Yilian Bio Strikes $1B+ HER3 ADC Deal with BioNTech, Accelerating Global Expansion

BioNTech

Developer of Novel Biologics

MediLink

Antibody-Drug Conjugates Developer

On October 12, 2023, Suzhou MediLink announced a collaboration agreement with BioNTech, granting BioNTech the global rights to its novel HER3 (Human Epidermal Growth Factor Receptor 3) antibody-drug conjugate (ADC), YL202, outside of Greater China. The transaction includes an upfront payment of $70 million, plus additional development, regulatory, and commercial milestone payments, with a potential total value exceeding $1 billion.

(Chart by VBInsight, compiled from public data)

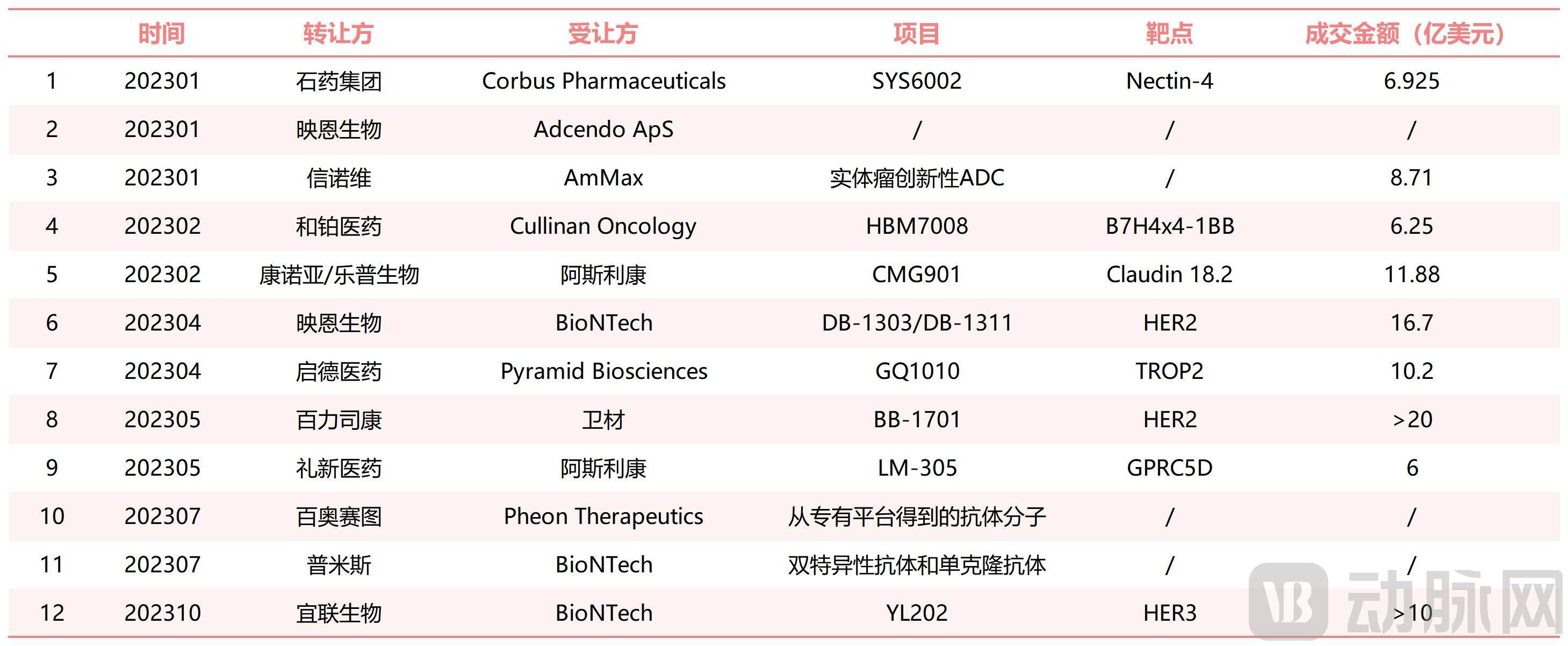

According to incomplete statistics, this is already the 12th overseas licensing deal in the ADC sector in 2023.

According to data from Lepu Biopharma’s prospectus, the global market size for antibody-drug conjugate (ADC) therapies is projected to reach $10.4 billion in 2024 and $20.7 billion in 2030. The market is experiencing robust growth, with a compound annual growth rate (CAGR) of 30.6% from 2019 to 2024 and a CAGR of 12.0% from 2024 to 2030.

