Domestic Brands Capture 63% of China's Laparoscopic Surgical Robot Tender Market in H1 2026, with Jingfeng Medical Leading the Pack

Edge Medical

Developer of Robot-Assisted Minimally Invasive Surgical Systems

MicroPort

High-end Medical Device R&D and Manufacturer

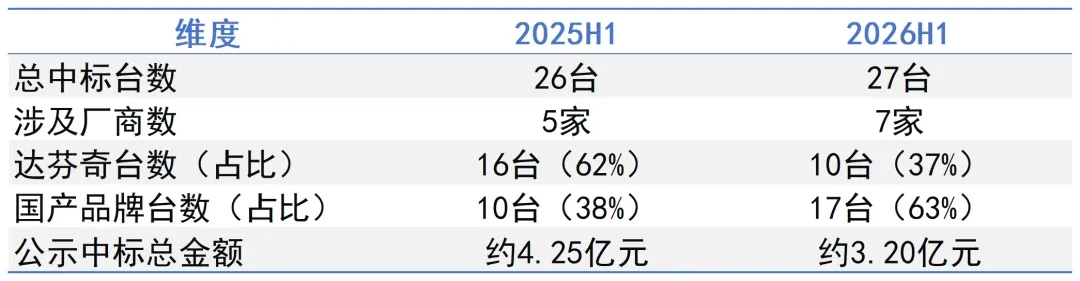

As of June 30, 2026, based on MedRobot’s statistics of publicly announced bid awards in public hospitals in China (excluding Hong Kong, Macao, and Taiwan), the total number of bid awards for laparoscopic surgical robots announced by public hospitals in the first half of 2026 amounted to27 units, involving7 Manufacturers, the total winning bid amount announced is approximatelyRMB 320 million. Compared with the same period in 2025 (26 units from 5 manufacturers), the total volume remained largely stable, consistent with the cyclical patterns of bidding processes; the number of manufacturers expanded, with domestic brands collectively winning bids for 17 units, accounting for approximately 63%, a significant increase from 38% in the same period last year.

Behind the Flat Total Volume, Structural Changes Deserve More Attention:Accelerated Advancement of Domestic Substitution, with Clear Tier Differentiation Within the CampMedRobot will systematically analyze the current data from four perspectives: the overall market landscape, the evolution of domestic manufacturers, price trends, and hospital selection behavior.

Table: Overall Market Comparison: 1H 2025 vs. 1H 2026

The bidding and tendering cycle for laparoscopic surgical robots has historically followed a pattern of relative moderation in the first half of the year and concentrated release in the second half. The total volumes in the two first halves were basically flat, consistent with this cyclical characteristic.

In terms of market structure, the most significant change stems from shifts in the proportion of domestic versus imported systems. In the first half of 2025, da Vinci captured 62% of the market with 16 units, while domestic brands accounted for a combined total of 10 units.In the same period of 2026, da Vinci fell back to 10 units, while domestic brands increased to 17 units, with their share jumping to 63%.This shift is not driven by a concentrated sales push from any single brand, but rather reflects the sustained market penetration of domestic manufacturers across multiple provinces and various types of hospitals, further substantiating the volume-based progress of domestic substitution.

The number of manufacturers expanded from five to seven, with Tuodao Medical, Weijing Medical, and Sizherui all having publicly recorded bid wins in this period.

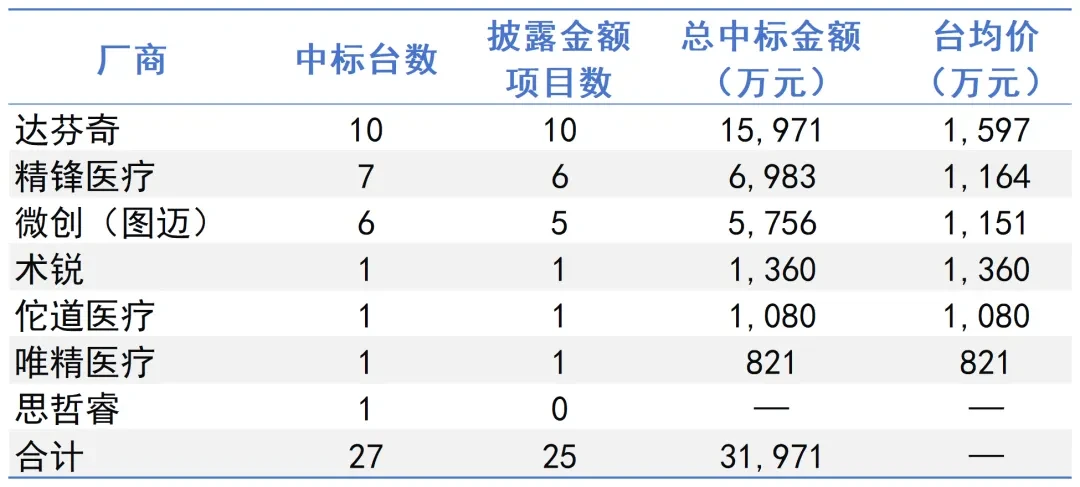

Table: Bid Winning Status of Various Manufacturers in the First Half of 2026

Note: The bid amounts for some projects were not disclosed; the average unit price is calculated based only on disclosed projects; the total amount includes only disclosed projects.

