A 12-RMB Antitoxin, 19 Years of Dominance: Jiangxi Biology Debuts on HKEX

JIANGXI BIOLOGY

Researcher, Producer, and Distributor of Antitoxins and Immune Serum Biological Products

Tetanus antitoxin (TAT) injections priced at 12 RMB per dose achieved annual sales of nearly 30 million units, generating RMB 235 million in revenue and nearly RMB 100 million in net profit. Its manufacturer, Jiangxi Biology, rang the bell on the Hong Kong Stock Exchange today, with an issue price of HK$11.20.

In 2026, when innovative drugs often burn through billions in R&D costs and biotech companies compete to build pipeline depth and pursue global licensing deals, Jiangxi Biology has made its public market debut with a time-honored approach—relying on its human tetanus antitoxin (TAT), approved in 1997, to deliver consistent profitability for years.

Jiangxi Biology IPO on HKEX, image source: RyanBen Capital

Despite being approved nearly 30 years ago, it has captured 65.8% of the domestic market and 45.8% of the global market for human TAT, maintaining a market share exceeding 50% for 19 consecutive years. In 2025, it sold 29.9 million doses, with 16.4 million exported and 13.5 million sold domestically. Overseas sales surpassed domestic sales, accounting for nearly 100% of China's total exports of human TAT.

A 12-RMB shot, an old factory in Ji'an, Jiangxi, and a drug approval nearly 30 years old have captured almost all of China's export share in this category. With robust cash flow and no shortage of orders, why would such a company choose to go public on the Hong Kong Stock Exchange at this juncture?

To answer the aforementioned question, one can start with reported revenue figures, which are more compelling than technological narratives.

From 2022 to 2025, Jiangxi Biology's revenue surged from RMB 142 million to RMB 235 million, while its net profit attributable to shareholders increased from RMB 26.46 million to RMB 94.79 million—nearly quadrupling over the period. In 2025, the company's overall gross margin reached an impressive 76.8%.

Supporting this revenue is the TAT product, priced at RMB 12. Over the three-year period, the single-product revenue from TAT amounted to RMB 184 million, RMB 206 million, and RMB 227 million respectively, with its share of total revenue rising from 93% to 96.4%. Its exports cover more than 30 countries and regions across Asia and Africa, achieving a market share as high as 90% in the Philippines and Egypt.

In terms of distribution channels, as of the end of 2025,Jiangxi Biology had 421 distributors, covering more than 27,000 medical institutions across China, including over 1,700 tertiary hospitals. This is a network woven over nearly 30 years, not something that can be replicated in the short term.

What is even more unusual is that, at a time when innovative pharmaceutical companies turn pale at the mention of centralized procurement, Jiangxi Biology's TAT not only avoided a drastic price cut but actually achieved a price increase through the centralized procurement process.

In August 2023, it won the bid in the Beijing-Tianjin-Hebei Alliance's centralized procurement, securing a 100% market share as the sole supplier. In December of the same year, it captured a 72% share in the 27-province alliance led by Guangdong. The average selling price under centralized procurement rose from RMB 8.1 per unit in 2023 to RMB 12.3 in 2024, and further increased to RMB 12.5 in 2025.

Centralized procurement has not only failed to lower prices but has instead consolidated the pricing power of market leaders.

The underlying logic is straightforward. TAT is classified as an essential medicine for emergency and critical care, included in the Class A national medical insurance reimbursement list and the National Essential Medicines List. Any supply disruption could pose a life-threatening risk to patients. Consequently, tendering authorities prioritize suppliers' consistent delivery capabilities over mere low-price competition.

Jiangxi Biology happens to be the most stable supplier. Leveraging process upgrades, it has reduced the adverse reaction rate of TAT to 0.03%, nearly doubling the standard set by the Pharmacopoeia. This level of quality control has enabled it not only to retain its market share in centralized procurement but also to capture a larger portion of the market.

It would be biased to attribute the success of Jiangxi Biology solely to the policy dividends following the restructuring of a long-established state-owned enterprise. After all, the Wuhan, Lanzhou, and Changchun Institutes of Biological Products under Sinopharm Group have historically held approvals for TAT. In the face of competitors with equal or even stronger state-owned backgrounds, Jiangxi Biology has not been overwhelmed but has instead emerged as the dominant market leader.

This indicates that it relies on far more than just policy support or cost control. There must be a deeper moat keeping competitors at bay.

The secret to keeping competitors at bay lies hidden in the Gobi Desert of Zhangye, Gansu.

Jiangxi Biology listed on the Hong Kong Stock Exchange, not through the Chapter 18A pathway for pre-revenue biotech companies, but via the traditional main board route requiring profitability. This is because it does not need to burn cash to hype up its story; at its core, it is an anti-serum platform company with significant barriers built on heavy assets.