The domestic Chinese ADC market did not emerge until 2020. Although it started late, it coincided with the golden age of ADC drug development, prompting innovative pharmaceutical companies worldwide to invest and enter the field. This has also created a favorable environment for Chinese biotech firms to expand their pipelines overseas.

On the flip side of license-in deals, overseas companies are increasingly betting on the Chinese pharmaceutical market.

Chinese biotech companies going global, undoubtedly, generally tend to target the European and American pharmaceutical markets.

Notably, the United States holds a globally leading position in the biopharmaceutical industry. As the global hub for biopharmaceutical development, the U.S. has established five major biopharmaceutical clusters, including Boston, San Diego, and the Research Triangle Park in North Carolina, driving comprehensive development and innovation across specialized therapeutic areas such as oncology, immunology, cardiovascular diseases, anti-infectives, vaccines, and neuroscience.

According to data from Frost & Sullivan, as of June 10, 2022, using market capitalization thresholds of $50 billion and $10 billion, there were 11 pharmaceutical companies with a market cap exceeding $50 billion. These companies accounted for only 2.6% of the total number of companies in the U.S. pharmaceutical sector, but their combined market capitalization represented 84.9% of the sector’s total value. There were eight companies with market caps between $10 billion and $50 billion, accounting for approximately 7.1% of the total market capitalization. The top 39 companies with market caps above $10 billion represented just 4.5% of the total number of companies in the U.S. pharmaceutical sector, yet their aggregate market capitalization reached $2.3 trillion, comprising 92.1% of the sector’s total market value.

MediLink has targeted the global market since its inception, with its product pipeline geared toward simultaneous regulatory filings in both China and the United States. As an innovative technology platform company, MediLink possesses the potential to leverage diverse targets to develop a broader portfolio of products; however, as a startup, it faces constraints in both focus and resources. Therefore, through external collaborations, the company aims to progressively refine and validate its proprietary technology platform while jointly generating robust product data to explore additional opportunities.

“Partner selection strategies vary depending on the specific target; however, the primary consideration remains whether the partner is willing to commit the necessary capabilities and resources to drive the product through to commercialization while maximizing the company’s interests. Additionally, it is essential to seek partners with complementary strengths,” said Xiao Liang, Co-founder of MediLink, in an interview with VCBeat New Medicine.

By analyzing the overseas expansion of other domestic biotech companies, it is not difficult to find that,These companies that have successfully expanded overseas not only rely on robust underlying technologies to drive their projects but also possess strong business development (BD) resources and strategic plans.

For example, when engaging with partners, most foreign pharmaceutical companies possess mature industrialization experience and comprehensive resources deeply embedded in local pharmaceutical markets; domestic enterprises often prioritize these resources when entering into collaborations.

Secondly, establishing a strong partnership requires maintaining close and comprehensive communication before formalizing the agreement. Relationships and mutual understanding are built through sustained, frequent interactions that encompass a deep grasp of product technology, innovation logic, and clinical data. Such exchanges also subtly foster perception and recognition of the company’s overall capabilities. Importantly, Chinese enterprises should proactively engage in external outreach, actively participate in industry events, and conduct face-to-face dialogues to enhance industry stakeholders’ and partners’ understanding of the company itself.

MediLink’s current collaboration with BioNTech aligns with the aforementioned logic.

Many may have come to know BioNTech due to the COVID-19 outbreak over the past three years, which propelled it to stardom with its mRNA vaccines for infectious diseases. However, BioNTech’s accumulated strengths in the European and American markets extend far beyond this, encompassing industrial resources, technological innovation, and product portfolio.

Since its establishment in 2008, BioNTech has conducted extensive research in the field of cancer. Its personalized mRNA cancer vaccine entered clinical trials in 2014, and a paper published in Nature in 2017 highlighted the potential of its mRNA vaccines to reduce recurrence in melanoma patients.

