Amid a 40% Decline in Newborns Over Five Years, Is the Assisted Reproductive Technology (ART) Business Still Viable?

JINXIN FERTILITY

Assisted Reproductive Technology Service Provider

Berry Genomics

High-throughput Gene Sequencing Technology Developer

Recently, the National Health Commission released the Statistical Bulletin on the Development of China's Health and Health Undertakings in 2022, with data showing thatIn 2022, China's live births totaled 9.56 million, marking the first time since 1950 that the figure fell below 10 million; the natural population growth rate was -0.60‰, also representing the first negative growth in nearly 61 years.。

However, this is not the end. In 2023, the number of newborns may hit a new low. This August, Qiao Jie, an academician of the Chinese Academy of Engineering and Dean of Peking University Health Science Center, stated at the “Forum on Pharmaceutical Innovation and Frontier Technologies” thatChina’s newborn population has declined by approximately 40% over the past five years, with the number of births in 2023 projected to be between 7 million and slightly over 8 million.。

Although the data remain contentious, this projection is not without merit. It is reported that Beijing Obstetrics and Gynecology Hospital, which previously ranked first in delivery volume in Beijing, saw its annual number of deliveries drop rapidly from 19,000 to 10,000—a nearly 50% decline—even after being included on the list of designated hospitals for assisted reproductive technology. Meanwhile, county-level maternal and child health hospitals, once high-volume delivery centers, are now facing financial deficits, with many having been absorbed by local county people’s hospitals and reduced to mere departments within them. Furthermore, some primary-care hospitals with relatively weaker technical capabilities have even abolished their obstetrics departments entirely, retaining only gynecology services.

Various cases and data indicate that the number of newborns in China is plummeting, and related industries are being affected to varying degrees. For instance, the wave of closures among private kindergartens is currently intensifying. According to data from the Ministry of Education,In 2022, the number of kindergartens in China decreased by 5,610., marking the first decline since 2007. In addition, in the maternal and infant industry, according to the "2022 China Maternal and Infant Physical Store Consumer Data Analysis Report," the average monthly sales per maternal and infant store in 2022 decreased by 8.1% compared to the same period in 2021, while the average monthly number of orders and the average monthly sales volume per store declined year-on-year by 15.6% and 12.8%, respectively.

Of course, the assisted reproductive technology (ART) industry, which has experienced significant volatility in recent years, has also been affected to some extent. However, at this stage, the industry as a whole is not yet in a position to address the current reality of low fertility rates.

Which Is More Important: Low Fertility Rates or Low Market Penetration?

Although the current decline in fertility rate is an objective fact,The Assisted Reproductive Technology Industry Is Not Short of “Business”。

On the one hand, according to the preliminary analysis results of the latest "13th Five-Year Plan" survey data from 2020,The prevalence of infertility in China has risen rapidly to approximately 18%., and according to projections by the National Medical Products Administration, China's infertility rate is expected to rise to 18.2% in 2023; if this figure is used for estimation,The number of infertility patients in China has exceeded 50 million.。

