Chengdu Adds Another Biotech IPO as HJ Science Debuts on the Hong Kong Stock Exchange

HJ Science

Innovative Small Molecule Drug Research, Development, and Production

On June 23, HJ Science was officially listed on the Main Board of the Hong Kong Stock Exchange.

Over the past week, this company has made significant waves in the market. HJ Science held its initial public offering from June 12 to 17, pricing its shares at HK$81.80 each. The company planned to globally offer 13.6 million H shares, raising a maximum of approximately HK$1.112 billion, with a total market capitalization of around HK$6.02 billion post-listing.

Even more striking were the margin financing figures: by the close of the IPO subscription period, margin-financed subscriptions totaled approximately HK$129.8 billion. Based on the public offering's fundraising target of HK$110 million, this represents an oversubscription of roughly 1,166 times—a level of enthusiasm for new share subscriptions that has been rare among recent Chapter 18A IPOs.

The cornerstone investor lineup reflects the stance of professional institutions, with six entities—Foresight Fund, Kaibo Private Equity, Lake Bleu Capital, Sage Partners, Panjing Fund, and Taikang Life Insurance—collectively subscribing to $65 million, accounting for 45.7% of the global offering. The willingness of a long-term institutional investor like Taikang Life to lock up its shares indicates that, in the eyes of professional investors, this company is not merely a cash-burning biotech firm.

What truly warrants attention is this: How has a biotech firm headquartered in Chengdu's Wenjiang Medical City secured cumulative investments of approximately RMB 619 million over the past eight years from Shanghai State-owned Capital Investment (holding ~9.2%), Legend Capital (holding ~7.08%), and Junshi Biosciences (holding ~2.1%), thereby driving its valuation to RMB 2.7 billion?

