China's Leading Artificial Heart Maker CoreMed Halts IPO Amid $70M Losses Over Three Years

Core Medical

Artificial Heart Series Product Developer

Source: Medical Device Business Review

Author: Qiuqiu

The First Domestic Artificial Heart Stock

IPO Put on Hold!

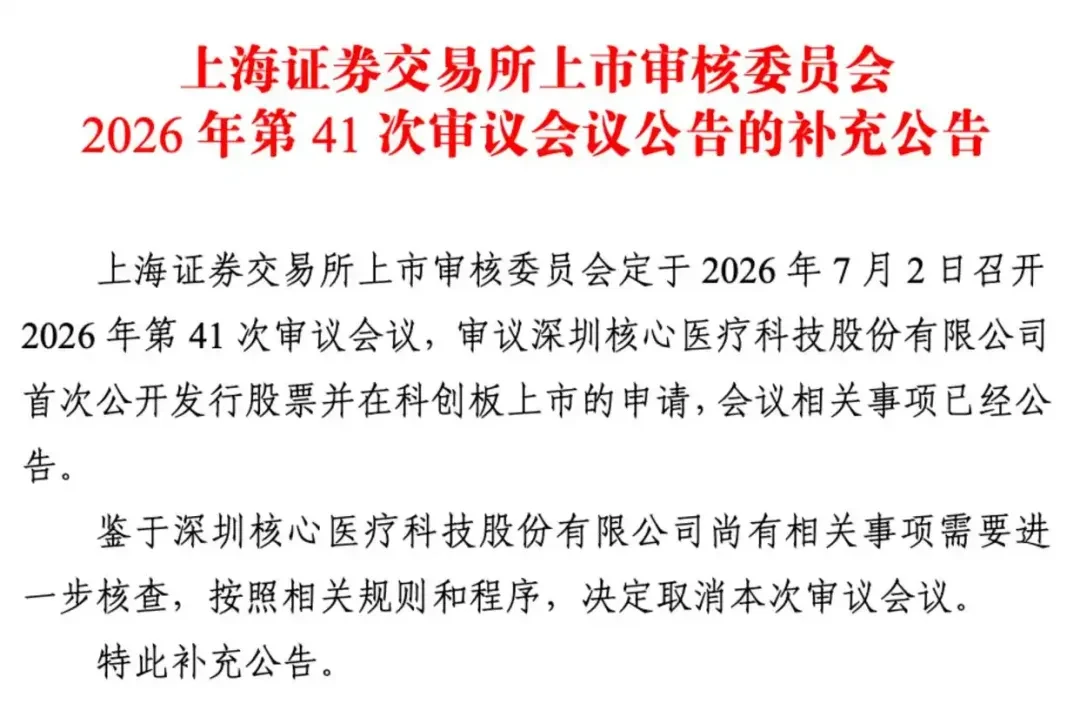

June 30, the Listing Committee of the Shanghai Stock ExchangeCancellation of Core Medical’s IPO review meeting originally scheduled for July 2,The reason is that "there are still related matters that require further verification."

This is not an IPO termination.

But it has brought a sharper question to the forefront:Core Medical has already developed and commercialized domestically produced artificial hearts, so why does the capital market continue to raise questions?

The answer does not lie in the product’s lack of rigidity.

On the contrary, Core Medical is one of the leading players in the domestic artificial heart sector:The fully magnetically levitated implantable artificial heart, Corheart 6, has achieved large-scale commercial sales, and the interventional ventricular assist device, CorVad 4.0, has also received regulatory approval.

The challenge is not whether products exist, but whether artificial hearts—a category that is technology-intensive, center-dependent, service-heavy, and payment-reliant—can truly evolve into a sustainable business.

No. 1 in Market Share!

What Makes the Leading Domestic Artificial Heart Manufacturer Stand Out?

Core Medical's flagship product, Corheart 6, is a fully magnetically levitated implantable left ventricular assist system.

