NeuroGen, the Drugmaker Behind a RMB 950 Million Single Product, Files for Hong Kong IPO After Taking Over UCB's China Assets

NeuroGen

Biopharmaceutical Manufacturer

UCB

Biopharmaceutical and Specialty Chemicals Developer

In June 2024, a transaction that sparked industry-wide discussion was quietly finalized. UCB, a global pharmaceutical company headquartered in Belgium, sold its entire commercial operations in China to funds under C-Bridge Capital (CBC) and ATIC, owned by the United Arab Emirates' sovereign wealth fund.

Following the transaction, a new entity reemerged under the name NeuroGen Pharma Limited. Two years later, in June 2026, NeuroGen Pharma filed its prospectus with the Hong Kong Stock Exchange, seeking to establish a new valuation in the Hong Kong equity market.

This is not a story of NeuroGen starting from scratch, but one that must still be retold.

1From the Joint Venture in 1997 to the Full Transfer in 2024

NeuroGen's origins can be traced back to 1997.

At that time, UCB established its presence in China under its Schwarz Pharma brand, gradually building a commercialization system covering neurological disorders such as epilepsy and Parkinson's disease. Over the following two decades, UCB accumulated an epilepsy drug portfolio in China centered on Vimpat (lacosamide) and Keppra (levetiracetam), forming substantial terminal coverage capabilities.

However, with UCB's global strategic realignment, the company is increasingly inclined to concentrate its resources on worldwide R&D and brand building, making its direct commercial operations in the Chinese market an asset that could be appropriately divested.

On June 11, 2024, C-Bridge V completed the acquisition of the relevant businesses, with ATIC Second International Investment Company LLC (a subsidiary of Mubadala's technology investment platform) simultaneously taking an equity stake. Each party initially held a 50% interest, which corresponded to 47.62% of the total shares in the restructured entity. The remaining 4.76% was allocated to an Employee Stock Ownership Plan (ESOP) and held in trust by ThriveCap Ltd. and AxisPoint Holdings Ltd.

This acquisition laid the foundation for NeuroGen's infrastructure and defined its initial business logic: leveraging UCB's legacy sales network and product assets to establish a stable base of commercial revenue, while incubating its proprietary pipeline.

In November 2024, NeuroGen and UCB officially signed a new commercial cooperation agreement, clarifying the continued promotional rights for five of UCB's core branded products in China, with the agreement term extended to November 2031.

This agreement provides significant assurance for NeuroGen's revenue visibility and offers a quantifiable time anchor for the commercial narrative surrounding its Hong Kong listing.

2Keppra: The “Ballast Stone” of the Epilepsy Market Behind 70% of Revenue

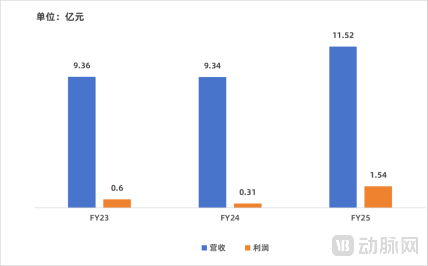

An examination of NeuroGen's financial structure reveals that a single product exerts absolute dominance. In 2025, the acquired assets (NeuroGen Zhuhai) generated RMB 1.152 billion in revenue, with Keppra (levetiracetam) alone contributing RMB 949 million, accounting for a substantial 71.9% of total revenue. This second-generation broad-spectrum antiepileptic drug, which entered the Chinese market in 2006, is not only the cornerstone of NeuroGen's revenue but also key to understanding the stability of its business operations.

Keppra's market position was not achieved overnight. As the originator product of levetiracetam, it has established strong brand recognition and prescribing habits among physicians and patients through nearly two decades of clinical use and market cultivation. The characteristics of the epilepsy treatment field have reinforced this barrier: epilepsy is a chronic condition requiring long-term or even lifelong medication, resulting in high patient adherence and brand loyalty.

Meanwhile, the conversion risks associated with neurological medications have made physicians more cautious in their prescribing practices. These characteristics collectively establish a robust "moat" for Keppra, enabling it to maintain its market leadership despite subsequent generic competition by leveraging its brand reputation, recognized efficacy, and trust among both physicians and patients.