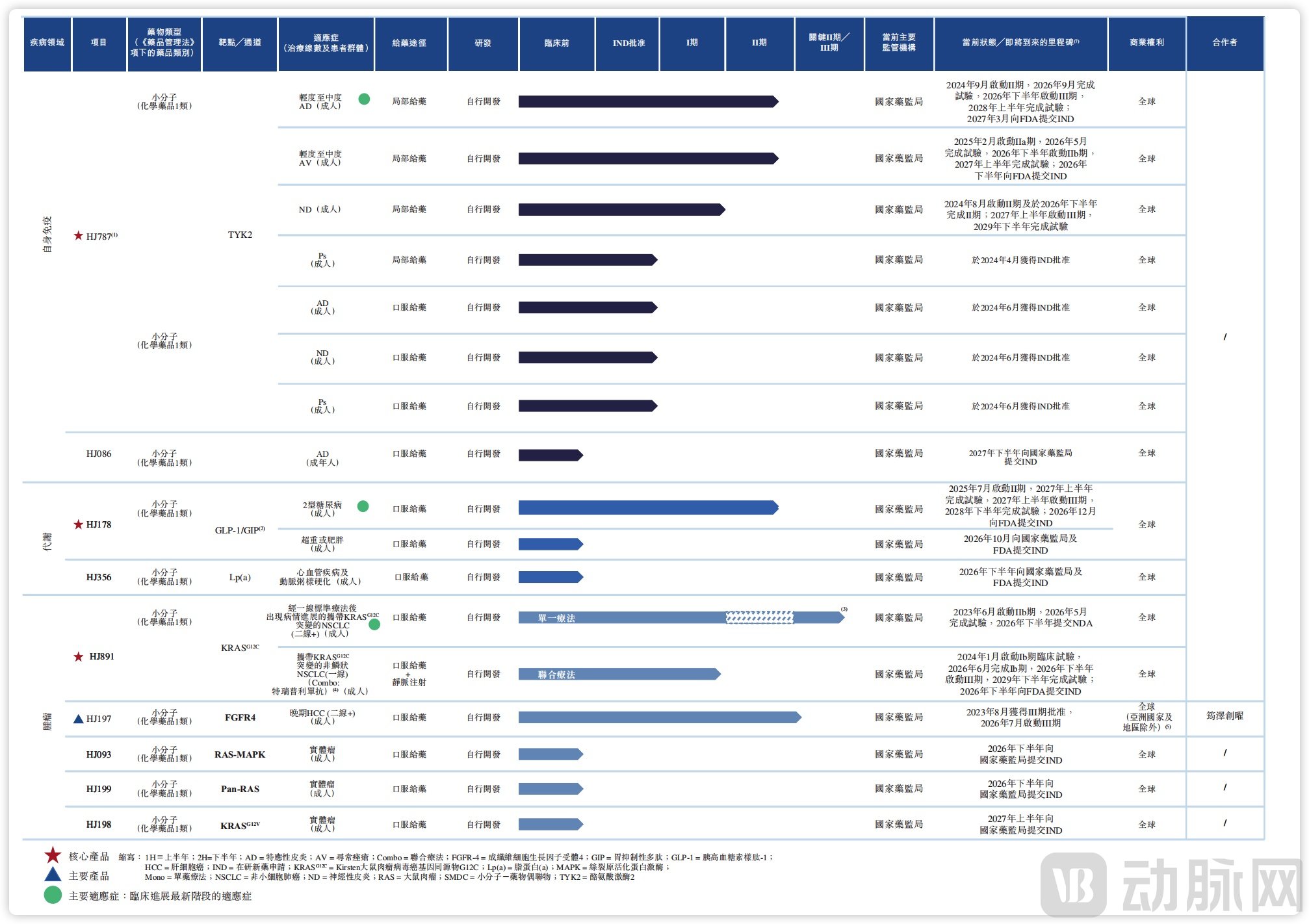

Corporate Pipeline Layout, Source: Prospectus

The answer lies not in the novel targets it selected, but in its choice of a development path that most consider difficult and unsexy, yet is in critical clinical shortage—elevating the value of popular targets from the molecular level to the formulation and delivery route levels.

High-prevalence chronic diseases are driving an engineering-led upgrade in the industry.

Atopic dermatitis (AD) is one of the most common chronic inflammatory skin diseases, affecting hundreds of millions of people worldwide. The population of patients with mild-to-moderate AD in China is particularly large. However, a close examination of the current treatment landscape for this group reveals a sobering reality.

Topical corticosteroids are the most commonly used and effective treatment; however, long-term use carries risks of skin atrophy, telangiectasia, and rebound effects, leaving countless patients in a dilemma where neither continuing nor discontinuing therapy seems viable. In upgraded treatment regimens, topical PDE4 inhibitors and non-steroidal AhR agonists offer alternatives, but their efficacy has a clear ceiling, and local irritant reactions cannot be overlooked.

As for oral JAK inhibitors, their focus lies in the field of moderate-to-severe AD, making them inherently less suitable for the long-term management of mild-to-moderate cases. After all, applying a systemic immunomodulatory regimen to patients with milder disease courses makes it difficult to balance efficacy and risk. Furthermore, the FDA's black box warning for pan-JAK inhibitors has further closed the door on their use in this setting.

Therefore, the unmet clinical needs in mild-to-moderate AD, including similar conditions such as neurodermatitis (ND) and certain cases of acne vulgaris (AV), have consistently pointed in one direction: potent local anti-inflammatory efficacy with minimal systemic exposure, ideally below the limit of detection. This represents the theoretical sweet spot for topical targeted therapies.

Given the clear rationale, why has no one previously developed a topical TYK2 ointment and advanced it to late-stage clinical trials?

The core challenges lie in medicinal chemistry and formulation engineering. As TYK2 is an intracellular kinase target, achieving effective penetration of small-molecule inhibitors from the stratum corneum and epidermis to the site of action in dermal immune cells, while ensuring minimal transdermal systemic absorption, imposes stringent balancing requirements on molecular parameters—such as the oil-water partition coefficient, solubility, and permeability coefficient—as well as on the formulation engineering of the ointment base.

In simple terms, efficacy requires sufficient penetration, but excessive penetration compromises the safety profile essential for topical application. Furthermore, Phase II clinical trials require robust statistical data to demonstrate that topical selective TYK2 inhibitors are superior to placebo ointments. Consequently, this therapeutic area has long remained a vacuum: deemed too small by large pharmaceutical companies while being beyond the capabilities of smaller firms.