Its value lies not merely in the label of “domestically produced artificial heart,” but in the fully magnetically levitated technology pathway itself. Compared with traditional mechanical bearing pumps, the magnetic levitation structure reduces mechanical contact and friction, helping to lower the risks of blood damage, thrombosis, and mechanical wear, making it more suitable for long-term circulatory support scenarios.

In the treatment of end-stage heart failure, artificial hearts can serve as a bridge to heart transplantation or as a long-term support option for patients who cannot wait for a donor.Due to the long-standing shortage of heart donors, the clinical value of such products is very clear.

The prospectus shows that Corheart 6 was approved for market launch by the National Medical Products Administration in June 2023, and commercial sales began in August of the same year. Sales volumes from 2023 to 2025 were 57 units, 379 units, and 684 units, respectively.In terms of terminal implantation volume, the national market share in China exceeded 45% in 2024, ranking first in the industry.

This demonstrates that Corheart 6 has successfully bridged the critical gap from regulatory approval to clinical application.

Another card in Core Medical’s portfolio is CorVad 4.0.

If the Corheart 6 addresses long-term circulatory support for patients with end-stage heart failure, the CorVad 4.0 targets interventional, short-to-medium-term ventricular assist scenarios.

Such products are typically used in critical and life-threatening scenarios, including high-risk percutaneous coronary intervention (PCI), cardiogenic shock, and perioperative circulatory support, providing temporary mechanical circulatory support via percutaneous interventional approaches. Their clinical rationale differs from that of implantable artificial hearts: rather than being implanted long-term, they assume part of the heart’s pumping function during the patient’s most critical window, thereby buying time for interventional therapy, myocardial recovery, or subsequent treatment steps.

CorVad 4.0 was approved for market launch in December 2025, signaling that Core Medical is expanding from a single implantable artificial heart to a broader circulatory support platform.

This step is critical. Although the implantable artificial heart market holds high value, patient selection is stringent and center expansion is slow. While interventional ventricular assist devices also present high barriers to entry, they offer opportunities to access higher-frequency scenarios for emergency and critical care support.

What Core Medical truly aims to convey is not merely an artificial heart, but a circulatory support platform encompassing both long-term implantable and short-to-medium-term interventional devices.

Losses of Nearly 500 Million Over Three Consecutive Years!

Can Core Medical's IPO Successfully Pass the Review?

Core Medical's revenue is growing rapidly, but losses have not disappeared either.