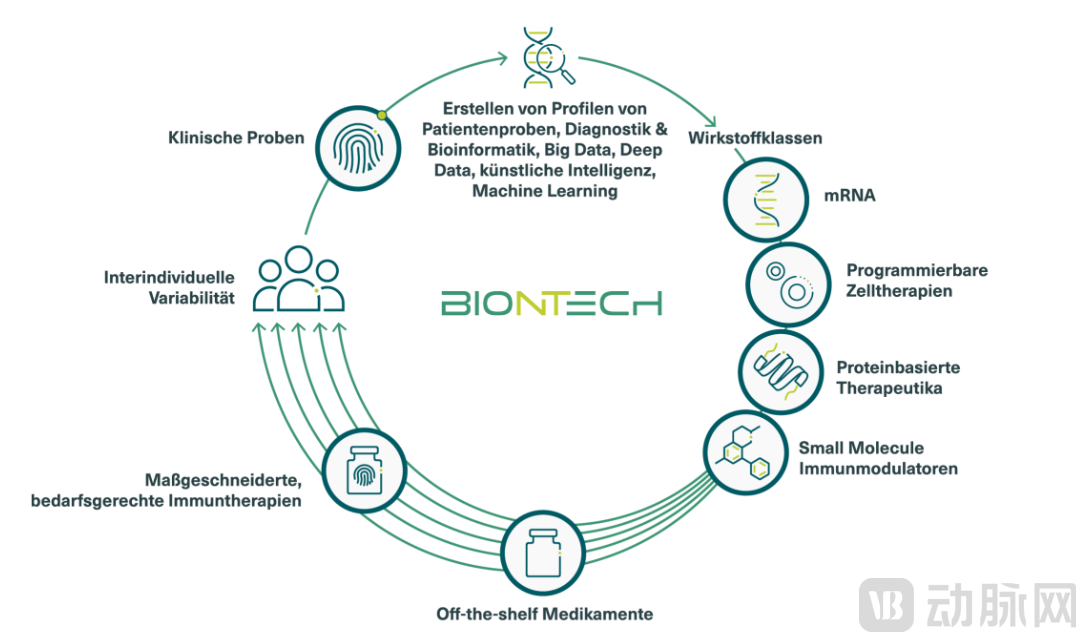

BioNTech has adopted a multi-platform innovation strategy, with platform technologies encompassing mRNA vaccines, cell and gene therapies, targeted antibodies, small-molecule immunomodulators, ribologicals, and next-generation immunomodulatory therapies. Among these, cancer treatment is a key strategic focus for future development. Furthermore, there is potential to enhance therapeutic efficacy through combination regimens across different modalities.

(BioNTech Cancer Treatment Strategy)

(BioNTech Cancer Treatment Strategy)

This is not the first time BioNTech has acquired ADC pipelines from China. In April this year, BioNTech entered into an exclusive license and collaboration agreement with Duality Biologics for DB-1303 and DB-1311. BNT323 (DB-1303), which has received Fast Track designation, announced in September that its Phase 3 clinical trial was imminent. As part of the DB-1311 agreement, Duality Biologics retains the option to exercise co-development and co-commercialization rights for the U.S. market in the future.

On August 7, BioNTech and DualityBiologics entered into an expanded collaboration agreement to jointly advance the development, manufacturing, and commercialization of a third ADC candidate, DB-1305, on a global basis (excluding mainland China, the Hong Kong Special Administrative Region of China, and the Macao Special Administrative Region of China).

Xiao Liang stated, “What we value most is BioNTech’s accumulated resources in the field of oncology therapeutics; their biological expertise in novel targets also aligns closely with our perspective. Furthermore, BioNTech has amassed sufficient capital from its COVID-19 efforts, enabling it to help partners extensively expand their clinical pipelines in the European and American markets.”

In the biopharmaceutical industry, a niche sector that attracts little interest is bound to have certain issues; likewise, if everyone rushes in, caution is warranted.

As a hot field of development in recent years, the drug research technology of ADC can be traced back more than 100 years. According to the report released by PatSnap, it is expected that global ADC drug innovation has gradually entered a golden period of development. ADC drugs have become a key focus for global innovative pharmaceutical companies, and may usher in a new peak in the next 3-5 years.

In terms of market size, according to predictions by Nature, the total sales of the 10 ADC products launched before 2020 will exceed $16.4 billion by 2026. The domestic ADC market in China was initiated in 2020 and is expected to reach RMB 7.4 billion and RMB 29.2 billion in 2024 and 2030, respectively, with a compound annual growth rate (CAGR) of 25.8% from 2024 to 2030.

However, the development of antibody-drug conjugate (ADC) drugs in China started relatively late, leading to a concentration of research and development efforts on similar targets and indications. In terms of R&D targets, competition is currently most intense for HER2-targeted ADCs, while drug development targeting c-Met, EGFR, Trop-2, CD20, BCMA, and other targets is gradually gaining momentum. Regarding indications, consistent with international trends, most domestic ADC companies are primarily focused on oncology drug development.

