Sci-Tech Innovation Board IPO Thaw: Junlin Capital and OrbiMed-Backed Sports Medicine Leader Tianxing Medical Files Prospectus

Star

Provider of Comprehensive Clinical Solutions in Sports Medicine

On September 26, 2023, the listing application of Star Sports Medicine, a leading domestic sports medicine company, was accepted by the STAR Market.

For nearly three months, no companies have had their IPO applications accepted on the STAR Market. Coupled with the CSRC’s recent phased tightening of IPO policies, the entire healthcare IPO sector is currently in a state of contraction.

The acceptance of Star Medical’s application for listing on the STAR Market broke the ice in IPO acceptances on the board, boosting confidence in the healthcare industry.

Star, the domestic leader in the field of sports medicine, is applying for listing. The company has established a comprehensive sports medicine product platform encompassing implants, arthroscopic instruments, active equipment, and surgical tools, dedicated to providing patients with holistic clinical solutions for sports medicine.

Prior to its initial public offering (IPO), Star Sports Medicine Co., Ltd. secured investments from multiple institutional investors, including Legend Capital, OrbiMed, Yahui Investment, 3W Partners, and Longma Peak Venture Capital. Before the company’s listing, Xiamen Defu held a 10.6401% stake, Legend Capital held 15%, OrbiMed held 9.2797%, and Best Alive held 5.3938%.

Star Medical plans to raise RMB 1.093 billion, of which RMB 440 million will be allocated to the Suzhou Smart Factory Project, RMB 219 million to the Product R&D Project, RMB 133 million to the Marketing Network Project, and RMB 300 million to supplement working capital.

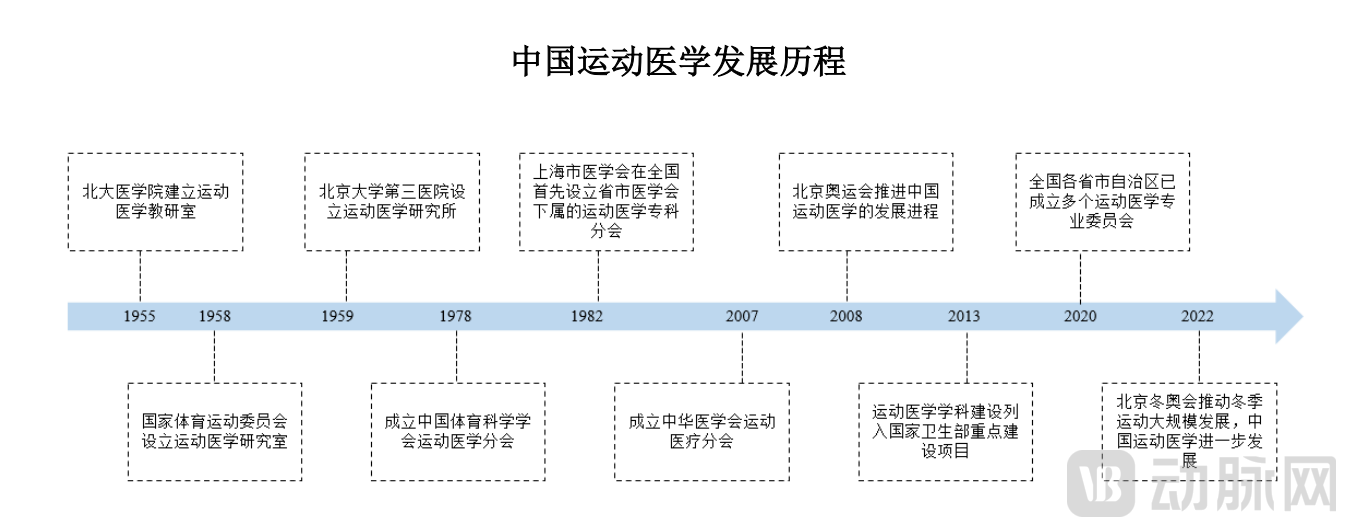

The sports medicine sector in which Star operates is one of the four major subfields of orthopedics and also the fastest-growing segment within the field.

The goal of sports medicine is to achieve maximal functional restoration with minimal trauma. Sports medicine products are primarily used to treat soft tissue injuries between bones, such as those involving the Achilles tendon, ligaments, meniscus, tendons, and cartilage. These include meniscal and cruciate ligament injuries, tendinopathy, skeletal muscle injuries, cartilage and osteochondral injuries, joint instability, and glenoid labrum injuries.

Sports medicine in China started relatively late. A simple example is that many well-known athletes often had to go abroad for treatment after sports injuries. With the state's strong promotion of sports medicine construction and the sports boom brought by major sporting events, domestic sports medicine has developed rapidly.

According to Frost & Sullivan, the market size of China’s sports medicine implant industry was approximately RMB 2.47 billion in 2018, growing to RMB 3.91 billion in 2022, representing a compound annual growth rate (CAGR) of approximately 12.1% during this period. The market size is projected to continue its growth trajectory, reaching RMB 8.93 billion by 2030, with an expected CAGR of approximately 10.9% from 2022 to 2030.