Its core asset is China's premier GMP-compliant facility for horse breeding and immune plasma collection.

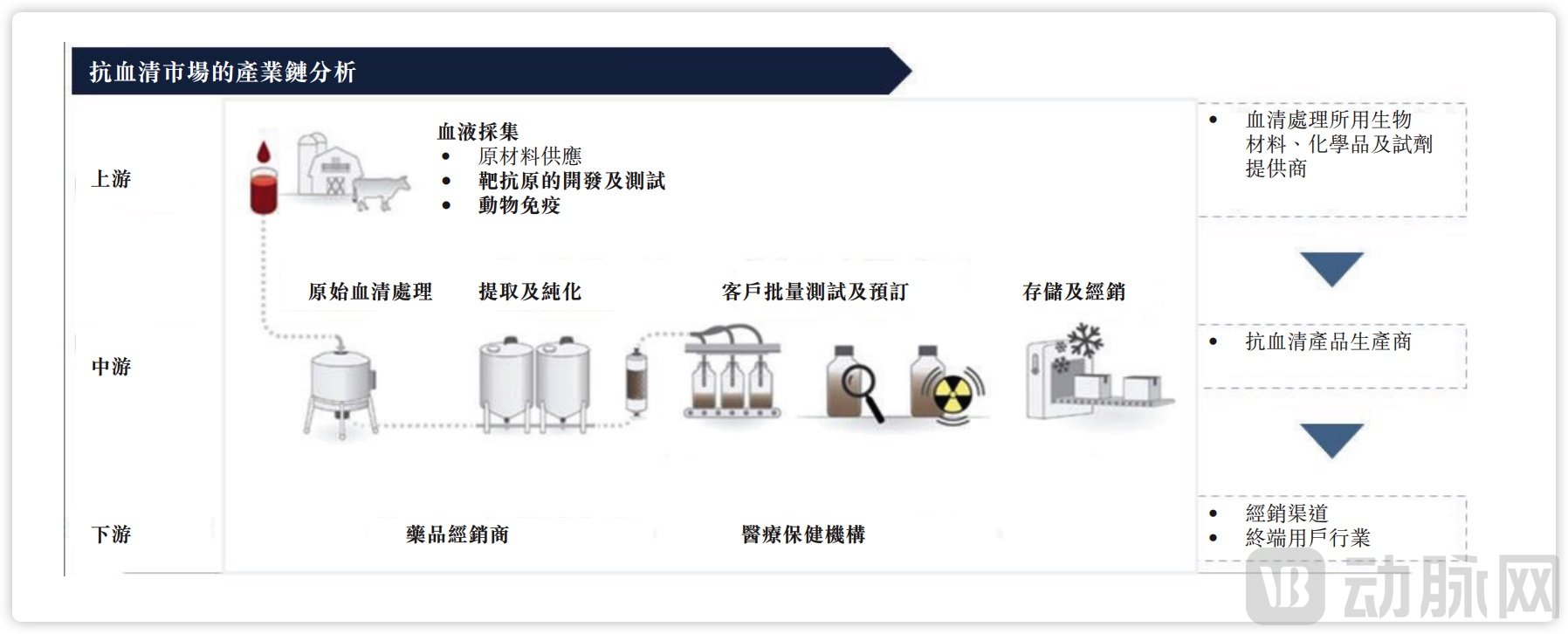

At first glance, this may sound somewhat like animal husbandry, but in reality, it is an extremely complex bioengineering process. The production logic of antiserum involves using horses as living bioreactors: horses are first immunized with specific antigens, such as tetanus toxoid; once high concentrations of antibodies are generated in the horse's body, plasma is collected and then processed through purification techniques to produce pharmaceutical products.

This process involves several significant barriers. For instance, regarding the number of horses, a TAT production line requires thousands of healthy, quarantined, and immunized horses, which necessitates considerable time to accumulate. Additionally, it demands closed-loop capabilities across the entire industry chain, spanning animal breeding, antigen development, immunization of host animals, collection of immune plasma, to antibody purification and formulation manufacturing. Globally, only a handful of companies have successfully integrated this entire industrial chain.

Antiserum Industry Chain, Source: Prospectus

Even for latecomers, it is impossible to accumulate decades' worth of equine herd immunity data and proprietary process know-how in the short term. Coupled with the entire journey from site selection and facility construction, through horse domestication, to obtaining GMP certification and product approvals, this undoubtedly represents a capital-intensive, long-term, asset-heavy investment.

