Soared 95%: Kidney-Disease Biotech Alebund, Backed by Tencent and Lilly Asia Ventures, Goes Public—Exclusive Interview With an Early Investor

Alebund

Developer of Kidney and Chronic Disease Treatment Products

Tencent

Internet Comprehensive Service Provider

Lilly Asia Ventures

Biopharmaceutical Investment Management Institution

June 29 marked the Hong Kong IPO of Alebund Pharmaceuticals (Jiangsu) Limited, a clinical-stage biotech focused entirely on chronic kidney disease (CKD). At press time, its stock traded at HK$44, representing a gain of over 95% and valuing the company at approximately HK$15 billion.

Photo of the bell-ringing ceremony for the HKEX listing. Image source: the company

Founded in 2018, Alebund completed multiple financing rounds ahead of its listing, drawing investment from top-tier backers including Med-Fine Capital, Huagai Capital, Lilly Asia Ventures and Shenzhen Tencent Computer System Co., Ltd. | Tencent, with a pre-IPO post-money valuation of RMB 3.8 billion. Bai Yang, Partner at Med-Fine Capital, first crossed paths with Alebund’s founding team back in 2020, and the group’s deep domain expertise and forward-looking pipeline strategy immediately impressed him.

“I first met them in a tiny office in Hong Kong Plaza, Huangpu District, Shanghai,” Bai recalled. “The team only had five full-time employees then, yet they had already laid out a complete organizational framework. Dr. Xia Guoyao, a former venture capitalist turned entrepreneur, laid out a crystal-clear roadmap for financing and global expansion that reflected the long-term vision typical of institutional investors. Dr. Tian Jin, meanwhile, demonstrated unparalleled mastery of nephrology research. When I raised nuanced questions around clinical and regulatory hurdles in kidney disease development, he delivered concise, authoritative answers forged from decades of hands-on R&D experience.”

What struck Bai most profoundly, however, was how far the lean five-person team could see into the future. At a moment when multinational pharmaceutical giants were largely stepping back from nephrology research, Alebund set out to build a fully global pipeline targeting unmet CKD needs. Before 2020, chronic kidney disease represented a largely overlooked blue ocean for innovative drug developers. Stringent FDA clinical endpoint requirements and steep R&D costs drove most large multinationals out of the space, leaving only a handful of small and mid-sized biotechs to advance novel candidates. Bai saw a clear upside amid the industry exodus: hundreds of millions of patients worldwide suffered from CKD complications including hyperphosphatemia, IgA nephropathy and diabetic nephropathy, yet no new mechanistic therapies had reached the market for years.

“The massive pool of unmet clinical demand was an investment opportunity too substantial to ignore,” Bai said.

Six years on, nearly every strategic vision outlined in that modest Shanghai office has materialized. Core asset AP301 has progressed through Phase 3 trials and nears New Drug Application (NDA) submission; AP306 secured China’s Breakthrough Therapy Designation; and Alebund’s purpose-built Yangzhou manufacturing facility stands complete—a rare heavy-asset pre-launch investment for asset-light biotech operators.

Bai frames his firm’s early investment as a long-dated wager on human capital: “We could not map out every milestone of 2026 back in 2020, but we could identify a standout team solving a critical unmet medical need, and that was worth patient capital.”

Alebund has built a synergistic pipeline matrix centered on prevalent complications of chronic kidney disease (CKD).

An estimated 123.8 million Chinese patients live with CKD, yet therapeutic innovation in nephrology has lagged far behind breakthroughs in oncology and cardiovascular care for years. Worse, the prevalence of severe comorbidities rises exponentially as renal function deteriorates. Take hyperphosphatemia as an example: its incidence sits at just 7.3% for patients in CKD Stage G3a, climbing to 12.4% in G3b, 26.7% in G4 and 65.9% in G5. More than 95% of dialysis-dependent patients develop the condition.

