Big Pharma's Strategic Retreat in China: Offloading Commercial Assets While Doubling Down on Innovation

Innovent

High-end Biologics Developer

GSK

Pharmaceutical R&D Manufacturer

CHIATAI TIANQING

High-quality pharmaceuticals research, production, and sales provider

Recently, a collaboration agreement between Eli Lilly and Innovent has once again stirred the pharmaceutical industry.

Eli Lilly has officially transferred the exclusive commercialization rights for its CDK4/6 inhibitor abemaciclib in mainland China to Innovent. The latter will assume full responsibility for importation, sales, promotion, and omnichannel distribution, while Eli Lilly retains only its status as the Marketing Authorization Holder (MAH), along with manufacturing supply and global R&D leadership.

The intense scrutiny surrounding this deal stems primarily from the fact that, historically, multinational pharmaceutical companies have mostly out-licensed mature, off-patent generic drugs included in centralized procurement; whereas this time, it isInnovative Targeted Drugs That Are Marketed, Covered by National Reimbursement Drug List (NRDL), and Still Within Their Peak Sales Period. Coincidentally, in May this year, GSK also licensed the commercialization rights for its potential blockbuster product, Bepirovirsen, in China to CHIATAI TIANQING.

“The narrative of ‘multinational pharmaceutical companies fully retreating from China’ has resurfaced. However, if we piece together the more than one hundred transactions over the past three years, it clearly cannot be categorized as a withdrawal. More accurately, this is a precise structural restructuring:”Accelerated Divestment of Mature Businesses, Tiered Management of Innovation Pipeline, and Reverse Heavy Investment in R&D. Three parallel threads, essentially a strategy of “vacating the cage to change the bird,” rather than a complete exit.

Innovative Drugs Hit the Shelves

The upgrade of licensed products from off-patent drugs to innovative medicines is a clear signal sent by MNCs, but this does not mean they are abandoning the Chinese market. Nowadays, MNCs have already begunImplement a tiered strategy in China, with refined business management, based on product life cycle, competitive landscape, and strategic priorities.。

The first wave of large-scale transfers involved mature products with continuously deteriorating return on investment, representing the most prominent industry trend over the past three years. From Pfizer’s fluconazole, palbociclib, and crizotinib, to Boehringer Ingelheim’s pucrasol and dabigatran etexilate, and Roche’s rituximab, these licensed assets share highly consistent characteristics: their patents have expired or are nearing expiration; most have been included in China’s national centralized procurement programs; they face direct competition from domestically produced generic drugs or biosimilars; and their pricing and profit margins continue to be compressed.

As the revenue foundation supporting a self-operated team of hundreds continues to erode, divesting asset-heavy segments such as distribution and promotion to domestic commercial giants like Sinopharm, China Resources Pharmaceutical, Shanghai Pharmaceuticals, and Baiyang, and leveraging their extensive downstream networks and cost advantages to maintain market share, represents a typical cost-reduction and efficiency-enhancement strategy, as well as a standard industry practice.

The true variable is that innovative drugs have begun to enter the authorization list., covering both marketed blockbuster products and first-in-class new drugs nearing launch. In addition to abemaciclib, two transactions are particularly landmark: GSK’s GSK836, a small nucleic acid drug for the functional cure of hepatitis B that is on the verge of launch.(Bepirovirsen), the exclusive commercialization rights in mainland China were fully granted to CHIATAI TIANQING; Novartis handed over the exclusive promotion rights in mainland China for two innovative ophthalmic biologics, ranibizumab and brolucizumab, to CMS Pharmaceutical.

However, this batch of innovative drug licenses also has clear boundaries, basically conforming to three characteristics:

The first category isProducts in the sector that have entered a red ocean of competition. Abemaciclib is a typical representative; multiple products have entered the CDK4/6 sector in China, intensifying price wars and shifting the market from a period of rapid growth to competition for existing market share. At this stage, entrusting Innovent’s oncology commercialization team to penetrate lower-tier markets and control operational costs yields a better return on investment than maintaining a high-cost in-house sales force.

The second category isProducts with high reliance on local specialty channelsGSK836 selected CHIATAI TIANQING, with the core rationale being that the latter possesses a deep network covering thousands of medical institutions in China’s liver disease field. Its deeply entrenched local advantages in hospital access, expert resources, and patient education cannot be replicated by foreign companies’ self-built teams in the short term.

The third category isProducts Outside the Global Core Strategic Therapeutic Areas. For niche segments with limited market size, such as ophthalmology and rare cancers, building dedicated in-house teams is not cost-effective; partnering with local companies specializing in these fields is a more agile and efficient option.

