Lannacheng Biotech Refiles for HKEX Listing With 109-Minute Shelf-Life Radiopharma Business

LNCYT

Radiopharmaceutical Developer

For most innovative drugs, shelf life is measured in years; for radiopharmaceuticals, it is minutes.

On June 12, 2026, Lannacheng Biotechnology Co., Ltd. refiled its listing application with the Hong Kong Stock Exchange.

This nuclear medicine innovation platform, spun off from Dongcheng Pharmaceutical, is once again knocking on the door of the capital market with a pipeline comprising 13 candidates, cumulative financing of RMB 1.031 billion, and a post-money valuation of RMB 3.291 billion. Unlike conventional innovative drugs, its core pipeline products have a shelf life of only 109 minutes from production to administration.

In the context of China's nuclear medicine industry, Lannacheng's filing has provided a window into the sector.

Lannacheng was not founded by a few scientists starting from scratch with angel investment; rather, it is an independent platform created by Dongcheng Pharmaceutical through the repackaging of its accumulated innovative nuclear medicine assets within its corporate system for separate development. The advantages are evident: the parent company has ten years of expertise in the nuclear medicine sector, and assets such as isotope supply, GMP systems, and the network of radiopharmacies are all inheritable assets.

The fundraising journey also reflects investor sentiment: Series A raised RMB 40 million → Series B raised RMB 200 million → Series B+ raised RMB 300 million → Series C raised RMB 491 million (closed in July 2025), resulting in a post-money valuation of approximately RMB 3.29 billion. Investors participating in this round include Shenzhen Capital Group-affiliated funds and the Greater Bay Area Fund under the National Social Security Fund—often referred to as "national team" investors. This is not speculative capital chasing hype, but strategic bets on one of the earliest companies to successfully establish a closed-loop business model for nuclear pharmaceuticals.