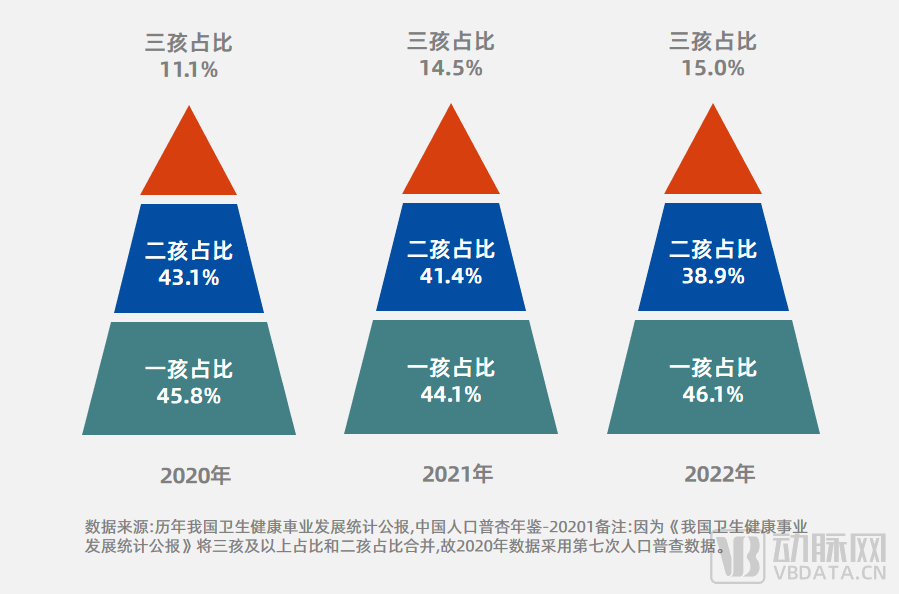

Figure 1. Proportion of First, Second, and Third Children, 2020–2022 (Data source: as shown in the figure; chart by VCBeat)

Figure 1. Proportion of First, Second, and Third Children, 2020–2022 (Data source: as shown in the figure; chart by VCBeat)

From another perspective, considering maternal age, the proportion of third-child births in China has risen rapidly since the introduction of the “three-child policy” in 2021, increasing from 11.1% in 2020 to 15% in 2022. The group with the highest fertility rate for three or more children is primarily concentrated among women aged 30–34. Due to declining physiological function in this age group, there is a significant demand for assisted reproductive technologies.

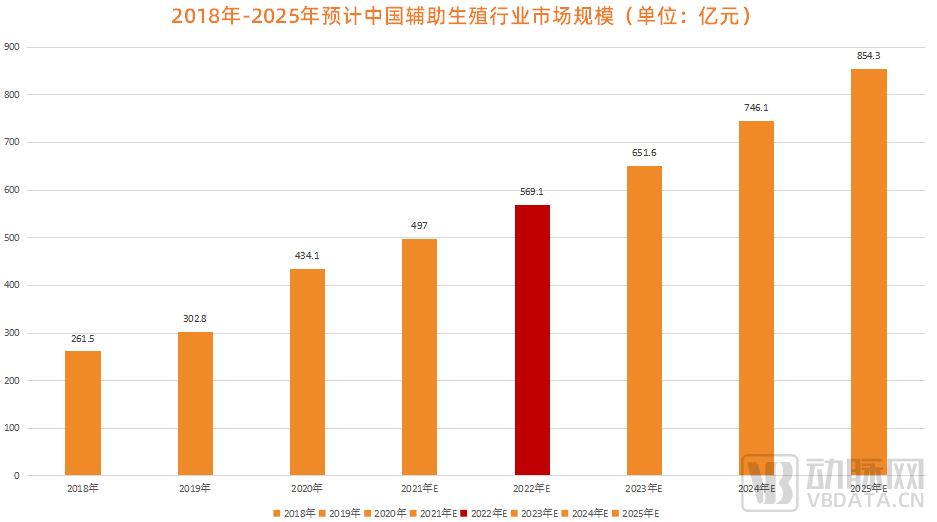

Figure 2. Estimated Market Size of China’s Assisted Reproductive Technology Industry, 2018–2025 (Data Source: LeadLeo Research Institute)

Therefore, the market demand for assisted reproductive technology is enormous, and it is precisely because of this thatChina's Assisted Reproductive Technology Market Has Achieved a Compound Annual Growth Rate of 14.5% Over the Past Five Years, but when viewed from the perspective of the entire healthcare industry, the market size of assisted reproductive technology (ART) in China is currently not substantial. According to forecasts by 36Kr Research,In 2022, the market size of China's assisted reproductive technology industry reached RMB 56.91 billion., still some distance away from the hundred-billion-yuan market,The key variable here lies in the industry’s currently low market penetration rate.。

According to Frost & Sullivan data,China's assisted reproductive technology market penetration rate stands at only 7%., which is a significant gap compared to the nearly 30% penetration rate in the United States. In this regard, a head of an assisted reproductive technology (ART) institution revealed to VCBeat, “Among individuals with infertility, only about 20% ultimately choose assisted reproductive technology.”

So, what is the reason?

This needs to be viewed from multiple perspectives.First, some patients are currently not eligible for childbearing., such as direct physiological causes, including severe genetic disorders, serious somatic diseases, and psychiatric or psychological conditions that contraindicate childbearing in some patients. However, these can all be attributed to technical limitations, namely that current assisted reproductive technologies cannot enable all women to achieve normal fertility.

