ImmuneOnco Biopharmaceuticals Launches IPO Backed by WuXi, RemeGen, ICON, and Harvest Global Investments After Raising $2B in Six Years

Morgan Stanley

International Financial Services Company

Since the mid-July IPOs of innovative companies such as Kelun-Biotech and Keep, there have been no new listings on the Main Board of the Hong Kong Stock Exchange (HKEX) for over a month. Today, Yiming Angke finally went public after filing its prospectus with the HKEX for the second time. After nearly 50 days, the Main Board of the HKEX has welcomed its first IPO company again, suggesting that the capital market may be starting to recover.

For this IPO, the joint sponsors for Yiming Angke are Morgan Stanley and China International Capital Corporation Limited (CICC). The company expects to issue 17.1472 million shares, with approximately 90% placed internationally and 10% offered publicly, along with an over-allotment option of approximately 15%. According to the prospectus, the offering price is HK$18.6 per share, with expected proceeds of nearly HK$319 million. Based on the offer price of HK$18.6 per share, Yiming Angke’s market capitalization upon listing is estimated at approximately HK$6.942 billion.

In addition to some routine data, one set of figures stands out prominently among the extensive data presented in the prospectus.According to the prospectus, for the periods ended April 30, 2021, 2022, and 2023, spanning less than two and a half years, Yiming Angke recorded net losses of RMB 732.9 million, RMB 402.9 million, and RMB 111.8 million, respectively, amounting to a total of RMB 1.2476 billion.

Why did this company, which has reported consecutive annual losses and is expected to require substantial ongoing R&D investment in the coming years, secure six rounds of financing between 2017 and 2022, gaining endorsement from leading institutions such as Sunshine Property & Casualty Insurance and Lilly Asia Ventures? In this IPO, Harvest Fund Management, WuXi Biologics, RemeGen, and ClinChoice participated as cornerstone investors, collectively subscribing for up to 70% of the offering and making a significant bet on Yiming Angke.

Both the prominence of its cornerstone investors and their subscription ratios are truly rare. What exactly is the appeal of Yiming Angke? Join VCBeat as we explore the answer.

Star Target CD47:

Niche Segments with a $10 Billion Market Potential

Yiming Angke is a biotechnology company dedicated to the development of tumor immunotherapies. Founded by Tian Wenzhi on June 18, 2015, and headquartered in Zhangjiang, Shanghai, it is one of the few biotechnology companies globally capable of systematically leveraging both the innate and adaptive immune systems.

Tian Wenzhi has over 30 years of academic and industrial experience in the field of oncology, with significant achievements in target validation for immunotherapy, molecular design, and drug development. As early as 2010, he recognized the immense potential of CD47 as an immunotherapeutic target and initiated drug research focused on this target.This occurred approximately 10 years before the CD47 target obtained clinical data validation.

In the field of immunotherapy, currently approved products primarily focus on the adaptive immune system, mainly targeting T-cell immune checkpoints such as PD-1/PD-L1, CTLA-4, and LAG-3.However, among patients with nearly all major cancer types, only approximately 10% to 25% benefit from PD-1/PD-L1 monotherapy.

Compared with the currently marketed immunotherapies, which suffer from low response rates in cancer indications and the inevitable issues of drug resistance and recurrence,Leveraging the innate and adaptive immune systems to develop products can overcome the limitations of current T cell-based immunotherapies and address the aforementioned clinical pain points.Among these, the CD47/SIRPα pathway has been clinically validated to play a pivotal role in regulating macrophage activity. It is one of the most attractive and innovative immune targets for cancer therapy in recent years and is poised to become the next revolutionary immune checkpoint following PD-1/PD-L1.

Regarding the CD47 target, ImmuneOnco has implemented a series of strategic initiatives. Its core product, IMM01, is a SIRPα-Fc fusion protein developed against CD47, while its key products—IMM0306, IMM2902, and IMM2520—are bispecific molecules also developed targeting CD47.

Currently, there are 59 CD47/SIRPα-targeted candidate drugs in clinical development worldwide, including 6 CD47-targeted fusion proteins, 19 CD47-targeted monoclonal antibodies, 24 CD47-targeted bispecific molecules, and 10 SIRPα-targeted monoclonal antibodies.

According to Frost & Sullivan data, the first CD47/SIRPα drug is expected to be launched in 2024. The market is projected to grow from USD 200 million in 2024 to USD 12.6 billion in 2030, representing a compound annual growth rate (CAGR) of 106.9%. Compared with the global market, China’s CD47/SIRPα targeted therapy market is expected to grow at a faster pace. The market size in China is projected to increase from USD 10 million in 2024 to USD 2.2 billion in 2030, with a CAGR of 159.1%.