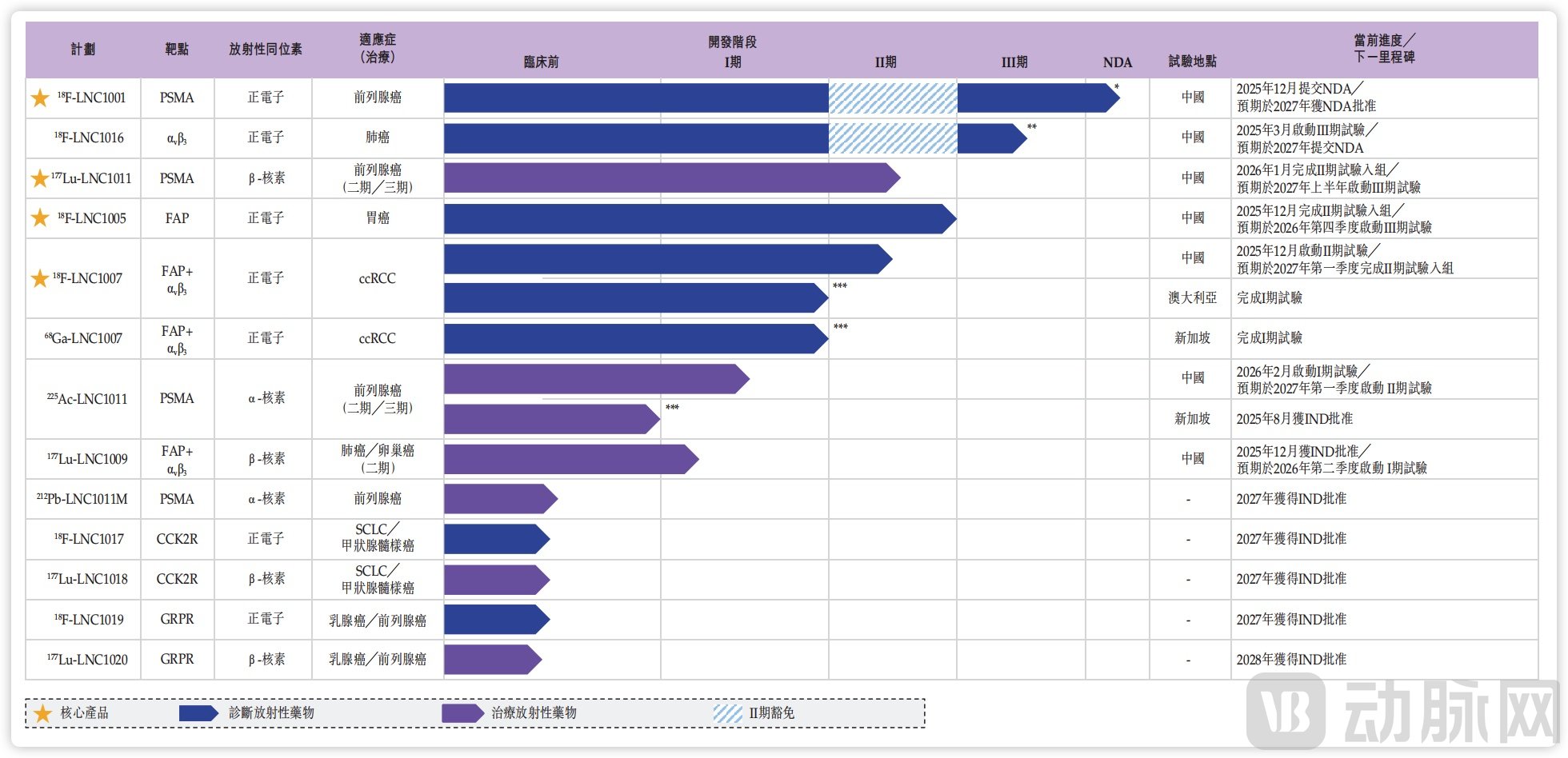

Backed by Dongcheng, the prospectus lists 13 candidate drugs (7 diagnostic and 6 therapeutic), with Frost & Sullivan bestowing the title of "ranked first in China for the number of clinical-stage theranostic radiopharmaceuticals."

Corporate Pipeline Layout, Source: Prospectus

The sheer number of pipeline assets is of limited significance in itself; more important is the underlying strategic logic governing their distribution across the three development stages.

The first phase is the near-term realization of 18F-LNC1001.

This is the anchor of the entire prospectus.

18F-LNC1001 is a PSMA-targeted PET imaging agent for prostate cancer. The New Drug Application (NDA) was submitted in December 2025, and it is poised to become the first 18F-labeled PSMA diagnostic agent approved in China. Compared with domestic competitors, it offers advantages such as a longer half-life, superior image quality, and suitability for long-distance distribution. Data from two completed Phase III clinical trials (enrolling a total of 488 patients) demonstrated a specificity of 93% in newly diagnosed patients and a positive predictive value exceeding 82% in patients with biochemical recurrence.

The message to the capital markets is clear: if approved smoothly, this will not merely add another imaging agent to the market, but will enable nuclear medicine departments to prescribe domestically produced PSMA PET radiopharmaceuticals that are compliant, reimbursable, and traceable for the first time. More importantly, without precise PSMA imaging for patient selection, subsequent 177Lu therapy would lack precision.

Its strategic value lies not only in revenue but also in paving the way for future therapeutic drugs.

Phase II is aimed at the long-term positioning of 177Lu-LNC1011 and alpha-emitting radionuclides.

177Lu-LNC1011 is a PSMA-targeted therapeutic radiopharmaceutical currently in Phase II clinical trials, with the prospectus disclosing that Phase III clinical trials will commence in the first half of 2027. It forms a diagnostic-therapeutic closed loop for prostate cancer together with 18F-LNC1001. This constitutes the core of Lannacheng's commercialization narrative: leveraging the diagnostic agent to gain hospital access, followed by the therapeutic agent driving long-term revenue.

Of particular note is 225Ac-LNC1011, the first alpha-emitting radiopharmaceutical led by a domestic company in China to receive approval for clinical trials, with its Phase 1/2 trial launched in February 2026. Alpha emitters exhibit higher linear energy transfer and shorter tissue range compared to beta emitters, offering greater potential for eradicating micrometastases and drug-resistant lesions, and are regarded within the industry as the next-generation technological direction for radiopharmaceuticals. Lannacheng aims to leverage its first-mover advantage in this field to position itself for technological iterations expected in five years.

The third phase is a bet on horizontal expansion.

Lannacheng did not place all bets on a single target but instead strategically diversified across the FAP (fibroblast activation protein) target and dual-targeting technology to enhance the pipeline's risk resilience. 18F-LNC1005 (FAP-targeted) primarily focuses on gastric cancer, particularly addressing the blind spot of peritoneal metastasis that poses significant challenges for conventional CT/MRI imaging. Currently in Phase II clinical trials, it is expected to initiate Phase III clinical trials in Q4 2026.

18F-LNC1007 is the only FAP/αvβ3 dual-targeting radiopharmaceutical in China to have entered clinical development, targeting metastatic clear cell renal cell carcinoma. Phase 1/2 clinical data demonstrated an approximately 30% improvement in tumor detection rate compared with single-target agents. Currently, there are no commercially available FAP-targeted diagnostic radiopharmaceuticals worldwide; this forward-looking strategic move primarily aims to differentiate itself from products focused solely on the PSMA target.

Nuclear medicine: why the decades-old field is now booming?

For a long period, radiopharmaceuticals were positioned as ancillary consumables for molecular imaging—serving as supplementary examinations following CT and MRI scans—with a significantly limited value ceiling. As nuclear medicine has deepened its involvement in the precise treatment of tumors, related infrastructure has witnessed explosive growth.

