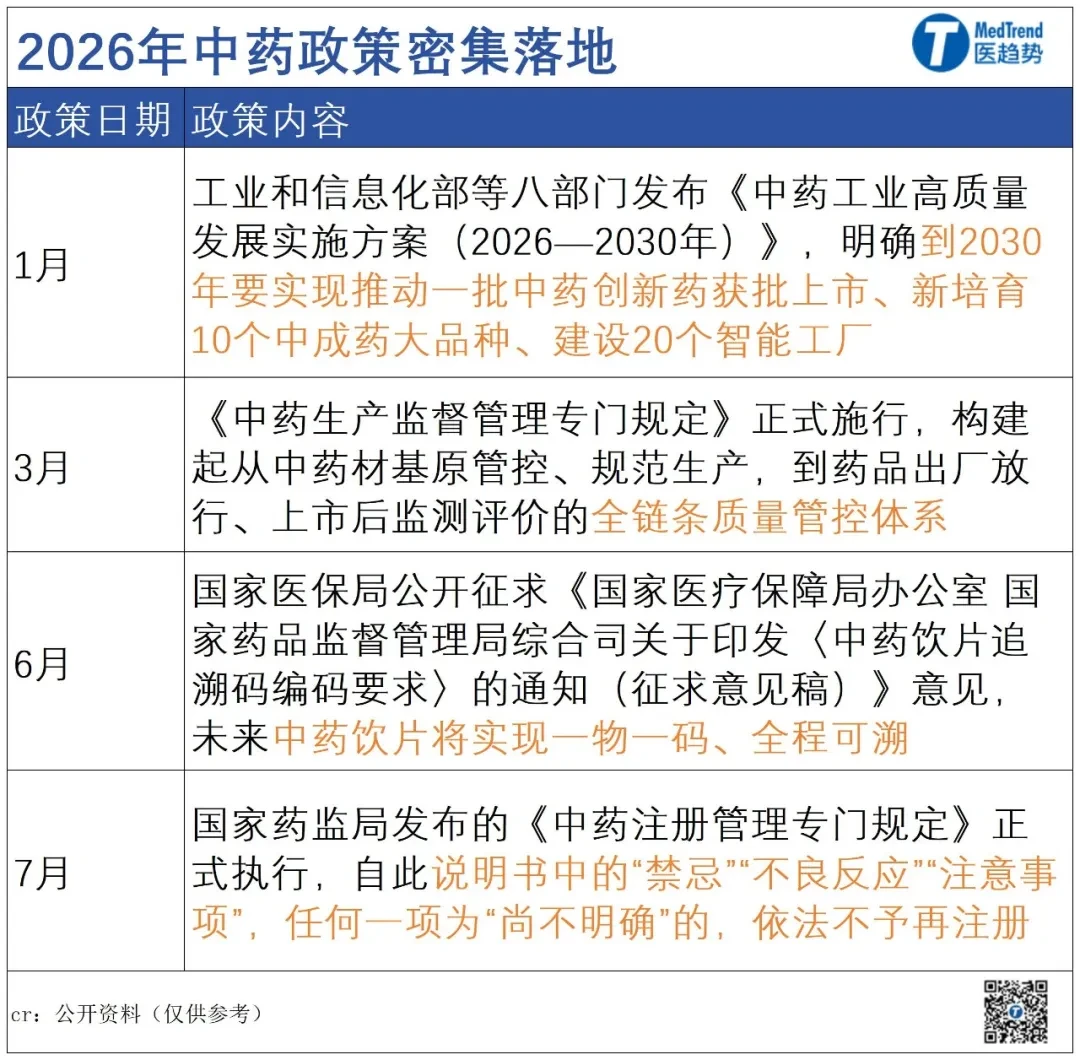

As a national treasure of China, traditional Chinese medicine (TCM) has always received state support for its development. Judging from the intensive policies issued this year—ranging from quality control in raw material production and post-market traceability to the refusal to register previously non-compliant products—only truly high-quality and compliant products will be able to enter the market in the future.