Regarding the topic of “involution” in the ADC space, many current articles draw comparisons between ADCs and PD-1 inhibitors to argue that the ADC field is highly saturated, making differentiation extremely difficult and suggesting that its development has reached a dead end. However, this notion of “involution” merely scratches the surface.From the perspective of targets alone, ADC products appear to be in a highly competitive landscape. However, unlike pure antibody drugs, ADCs do not exert their therapeutic effect by killing tumor cells through modulating the intrinsic function of the target. The target serves merely as a docking site, while the cytotoxic payload is the actual agent responsible for the therapeutic effect.

Furthermore, the therapeutic window of current ADC drugs remains relatively narrow, falling far short of the safety profile expected of an ideal “magic bullet,” thus leaving substantial room for improvement. On the other hand, various aspects of ADCs can be optimized and enhanced, including the specific binding affinity of antibodies, the diversity of toxin mechanisms of action, and the site-specific cleavage and release by linkers. Additionally, the application of ADCs in non-oncological diseases represents a new frontier yet to be fully explored.

In this blue ocean, MediLink has adopted a distinct strategy by selecting emerging targets such as B7-H3, HER3, and DLL3 for its pipeline development.

In response, Xiao Liang explained, “As founders, we had previously developed pipelines targeting popular antigens such as HER2, so it would have been easier for us to get started. However, MediLink did not want to create business-level conflicts with our former employers. The ADC field offers ample new opportunities worth exploring, rather than digging for innovative technologies in established areas.”

As part of its global expansion, MediLink has licensed to BioNTech an ADC product that is a next-generation antibody-drug conjugate targeting human epidermal growth factor receptor 3 (HER3).

HER3 is highly expressed in multiple cancer types, such as non-small cell lung cancer and breast cancer, and is closely associated with tumor metastasis and disease progression. Furthermore, HER3 expression is further upregulated following first-line drug therapy, making it a highly promising therapeutic target for cancer. Currently, no HER3-targeted therapies have been approved globally, indicating significant market potential.

By leveraging MediLink’s TMALIN® (Tumor Microenvironment Activable LINker-payload) technology, the project has demonstrated superior efficacy and safety across various preclinical tumor models, with preliminary clinical data further supporting its proof of concept.

Compared to its HER3 ADC pipeline, which holds significant market potential, MediLink’s novel antibody-drug conjugate platform technology, TMALIN®, is the true source of its continuous innovation.

MediLink possesses independent intellectual property rights. Based on this platform, MediLink’s technology enables a dual cleavage mechanism both extracellularly and intracellularly by leveraging the tumor microenvironment and traditional lysosomal pathways. It features high water solubility, high homogeneity, high stability both in vitro and in vivo, as well as tumor tissue enrichment properties. This technology has demonstrated a wider therapeutic window compared to existing ADC technologies in multiple in vivo efficacy models and large-animal toxicology studies. Currently, several ADC candidates from MediLink based on this platform have entered clinical trials.

As mentioned at the beginning, there have been 12 overseas licensing deals in the ADC sector this year alone. It is conceivable that the total number of overseas transactions across China’s broader biopharmaceutical industry is certainly even higher.

In recent years, not only have Chinese biotech companies been eager to “go global,” but large overseas enterprises have also been keen to enter the Chinese market. As an emerging fertile ground for biopharmaceuticals, China is experiencing rapid growth in market demand.

According to Frost & Sullivan, the market size of biologics in China was RMB 312.0 billion in 2019 and is expected to reach RMB 712.5 billion in 2024 and RMB 1,302.9 billion in 2030, representing a compound annual growth rate (CAGR) of 18.0% from 2019 to 2024 and 10.6% from 2024 to 2030. During the same periods, the global biologics market is projected to grow at CAGRs of 9.8% and 9.0%, respectively.

The rapid growth of China’s biopharmaceutical market cannot be underestimated. In tandem, source innovation within the Chinese pharmaceutical industry is also surging. Overseas markets have recognized this potential and are actively extending olive branches to domestic enterprises.

Major global pharmaceutical giants such as Eisai, AstraZeneca, Roche, GSK, Sanofi, and Merck & Co. have been increasingly active in the Chinese market in recent years. Taking BioNTech, the star company discussed today, as an example, it has entered into licensing and collaboration agreements for more than seven projects with Chinese enterprises—including MediLink, Duality Biologics, OncoC4, and Promab—within just ten months this year.

From a different perspective, when domestic companies discuss dual filing in China and the United States and the “in China for Global” strategy, and when we will inevitably choose to go global after reaching a certain stage of development sooner or later.

Do overseas companies also regard entering the Chinese pharmaceutical market as the gold standard for their global expansion strategies?