According to data from the Chinese Medical Association, as of 2023, there were over 700 PET/CT scanners nationwide. The 14th Five-Year Plan projects the addition of 860 new PET/CT units across China, representing a 56% increase compared to the 551 units added during the 13th Five-Year Plan period. This signifies that nuclear medicine is no longer confined to a few dozen top-tier Grade A tertiary hospitals nationwide, but is instead expanding downward to leading provincial-level hospitals.

Only when equipment penetration reaches a sufficient level can we discuss the large-scale commercialization of compliant diagnostic radiopharmaceuticals. Without this infrastructure, even the most promising pipeline molecules will remain confined to the research stage.

Novartis' Pluvicto was approved in China, bringing theranostics from theoretical research to clinicians' hands. Previously, radiopharmaceuticals had PET imaging capabilities but lacked therapeutic efficacy; now, while treatment is available, PSMA-positive patients must first be identified through compliant screening.

The difference lies in the fact that diagnostic radiopharmaceuticals have evolved from advanced tools in nuclear medicine departments into mandatory prerequisites for therapeutic procedures, fundamentally altering the magnitude of overall demand.

Moreover, the technical challenges posed by the half-life of radiopharmaceuticals have also found solutions after years of development.

In short, radiopharmaceuticals with short half-lives (e.g., 18F, approximately 109 minutes) require a networked radiopharmacy distribution network, whereas those with long half-lives (e.g., 177Lu, 225Ac, ranging from 8 to 72 hours) can be managed through centralized production coupled with cold-chain distribution.

For a nuclear medicine biotech startup building from scratch, establishing such a distribution network and a stable supply chain would take no less than three to five years. In contrast, Lannacheng, backed by its parent company Dongcheng Pharmaceutical, enjoys the advantage of full-industry-chain synergy.

Dongcheng Pharmaceutical currently operates 31 radiopharmacy production centers, with an additional 8 under construction, enabling coverage of approximately 93.5% of the national demand for nuclear medicine. This has saved Lannacheng several years in channel development.

Dongcheng Pharmaceutical has also established a "one-pile, two-reactor" production platform for radioactive medical isotopes, making it one of the few enterprises in China qualified to produce and steadily supply radioisotopes to external clients. In addition, professional transportation companies with qualifications for transporting radioactive materials and a nationwide dedicated transport network have been established.

Coupled with Lannacheng's self-built cGMP-compliant production facility (currently in pilot production, with an annual capacity of approximately 7.674×10¹⁴ Bq), these factors point to a reality: the inflection point for the development of the radiopharmaceutical industry may lie not in R&D, but in logistics for short-half-life isotopes. The 109-minute physical half-life constraint requires companies to possess capabilities for stable synthesis, reliable distribution, and consistent quality control; otherwise, even approved products cannot achieve commercial viability.

Backed by Dongcheng Pharmaceutical, Lannacheng has become one of the few nuclear medicine companies in China to possess a complete industry chain—from diagnostic approval and radiopharmacy distribution channels to therapeutic follow-up—laying the foundation for its commercial breakthrough during this industry inflection point.

Lannacheng's recent filing unexpectedly coincided with the convergence of its own development stage and a critical juncture in the industry's evolution.

From an industry development perspective, the sector is currently at a critical juncture transitioning from diagnostics-dominated to therapy-driven growth. In 2024, therapeutic radiopharmaceuticals accounted for less than half of the global market, yet their growth rate far surpassed that of diagnostic agents; the two segments are projected to reach parity around 2030. In China, this transition is still in its early stages: diagnostic radiopharmaceuticals are beginning to gain widespread adoption, while therapeutic radiopharmaceuticals are just emerging.

In terms of corporate development, Lannacheng is precisely at a critical juncture where its diagnostic product is on the verge of approval, its therapeutic product has entered Phase II clinical trials, and its distribution channels are largely in place. Other competitors face similar situations. For instance, Grand Pharma's TLX591-CDx has had its New Drug Application (NDA) accepted, while its corresponding therapeutic product, TLX591, has also reached the mid-to-late stages of clinical development. Sinotau holds a leading position in diagnostics, but its therapeutic products remain in the early stages. Hengrui Medicine's radiopharmaceutical pipeline is also in the mid-development stage.

As a window into observing the industry, Lannacheng is one of the few companies in China to simultaneously deploy both diagnostic and therapeutic solutions on the same target, with its diagnostic products nearing market launch, its therapeutic products following an orderly development pipeline, and its operations backed by an established network of radiopharmacies.

This convergence of its own development and industry development at this particular stage holds special significance.

If the industry inflection point is delayed by two years, Lannacheng's cash reserves would still be sufficient, but the company would face risks of intensified competition and valuation pressure. However, if the inflection point materializes as expected within these two years, Lannacheng will emerge as an industry benchmark, successfully establishing a complete commercial closed-loop encompassing diagnostic approval, radiopharmacy channel development, and subsequent therapeutic follow-up.

Thus, theranostics will no longer be merely a concept, but a quantifiable business model. The entire radiopharmaceutical industry needs such a milestone event.