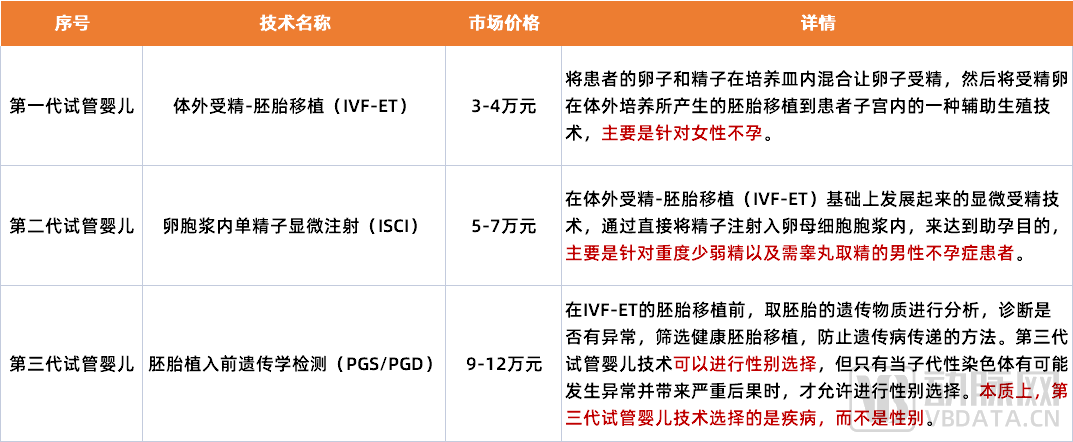

Secondly, the balance between success rate and priceCurrently, the success rate of assisted reproductive technology (ART) in China is approximately 40% to 60%, whereas in major global ART markets such as the United States and Thailand, it has reached 70% to 80%. Furthermore, domestic pricing does not offer a significant advantage. According to the latest market data, taking third-generation in vitro fertilization (IVF) as an example, the cost per treatment cycle in China ranges from RMB 90,000 to 120,000, while in Thailand it is approximately RMB 80,000 to 100,000, indicating a minimal difference.

Figure 3. Details and Market Pricing of Third-Generation IVF Technology

Figure 3. Details and Market Pricing of Third-Generation IVF Technology

However, considering the success rates, a portion of Chinese patients still choose to undergo in vitro fertilization (IVF) in Thailand. It is reported that Thailand performs over 30,000 IVF cycles annually, with Chinese clients accounting for 80% of this volume.

In response, the head of an assisted reproductive technology (ART) device company explained the reasons to VCBeat: “Assisted reproduction is, after all, a medical procedure; therefore, safety and success rates must be prioritized. As a pioneer in IVF in Asia, Thailand has developed highly refined and mature related technologies and services, with current success rates maintaining at approximately 75%. Coupled with relatively straightforward procedures and geographical proximity to China, many people are naturally willing to pay for these services. In fact, looking across the entire Southeast Asian market, Malaysia, not just Thailand, is also a top choice for many Chinese nationals seeking IVF treatment.”

Of course, there are many reasons for this,For instance, there is still a significant supply-demand gap in China's assisted reproductive technology market.. It is reported that although the penetration rate of China's assisted reproductive technology (ART) market remains low at present, appointments at some leading fertility institutions are still fully booked. This is primarily due to the difficulty in obtaining relevant licenses.Currently, fewer than 100 institutions in China are licensed to provide PGD/PGS (third-generation IVF) services., with public hospitals dominating the sector; reproductive institutions affiliated with private hospitals or funded by private capital account for less than 10%.

Finally, there are still hidden corners in China's assisted reproductive technology market that remain uncovered.A leading obstetrician in Shanghai told VCBeat, “In fact, some patients’ reproductive needs go beyond simply having a child; they may also wish to select the baby’s sex or even hope for twins or boy-girl twins. In addition to married couples, a significant number of same-sex partners or individuals opt for surrogacy. However, these practices are explicitly prohibited by Chinese law, although they are legal in certain overseas markets.”

Therefore, for the entire assisted reproductive technology (ART) industry, focusing on fertility rates at this stage is of limited significance, as these are beyond the industry’s control. What the industry can currently influence is how to increase market penetration by offering more cost-effective services.