HJ Science's HJ787 specifically targets this therapeutic area. According to the prospectus, as of the Latest Practicable Date, HJ787 was the only topical selective TYK2 inhibitor in clinical development in China, and no topical or systemic TYK2 inhibitors had been approved in China for the treatment of AD. Phase 2 data in patients with mild-to-moderate AD showed that the EASI-75 response rates for the three dose groups (0.5% once daily, 3% once daily, and 3% twice daily) were 25.0%, 30.0%, and 62.5%, respectively. All treatment-related adverse events were mild, and no serious adverse events leading to discontinuation were observed.

More critically, the company's disclosed safety profile demonstrates minimal systemic absorption following local administration, which constitutes the fundamental basis for the viability of the topical route. The Phase II trial for AD is expected to be completed in September 2026, with the Phase III trial launching in the second half of the year. The Phase IIb trial for acne vulgaris is advancing concurrently, while the Phase III window for neurodermatitis is targeted for the first half of 2027.

The strategic rationale behind this pipeline warrants attention. Rather than aiming to outperform oral TYK2 inhibitors, it seeks to define a new category of localized targeted therapy—one that offers significantly superior efficacy compared to conventional non-steroidal topical agents and a better safety profile than pan-JAK inhibitors. This makes it well-suited for chronic disease management, characterized by long-term, recurrent treatment needs across a large population of outpatients and those receiving care outside hospital settings.

Novo Nordisk and Eli Lilly, the two industry giants, have already demonstrated at major industry conferences in 2026 that the maintenance therapy market will be a significant blue-ocean growth opportunity.

The GLP-1 sector no longer requires any endorsement. Drugs represented by semaglutide and tirzepatide have demonstrated the immense commercial potential of weight loss and glucose-lowering therapies through their injectable formulations. Yet, it is precisely this success that has brought another market undercurrent to the surface. Once consensus on efficacy is established, the limiting factors shift from whether the treatments are effective to whether patients can and will adhere to them long-term.

Barriers to injection, gastrointestinal side effects such as nausea, vomiting, and diarrhea, along with multiple factors including cold chain logistics, supply, and reimbursement, are essentially narrowing market penetration. A growing consensus in the industry holds that the next wave of growth for GLP-1 therapies will not come from squeezing out an additional 10% weight-loss efficacy from injectables, but rather from developing oral, non-peptide small-molecule drugs with better tolerability and more controllable production costs and supply chains—so that they can be adopted in primary care clinics and home settings.

HJ Science's HJ178 follows the non-peptide oral GLP-1/GIP dual-target pathway, currently in Phase 1b/2a clinical trials, primarily targeting type 2 diabetes and selected overweight/obesity indications.

The prospectus emphasizes the optimization in molecular design to reduce the side effect profile characteristic of classic GLP-1 peptides (particularly nausea, vomiting, and psychiatric adverse events), as well as the inherent advantages of oral small-molecule formulations for long-term disease management.

However, this pipeline is not a frontrunner in terms of development progress. In the global landscape of oral GLP-1 therapies, Eli Lilly's orforglipron is already approaching its NDA submission, while domestic players such as Hengrui Medicine and Huadong Medicine also have their oral candidates at various stages of development. HJ Science's rationale for including this asset in its portfolio is clear: it does not expect HJ178 to single-handedly underpin its listing valuation, but rather bets on the long-term structural value of the oral small-molecule chronic disease therapeutic sector.

The third notable industry shift occurs in precision oncology.

The story of KRAS G12C is well-known. Amgen's sotorasib and BMS's adagrasib transformed this once "undruggable" target into a druggable one. In China, Genfleet/Innovent's fulzerasib, InventisBio's garsorasib, and Jacobio's glecirasib have also been approved and included in the National Reimbursement Drug List, significantly compressing the commercial potential for later-line monotherapy.