From the perspective of market share, imported products account for a relatively high proportion of the Chinese sports medicine market. According to data from Frost & Sullivan, international brands represented by Smith & Nephew, DePuy Synthes, Arthrex, and ConMed have long held over 80% of the domestic market share. The technical barriers for sports medicine implants are relatively high, resulting in a low rate of localization for these products.

Domestic companies in China involved in the field of sports medicine are still in their early stages. The main participants include specialized sports medicine companies such as Star Sports Medicine, Ruijian Medical, and Deyidamei Medical, as well as orthopedic medical device companies that have established product portfolios or business plans in the sports medicine sector, such as Chunli Medical, Kellytai, Weigao Orthopaedics, and Double Medical.

How Does Star Break Through the Import-Dominated Market Landscape?

Star Sports Medicine Co., Ltd. was established in 2017 with capital contributions from Nie Wei, Dong Wenxing, and Chen Hao. At that time, Dong Wenxing, Nie Hongxin, and Chen Hao recognized the market potential in the field of sports medicine and planned to co-found a company. Leveraging Dong Wenxing’s technical expertise and professional background in absorbable materials, Nie Hongxin’s investment and industrial experience in the medical device sector and other investment areas, and the production experience in sports medicine-related products held by Guangzhou Tianying, which is controlled by Chen Hao’s family, the three parties founded Star Sports Medicine Co., Ltd.

The founding team of Star has extensive experience in the orthopedics field in China.Nie Hongxin previously served as Managing Director of Kanghui Medical and was an early investor in Star Medical. Kanghui was the first Chinese orthopedic company to list on the New York Stock Exchange and was later acquired by Medtronic. All equity interests held by Nie were held on behalf of Nie Hongxin.

Founder Dong Wenxing has accumulated specialized technical expertise and a professional background in the field of absorbable materials. He holds a Ph.D. in Advanced Manufacturing from Harbin Institute of Technology and serves as the Chairman of Star Sports Medicine Co., Ltd. From August 2010 to September 2015, Mr. Dong served as a reviewer at the Center for Medical Device Technical Evaluation under the China Food and Drug Administration. From September 2015 to May 2017, he served as Deputy General Manager of Changchun Shengboma. Prior to the IPO, Mr. Dong directly held 33.1449% of the company’s equity, making him the largest shareholder. Through Tianjin Yunkang, Tianjin Puhe, and Tianjin Jikang, he effectively controlled the voting rights of 41.4739% of the company’s shares, serving as the controlling shareholder and actual controller.

Star has long been committed to independent research and development and technological innovation, establishing two core technology platforms: the Sports Medicine Implant Development Platform and the Imaging and Powered Energy Platform. In the field of implants, the company has developed technologies for the preparation of functionally graded bioabsorbable materials, precision injection molding of ultra-high-temperature polymer materials, and the manufacturing of heavy-load woven implants. In the area of active devices and consumables, Star has developed 4K imaging technology, intelligent control shaver power technology, and low-temperature plasma ablation technology.

The prospectus shows that Star Medical’s revenues in 2020, 2021, and 2022 were RMB 26.407 million, RMB 73.013 million, and RMB 150 million, respectively; net profits were -RMB 50.81 million, -RMB 110 million, and RMB 40.34 million, respectively; and net profits excluding non-recurring items were -RMB 17.6496 million, RMB 4.55 million, and RMB 38.81 million, respectively.

According to data disclosed in the prospectus, Star’s market share in China’s sports medicine sector was approximately 3% in 2022, indicating substantial potential for further market expansion. Volume-based procurement is expected to accelerate this process.

On September 14, 2023, the Joint Procurement Office for National Organization of High-Value Medical Consumables issued the “Announcement on Centralized Volume-Based Procurement of Artificial Crystal and Sports Medicine Medical Consumables Organized by the State (No. 1),” launching national-level volume-based procurement bidding for sports medicine medical consumables. Star’s main products in sports medicine implants were included in the scope of national centralized procurement.

As the state further advances volume-based procurement (VBP) policies for sports medicine consumables, Star Sports Medicine believes that VBP will pose certain challenges to the sports medicine industry in the short term. Due to its characteristic of exchanging price for volume, product prices in the sports medicine sector are expected to decline to some extent following the implementation of VBP. On one hand, the price reduction is likely to rapidly increase the clinical penetration rate of sports medicine-related products that were previously limited by their high costs. On the other hand, VBP imposes higher requirements on companies in the sports medicine industry regarding production costs, product coverage, and manufacturing capacity.

Following the volume-based procurement (VBP) of artificial joints, the market share of leading domestic manufacturers has increased; similarly, the market share of leading domestic companies in the sports medicine sector is expected to rise after the implementation of VBP.

As the 19th Asian Games are held in Hangzhou, sports medicine is presented with another development opportunity. We look forward to seeing outstanding achievements from China in the sports medicine industry.