Jiangxi Biology traces its origins to the Jiangxi Branch of the Shanghai Institute of Biological Products, established under the Ministry of Health in 1969. After decades of development, it constructed a facility in Zhangye capable of housing 4,000 horses. This explains why affiliated entities within the Sinopharm group, despite holding regulatory approvals, have gradually fallen behind in large-scale supply; maintaining thousands of horses in the Gobi Desert demands a level of patience and determination that is difficult to muster.

Therefore, this is not a simple price war, but a long-term business centered on who can best raise and maintain horses.

Jiangxi Biology has gradually widened the gap with its competitors not through marketing or purely pharmaceutical manufacturing processes, but by adopting a hybrid model integrating agriculture, industry, and biotechnology.

This is also the biggest difference between Jiangxi Biology and typical 18A Biotech companies. It does not follow the model of scientist-founded startups backed by multiple rounds of venture capital, betting on a blockbuster pipeline for future success; rather, it is an asset-heavy, long-value-chain, hard-to-replicate platform-based biological products enterprise.

If Jiangxi Biology remains fixated on selling TAT, its growth ceiling will be plainly visible; however, the prospectus reveals that the company has a clear-eyed understanding of generational competition within the industry.

The market for passive immunization against tetanus is undergoing technological iteration.

First-generation TAT is inexpensive but requires skin testing and has a high allergy rate; second-generation HTIG rarely causes allergic reactions, but relies on human plasma, has limited production capacity, and is expensive; third-generation equine tetanus immune globulin F(ab')₂ fragments have higher purity and are currently exclusively supplied in China by Serum Bio-technology; fourth-generation recombinant monoclonal antibodies include

Siltartoxatug, approved in February 2025 from Zhuhai Trinomab, which offers advantages such as no need for skin testing, rapid onset of action, and long-lasting protection. Although priced at 798 RMB per dose, it was included in the national medical insurance catalog by the end of 2025.

In the long term, monoclonal antibodies exert substitution pressure on both TAT and HTIG. The market size for TAT is projected to enter negative growth after 2028. This is a realistic challenge that Jiangxi Biology must confront. On the other hand, while technological iteration is occurring in high-end markets, the fundamental global demand in less developed regions such as Southeast Asia and Africa still relies on TAT. This constitutes the foundation of Jiangxi Biology's confidence in expanding into 30 countries across Asia and Africa.

Corporate Product Portfolio, Source: Prospectus

Meanwhile, its response strategy is not to rigidly adhere to TAT, but to develop antiserum into a platform.

First Move: Targeting Antivenom. In China, there are approximately 250,000 to 280,000 cases of venomous snakebites annually, yet the antivenom market has long been exclusively monopolized by Serum Bio-Technology, making it a widely recognized high-margin sector. Jiangxi Biology's anti-Gloydius brevicaudus (short-tailed mamushi) antivenom initiated Phase II clinical trials in June 2026 and is expected to submit its marketing authorization application by the end of 2027; its anti-Deinagkistrodon acutus (five-pacer) antivenom is also currently in Phase I clinical trials. If successful, Jiangxi Biology will become the first substantial challenger to Serum Bio-Technology in the domestic market.

The second strategy targets veterinary products. The company plans to launch Pregnant Mare Serum Gonadotropin (PMSG) in July 2026 to enhance livestock reproductive performance. The global PMSG market is projected to reach $377 million by 2033. In addition, new veterinary drugs such as veterinary tetanus antitoxin and chicken infectious bursal disease antibody injection are being approved sequentially. These products share the same underlying technology as human-use antisera, resulting in a high degree of R&D and production platform reuse.

The prospectus disclosed that the net proceeds from this IPO amounted to approximately HK$338.6 million, with 33.7% allocated to the research and development of candidate products, 31.4% to the construction of new facilities and production lines, 15.7% to technology upgrades, and 10.3% to strengthening sales efforts. The specific initiatives funded by these proceeds are clearly defined: a portion is directed toward the clinical development and regulatory filing for antivenom products; another portion is dedicated to expanding production capacity for PMSG and veterinary TAT; and the remaining funds are used to expand the sales team and facilitate the distribution of new products through sales channels.

This is the true purpose behind Jiangxi Biology's IPO. The company is not short on cash flow; rather, it needs a capital vehicle to replicate the monopoly power of a single injection into the expansion capability of an antiserum platform.

As the entire pharmaceutical industry focuses on first-in-class (FIC) drugs, globalization, and pipeline depth, Jiangxi Biology's IPO has delivered its own answer. In the biopharmaceutical sector, exceptional single-product capability combined with full industrial chain integration can still support a publicly listed company. In an era of fierce competition in innovative drugs, this traditional and less glamorous listing story may offer another inspiration to the industry: not all successful businesses need to take the form of a Biotech.