The true next battleground for KRAS G12C inhibitors lies not in later-line monotherapy, but in two directions: first, optimizing safety profiles and oral outpatient administration to better suit long-term combination therapy; second, advancing into first-line combination regimens with PD-1/PD-L1 inhibitors.

HJ Science's HJ891 (an oral covalent KRAS G12C inhibitor) is strategically positioned at this juncture, emphasizing the selective advantage conferred by its lung/tissue-enriched properties, while prioritizing clinical development efforts on a monotherapy Phase 2b trial and a Phase 1b/3 trial in combination with Junshi Biosciences' toripalimab.

The prospectus reveals that in the PD-L1 ≥50% population, the combination therapy cohort achieved an objective response rate (ORR) of 92.3% (based on a small sample size), compared to an ORR of 47.2% for monotherapy. The incidence of grade 3 or higher adverse events was only 13.5%, significantly lower than that of existing products. While these figures require validation through larger sample sizes and Phase III trials, the strategic positioning is spot-on. Amidst intense price competition among marketed competitors in later-line settings, the key driver supporting valuation growth lies in the first-line combination therapy segment—a position not yet fully captured.

Notably, Junshi Biosciences is both a shareholder of HJ Science (holding approximately 2.1% equity) and the industry partner that has secured the Asian rights to HJ891 through a licensing agreement (signed in 2020 with an upfront payment). This dual tie-up via equity and licensing underscores the intrinsic potential value of the pipeline more effectively than pure financial investment alone.

Examining HJ Science's entry strategies across three niche sectors reveals a clear logical chain underpinning its choices, with this chain originating from a single individual.

Founder Ji Jianxin, 50, is a leading figure under the Chinese Academy of Sciences' "Hundred Talents Program" and the National "Ten Thousand Talents Program." With an academic foundation in medicinal chemistry and molecular pharmacology, he conducted postdoctoral research at Vanderbilt University in the United States.

The most pivotal phase of his career was not in academia, but in industry. In 2007, Ji Jianxin joined Chengdu Diao Pharmaceutical, rising through the ranks to Executive Vice President. He played a key role in hard-fought battles such as securing EU registration for Diao's Xinxuekang Capsules, marking a significant milestone for Chinese chemical drugs going global. Starting in 2017, he also served as a member of the Investment Decision Committee of CAS Venture Capital. That same year, he left Diao to found HJ Science.

Core members, including COO Yang Xiangyu, also hail from the Diao drug development system. The early founding team of HJ Science is essentially a hands-on team with comprehensive expertise in the full industrialization chain of small molecules. This background is reflected in its R&D strategy: HJ Science resembles less a trend-chasing biotech company and more an engineering-driven organization focused on small molecules.

Its competitive moat lies not in discovering targets invisible to others, but in transforming each mature target into product forms better suited for large-scale clinical use and long-term management through selective optimization, refinement of physicochemical properties, and reengineering of dosage forms and administration routes.

In addition to the three core pipelines mentioned earlier, HJ Science also has an oral FGFR4-selective inhibitor, HJ197, in clinical development for advanced hepatocellular carcinoma, along with several preclinical candidate pipelines. While these may not necessarily become blockbusters, their very existence points to a clear direction: like the three core assets, they were all incubated using the same integrated system for screening, design, formulation, and clinical translation. This is a testament to the company's platform capabilities.

Approximately 80% of the funds raised will be allocated to advancing clinical development of the pipeline. The underlying rationale is straightforward: rather than incurring high costs to build a sales team, the focus is on achieving Phase III milestones first, leveraging data to secure future commercialization prospects.

The clamor of an IPO will soon fade; the true test for an innovative pharmaceutical company always begins after the opening bell.

SDIC, Legend Capital, Junshi Biosciences, and Taikang are not betting on a single miracle drug, but rather on a set of engineering capabilities that refine and thoroughly exploit mature targets to suit China's specific context. The next wave of innovation in China's pharmaceutical industry will not belong exclusively to companies that identify the newest targets; it will also include those that leverage engineering approaches to transform validated targets into therapies optimized for long-term patient use, widely prescribed by physicians across specialties, and supported by robust, large-scale supply chains.