Smartee Denti-Technology Surpasses Invisalign, Files for IPO

Zhejiang Smartee

Oral Medical Device R&D and Manufacturer

Following Angelalign, another Chinese clear aligner company is poised to go public! On June 29, Smartee Denti-Technology submitted its IPO prospectus to the ChiNext Board.

As one of the leading domestic enterprises in invisible orthodontics, Smartee Denti-Technology was established in 2004 and was among the early players to enter this sector. Over more than two decades of development, Smartee Denti-Technology has built a comprehensive product portfolio, including core categories such as the Classic Edition, Joy Edition, GS Series, and the Children and Adolescents Series, meeting diverse needs ranging from dental alignment to complex jaw position reconstruction. In 2023, 2024, and 2025, Smartee Denti-Technology achieved operating revenues of RMB 648 million, RMB 786 million, and RMB 938 million, respectively.

Notably, in terms of case volume, Smartee Denti-Technology surpassed Align Technology's Invisalign in 2025, securing the second position in the Chinese domestic market. Just five years ago, the domestic clear aligner market was dominated by the duopoly of Angelalign and Invisalign, with Smartee Denti-Technology lagging significantly behind both competitors.

After nearly two years of intense price competition and bubble clearance, some small and medium-sized brands have exited the market. Based on the core market data disclosed by Smartee Denti-Technology, has a stable competitive landscape dominated by three major players taken shape in China's clear aligner orthodontics market?

In recent years, the domestic invisible orthodontics market in China has experienced rapid growth, with a surge of new brands entering the market and numerous new products receiving regulatory approval. Nevertheless, the market has long maintained a highly concentrated structure dominated by top players. Measured by the number of cases, the top three companies collectively held a 91% market share in 2020 (all market shares mentioned hereafter are calculated based on the number of cases); by 2025, the combined market share of the top three companies remained above 90%. The biggest change over the past five years lies in the restructuring of the top-tier landscape.

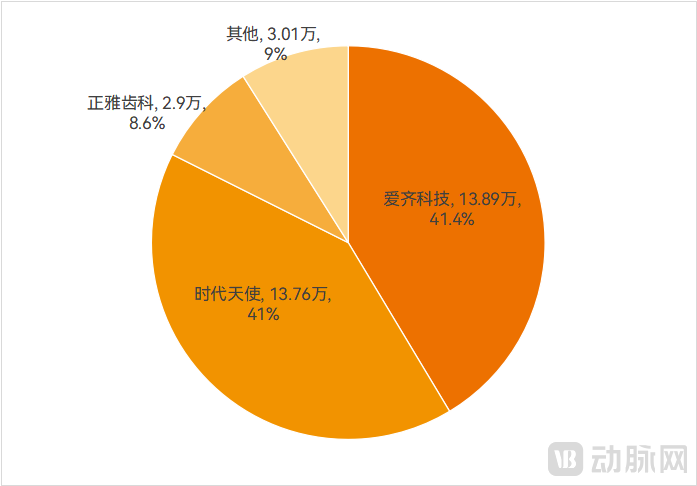

According to data from China Insights Consultancy (CIC), in 2020, Align Technology, Angelalign, and Smartee Denti-Technology held market shares of 41.4%, 41%, and 8.6%, respectively. This indicates that although Smartee Denti-Technology ranked among the top three that year, its market share lagged significantly behind the other two companies, with the market essentially dominated by two major giants.

2020 Market Share of Invisible Orthodontics in China (by Number of Cases); Source: Frost & Sullivan Report, Angelalign Prospectus, Public Corporate Information

2020 Market Share of Invisible Orthodontics in China (by Number of Cases); Source: Frost & Sullivan Report, Angelalign Prospectus, Public Corporate Information

Over the following five years, Smartee Denti-Technology achieved leapfrog growth. By the end of 2025, Smartee Denti-Technology had partnered with more than 80,000 medical institutions, including large dental chains and private dental clinics; it had served over one million patients, with an increasing proportion of complex cases; and its products and services had entered more than 50 countries and regions worldwide.