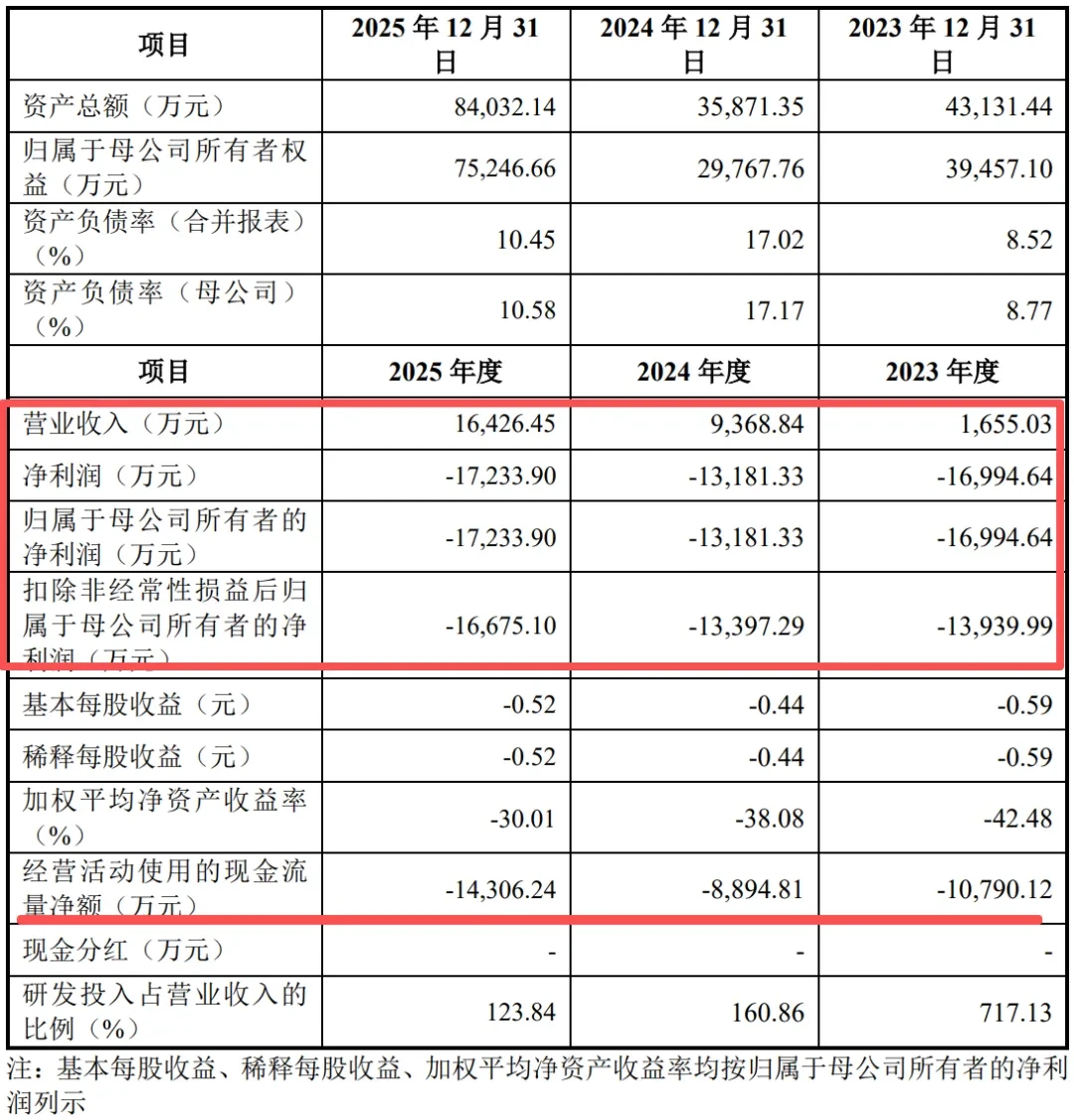

From 2023 to 2025, the company's revenue grew from RMB 16.5503 million to RMB 164 million, nearly a tenfold increase over three years;However, the net profit attributable to shareholders of the parent company for the same periods was RMB -170 million, RMB -132 million, and RMB -172 million, respectively.In other words, despite its 2025 revenue exceeding RMB 100 million, the company still returned to an annual loss level of nearly RMB 170 million.

This is not simply a case of "poor sales."

Artificial hearts are fundamentally different from ordinary consumables. Behind each device lies a comprehensive framework encompassing patient selection, preoperative assessment, intraoperative support, postoperative follow-up, anticoagulation management, infection control, and device maintenance. Manufacturers must do more than simply deliver products to hospitals; they must also engage in the long-term development of clinical care systems.

This category inherently carries a heavy commercialization burden and is naturally capital-intensive.

The most direct pressure behind the losses is the high investment in both R&D and sales.

2023 to 2025,The company's R&D investments were RMB 119 million, RMB 151 million, and RMB 203 million, accounting for 717.13%, 160.86%, and 123.84% of its operating revenue, respectively.Although the proportion decreases with revenue growth, the absolute amount of R&D expenditure continues to rise.

Selling expenses are also not low. In 2025,The company's sales expenses reached RMB 65.737 million, with a sales expense ratio of 40.02%.This is not merely “sales personnel expenses”; it also encompasses long-term investments such as clinical education, center development, surgical support, patient management, and after-sales service.