Volatility and Swings: How Are the Primary and Secondary Markets for Assisted Reproductive Technology Performing?

The release of the “Three-Child Policy” in 2021 quickly propelled assisted reproductive technology into the spotlight of the capital market.

According to VCBeat, on the day the policy was released, assisted reproduction concept stocks in the secondary market rose collectively. By the close of trading, the A-share assisted reproduction sector index increased by 2.32%. In the Hong Kong stock market, BASECARE surged by 15.1%, while JINXIN FERTILITY jumped by 17.51%.

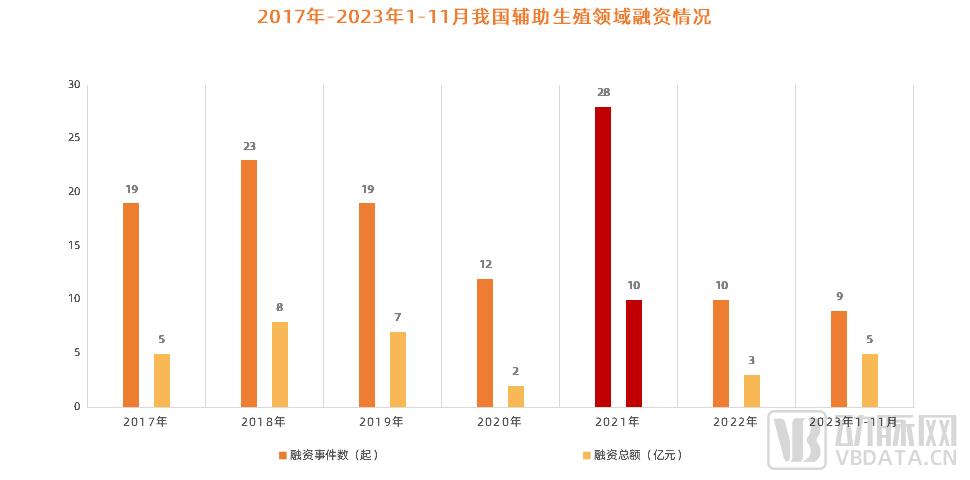

As time passed, the heat in the secondary market gradually spilled over into the primary market. According to incomplete statistics from the VCBeat Orange Database,In 2021, China's assisted reproductive technology sector completed a total of 28 financing rounds, with the total amount exceeding RMB 1 billion., with nearly 50 top-tier institutions, including Sequoia Capital, IDG Capital, CICC Capital, and Shenzhen High-Tech Investment Group, actively investing.

Figure 4. Investment and Financing in China’s Assisted Reproductive Technology Industry, January–November 2017–2023 (Data source: VCBeat)

Figure 4. Investment and Financing in China’s Assisted Reproductive Technology Industry, January–November 2017–2023 (Data source: VCBeat)

However, the buzz did not last. As 2022 began, assisted reproductive technology was suddenly forgotten by the industry. According to incomplete statistics from VCBeat, in the nearly two-year period from January 1, 2022, to November 1, 2023,China’s Assisted Reproductive Technology Industry Saw Only 19 Financing Deals in the Primary Market, with a Significant Decline in Overall Funding Volume。

This is certainly attributable to the objective factor of a broader cooling in the healthcare market, but more importantly, it stems from the inherent limitations within the assisted reproductive technology (ART) industry itself. For instance, as mentioned earlier, market penetration remains low. In addition, relevant laws and regulations are still imperfect. It is reported that neither the current Biosecurity Law nor the Office of Human Genetic Resources Administration...Assisted reproductive technology is a relatively sensitive clinical service under laws and regulations, and many standardized protocols have not yet been fully established.。

Another issue is the insufficient innovation capability across the entire assisted reproductive technology (ART) market. It is reported that domestically produced devices hold a significant advantage over imported ones in low-value-added, low-technical-content products such as ART oocyte retrieval needles/sperm aspiration needles and ART micro-tools, butIn the high-priced, technically barriered market of culture media for assisted reproductive technology (ART), imports still dominate, accounting for as much as 81% of the market share.。

Figure 5. Representative Enterprises with Innovative Technologies in China’s Assisted Reproductive Technology Sector (Data Source: VCBeat)

In response to this, an investor focusing on the field of assisted reproduction told VCBeat, “Over the past two years, our attention to assisted reproduction has been relatively low. This is partly because there are still many uncertainties in the industry, making it difficult to identify market patterns at this stage; and partly because assisted reproduction is actually a niche sector with extremely high entry barriers but limited profitability. Many institutions are currently ‘operating at a loss just to gain visibility.’”Coupled with the downturn in the broader capital markets, we lacked the patience and financial resilience to wait for the industry’s explosive growth.。”

If this is the case in the primary market, what about the secondary market?