With this, the landscape of the top three players in the industry has been reshaped. According to a research report by Biaodian Information, Smartee Denti-Technology ranked second in the Chinese market for the number of clear orthodontic cases in 2025.

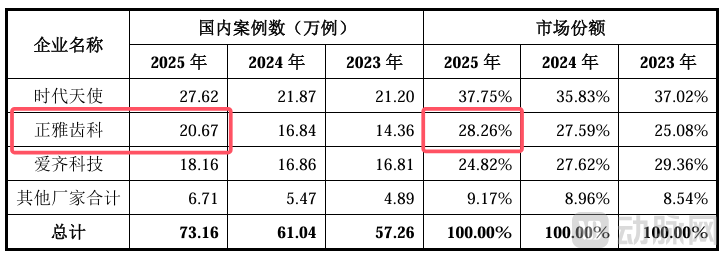

2025 Market Share of Clear Aligner Orthodontics in China (by Number of Cases), Source: Annual Reports of Listed Companies, Menet, Smartee Denti-Technology Prospectus

2025 Market Share of Clear Aligner Orthodontics in China (by Number of Cases), Source: Annual Reports of Listed Companies, Menet, Smartee Denti-Technology Prospectus

Specifically, in 2025, Smartee Denti-Technology's case volume exceeded 200,000, surpassing Align Technology's 181,600; the market shares of the top three players were 37.75%, 28.86%, and 24.82%, respectively. Compared to five years ago, the gap in market share among the three companies has narrowed significantly. In other words, China's clear aligner market has officially transitioned from a duopoly to a triopoly.

The past few years have been a period of rapid market development as well as a phase of intense competition.

Looking upward, Align Technology's Invisalign brand has become virtually synonymous with clear aligners, while Angelalign stands as the representative of domestically produced clear aligners in China; both wield significant influence among clinicians and consumers. Looking downward, a surge of emerging brands is entering the market, particularly clustering in the treatment of simple cases and capturing price-sensitive customers through low-price strategies. For Smartee Denti-Technology, it is no exaggeration to describe the situation of the past few years as being "attacked from both front and rear."

Based on Smartee Denti-Technology's current business operations, the main reason for its rapid increase in market share within five years is that it has adopted a differentiated strategy compared to both leading and trailing enterprises.

Upward, compared with the two industry giants, Smartee Denti-Technology's core differentiation strategy is undoubtedly price, meeting market demand with cost-effective products.

In terms of end-user pricing, the price tiers among brands are clearly defined: taking mild to moderate orthodontic cases as an example, Invisalign falls into the first tier, priced at approximately RMB 30,000–50,000; Angelalign occupies the second tier, priced at around RMB 20,000–30,000; while Smartee Denti-Technology is priced at approximately RMB 20,000 or less. Price is a key factor influencing consumers' choice of orthodontic treatment and brand. For those seeking clear aligner therapy but hesitant due to budget constraints, Smartee's pricing positioning undoubtedly represents an attractive option.

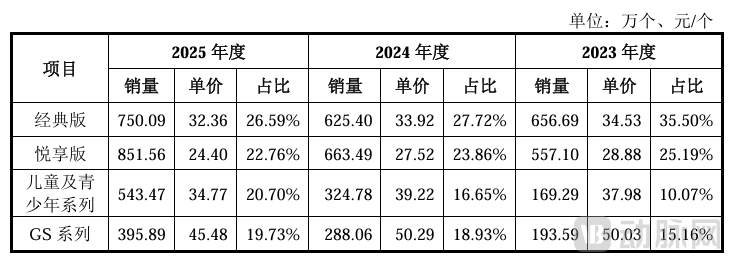

Sales Volume and Selling Prices of Smartee's Main Products, Image Source: Prospectus

Sales Volume and Selling Prices of Smartee's Main Products, Image Source: Prospectus

Data such as the unit price and gross profit margin of aligners more clearly demonstrate Smartee Denti-Technology's strategy of high sales volume with low profit margins. According to the prospectus, the unit price of Smartee Classic aligners from 2023 to 2025 ranged from RMB 32.36 to RMB 34.53 per unit, whereas the equivalent unit price for Angelalign Standard aligners was approximately RMB 75 per unit (based on data from Angelalign's prospectus: the average selling price of the Standard version in 2020 was RMB 7,600, with an average requirement of 51 pairs of aligners).