Therefore, Core Medical’s losses are not due to a single cost overrun, but rather reflect the dual burden of upfront R&D investment and early-stage market education that artificial heart companies must bear during the initial phase of commercialization.

The question is whether the capital market will continue to ask: When will these investments be diluted by scaled-up revenue?

The biggest issue facing Core Medical is not a lack of revenue, but rather an insufficiently robust revenue structure.

During the reporting period, the Company's revenue was derived entirely from Corheart 6.Corheart 6 sales increased from 57 units to 684 units,This demonstrates that there is a market for domestically produced implantable artificial hearts; however, it is difficult for a single product to sustain an artificial heart platform company with high R&D and sales investments over the long term.

Moreover, the average selling price (ASP) of Corheart 6 decreased from RMB 290,400 per unit in 2023 to RMB 240,200 per unit in 2025. Downward pricing pressure, front-loaded expenses, and concentrated revenue recognition will all impact the subsequent profitability trajectory.

Therefore, the significance of CorVad 4.0 extends far beyond “just another registration certificate.”

It determines whether Core Medical can upgrade from a single implantable artificial heart company to a circulatory support platform company.If CorVad 4.0 can penetrate higher-frequency scenarios such as high-risk PCI, cardiogenic shock, and perioperative support, Core Medical will have the opportunity to shift its revenue structure from single-product volume growth to a multi-product relay model.

But before that,Annual losses exceeding RMB 100 million for three consecutive years will remain a core issue that cannot be bypassed in IPO reviews and within the capital market.

The Competition for Domestic Artificial Hearts!

From Certification to Systemic Capability

Domestic artificial hearts have moved beyond the stage of “whether there are domestic products.”

In the field of implantable ventricular assist devices (VADs), products such as Core Medical’s Corheart 6, Tongxin Medical’s CH-VAD, and Yongrenxin’s EVAHEART have propelled domestically produced artificial hearts into real-world clinical application. The true competition ahead lies not merely in technical specifications and regulatory approvals, but in which companies can gain entry into more leading cardiac centers and establish more mature systems for surgeon training and patient management.

An artificial heart is not a product whose lifecycle ends with a one-time implantation.

Postoperative follow-up, patient management, complication management, and equipment maintenance will all become part of a company’s long-term competitive strategy.

Interventional Ventricular Assist Devices Are Emerging as a Second Mainstream Therapy.

Core Medical’s CorVad 4.0 has received approval, and Fengkaili’s SynFlow 3.0 has also been approved for market launch by the NMPA. With the commercialization of domestically produced pVAD products, the short- to medium-term mechanical circulatory support market is beginning to heat up.

The clinical landscape behind this track is broader: high-risk PCI, cardiogenic shock, acute heart failure, and perioperative support may all serve as incremental entry points.

However, the broader scope also leads to more complex competition. Companies must compete not only on product performance but also on clinical pathways, physician education, hospital access, and evidence accumulation.

Core Medical’s suspension of its listing review serves as a wake-up call for the entire sector: artificial heart companies must not only highlight “product approval” but also demonstrate their ability to integrate products into real-world clinical systems and sustain revenue generation.

Core Medical’s temporary pause does not necessarily alter its long-term value.

But it will change how the market views artificial heart companies.

In the past, the most important narratives surrounding domestically produced artificial hearts were domestic substitution, technological breakthroughs, and urgent clinical needs. Today, while these factors remain significant, they are no longer sufficient.

The capital markets will next focus more on several specific issues:

Can Multiple Products Continue to Ramp Up Volume?

Can Revenue Growth Lead to a Narrowing of Losses?

Can High R&D and Sales Investments Be Diluted Through Scaling?

Can interventional products unlock higher-frequency clinical scenarios?

Core Medical has proven that domestically produced artificial hearts can be manufactured and sold.

However, the second half of the race for artificial hearts is not about who obtains regulatory approval first, but rather about who can successfully streamline the integration of patients, hospitals, payment systems, product pipelines, and service networks.

This is the question that Core Medical truly needs to answer.