Big Pharma Spends $134 Billion in First Half of 2026 to Accelerate Pipeline Amid Urgency for Time and Certainty

GSK

Pharmaceutical R&D Manufacturer

Nuvalent

Targeted Therapy Drug Developer

This is AbbVie’s largest acquisition in over five years. What it has its sights on isApogeeFocused on atopic dermatitis in handLong-actingIL-13Pipeline, a potential future challengerDupixentcandidate drugs.

Two weeks ago,GSKJust used106Acquired for $100 millionNuvalent, adding two targeted lung cancer drugs to its portfolio. Eli Lilly was also active, acquiring a non-opioid pain medication company4E Therapeutics, this is already Eli Lilly2026the announced in the year11Pen acquisition.

These transactions are not impulsive moves by a few major pharmaceutical companies.

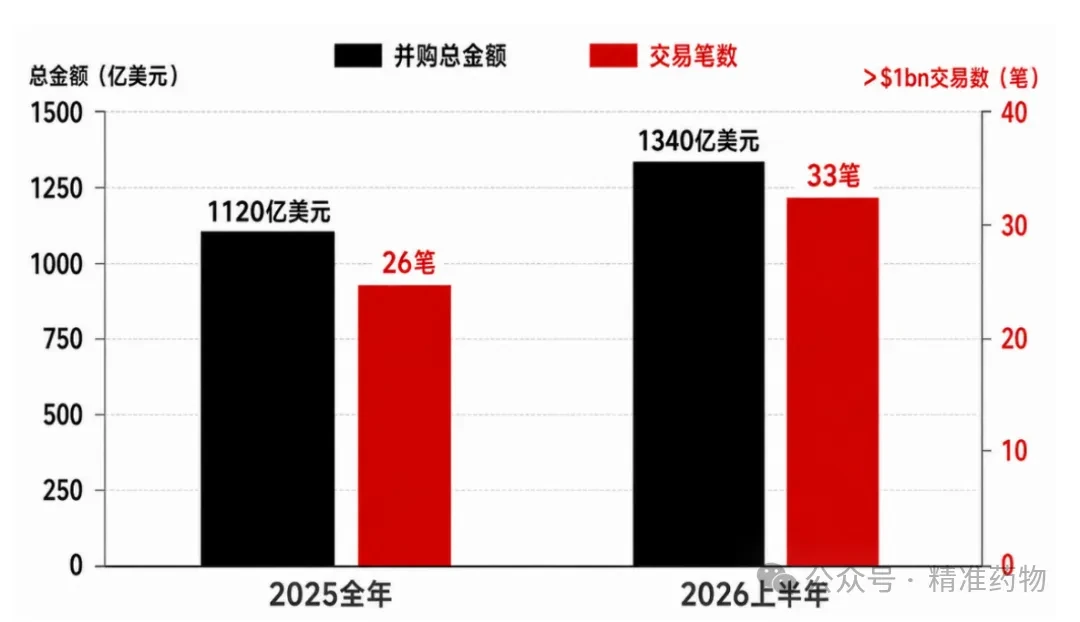

According toSTATStatistics,2026In the first six months of the year, globally there have already occurred33Valuation exceeds10of USD 100 millionBiotechAcquisition, total amount approximately1340hundred million U.S. dollars.2025For the full year, this figure was26Pen,1120hundred million USD.

In other words, with only half of the year elapsed, pharmaceutical companies have already exhausted their full-year M&A budgets from last year, exceeding them in the process.220hundred million U.S. dollars.

On the surface,BiotechThe good old days seem to be back.

But1340Behind the hundreds of millions of dollars, the real question to answer is not why pharmaceutical companies have suddenly become wealthy, but rather another question: Why are they suddenly unwilling to wait?

01

Big Pharma Begins Spending to Buy Time

The growth of pharmaceutical companies is determined by two clocks.

One is the commercial clock. The launch of blockbuster drugs, sales ramp-up, and patent expirations are largely predictable. Once a core product loses market exclusivity, generics and biosimilars rapidly enter the market, potentially causing a swift decline in sales.

The other is the R&D clock. It is far less punctual.

It often takes more than ten years to go from discovering a target to obtaining a new drug. Early experimental success does not guarantee efficacy in humans; promising Phase II data does not ensure successful completion of Phase III trials; and even if clinical trials succeed, challenges may still arise during regulatory approval, manufacturing, or commercialization.