Despite the intense competition in the CD47 space, with major pharmaceutical companies such as Bristol Myers Squibb (BMS), Gilead Sciences, AbbVie, and Boehringer Ingelheim actively investing in this area, no CD47-targeted therapy has yet received regulatory approval for market launch.

The $10 Billion Blue Ocean of CD47 with No Successful Commercialized Products: What Are the Development Challenges? There Are Four Key Points:

① Hematologic Toxicity Issues: Safety concerns represent the primary challenge for CD47-targeted therapies. In addition to tumor cells, CD47 is widely expressed on human red blood cells and platelets. Consequently, CD47/SIRPα blockers may also bind to normal blood cells, causing severe hematologic toxicities such as anemia, thrombocytopenia, and hemagglutination. These adverse events, in severe cases, can lead to the suspension or termination of clinical trials.

② Antigen Silencing Issue: Since CD47 is widely expressed on normal cells, CD47-targeting agents, particularly CD47 antibodies, may be rapidly depleted after administration, resulting in limited drug exposure in tumor tissues. The "antigen sink" effect necessitates higher doses to achieve the minimum effective concentration, but these elevated doses in turn lead to more severe hematologic toxicity.

③ Fc Isotype Selection Issue: Since CD47 antibodies inevitably bind to red blood cells, most of these antibodies rely on the IgG4 Fc region with weak effector function, requiring higher doses and trading therapeutic efficacy for safety.

④ T-cell Apoptosis Issues: CD47 is also expressed on T cells; upon binding to specific CD47 epitopes on T cells, certain CD47-targeting antibodies may induce T-cell apoptosis, leading to compromised efficacy, drug resistance, and severe adverse effects.

Pharmaceutical companies such as BMS, Gilead, and Surface Oncology have previously suspended or partially suspended relevant clinical trials due to the aforementioned safety concerns.

Amidst formidable barriers and the relentless failures of competing pharmaceutical companies,Yiming Angke designed IMM01, featuring a specialized CD47-binding domain and an IgG1 Fc region., and demonstrated its strength through clinical data and progress.Among the numerous pharmaceutical companies worldwide developing CD47-targeting molecules, ImmuneOnco is one of only two that have observed complete response (CR) with favorable tolerability and safety in monotherapy clinical trials (the other being Trillium Therapeutics, which was acquired by Pfizer in 2021).

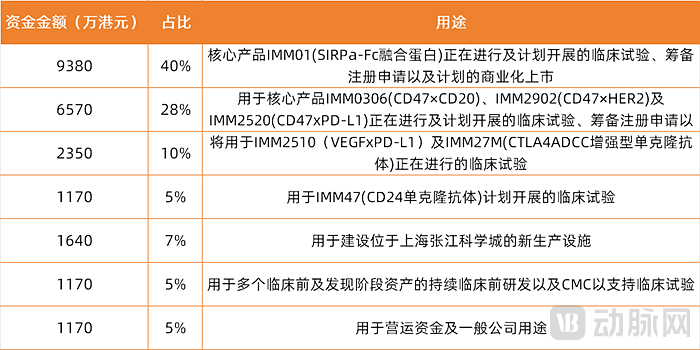

Following this IPO, Yiming Angke is expected toApproximately 68% of the funds raised were allocated to the product pipeline centered around the CD47 target.Only about 30% of the remaining funds raised will be allocated to other uses, such as pipeline development and production facility construction.

Use of Proceeds; Data Source: Prospectus

In less than two and a half years, a loss of 1.248 billion,

How Far Is It From the Multi-Billion Blue Ocean?

In addition to its strategic focus on CD47-targeted products, ImmuneOnco has also expanded its pipeline in the fields of innate and adaptive immunity to include innovative targets such as CD24 and CD70, as well as monoclonal antibodies against IL-8, NKG2A, and PSGL-1. The company boasts a total of 14 drug candidates, eight of which have entered clinical development.

ImmunOnco’s Pipeline Under Development, Source: Prospectus

CD24, as another important innate immune checkpoint, is widely expressed in many types of tumor cells, including breast cancer, non-small cell lung cancer, colorectal cancer, hepatocellular carcinoma, renal cell carcinoma, and ovarian cancer, and is regarded as a significant marker of poor prognosis for these cancers.