The number of units from domestic brands increased from 10 to 17, a 70% rise, representing the structural indicator with the largest magnitude of change in this period’s data. In terms of manufacturer distribution, this growth was not evenly allocated: Edge Medical and MicroPort accounted for a combined 13 units, approximately 76% of the total domestic volume, indicating a pronounced concentration among top players; the remaining five domestic manufacturers each won bids for one unit.

Edge Medical Ranks First Among Domestic Brands in Bid Wins with 7 Units,The gap in the number of units compared to da Vinci has narrowed from 10 units in the same period last year to 3 units.A review of data from recent cycles reveals that this lead has been sustained:

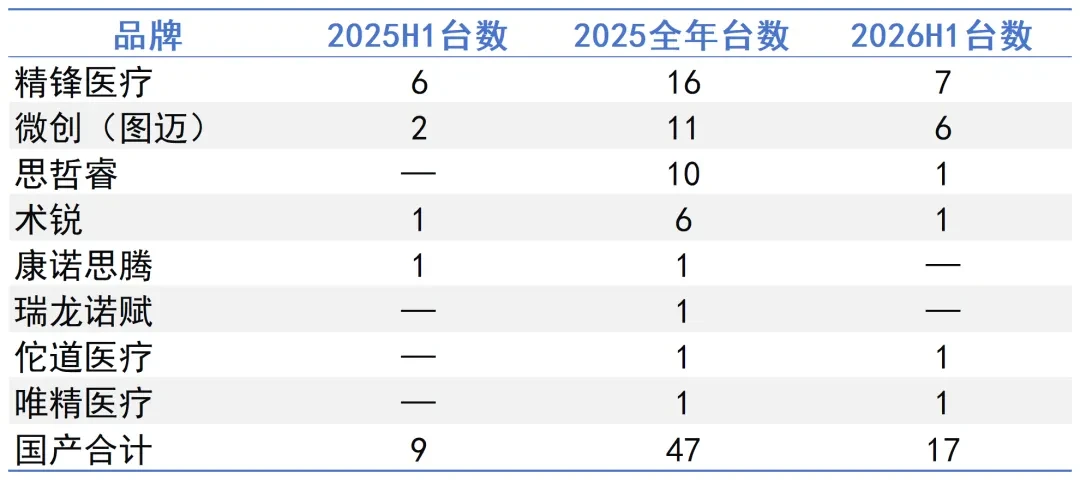

In the first half of 2025, domestic brands won a total of nine bids, with Edge Medical securing six alone, accounting for a dominant 66.7% share within the domestic camp and leading by a wide margin;

In 2025, a total of 47 units were sold by domestic brands. Edge Medical won bids for 16 units throughout the year, capturing a 34% share within the domestic market and maintaining its top position among Chinese brands for the full year.

In the first half of 2026, the total volume of domestically produced units expanded to 17, with Edge Medical securing an additional 7 units. The domestic market share reached 41.2%, maintaining its leading position.

In contrast, the performance of other manufacturers has fluctuated. Against the backdrop of the overall expansion of the domestic sector and the continuous evolution of the competitive landscape, Edge Medical has maintained a leading position in volume and demonstrated stable performance across multiple statistical periods, making it worthy ofContinuousLeading Manufacturers Under Observation

Table: Comparison of the Number of Winning Bids by Domestic Brands Across Different Periods

Note: The full-year 2025 data are sourced from MedRobot’s annual public statistics on winning bids.

In this issue's data,An important characteristic of Edge Medical isSynchronized Commercialization Across Multiple Platforms—Achievements in Porous, Single-Port, and “Three-in-One” Product Lines。

From the perspective of the product structure of the winning bids, a three-dimensional growth curve of "high-end general multi-port + specialized single-port features + affordable economic type" has been formed;

From a product perspective, Edge Medical has currently established a complete portfolio comprising multi-port, single-port, and integrated platforms, offering differentiated system options tailored to the specific characteristics of various medical departments and surgical procedural requirements—a distinction that currently makes it unique among endoscopic surgical robot manufacturers.