The patent cliff arrives on schedule, but new drugs never graduate on time.

This is exactlyBig PharmaThe most anxious part.

They may hold cash reserves, possess clinical teams, have global regulatory registration capabilities, and maintain mature sales networks; however, these resources cannot instantly mature a project that has just entered the clinical stage. If the internal pipeline fails to fill the revenue gap in a timely manner, the only viable strategy to significantly compress timelines is to acquire a company that has already completed the early stages of development on their behalf.Biotech。

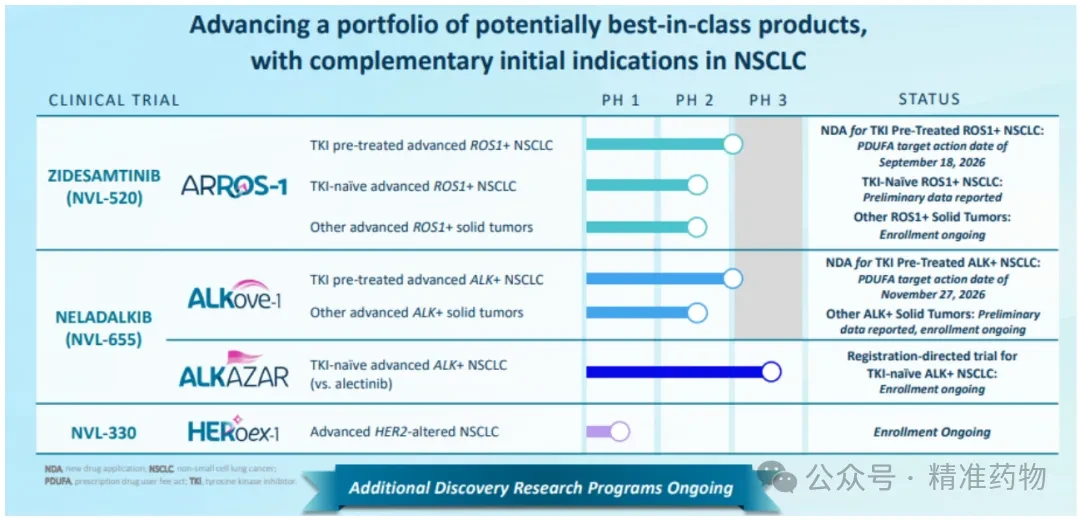

GSKAcquisitionNuvalentThis is a typical case.

Nuvalentwhat it brings is not a technological concept confined to the laboratory, but one that has already enteredFDAMarketing Authorization Reviewtwo productsTargeted Therapy Drugs for Lung Cancer(New GenerationALKInhibitorNeladalkib、ROS1InhibitorZidesamtinib)。GSKThe transaction announcement explicitly stated that this acquisition is expected to create new near-term sales growth opportunities, and from2027began to improve profit contribution.

Nuvalentof3Oncology Pipeline

106The hundreds of millions of dollars spent were not just for two drugs, but alsoNuvalentTime of completed clinical development.

AbbVie AcquisitionApogeeThe same logic applies. AbbVie is not short of immunology drugs, but it needs to continuously replenish its next-generation products to maintain its long-term advantage in the immunology market. Rather than cultivating a new project from scratch, it is more advantageous to directly acquire a pipeline that has already entered clinical validation.

Therefore, the core commodity in this wave of mergers and acquisitions is neither companies nor entirely technology. What large pharmaceutical companies are truly purchasing is time.

02

Buyers Are No Longer Willing to Pay for Stories

Previous RoundBiotechDuring boom periods, merely possessing a hot technology platform gave companies the opportunity to achieve high valuations.

Gene Therapy, Cell Therapy,mRNA、AIPharmaceuticals and protein degradation: Many companies have secured substantial financing based on the perceived potential of their platforms, despite lacking clinical data.

But2026Buyers are significantly more realistic.

They are no longer focused solely on what this technology might achieve in the future, but rather on how close this drug is to market launch.

Therefore, the most sought-after assets typically share several common characteristics: they have already obtained human data, advanced to mid-to-late clinical stages, target indications with sufficiently large markets, can be integrated into the buyer’s existing clinical and commercial infrastructure, and offer the potential to generate revenue within a few years.

This is also why this year’s large-scale transactions have been concentrated in mature therapeutic areas such as oncology, immunology, metabolism, and neuroscience.