These epidemiological data highlight a stark clinical disconnect: while hyperphosphatemia grows drastically more common and severe with advancing CKD, existing treatments carry poor patient adherence, significant side effects and limited efficacy—an unaddressed gap Alebund’s pipeline was built to fill.

Standard-of-care phosphate binders for hyperphosphatemia, namely Sanofi’s sevelamer carbonate and Takeda’s lanthanum carbonate, were approved over a decade ago. Globally, only two novel drug candidates for hyperphosphatemia are currently in clinical development: Alebund’s proprietary AP301 and AP306.

AP301, Alebund’s flagship asset, is a potential best-in-class phosphate binder indicated for hyperphosphatemia in CKD patients. Alebund acquired full global rights to AP301 from Vidasym with no additional milestone payments required. Compared to legacy phosphate binders, AP301 delivers superior phosphate-binding capacity, requires no chewing, features low volume expansion and exhibits zero systemic absorption—addressing core patient pain points including severe gastrointestinal adverse events and burdensome daily pill regimens that undermine treatment compliance.

Findings from the Phase 3 clinical trial conducted in China underscore AP301’s clinical edge: the candidate reduced serum phosphorus levels by 2.22 mg/dL over a 12-week treatment window, with a 66.7% long-term treatment success rate across 52 weeks, outperforming sevelamer carbonate’s respective benchmarks of 2.17 mg/dL and 58.6%. Less than 5% of participants discontinued treatment due to adverse safety events.

Alebund completed China’s Phase 3 trial of AP301 in November 2025, targeting domestic NDA filing in June 2026 alongside concurrent global Phase 3 multi-center trials across China and the U.S. The firm plans to file for FDA approval in Q3 2027, positioning AP301 as the first domestic Chinese hyperphosphatemia therapeutic candidate targeting global commercialization.

AP306, a potential first-in-class pan-phosphate transporter inhibitor also developed to treat hyperphosphatemia, blocks intestinal phosphate absorption and drastically cuts daily pill intake versus conventional binders.

Its novel mechanism simultaneously inhibits three key intestinal phosphate transporters—Napi-IIb, PiT-1 and PiT-2—to deliver deep, sustained serum phosphorus control, making it ideal for patients with refractory hyperphosphatemia or those requiring rigorous phosphate management. The asset secured Breakthrough Therapy Designation from China’s National Medical Products Administration (NMPA) in 2024.

Phase 2 clinical data demonstrates AP306’s transformative clinical value: nearly 95% of patients maintained controlled serum phosphorus levels after seven weeks of treatment, compared to a 50% success rate for traditional phosphate binder regimens, with average serum phosphorus reduced to the optimal 3.5–4.5 mg/dL range. Daily dosing requirements plummet from the 6–12 tablets required for legacy binders to just 2–3 tablets of AP306, with fewer than 5% of patients discontinuing therapy for safety reasons.