In terms of gross profit margin, Angelalign's margin exceeded 70% at the time of its IPO, leading the public to perceive the clear aligner industry as highly lucrative. Smartee Denti-Technology disclosed that its gross profit margin over the past three years ranged from 52.67% to 55.34%, which is far below the high-profit levels perceived by the public and significantly lower than the gross profit margins of over 60% reported by Angelalign and Align Technology.

In the process of expanding its overseas business, Smartee Denti-Technology has adopted a differentiated approach in regional selection and expansion strategies compared to other leading enterprises.

In 2025, Angelalign has established local teams and support systems in four major regional markets: Europe, Africa, and the Middle East; North America; Asia-Pacific; and South America. It has also set up medical design centers in Brazil and Southeast Asia, expanded its production facility in Brazil to manufacture Angelalign-branded products, and is currently constructing a production center in the United States.

In the same year, Smartee Denti-Technology's products and services expanded to cover more than 50 countries and regions, including Spain, Japan, Italy, the United Kingdom, and France. With the commissioning of its Madrid production base in Spain, the company achieved localized manufacturing and service capabilities in the European market.

On the surface, both companies have established extensive overseas markets with some regional overlap. However, since local production of clear aligners better ensures delivery speed, the location of manufacturing bases more accurately reflects their key strategic regions. Smartee Denti-Technology's overseas production base is located in Spain, primarily serving the European market, while Angelalign has a production base on the other side of the globe in Brazil, primarily serving the South American market. This highlights the differentiated approach Smartee Denti-Technology has taken in selecting its overseas markets.

The overseas market is not limited to Angelalign; it also features global international brands under companies such as Align Technology and ENVISTA. Therefore, Smartee Denti-Technology has adopted a hybrid model for its international business, combining independent brand operations with OEM and ODM services. By providing contract manufacturing for overseas clients, the company maximizes the efficiency of its market penetration in overseas regions, rather than engaging in direct head-to-head competition with major international brands.

Downward, it is also necessary to break through the low-price competition of small and medium-sized brands. Although Smartee aligners have adopted a lower pricing strategy compared to the other two leading brands, they do not engage in price wars with other brands. While many small and medium-sized brands focus on simple cases, Smartee Denti-Technology has made significant investments in the treatment of complex skeletal malocclusions and orthodontic care for children and adolescents, thereby breaking away from homogeneous competition.

