2023 Surgical Robotics Industry Report: Over 100 Funding Rounds in Four Years, Advancing Toward Automation and Full-Procedure Coverage

Robots are hailed as the crown jewel of the manufacturing industry. In recent years, technological research and product development in medical robotics have continued to advance, with surgical robots becoming the largest and most important segment within the medical robotics category.

Surgery primarily originates from the field of general surgery. From the perspective of technological evolution, the transition from manual to automated and then to intelligent systems represents a major trend. Over the past two decades, surgery has undergone a transformation from open procedures to minimally invasive techniques. Approximately ten years ago, it began advancing toward digitalization and intelligence, whileThe primary vehicle for digital and intelligent surgery is the surgical robot; just as assisted driving has gained widespread public acceptance, surgical robots will become an indispensable aid to surgeons.

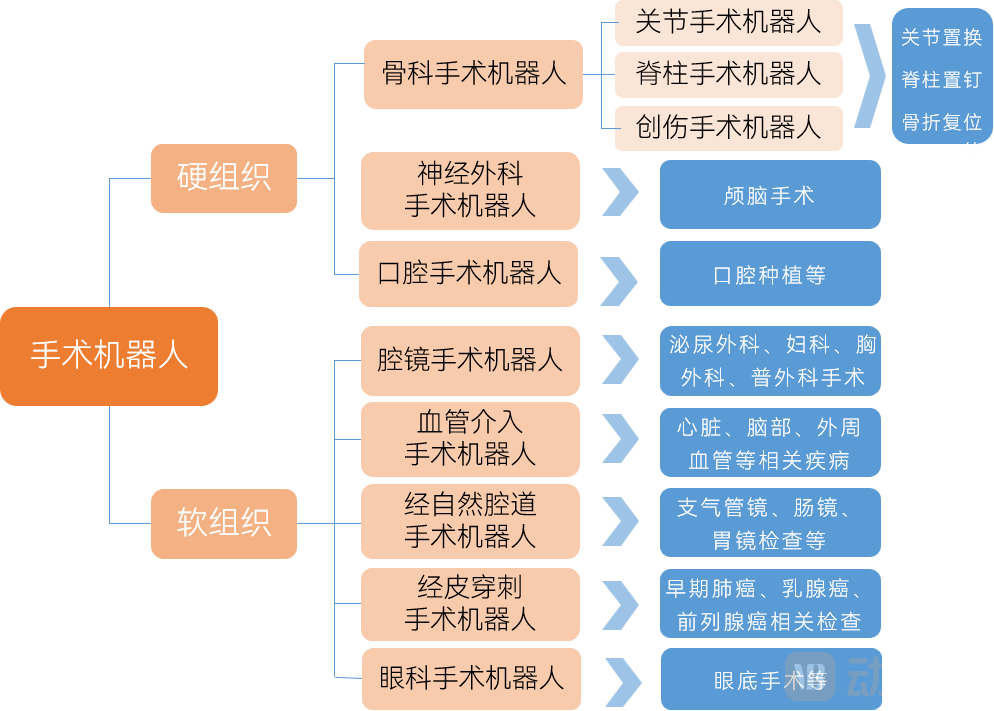

Figure Classification of Surgical Robots

Image source: VCBeat

Surgical robots are a new type of medical device that integrates clinical medicine, biomechanics, mechanics, computer science, microelectronics, and other disciplines. With clear imaging systems and flexible robotic arms, they assist physicians in performing complex surgical procedures through minimally invasive techniques, enabling intraoperative tasks such as positioning, cutting, puncture, hemostasis, and suturing. Based on the type of target organ, surgical robots can be further classified into hard-tissue robots and soft-tissue robots.

Surgical robots have been applied in multiple fields, including general surgery, urology, cardiovascular surgery, thoracic surgery, gynecology, orthopedics, and neurosurgery, marking a milestone in the development of clinical medicine. Against the backdrop of insufficient medical resources today, surgical robots are held in high expectation. The da Vinci Surgical System has remained in the spotlight, validating its immense market potential. Meanwhile, driven by policy support and capital investment, the surgical robot industry is experiencing rapid development and stands out prominently in the global capital market.

VCBeat Releases Surgical Robotics Industry Report, Aiming to Present a Relatively Comprehensive Overview of the Current Industry Landscape and Commercial Map Through Our Research Interviews with 12 Companies and Nearly 20 Experts in the Field.

Based on our research compilation, we have conducted an analysis of the surgical robotics industry and arrived at the following conclusions:

1. The surgical robotics sector is heating up, with over 100 financing rounds completed in China over the past four years. This surge is driven by: substantial and unmet clinical needs, the strong market performance of the da Vinci Surgical System, and the “gap” in surgical robotics products among major Chinese medical device companies;

2. The product strength of surgical robots is mainly reflected in three aspects: irreplaceability, powerful assistance, and scalability. In terms of product promotion, the da Vinci Surgical Robot started with irreplaceability, addressing high-difficulty surgeries that are challenging for general surgeons. At present, the conditions for promoting its powerful assistance capabilities may already be in place;

3. Mergers and acquisitions by foreign giants have mostly occurred in the orthopedics sector, achieving bundled sales of surgical robots and consumables; however, China’s centralized procurement of medical consumables has weakened this model. In laparoscopy, single-port systems have gained regulatory approval in China, accelerating the substitution of imported products with domestically produced alternatives.