Meanwhile, there is a red line that has never been crossed:Global Blockbuster Drugs in Their Prime Growth Phase: MNCs Invariably Retain Firm Control。

For instance, in the GLP-1 sector, Eli Lilly’s tirzepatide and Novo Nordisk’s semaglutide are rapidly expanding in the Chinese market; rather than outsourcing, these companies are continuously enlarging their commercialization and medical teams. In the oncology field, Merck’s pembrolizumab, AstraZeneca’s osimertinib and trastuzumab deruxtecan(Co-developed with Daiichi Sankyo), all operated by in-house teams, with the neoadjuvant indication for early-stage breast cancer of UHERD achieving its global debut in China; forward-looking pipelines in autoimmune diseases and rare diseases are also largely maintained under self-operated models.

In short, what is divested comprises products for which outsourcing is more cost-effective than in-house production, while what is retained constitutes the core assets that truly drive high growth and high profitability.

The Rules of the Chinese Market Have Changed

The intensive adjustments by multinational pharmaceutical companies in China stem fromSystemic Restructuring of the Chinese Market Environment. The direct driver is the change in the operating rules of China's pharmaceutical market over the past five years.

First, it isRigid Restructuring of the Pricing SystemAccording to publicly available data from the National Healthcare Security Administration, the average price reduction under national centralized procurement has exceeded 50%, and the annual average price cut in medical insurance negotiations has remained in double digits, thereby breaking the long-standing “import premium” logic relied upon by originator drugs. Not only have profit margins for mature drugs narrowed, but prices of innovative drugs are also significantly reduced after inclusion in the medical insurance coverage, continuously eroding the profit foundation that supports large-scale self-operated sales teams.

Secondly, it isThe Accelerating Impact of Domestic SubstitutionCompetition has extended from generic drugs to innovative therapeutics, giving rise to a unique “commercial patent cliff”: although global patents for many drugs are far from expiration, their commercial value has eroded prematurely due to the entry of domestically produced competitors and price reductions under national medical insurance programs. In 2025, Sanofi discontinued Plavix(Alirocumab Injection)supply in the Chinese market, but its global patent will not expire until 2028; the supply halt is mainly due to global supply issues, as well as the company’s cardiovascular market strategy and pipeline optimization.

Third, it isChannel Access Advantages of Domestic EnterprisesMultinational pharmaceutical companies excel in top-tier academic promotion and coverage of tertiary hospitals; however, in the “last mile” aspects—such as penetration into county-level markets, expansion of out-of-hospital channels, liaison for medical insurance affairs, and efficiency in hospital formulary access—domestic enterprises offer lower costs, higher efficiency, and greater flexibility. This comparative advantage is difficult for foreign-funded companies to bridge by building their own teams.

Fourth, isResetting Global Strategic PrioritiesAround 2020, the China region served as the primary global growth engine for most multinational pharmaceutical companies, with growth rates generally exceeding the global average. By 2025, the growth rates in the China operations of several leading pharmaceutical companies no longer led the global market. As high-growth emerging markets transition into mature markets, the logic governing resource allocation by global headquarters naturally adjusts accordingly.

Looking globally, Japan has also experienced the full transition from direct operations by multinational pharmaceutical companies to a local agency model. However, its trajectory is entirely opposite to that of China: Japan adopted the agency model from the outset of market access as a passive choice, whereas China first went through a “golden age” of fully direct operations from 2010 to 2020 and is now beginning a structural contraction as an active efficiency adjustment.

The fundamental logic of the pharmaceutical industry remains unchanged: market size and profit margins determine the depth of direct commercial operations. As the largest and most profitable markets globally, the United States and the core four European countries see multinational pharmaceutical companies predominantly relying on in-house commercial teams, with core products never entrusted to third parties. Pure agency models are generally adopted only in small-to-medium-sized countries and underdeveloped markets. Japan stands as the sole exception among major developed markets, a unique outcome of its specific historical and institutional context, and is not replicable elsewhere.

MNCs’ Reverse Bets in China

If one focuses solely on multinational corporations (MNCs) divesting assets and licensing out rights in China, it is easy to conclude that they are retreating. However, another more critical clue is often overlooked:Multinational pharmaceutical companies are acquiring Chinese innovative assets with unprecedented intensityThis is not merely an improvement in efficiency, but a strategic asset reallocation: divesting low-margin commercialized businesses to heavily invest in high-potential innovative assets.

Multiple institutions predict that 2025–2030 will witness a concentrated wave of patent expirations in the global pharmaceutical industry, affecting sales volumes at the scale of hundreds of billions of dollars. Major players such as Takeda, GSK, and Sanofi are allGlobal restructuring, divestment of non-core assets, and streamlining of commercial teams to concentrate resources on late-stage innovative pipelines constitute the broader global context for multinational pharmaceutical companies’ strategic adjustments in China.

China’s market also features a unique “commercial cliff”: while patent protection remains in force, national reimbursement negotiations and competition from domestically produced alternatives have already driven product profits to their nadir. The compounding effect of these dual pressures has accelerated the business restructuring of multinational pharmaceutical companies in China. So-called localization is not, in essence, a “concession and retreat,” but rather an industrial division of labor based on comparative advantage—Multinational pharmaceutical companies focus on global R&D and clinical development, while domestic enterprises handle market access and commercialization in China., each focusing on their respective areas of expertise to achieve optimal overall efficiency.