NeuroGen's strategic footprint in the epilepsy field extends beyond a single product. Vimpat (lacosamide), a third-generation antiepileptic drug approved in 2018 and obtained through the acquisition, focuses on focal seizures and contributed RMB 218 million in revenue in 2025, accounting for 16.5% of the total.

It forms an effective portfolio strategy with Keppra: Keppra, as a broad-spectrum foundational medication, covers a wide patient population with epilepsy and provides stable cash flow; Vimpat, as a next-generation specialized product, targets more segmented treatment scenarios with higher efficacy demands, representing future growth potential. This "cornerstone product + growth product" combination effectively balances current revenue with future opportunities.

3From CNS to Allergy: Horizontal Expansion of “Specialization”

While solidifying its position in the CNS sector, NeuroGen has horizontally expanded its business boundaries into the field of allergic diseases through the acquisition of Zyrtec (cetirizine) and Xyzal (levocetirizine). This strategic move is not merely a simple addition of products, but a synergistic extension based on the logic of "specialization."

As an over-the-counter (OTC) medication, Zyrtec holds strategic value that significantly differs from prescription drugs. It bypasses complex hospital access and medical insurance negotiation processes, directly reaching end consumers through retail pharmacies, pharmacy outlets near hospitals, and e-commerce platforms. In 2025, Zyrtec generated RMB 131 million in revenue, providing NeuroGen with a stable cash flow unaffected by hospital policy cycles.

More importantly, as UCB's original research brand, Zyrtec enjoys exceptionally high brand awareness among consumers. This direct-to-consumer brand equity effectively complements the professional brand image of prescription drugs.

From a business synergy perspective, the dual-domain layout of "CNS + Allergy" has an inherent logic. Although neurology and allergy are distinct disciplines, the target physician groups of their marketing teams partially overlap at the hospital level, allowing academic promotion resources to generate synergistic effects.

At a deeper level, both fall within "specialty therapeutic areas," sharing common characteristics such as high barriers to entry, the need for long-term patient management, and high brand loyalty. NeuroGen has chosen a focused specialty pathway, rather than adopting the broad-based model of a generalist pharmaceutical company.

Xyzal (levocetirizine), as a second-generation H1 receptor antagonist, further enriches NeuroGen's product portfolio in the allergy field with its advantage of "low sedation" side effects, meeting the differentiated needs of patients for drug tolerability.

The sales model for allergy medications through retail and e-commerce channels complements the hospital-based market relied upon by prescription drugs for conditions such as epilepsy and Parkinson's disease, jointly forming the initial framework of NeuroGen's omnichannel commercialization capability characterized by "integration of in-hospital and out-of-hospital markets, with equal emphasis on prescription and retail sectors."

4AJOVY Enters the Fray: Seizing a Share of the Billion-Dollar Migraine Market

If the product portfolio acquired through M&A constitutes NeuroGen's "core foundation," then its 2026 moves clearly point to its future "growth engine."

In June 2026, AJOVY (fremanezumab), indicated for the prevention of migraine, received marketing approval from China's National Medical Products Administration (NMPA). This product was not acquired through a merger or acquisition; rather, it is a key asset proactively in-licensed by NeuroGen.

The introduction of AJOVY marks a new phase in NeuroGen's platform-based strategy, combining "self-sustaining growth" with "external infusion."

As early as April 2026, NeuroGen entered into a licensing agreement with Teva for the introduction of AJOVY, demonstrating its capability to acquire cutting-edge global innovative drug assets.

AJOVY is highly competitive, being the first and only CGRP (calcitonin gene-related peptide) antagonist approved by the U.S. FDA for both pediatric episodic migraine and adult migraine. The CGRP target represents one of the most significant breakthroughs in migraine preventive therapy in recent years; compared to traditional medications, it offers a more precise mechanism of action and superior preventive efficacy.

Migraine, as a common neurological disorder, has a large patient population in China, resulting in significant unmet clinical needs.

The introduction of CGRP-targeted therapies directly taps into a blue-ocean market experiencing rapid growth. For NeuroGen, AJOVY is not only a potential blockbuster product but also a "spearhead" for penetrating this vast market. Its launch will significantly enhance NeuroGen's professional reputation in neurology and elevate the technological sophistication of its product portfolio. In the coming years, it is poised to become another key revenue pillar following Keppra, thereby breaking through NeuroGen's growth ceiling.

