Junshi Biosciences Licenses Anti-IL-17A Monoclonal Antibody JS005 to Fosun Pharma for Up to RMB 1.34 Billion

Junshi Biosciences

Innovative Drug Developer

On the evening of July 1, Junshi Biosciences (688180.SH) announced that it had signed a License Agreement with Fosun Wanbang, a wholly-owned subsidiary of Fosun Pharma, on June 30. Under the agreement, Junshi Biosciences has out-licensed the exclusive rights for the development, registration, manufacturing, and commercialization of its self-developed anti-IL-17A monoclonal antibody, ruokiqibai mAb (JS005), in the Greater China region. The transaction consideration consists of a non-refundable upfront payment of RMB 215 million, tiered milestone payments of up to RMB 1.125 billion, and graded sales royalties, bringing the total potential value to a maximum of RMB 1.34 billion.

From a timeline perspective,This transaction occurred during the critical window as the product approached commercialization.In December 2025, the National Medical Products Administration (NMPA) accepted the New Drug Application (NDA) for nankocimab for the treatment of moderate-to-severe plaque psoriasis.

Retrospective pipeline layout,Junshi Biosciences has previously out-licensed multiple assets at various stages.: In October 2023, the exclusive license for the PCSK9 monoclonal antibody ongoricimab (JS002) in mainland China was granted to Bochuang Medicine; earlier, in 2021, the rights to develop and commercialize the PD-1 monoclonal antibody toripalimab injection in the U.S. and Canadian markets were licensed to Coherus BioSciences.

From PD-1 to PCSK9 and then to IL-17A, the overall trajectory exhibits a consistent pattern: advancing R&D to the late clinical stages, leveraging external partners for commercialization, while recouping capital to reinvest in upstream R&D.

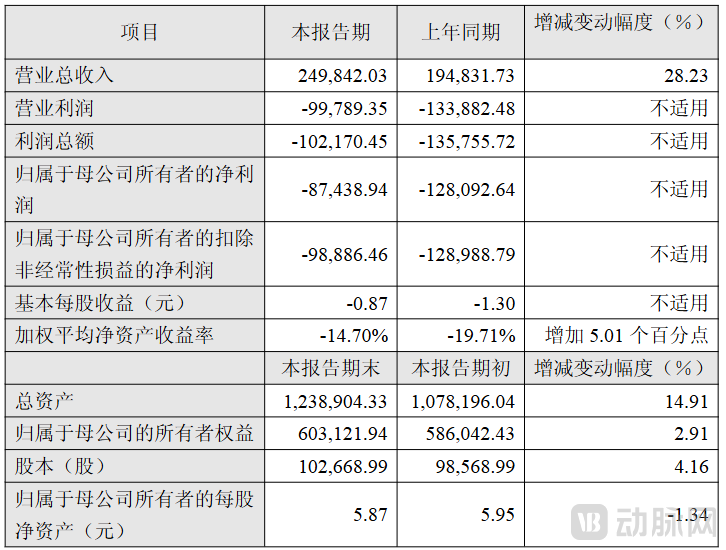

From the profitability perspective, the company’s net profit attributable to shareholders remained at -RMB 875 million, indicating that it has been in a continuous investment phase since its listing in 2020. In 2025, R&D expenditure amounted to RMB 1.342 billion, representing a year-on-year increase of 5.24%. Both R&D spending and sales expenses remain at relatively high levels.

2025 Annual Key Financial Data and Indicators (Unit: RMB 10,000)

Nokacimab: Robust Clinical Data, but the Track Is Crowded with Competitors

Xokibart is a specific anti-IL-17A monoclonal antibody. IL-17A (Interleukin-17A), secreted by Th17 cells, plays a key amplifying role in the inflammatory cascade in various autoimmune diseases such as psoriasis, ankylosing spondylitis, and rheumatoid arthritis.

Traditionally, broad-spectrum immunosuppressants such as methotrexate and cyclosporine have been commonly used in clinical practice to control symptoms. These agents lack targeted selectivity and rely on systemic suppression of the immune system to alleviate inflammation. Long-term use not only leads to cumulative hepatorenal toxicity but also results in decreased patient tolerance over the course of treatment; furthermore, some patients with moderate-to-severe disease fail to achieve an optimal therapeutic response.

The advent of targeted biologics has transformed this treatment paradigm. By selectively blocking key cytokines such as TNF-α and IL-17A, therapeutic strategies have gradually shifted from systemic immunosuppression to precise intervention in specific inflammatory pathways, achieving long-term stable disease control. Runcokibart specifically binds to the IL-17A homodimer and the IL-17A/F heterodimer, thereby preventing their interaction with cell membrane receptor complexes and interrupting the sustained activation of downstream inflammatory signaling. This mechanism of action has been validated for efficacy in two pivotal clinical studies.

In the pivotal registrational Phase III clinical study (JS005-005-III-PsO) conducted in adult patients with moderate-to-severe plaque psoriasis, the PASI 90 response rate in the 150 mg dose group reached 91% at Week 16; during the follow-up phase with continued treatment up to Week 52, the PASI 100 response rate was 65%. In terms of efficacy endpoints, these data place the drug among the leading performers within the IL-17A inhibitor class.

In the Phase II clinical study of ankylosing spondylitis (data disclosed at EULAR 2026), the ASAS40 response rate at Week 16 was 51.4% in the 150 mg group and 46.4% in the 300 mg group, both higher than the 25.6% observed in the placebo group. No deaths or discontinuations due to adverse events were reported in terms of safety.

Based on the currently disclosed results, this product has completed preliminary efficacy validation for its two primary indications: psoriasis and ankylosing spondylitis. However, it is also important to note that the IL-17A therapeutic landscape has entered a phase of intense competition with multiple products.