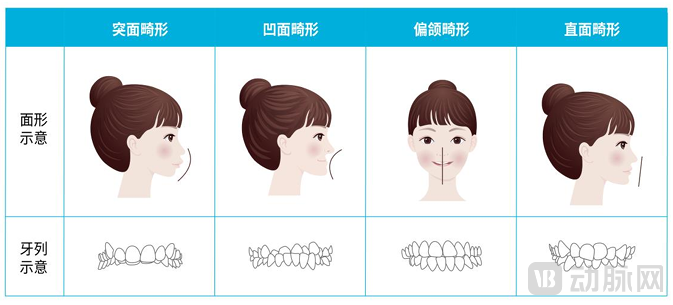

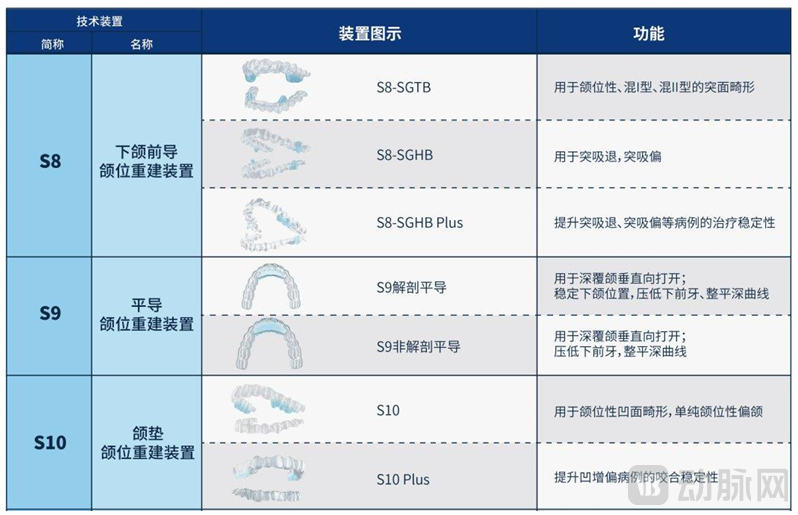

To address the limitations of the Angle classification system in diagnosing malocclusion among the Chinese population, Smartee Denti-Technology has collaborated extensively with Professor Shen Gang's team to propose an original diagnostic framework: the Shen Gang Classification System for Malocclusion and the Theory of Jaw Position Reconstruction. Corresponding solutions for malocclusion have been developed, namely the GS Series of Smartee aligners. This series is designed to specifically address four types of skeletal deformities prevalent in China: protrusive, concave, asymmetric, and straight facial profiles.

Schematic Diagrams of Four Types of Malocclusion and the Smartee GS Series Aligners, Image Source: Prospectus

Schematic Diagrams of Four Types of Malocclusion and the Smartee GS Series Aligners, Image Source: Prospectus

Pediatric and adolescent orthodontics represents a blue-ocean market with higher technical barriers. In response, Smartee Denti-Technology has established a comprehensive product portfolio covering clear aligners, removable/functional appliances, myofunctional appliances, and orofacial myofunctional training systems. The lineup primarily includes the Orofacial Myofunctional Training Edition (T0), Occlusal Guidance Edition (T1), Early Treatment Edition (T2), and Myofunctional Orthodontic Edition (T3), catering to personalized and precise early treatment needs.

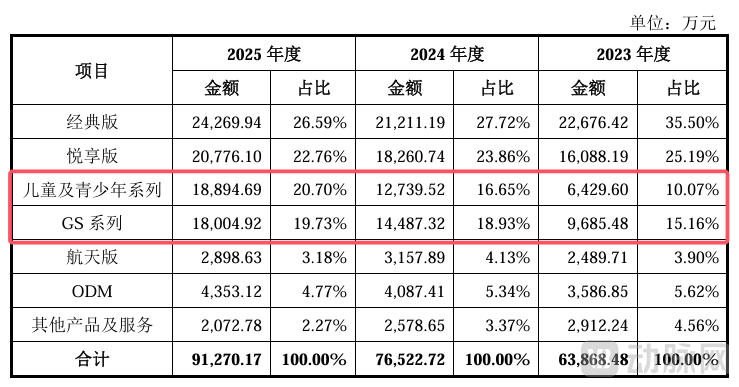

Smartee Denti's Revenue Structure: Rapid Growth in the GS Series and Pediatric & Adolescent Series. Image Source: Prospectus

Smartee Denti's Revenue Structure: Rapid Growth in the GS Series and Pediatric & Adolescent Series. Image Source: Prospectus

Over the past three years, the GS Series and the Children & Adolescents Series have experienced rapid growth, with revenues increasing from tens of millions of yuan to nearly 200 million yuan, becoming key growth drivers for Smartee Denti-Technology.