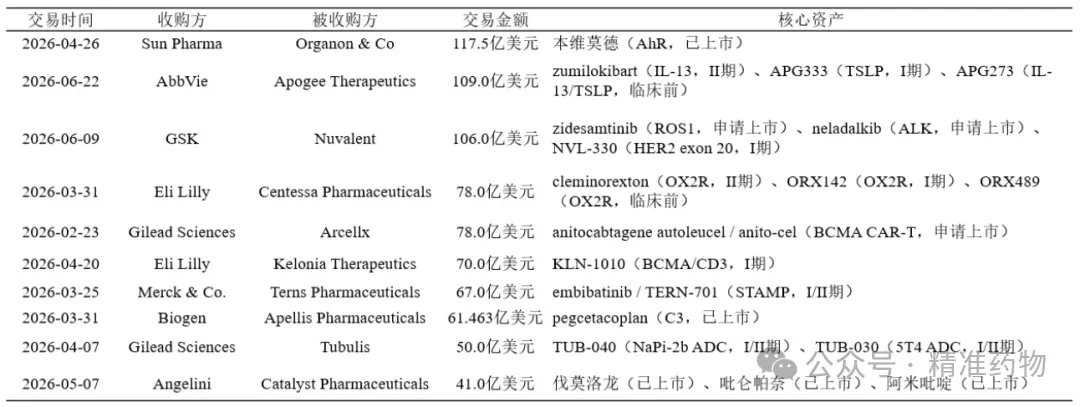

2026H1ofTop 10M&A Transactions

Although competition in these areas is intense, the patient population size, reimbursement pathways, and business models are relatively clear. For large pharmaceutical companies, acquiring a lung cancer drug nearing regulatory approval offers a far more calculable return on investment than acquiring an unvalidated platform.

Eli Lilly’s successive acquisitions also illustrate this point.

Weight-loss drugs have brought strong cash flow and market capitalization to Eli Lilly, but Eli Lilly has not pinned all its hopes on continuing to bet onGLP-1above. It is continuously acquiring in the fields of pain, oncology, neuroscience, and immunological diseases, using existing growth to seed the next round of expansion.

Acquisition4E Therapeutics, what Eli Lilly has its sights on is a portfolio of oral, non-opioid medications for chronic pain. While they may not become the next blockbuster weight-loss drug, the pain market is substantial, and there is a clear clinical need for non-opioid therapies.

This round of mergers and acquisitions has givenBiotechThe signal is clear: while interesting science remains important, science alone is no longer sufficient. Buyers are willing to pay a premium for certainty partially validated by clinical data, shorter time-to-market pathways, and products that can be rapidly absorbed by existing commercial systems.

Valuation Standards in the Innovative Drug Market Are Shifting from Technological Novelty to Risk Mitigation

03

M&A Rebounds

≠BiotechSpring is here

33A multi-billion-dollar acquisition can easily create an illusion:BiotechThe industry has fully recovered.

However, the reality is not so optimistic.

On one side, major pharmaceutical companies are writing checks worth billions of dollars; on the other, there are still numerousBiotechLayoffs, pipeline cuts, fundraising efforts, and even company sales. Capital has not returned evenly to all enterprises; instead, it is increasingly concentrated in a few projects with mature data.

High-quality assets are becoming increasingly expensive, while ordinary assets are becoming increasingly difficult to sell.

This is not a broad-based industry recovery, but rather a further intensification of sectoral divergence.

For the few companies with late-stage pipelines, it may currently be a rare seller’s market. With several large pharmaceutical companies simultaneously seeking growth assets, transaction prices can easily be driven up. However, for companies that only have early-stage platforms, lack human data, or whose clinical results lack differentiation, buyers have more options. They can wait, negotiate lower prices, or simply bypass these opportunities.

Therefore,1340$100 million does not mean that the capital winter has ended.

More accurately, the capital winter has merely changed its form: money has not disappeared, but the channels to access it have become narrower.

On one end are the few star assets fiercely contested by large pharmaceutical companies; on the other are the numerous ordinary ones still striving to extend their cash runway.Biotech。

Capital is sending the clearest message to the industry:

Not all innovations are valuable; only those that save buyers time and reduce risks have the potential to command high prices.

04

Buying More Does Not Mean Buying Right

Mergers and acquisitions can shorten R&D timelines but cannot circumvent biological risks.