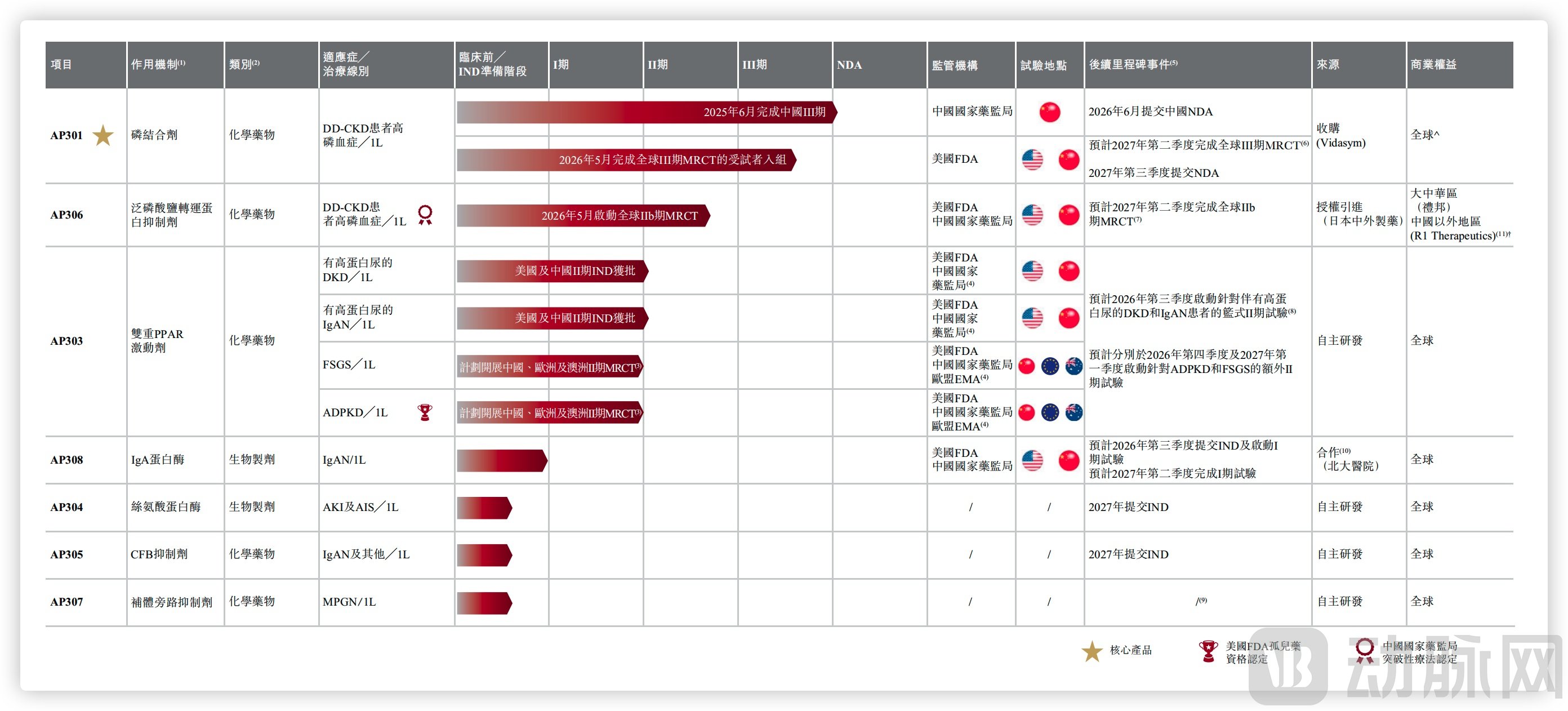

Alebund’s Pipeline Portfolio, Source: Prospectus

Beyond its dual hyperphosphatemia flagship assets AP301 and AP306, Alebund boasts a diversified pipeline spanning the full spectrum of chronic kidney disorders. AP601(Mixelot), a long-acting erythropoietin product already commercialized by Alebund, addresses renal anemia; AP303, a dual PPAR agonist, targets progressive nephropathies including diabetic nephropathy, IgA nephropathy, autosomal dominant polycystic kidney disease and focal segmental glomerulosclerosis, with global Phase 2 trials set to launch in Q3 2026. AP308, a recombinant IgA protease, enters the functional cure space for IgA nephropathy with the potential to redefine standard treatment paradigms for the indication. The firm further bolsters its early-stage portfolio with preclinical candidates AP304, AP305 and AP307.

Rather than pursuing isolated single-asset breakthroughs, Alebund structured its pipeline to address immediate symptomatic CKD complications first, before advancing disease-modifying root-cause therapies, covering pivotal clinical intervention points across the full CKD disease progression continuum.

Long before its lead candidates reached late-stage clinical trials, Alebund built out foundational infrastructure to support post-approval commercial rollout.

On the commercial channel front, Alebund secured exclusive Chinese marketing rights to Roche’s long-acting EPO Mixelot back in 2023. The asset generated roughly RMB 30 million in revenue for Alebund in 2025, but its strategic value extends far beyond near-term top-line gains: Mixelot’s core patient base consists of long-term dialysis patients, precisely the target demographic for AP306 upon launch.