Currently,China Has Established a Relatively Complete IL-17 Product Pipeline, including imported original products such as secukinumab (with global sales reaching $6.668 billion in 2025) and ixekizumab (with global sales reaching $17.562 billion in 2025), as well as multiple domestically produced innovative drugs or drugs with similar mechanisms targeting the same pathway. Meanwhile, the IL-17A/F dual-target inhibitor bimekizumab has entered the Chinese market, further intensifying competition in this therapeutic area.

Crowding in the therapeutic赛道 also means that relying solely on efficacy advantages is no longer sufficient to drive market conversion. Ultimately, volume growth will depend more on hospital access, academic promotion networks, reimbursement strategies, and long-term patient management capabilities—competencies typically held by comprehensive pharmaceutical companies with mature distribution channels and diversified product portfolios.

Fosun Pharma: Taking Over Late-Stage Pipeline to Complete the Autoimmune Puzzle

From the perspective of financial and operational fundamentals, Fosun Pharma achieved an operating revenue of RMB 41.662 billion in 2025, a year-on-year increase of 1.45%; net profit attributable to shareholders of the listed company amounted to RMB 3.371 billion, up 21.69% year on year; and net cash flow from operating activities reached RMB 5.213 billion, providing relatively ample financial support for external business development (BD) transactions.

At the structural level, the company’s product portfolio continues to shift toward innovative drugs, while its global market expansion is being steadily intensified. In 2025, revenue from innovative drugs in the pharmaceutical segment reached RMB 9.893 billion, a year-on-year increase of 29.59%, accounting for 33.16% of the segment’s total revenue. Full-year R&D investment amounted to RMB 5.913 billion, with resources continuously allocated to the innovative pipeline. In terms of regional markets, overseas revenue during the period totaled RMB 12.977 billion, representing a 14.87% year-on-year growth and contributing 31.15% to total operating revenue, thereby demonstrating the ongoing realization of benefits from its globalized operations. Overall, innovative drugs have become the core driver of the company’s growth.

In terms of product portfolio, the company focuses on oncology, anti-infectives, and metabolism, having established a mature commercialization system. With products such as Hansizhuang (serplulimab), Hanlikang (rituximab), and Hanquyou (trastuzumab), it has built a stable and rapidly expanding oncology portfolio.

In the autoimmune disease sector, Fosun Pharma has long established a multi-tiered pipeline, rather than starting from scratch. In the biologics segment, its subsidiary Henlius boasts Han Da Yuan (adalimumab injection), which has been approved for autoimmune indications including rheumatoid arthritis, ankylosing spondylitis, and psoriasis. In the small-molecule arena, the company secured exclusive development and commercialization rights for AC-201, an oral TYK2/JAK1 inhibitor from Aikenuo, in Greater China in August 2025; this small-molecule drug has completed Phase II clinical trials for psoriasis. In the frontier cell therapy dimension, Fosun Kite is simultaneously advancing its in vivo CAR-T pipeline, continuously expanding technological pathways for autoimmune diseases.

Overall, compared to the high-density portfolio of blockbuster drugs established in the oncology sector, the autoimmune disease field remains dominated by broad-coverage products, and has yet to form a core product structure with sustained volume growth potential in key specialties such as dermatology and rheumatology. The introduction of resokibart serves precisely to fill this strategic gap.

Intensifying Competition in the Autoimmune Disease Sector: Commercialization Capabilities May Become the Core Variable

The domestic autoimmune disease market offers substantial long-term growth potential. According to the "Chinese Guidelines for the Diagnosis and Treatment of Psoriasis" and multicenter studies, the number of psoriasis patients in China exceeds 6 million, with moderate-to-severe cases accounting for approximately one-third. As biologics gradually become the mainstream treatment option, the market continues to expand.

On this basis, the autoimmune disease drug market has transitioned from a "phase of scarce targets" to a "phase of intensive product competition." Taking IL-17A as an example, since the approval of the first-in-class drug in 2015, this pathway has completed the full cycle from mechanism validation to multi-product commercial scale-up, entering a mature competitive landscape.

As competition intensifies, with imported originator drugs and domestically produced products competing on the same stage, and continuous price reductions driven by medical insurance reimbursement policies, differences among various products in terms of efficacy, safety, and dosing intervals are gradually converging. At this stage, relying solely on clinical data advantages is no longer sufficient to directly translate into stable commercial returns, thereby increasing the importance of commercialization capabilities.

Junshi Biosciences has transferred the commercialization rights of JS005 to Jiangsu Wanbang Biopharmaceuticals, essentially handing over an asset nearing market launch to a company with mature distribution and promotional capabilities. This arrangement enables revenue recovery through upfront payments and royalty mechanisms, allowing Junshi to concentrate its resources on early-stage R&D.

For Fosun Pharma, such assets serve to complement its product portfolio in the autoimmune field, further expanding its immunotherapy layout beyond its existing oncology and anti-infection frameworks.

The two parties thus form a division of labor structure with complementary capabilities.

This model has seen a gradual increase in recent years. Keymed Biosciences completed overseas licensing through the NewCo model, while Hengrui Medicine achieved capitalization of its pipeline assets via two pathways: spinning off its domestic innovation platform and establishing an overseas NewCo entity. Both cases point to the same trend: Chinese innovative pharmaceutical companies are shifting from “building the entire value chain in-house” to “a division of labor between R&D and commercialization.”Gradual Stratification of Roles in the Industry Chain。

IL-17A is a microcosm of this trend. As products enter a phase of intense competition, the realization of value for innovative drugs increasingly depends on whether R&D outcomes can be effectively absorbed by commercialization systems.