While leveraging technology and products to create a competitive edge, Smartee is simultaneously building a differentiated brand image to shed the "low-cost traffic" label often associated with small and medium-sized brands. On one hand, the company collaborates with airlines to place advertisements, leveraging the aviation scenario to precisely reach middle- and high-income groups and establish a professional, premium brand image. On the other hand, it has secured official Disney IP licensing to launch co-branded orthodontic products exclusively for children, becoming one of the earliest brands in the early orthodontic correction sector to partner with a major international IP, thereby gaining an early advantage in brand recognition.

As can be seen, when faced with the multi-dimensional advantages of the two industry giants, Smartee Denti-Technology adopted a strategy of differentiated competition by leveraging price tiering and differentiation in overseas markets; in response to the intense price wars among smaller brands, it penetrated niche segments with higher technical barriers, thereby establishing moats in technology, products, and brand.

Currently, the three leading domestic companies in invisible orthodontics have each established their own competitive advantages.

Angelalign has deeply cultivated the Chinese market, enjoying high brand recognition. Its localized medical solutions offer rapid response capabilities, while its dual-layer film technology and diversified product portfolio effectively cover various consumer segments. Smartee Denti-Technology has established competitive barriers through clinical expertise and digital manufacturing, developing distinctive advantages in early childhood orthodontic treatment and complex skeletal cases, with full control over its entire industry chain. Align Technology leverages its first-mover advantage and brand influence in the global orthodontics industry, boasting mature system algorithms and material technologies, as well as a comprehensive global clinical case database and physician training system.

From 2020 to 2025, Smartee Denti-Technology reshaped the market landscape. Will there be another "Smartee" in the market?

Given the industry's characteristics and historical trends, it is unlikely that another comprehensive enterprise with a complete product portfolio, serving both domestic and international markets, and experiencing rapid business expansion will emerge in the short term. As an investor in the field remarked, "The market share and landscape of the major brands have remained relatively stable, with the strong getting stronger."

Invisible orthodontics is a long-cycle sector, with treatment durations ranging from as short as two years to as long as three to five years per case. Companies must build long-term capabilities in technology, branding, distribution channels, and capital, as these elements are closely interlinked and indispensable, making it difficult to achieve rapid overtaking in the short term. In fact, Smartee Denti-Technology did not emerge out of nowhere; it attained its current market position after already breaking into the top three.

Currently, the domestic grassroots market and overseas markets are widely recognized within the industry as new growth engines. However, both sectors present significant barriers to entry. The grassroots market is fragmented, with varying levels of clinical proficiency among physicians, necessitating the establishment of large-scale training and support service systems. This makes it difficult for small and medium-sized brands to independently build comprehensive networks. Furthermore, expanding into overseas markets relies heavily on mature domestic technologies and a robust portfolio of case studies. Companies lacking a strong local foundation will struggle to gain a foothold when going global.

Over the past two years, the clear aligner orthodontics market has undergone a round of consolidation. Small and medium-sized enterprises with weak clinical support systems and broken capital chains have exited the market, including some once-popular star companies. This reflects the development dilemmas faced by small and medium-sized brands.

Of course, small and medium-sized brands are not without room for survival. Under the premise of mastering break-even analysis and stabilizing cash flow, they may integrate or develop synergies with leading enterprises in terms of production capacity, distribution channels, and service networks. The investment by Angelalign in Suya Star Aligner is a typical case in point.

Nevertheless, compared with traditional orthodontics, which has been developed for many years, clear aligner therapy remains an early-stage industry with significant potential for innovation. There is ample room for advancement in areas such as iterative improvements in film materials, the application of digital technologies, and the expansion of indications. Meanwhile, bottlenecks in trust between doctors and patients persist: poor patient compliance with wearing schedules directly leads to uncontrollable treatment durations and final outcomes, thereby undermining mutual trust in clear aligner therapy and hindering further increases in market penetration.

In the future, companies that achieve significant breakthroughs in the aforementioned key technical areas or address root pain points will still have the opportunity to disrupt the existing market landscape.