As of now, there are nearly 50 listed companies associated with the concept of assisted reproductive technology (ART), with JINXIN FERTILITY being a typical representative.As China’s first listed assisted reproductive technology (ART) company, JINXIN FERTILITY saw its market capitalization exceed HK$24 billion upon its 2019 Hong Kong Stock Exchange listing, but it has since declined to around HK$10 billion.。

Even so, JINXIN FERTILITY remains one of the most profitable listed companies in the assisted reproductive technology (ART) industry. According to its interim report, JINXIN FERTILITY recorded revenue of RMB 1.334 billion in the first half of 2023, a year-on-year increase of 17.2%; net profit reached RMB 224 million, up 19.3% year on year; and adjusted net profit amounted to RMB 255 million. In its interim report, JINXIN FERTILITY attributed this business growth primarily to the rapid recovery of overseas patient demand following the lifting of pandemic-related restrictions. Notably, the company’s U.S. operations saw a 21% year-on-year increase in revenue and more than a 200% year-on-year surge in net profit during the first half of the year.

Unlike JINXIN FERTILITY,Most Listed Assisted Reproductive Technology Companies Remain Trapped in a Profitability Vicious Cycle. On October 28, A-share listed companiesBerry GenomicsReleased the performance report for the first three quarters of 2023, with a net loss of RMB 135 million during the period, representing a year-on-year increase in losses of 733.37%.

In addition, there areBASECARE, as the “first stock in assisted reproductive genetic testing,” it achieved double-digit growth in the first half of this year, with total revenue reaching RMB 85.546 million, a year-on-year increase of 24.8%. However, it has not yet turned a profit. In the first half of this year, the loss from continuing operations amounted to RMB 62.493 million.

While losses vary in their specifics, the core issue remains the imbalance between substantial R&D investment and the contraction of service volume in lower-tier markets. In its 2022 annual report, Berry Genomics stated that the change in company performance was primarily due to a decline in revenue caused by regional fluctuations in orders for its basic scientific research business.

Perhaps it is precisely for this reason that since BASECARE’s listing on the Hong Kong Stock Exchange in 2021, no new companies in the assisted reproductive technology (ART) sector have gone public in the nearly two years that followed. The most recent news came this February, when an ART biologics manufacturerJingze BiotechInitiated A-share listing tutoring, but there has been no new progress to date.

Assisted Reproductive Technology Makes Major Strides into National Health Insurance: Can It “Save” the Field?

On October 27, the Healthcare Security Administration of Guangxi Zhuang Autonomous Region issued a notice,Starting November 1, Guangxi will include certain therapeutic assisted reproductive technology services, such as oocyte retrieval, in the coverage of basic medical insurance and work-related injury insurance funds.. Following the news, multiple stocks in the assisted reproductive technology sector rose against the market trend. By the midday close, A-share listed Caina Shares and Sinobiologics had gained more than 8%, while Hong Kong-listed JINXIN FERTILITY was up over 6%.

However, this is not the “first time” this year. As early as June of this year,BeijingThe Beijing Healthcare Security Administration took the lead in issuing a notice to include 16 therapeutic assisted reproductive technology services—such as ovulation induction monitoring, oocyte retrieval, artificial insemination, and embryo transfer—in Beijing’s basic medical insurance scheme, covering them under Category A for outpatient reimbursement. Around the same time,Liaoning ProvinceIt was also announced that 18 assisted reproductive technology services, including embryo culture and embryo transfer, would be included in the maternity insurance coverage list.

In fact, many more followed closely behind. On November 1,Henan ProvinceThe Healthcare Security Administration stated that it strives to include certain therapeutic assisted reproductive technology services, which are “clinically necessary, technically mature, safe and effective, and cost-appropriate,” within the provincial medical insurance coverage by the end of this year. In addition, includingZhejiang, Hunan, Jiangxi, Sichuan, HubeiOther regions have also announced plans to include assisted reproductive technology in medical insurance coverage.