Over years of promoting Mixelot, Alebund established direct relationships with nephrology specialists at hundreds of tier-one hospitals, secured dialysis center access and navigated national medical insurance channels. Nephrology patients demonstrate exceptionally high physician loyalty, meaning Alebund will enter the market for its proprietary innovative drugs with an established, trusted network rather than building commercial reach from scratch.

For manufacturing capacity, phosphate binders require chronic, high-volume dosing for millions of patients. Under China’s thin-margin medical insurance pricing framework for chronic disease therapies, contract development and manufacturing organization (CDMO) partnerships cannot sustain cost competitiveness long-term. Alebund’s in-house production capacity will shield AP301 against pricing pressure from centralized volume-based procurement (the 10th round of national bulk procurement capped sevelamer carbonate pricing at HK$22.47 per bottle), while guaranteeing consistent supply for AP306 at launch.

The firm’s fully completed Yangzhou manufacturing base delivers an annual design output of 200 metric tons, enabling end-to-end control over R&D, production and commercialization.

Sustained capital inflow underpinned Alebund’s pipeline expansion. The firm booked RMB 6.525 million in revenue in 2024 and RMB 30.556 million in 2025, all originating from Mixelot’s commercial sales, yet recorded R&D expenditures of RMB 235 million and RMB 373 million in the respective years. As proprietary candidates advance into costly late-stage clinical phases, revenue generated from Mixelot alone could no longer offset R&D outlays, making the Hong Kong IPO a necessary strategic step.

The IPO proceeds of HK$1.181 billion will be allocated as follows: 34% toward AP301’s domestic NDA filing and global Phase 3 multi-center trials, 37% to global Phase 2b trials of AP306 plus pipeline advancement for AP308, AP303 and other preclinical candidates, and 12% for capacity upgrades at the Yangzhou manufacturing plant and pre-launch commercialization preparations for future approved therapies.

The chronic kidney disease treatment landscape is shifting from symptomatic management to precision disease intervention, marking a critical inflection point for China’s biotech sector.

For years, most Chinese clinical-stage biotechs followed a blockbuster single-asset playbook: advancing one potential best-in-class or first-in-class molecular candidate to generate clinical data-driven valuation upside, before exiting via business development deals or commercialization launches. This strategy has delivered results in fast-cycle therapeutic areas like oncology, yet faces structural headwinds in chronic nephrology. CKD patient populations are highly stratified with divergent payment capacity, and even high-efficacy single molecular candidates fail to address the full spectrum of clinical scenarios across disease stages.

Alebund’s differentiated strategy rejects the pursuit of incremental molecular improvements within narrow indications, instead building iterative, complementary asset tiers within the same therapeutic space. AP301 targets market share capture via substitution of legacy standard-of-care drugs within the national medical insurance system, while AP306 unlocks premium pricing with its novel mechanism of action to capture high-value patient segments. This dual-asset framework delivers built-in commercial synergy long before Alebund launches any self-developed innovative drug.

Complicating matters further, CKD follows a lengthy disease progression trajectory with overlapping comorbidities, and patient clinical needs evolve sequentially from biomarker control to disease progression delay to potential functional cures—no single therapeutic molecule can fully cover this spectrum. Alebund’s pipeline roadmap begins with complication-focused treatments before advancing root-cause disease-modifying therapies, positioning the firm to capture pivotal intervention touchpoints across the full nephrology care continuum.

While the broader biotech industry debates the transition from single-product developers to fully integrated therapeutic platforms, Alebund has delivered a tangible playbook for chronic disease-focused firms. In nephrology, the company argues, the most durable competitive moat lies not in isolated molecular technical superiority, but in a portfolio of therapies that seamlessly address every clinical scenario along the patient’s disease journey. Rather than debating whether Alebund qualifies as China’s first pure-play nephrology IPO candidate, investors should focus on whether its synergistic pipeline logic can translate into tangible improvements in patient quality of life and sustainable long-term commercial returns.