What most effectively refutes the “abandoning the China market” narrative is the surging wave of reverse licensing. While multinational pharmaceutical companies divest low-margin mature businesses, they are simultaneously acquiring Chinese innovative assets with unprecedented intensity. China has thus evolved from a mere “sales market” into one of the core sources of global innovation.

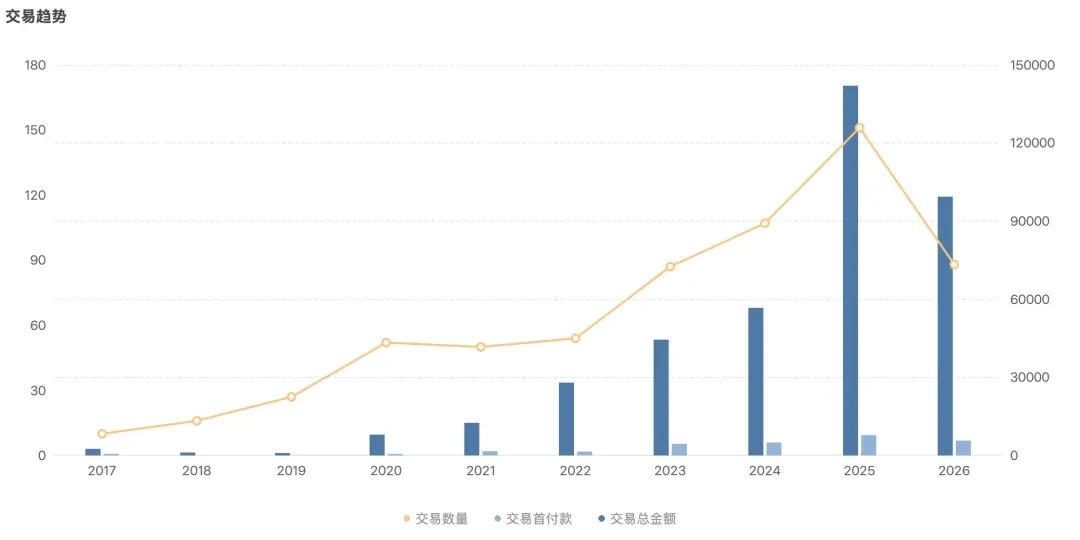

Total Value of Out-licensing Deals for Innovative Drugs in China in 2025, According to the Insight DatabaseExceeding $140 Billion, surpassing the United States for the first time; the total transaction value in the first half of 2026 has already approached two-thirds of the full-year total for 2025. The scope of transactions has also expanded from single late-stage projects to early-stage pipelines, technology platforms, and even joint research and development.

Source: DXY Insight Database

Landmark deals clearly outline the trend. In July 2025, GSK licensed the overseas rights to HRS-9821, a novel drug for chronic obstructive pulmonary disease (COPD) from Jiangsu Hengrui Pharmaceuticals, along with options for 11 additional projects, for an upfront payment of $500 million and potential milestones totaling up to $12 billion. In May 2026, Bristol Myers Squibb (BMS) and Hengrui reached a strategic collaboration valued at up to $15.2 billion, featuring a two-way exchange of 13 early-stage pipelines, representing a typical asset swap. In the same month, Pfizer entered into a global collaboration with Innovent Biologics on 12 early-stage oncology projects, covering cutting-edge technologies such as antibody-drug conjugates (ADCs) and multispecific antibodies, with an upfront payment of $650 million and potential milestones totaling up to $9.85 billion.

Meanwhile,Investment in production and R&D continues to increase.: Eli Lilly plans to invest $3 billion over ten years to expand its oral GLP-1 production capacity in China, while Roche and Novartis continue to expand their early-stage R&D centers.

On one hand, subtracting by divesting low-margin, asset-heavy commercialization segments; on the other, adding by heavily investing in high-potential innovative assets and production capacity. This is not a retreat, but a standard case of “vacating the cage to change the bird.”

Conclusion

The patent cliff is a global phenomenon, while localization is a strategic choice for efficiency. Multinational pharmaceutical companies are not exiting the market; instead, they are deepening their ties with China’s pharmaceutical industry by in-licensing innovative assets. The ultimate outcome of this transformation will not follow a binary narrative of “foreign exit and domestic takeover.” Rather, a mature division of labor is more likely to emerge: mature drugs and non-core innovative products will undergo deep localization through local channels, while global blockbuster innovations will continue to be marketed via direct operations. In R&D, bidirectional licensing and joint development will become the norm.

The Role of China’s Pharmaceutical Industry Is Quietly Shifting from a Market Taker to a Co-builder of the Global Innovation Ecosystem. This May Be the More Significant Underlying Change Worth Monitoring, Beyond the Question of “Whether the Tide Is Receding.”

References:

1. Official WeChat accounts and official websites of various pharmaceutical companies

2. DXY Insight Database