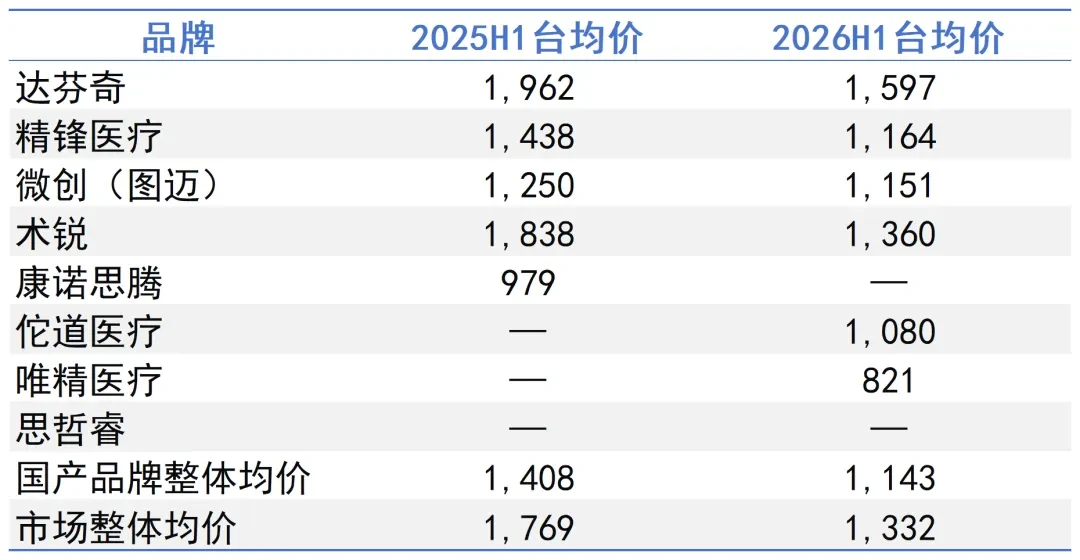

The total winning bid amount announced in this period is approximately RMB 320 million, lower than the approximately RMB 425 million during the same period last year.The overall average market price decreased from approximately RMB 17.69 million per unit to approximately RMB 13.32 million per unit.. The decline in prices is primarily driven by structural factors—the share of domestic brands rose from 38% to 63%, and their overall pricing is lower than that of the da Vinci system; as the number of domestically produced units increased significantly, the market-weighted average price consequently decreased.

The average price of da Vinci systems has decreased from approximately RMB 19.62 million per unit to approximately RMB 15.97 million per unit, representing a decline of about 19%.In light of current domestic procurement policy trends, pricing for both the da Vinci system and Chinese-made brands is converging toward a range more aligned with domestic procurement expectations, which serves as one of the contributing factors to the overall decline in average prices.The average price of domestic brands decreased from approximately RMB 14.08 million per unit to around RMB 11.43 million per unit, with the price gap between da Vinci and domestic brands continuing to narrow.

It should be noted that the average price is significantly influenced by the composition of disclosed items and variations in procurement configurations across hospitals. The aforementioned data reflect overall trends, with a certain degree of dispersion observed among individual cases.

Table: Comparison of Average Price per Unit by Brand (10,000 RMB/Unit), H1 2025 vs. H1 2026

Note: The average unit price is calculated based on the disclosed amounts for each brand; for newly entered brands, the change column is marked with “—” due to the absence of comparable period data.

In the first half of 2026, the procurement of laparoscopic surgical robots remained highly concentrated in tertiary A hospitals, with secondary and lower-tier hospitals largely absent from the market. This phenomenon is not difficult to understand: surgical robots impose stringent requirements on supporting anesthesia services, surgical volume, and physician training systems. Tertiary A hospitals, with their established foundations in minimally invasive surgery, are currently the primary institutions capable of effectively utilizing these devices. Consistently winning bids at this level indicates that the systems have successfully undergone comprehensive evaluation by hospital management and clinical teams with specialized professional backgrounds.

Based on the distribution of hospitals awarded bids in this period, the covered provinces have expanded compared to the same period last year,The implementation records of leading domestic brands are relatively dispersed across regions, with no significant reliance on a single market.。Taking Edge Medical as an example, its seven successful bids are distributed across six provinces and municipalities—Sichuan, Zhejiang, Jilin, Shandong, Hubei, and Beijing—covering five major regions: Southwest, East China, Northeast, Central China, and North China. The hospital coverage spans multiple tiers, including provincial-level general Grade 3A hospitals, specialized benchmark institutions, and prefecture-level Grade 3A hospitals. This multi-tiered penetration demonstrates the company’s stable capability for cross-regional and cross-level implementation, as reflected in the current data.

Conclusion

In the first half of 2026, the laparoscopic surgical robot market maintained a relatively steady bidding pace, with the total volume remaining largely on par with the same period last year. Beneath this stability, structural changes continued to advance:The market share of domestic brands continues to rise, the manufacturer landscape is further expanding, commercial implementation in the single-port surgical sector is steadily advancing, and hospital procurement decisions are evolving toward greater precision.Among them, Edge Medical has maintained its leading position among domestic manufacturers, with multiple product lines advancing simultaneously.。

Over a longer horizon, the bidding data reveals not just procurement volumes for a given period, but also the outcomes of choices made by market participants—manufacturers, hospitals, and clinical teams—in real-world settings. The accumulation of these choices is shaping the evolving landscape of the laparoscopic surgical robot market. Data from the second half of 2026 will serve as a critical window to observe whether this landscape becomes further defined.