This targeted therapy currently represents an untapped blue ocean market, with no approved drugs available globally. Apart from one candidate drug that has received FDA approval and is currently in Phase I clinical trials, all other CD24-targeted candidate drugs worldwide have not yet entered the clinical stage.Yiming Angke’s fastest-moving CD24 pipeline candidate, IMM47, is currently in the IND-enabling stage. Its other pipeline candidate, which simultaneously targets CD24 and CD47, is the only reported investigational CD24-targeted bispecific molecule for cancer treatment worldwide, holding first-in-class potential.

In addition to these niche segments with significant blue-ocean potential, the global oncology immunotherapy market reached $50.2 billion in 2022, driven by the rising incidence of cancer, improved patient survival rates, prolonged treatment cycles, and advances in immunotherapy. According to Frost & Sullivan’s projections, the global oncology immunotherapy market is expected to reach $340.4 billion by 2035, accounting for more than 54% of the total global oncology market.

Simultaneously advancing such an extensive pipeline of immunotherapies naturally requires substantial capital support. Several investors, including Guoke Jiahe, Founder Life Sciences, Sunshine Property & Casualty Insurance, Licheng Asset Management, CCB Trust, Lilly Asia Ventures, Fuxian Growth, Rongchang Venture Capital, East Equity Investment, Zhouling Capital, Zhangke Lingyi, and the Greater Bay Area Fund, have all shown favor toward Yiming Angke.

It is reported that between February 2017 and January 2022, Yiming Angke completed a total of six financing rounds. The largest single round amounted to approximately RMB 610 million (calculated based on the central parity rate of the RMB against the USD in the interbank foreign exchange market on December 31, 2022, which was USD 1 = RMB 6.9646). The total amount raised exceeded RMB 1.4 billion.

Financing History, Data Source: Prospectus

Although Yiming Angke has secured substantial funding in recent years, the company incurred losses of RMB 1.2476 billion in the less than two-and-a-half-year period from 2021 to April 30, 2023.During this period, Yiming Angke’s revenues were RMB 5.067 million, RMB 538,000, and RMB 73,000, respectively. These revenues, primarily derived from licensing fees, cell line sales, and other testing services, are not considered representative.

Therefore, to smoothly advance the clinical development of its pipeline, Yiming Angke has reached a stage where an IPO is imperative.This trend is evident from the reduction in its R&D spending this year: according to the prospectus, Yiming Angke’s R&D expenses (including share-based payments) amounted to RMB 176 million, RMB 277.3 million, and RMB 75 million in 2021, 2022, and the four months ended April 30, 2023, respectively.

Logically, as the clinical pipeline advances and new candidates enter clinical trials, Yiming Angke’s R&D expenses should gradually increase; however, its R&D spending for the first four months of this year amounted to only RMB 75 million.According to the prospectus, IMM01, Yiming Angke’s most advanced core pipeline candidate, is currently in Phase II clinical trials and is expected to complete these trials in the first quarter of 2024. Given the typical R&D cycle for biopharmaceuticals, Yiming Angke still faces a considerable period before achieving commercialization.

To ensure smooth corporate operations and advance its pipeline, Yiming Angke is expected to engage in collaborations with third parties for the clinical development and commercialization of its drug candidates through licensing, co-commercialization, or other strategic partnerships, thereby securing enhanced resources and generating certain cash flows.

According to the prospectus, on January 18, 2021, Yiming Angke entered into a joint drug development cooperation agreement with 3SBio, under which the two parties will collaborate in mainland China to conduct clinical studies evaluating the combination therapy of ineptuzumab and IMM01 for the treatment of HER2-positive solid tumors.

Pursuant to the agreement, 3SBio is responsible for designing the clinical study protocol, coordinating with contract research organizations (CROs), and handling regulatory filings associated with each phase of the clinical studies. All costs incurred from conducting the clinical studies in China shall be borne by 3SBio, except for certain costs specified in the agreement that shall be borne by ImmuneOnco, including the costs of supplying IMM01, assigning its representatives to participate in clinical development and regulatory communications, and providing related technical support.

Based on this, it is evident that the innate and adaptive immunity sectors, where ImmuneOnco Biopharmaceuticals focuses its efforts, indeed hold a market potential worth hundreds of billions. Once its pipeline receives first-to-market approval, the company can swiftly capture this blue-ocean market. However, biopharmaceuticals is inherently a high-risk sector requiring substantial long-term investment; therefore, let us exercise sufficient patience and allow time to unfold as we anticipate the future of ImmuneOnco Biopharmaceuticals.