However, this must be examined from two perspectives.

Let’s start with the positive aspects. In the future, more regions will undoubtedly include assisted reproductive technology (ART) in their medical insurance coverage, which will certainly alleviate the financial burden on some individuals seeking ART services. For instance, regarding the recent inclusion of ART in Guangxi’s medical insurance scheme, Li Rong, Director of the Reproductive Medicine Center at Nanning No. 2 People’s Hospital, stated, “With ART covered by medical insurance, oocyte retrieval, embryo culture, and embryo transplantation—these three procedures alone are reimbursable at 70%, amounting to 6,230 yuan, leaving patients to pay only 2,670 yuan out-of-pocket. Additionally, women facing infertility who undergo first- or second-generation in vitro fertilization (IVF) treatments, depending on the specific insurance plan,”Reimbursement amounts range from over RMB 4,000 to more than RMB 10,000.。”

This is also beneficial for corporate players. At JINXIN FERTILITY’s recent earnings conference, Chairman Zhong Yong stated, “The company remains optimistic about the prospects of including assisted reproductive technologies in the national medical insurance scheme and is making relevant preparations.”The Inclusion of Assisted Reproductive Technology in Medical Insurance May Not Lead to a Rapid Surge in Treatment Volume in the Short Term, but Will Promote the Popularization of Related Concepts。”

Therefore, for an emerging industry such as assisted reproductive technology (ART), broad inclusion in medical insurance coverage will inevitably and effectively enhance market penetration. However, this is not entirely the case,There are still some contradictions in the inclusion of assisted reproductive technology in medical insurance.。

For instance, regarding payment intensity, it is widely believed within the industry thatMedical insurance, positioned to “cover basic needs,” currently provides limited support for the reimbursement of assisted reproductive technologies.. In this regard, a head of an assisted reproductive technology (ART) device company told VCBeat, “The characteristic of ART projects is that the single-session fee is relatively high, and success is not guaranteed even after multiple attempts. If the number of people receiving ART-related medical services increases, it will place significant pressure on the medical insurance fund. Furthermore, based on international practical experience,”In vitro fertilization (IVF) involves numerous procedures and technologies. The implementation of relevant policies requires the formulation of supporting detailed rules to clarify reimbursement coverage and impose restrictions on patient age and treatment cycles; an open-door policy is not feasible.。”

It is precisely for this reason that the contradictions within the current assisted reproductive technology (ART) industry have become irreconcilable, namely:In regions with strained basic medical insurance funds, fertility intentions are high, yet assisted reproductive technology (ART) is not covered by insurance; conversely, in areas where basic medical insurance funds are relatively ample, fertility intentions are lower, but ART is included in the insurance coverage.。

Additionally,Inclusion of Assisted Reproductive Technology in Medical Insurance Actually Only Addresses Issues in the Pre-Conception Phase, followed by child-rearing after birth and education as children grow up, all of which directly impact initial fertility intentions. This is why assisted reproduction is considered the only niche sector that policy measures alone cannot directly stimulate; it is not merely a medical issue but a societal one that integrates technology, ethics, morality, law, and other factors, with a level of complexity far exceeding that of medical research itself.

Nevertheless, the latent future value of the assisted reproductive technology (ART) sector should not be overlooked. The rapidly rising infertility rate is an objective reality, and given China’s vast population base, market demand for ART remains substantial. Furthermore, driven by both enterprises and capital, core technologies and services related to ART in China are undergoing rapid iteration, positioning the sector to accommodate a significantly larger customer base in the future.

And how to break through boils down to two key words,One is “improving success rates,” and the other is “enhancing cost-effectiveness.”。

1. “It’s Hard to Enter the Market, and Even Harder to Make Money: The Hurdles for Private Assisted Reproductive Technology Institutions Go Beyond Licensing” — National Business Daily;

2. “Assisted Reproductive Technology Finally Covered by Medical Insurance, Yet Fails to Reverse Declining Birth Rates; Maternity Hospitals Are Laying Off Medical Staff” — Ba Dian Jian Wen;

3. “Capital Bets Heavily: Why Is Assisted Reproductive Technology So Hot?” — Yike Business