4. Surgical robots for percutaneous procedures, neurosurgery, oral and maxillofacial surgery, and ophthalmology have basically achieved synchronous development with foreign products; those for natural orifice procedures are in a stage of rapid follow-up; and vascular interventional robots are, to some extent, leading their foreign counterparts.

5. At present, most surgical robots lack automation, with only some achieving Level 1 and Level 2 automation. In the future, surgical robots will evolve in terms of their “eyes,” “hands,” “brains,” and “bodies,” advancing toward greater automation and intelligence.

6. In terms of functional evolution, surgical robots will cover core operations throughout the entire process, from preoperative to intraoperative stages. Additionally, this phase will see an expansion in applications, encompassing a broader range of surgical procedures, such as products for orthopedics and pan-vascular interventions.

7. From a product perspective, the domestic market places greater emphasis on the cost-effectiveness of surgical robots, while still adhering to the potential business models observed internationally; the “surgical robot + consumables” model represents a sustainable ecosystem.

8、Amid Tighter IPO Regulations, the Surgical Robotics Industry, Characterized by Lengthy R&D Cycles, May Face Significant Impact; Self-Sustaining Revenue Generation Capability Is Key

Policy and Capital Join Forces: Over 100 Financing Rounds in Four Years

Policy: Accelerated Approval, Expanded Capacity, and Health Insurance Support

The National “Green Channel” for the Approval of Innovative Medical Devices Has Given Surgical Robots a “Green Light.” In terms of approval, as innovative medical devices, several domestically produced surgical robots have passed special review applications and entered the “Green Channel,” shortening the original market launch application process by approximately six months.

Further expansion in the allocation of laparoscopic surgical robots. According to the “14th Five-Year Plan for the Allocation of Large-Scale Medical Equipment,” 559 additional endoscopic laparoscopic surgical systems are to be allocated (increasing from a previous stock of 260 units, a 215% rise), with the price ceiling adjusted upward from RMB 10–30 million to RMB 30–50 million.

Policy “tailwinds” continue to favor surgical robots, with medical insurance policies also providing support. In the area of medical insurance, Shanghai included radical prostatectomy, partial nephrectomy, total hysterectomy, and radical resection for rectal cancer performed using the “da Vinci Surgical System” in its medical insurance reimbursement coverage in April 2021.

In August 2021, Beijing established government-set pricing for “robot-assisted orthopedic surgery” (Class A medical insurance) as an auxiliary procedure, and included it along with “disposable robot-specific instruments” in the Beijing Medical Insurance Reimbursement Catalog.

Additionally, multiple provinces and municipalities, including Hunan, Guangdong, and Jiangxi, have successively followed suit, incorporating surgical robots and related consumables into medical insurance coverage. This year, Shanghai has further included 76 newly added medical service items and new medical device (consumable) entries, such as the “da Vinci” system, in its medical insurance scheme.

According to incomplete statistics, since 2015, the national government has issued a total of 18 policies related to surgical robots and associated areas, providing strong encouragement and support in aspects such as approval, allocation, medical insurance coverage, technology, and clinical application. These are as follows:

Figure: National Policies on Surgical Robots in Recent Years

Image source: VCBeat

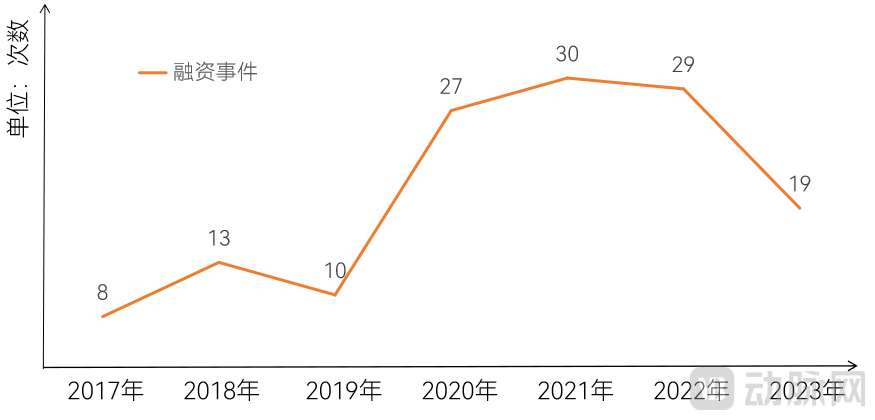

Financing: Over 100 financing rounds in four years

Over the past five years, the surgical robotics industry has entered a period of explosive growth, marked by the emergence of numerous startups. Companies such as MicroPort MedBot and Tinavi Medical Technologies have gone public, while several other well-known firms have advanced to the commercialization and IPO filing stages. On the other hand, the recent cooling of the capital market has also impacted surgical robotics companies, with their commercialization strategies facing increased scrutiny.