As the world's first CGRP antagonist approved for dual indications (pediatric and adult), AJOVY represents not only a pivotal step in NeuroGen's strategic expansion from "acquisition and integration" to "innovative licensing-in," but also its core weapon for capturing China's billion-yuan migraine prevention market.

Its commercial success or failure will directly test the effectiveness of NeuroGen's "introduction + commercialization" dual-wheel drive model.

5Pipeline Strategy: The Calculations Behind Acquisitions and In-licensing

In addition to its marketed products, NeuroGen's pipeline of investigational drugs also reveals its clear strategic "calculations."

The pipeline strategy does not pursue a "broad-net" approach focused on sheer volume; instead, it concentrates on the CNS and pain management sectors, acquiring or in-licensing assets that are near commercialization or possess clear differentiation to rapidly build competitive capability.

The most advanced candidate in the current pipeline is NG1807, an orally dissolving film formulation of brexpiprazole for the treatment of schizophrenia, with its New Drug Application (NDA) currently under regulatory review. The core differentiator of this product lies in its "orally dissolving film" dosage form, which effectively addresses the common issue of "drug hiding" among patients with schizophrenia, thereby ensuring medication adherence and demonstrating clear clinical value. NeuroGen also plans to expand the indications to include agitation associated with Alzheimer's disease, further unlocking market potential.

NG1806 is a postoperative pain management drug acquired in January 2026. It is positioned as "China's first-in-class, dual-mechanism, long-acting non-opioid analgesic," capable of providing sustained pain relief for over 72 hours. Amidst stringent global regulations on the risk of opioid abuse, a long-acting, non-opioid postoperative analgesic holds significant market demand and policy advantages.

Another investigational drug, NG1706, acquired through an in-licensing collaboration with Xgene, is an oral non-opioid analgesic. Its uniqueness lies in its dual mechanism of action, simultaneously targeting COX and α2δ calcium channels, aiming to treat both neuropathic and nociceptive pain, thereby covering a broader population of pain patients.

A review of NeuroGen's pipeline layout clearly reveals its strategic logic: focusing on areas of strength (CNS, pain), avoiding early-stage risks (by in-licensing assets nearing commercialization or in late-stage clinical trials), and pursuing differentiated value (addressing drug hiding, long-acting non-opioids, dual mechanisms, etc.). This "in-licensing + acquisition" model for pipeline building is consistent with its approach of rapidly establishing a commercial platform through acquisitions, with the core objective of accelerating value realization and reducing uncertainty.

6Commercialization Foundation: Covering 18,000 Hospitals + 100,000 Retail Pharmacies

The value of any pharmaceutical product must ultimately be realized through commercialization.

NeuroGen possesses a mature foundation in this regard—not built from scratch, but inherited from UCB—which constitutes one of the most solid pillars of its platform-based strategy. This commercialization network functions like "capillaries" spreading across China, deeply reaching every terminal point of the healthcare market.

As of 2025, NeuroGen's terminal network covered more than 18,000 hospitals across China; in the out-of-hospital market, its products reached approximately 100,000 retail pharmacies through its distribution network. This depth and breadth of coverage ensured seamless connectivity from core Grade A tertiary hospitals to primary healthcare institutions, and further to extensive retail terminals.

Its business model exhibits an "omni-channel" characteristic: prescription drugs are sold through public hospitals and pharmacies adjacent to hospitals, while OTC products reach consumers directly via retail chains and e-commerce platforms. This channel mix enhances NeuroGen's resilience against policy fluctuations in any single channel. On the production side, its self-owned manufacturing base in Zhuhai is responsible for producing the core products, Keppra tablets and oral solution, ensuring supply chain security and cost controllability for key products.

Strong commercialization capabilities are ultimately reflected in financial metrics.

In 2025, at the group level (post-acquisition), the net operating cash flow amounted to RMB 340 million, with cash and cash equivalents reaching RMB 729 million by the end of the period. Meanwhile, NeuroGen maintained robust profitability, reporting an adjusted EBITDA of RMB 494 million.

(Note: Statistics are based on NeuroGen Zhuhai as the reporting entity.)

Robust cash flow and ample cash reserves provide sufficient "ammunition" for the subsequent in-licensing of pipeline assets, market expansion, and potential further mergers and acquisitions.