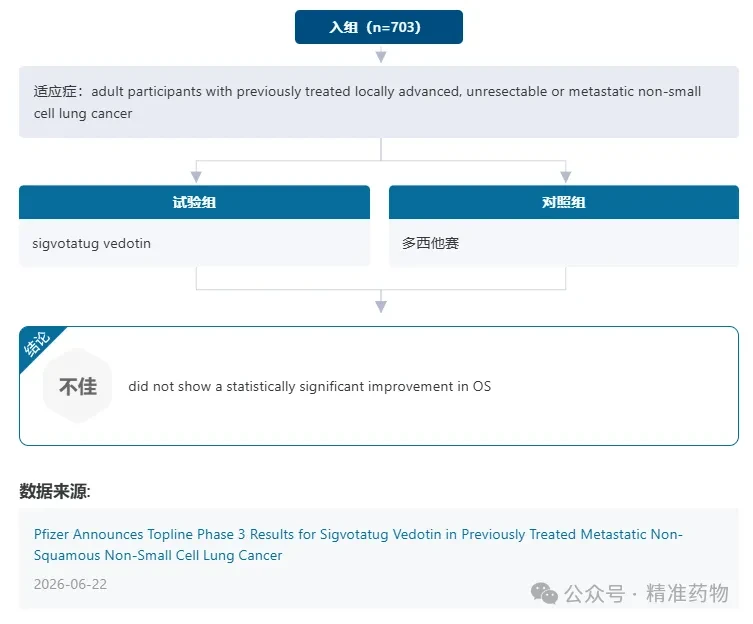

Pfizer is the most direct reminder.

2023year, Pfizer spent430Acquisition for $100 millionADCLeading EnterpriseSeagen, with the aim of rebuilding its oncology business and gaining matureADCR&D Platform.

But2026Year6In May, Pfizer announcedsigvotatug vedotinPhase III Results. This is an acquisitionSeagen, the first to announce pivotal clinical data for a novelADC. The results showed that the drug did not significantly improve overall survival compared with docetaxel in previously treated patients with non-squamous non-small cell lung cancer, and the trial failed to meet its primary endpoint.

sigvotatug vedotinofIIIPhaseToplineData

430Hundreds of millions of dollars can buy a technology platform, several marketed products, and an R&D team, but it cannot guarantee clinical success.

This is also the most easily overlooked aspect of the M&A boom.

Pharmaceutical company acquisitionBiotech, it does not eliminate risk, but rather transfers the risk from“Can candidate drugs be identified?”, transferred to“Can the candidate drug pass clinical, regulatory, and commercialization stages?”。

The higher the transaction amount, the greater the future sales expectations. Should the core project fail, the buyer would not only bear the R&D losses but also face goodwill impairment, pipeline contraction, and strategic realignment.

Today’s star deals may end up on the impairment list in a few years.

Nevertheless, large pharmaceutical companies will continue to make purchases.

For them, the risk of making a wrong acquisition is high, but the risk of not acquiring anything at all may be even higher. Patents on core products will expire, revenue gaps must be filled, and capital markets will not wait indefinitely for internal R&D to deliver results.

Mergers and acquisitions are not the safest option, but they may be the fastest among the remaining choices.

Final Remarks

Half a year1340hundred million US dollars, it seems that capital has regained confidence in innovative drugs.

But it is more likeBig PharmaA premium paid for anxiety.

As the patent cliff looms ever closer and internal R&D fails to guarantee the timely delivery of the next blockbuster drug, major pharmaceutical companies are forced to take their cash to the market, acquiring completed experiments, clinical data, and development timelines from others.

What this wave of mergers and acquisitions truly proves is not how wealthy pharmaceutical companies are, but rather how expensive time has become.

Big PharmaIt’s not that they’ve suddenly become wealthier. They just can’t afford to wait any longer.

Ref

https://www.statnews.com/2026/06/22/pharma-biotech-ma-boom-2026-deals-total-123-billion/

https://nextpharma.pharmcube.com/

https://www.fiercebiotech.com/biotech/fierce-biotech-layoff-tracker-2026

https://investors.nuvalent.com/

https://www.pfizer.com/news/press-release/press-release-detail/pfizer-announces-topline-phase-3-results-sigvotatug-vedotin

Disclaimer: The publication/reproduction of this article is solely for the purpose of disseminating information and does not imply endorsement of the views of this official WeChat account or verification of the authenticity of its content. Any judgments made based on this content are at your own risk.If there is any infringement, please inform us and it will be deleted immediately!

Long-press to follow this official account