Nevertheless, even against this backdrop, surgical robots have continued to “outperform their peers” in the capital markets. According to incomplete statistics, the surgical robotics sector recorded 27, 30, 29, and 19 financing events in 2020, 2021, 2022, and 2023 (as of September 30; multiple financing rounds by the same company were counted as a single event), respectively. With over 100 financing events across these four years, the sector’s overall performance has been remarkable, as shown in the figure below.

Figure: Number of Financing Deals in the Surgical Robotics Sector in Recent Years

Image source: VCBeat

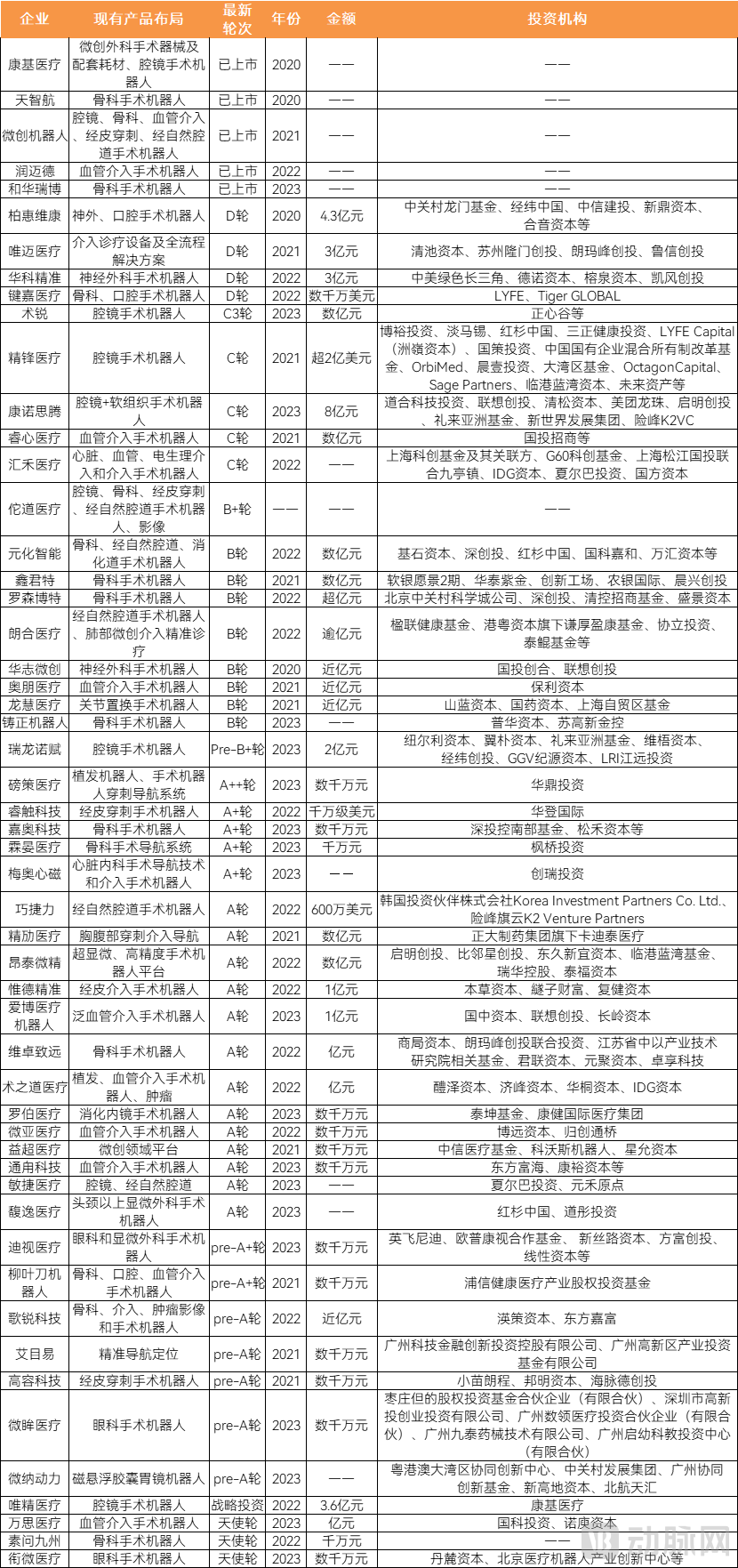

Meanwhile, looking solely at the amounts from the latest funding rounds in 2023, as of October 15, 2023, there had already been five financing deals exceeding RMB 100 million. In terms of the number of financing deals, 2023 saw a decline, indicating that capital has become more rational. Furthermore, based on the latest funding rounds, Series A and earlier-stage investments accounted for 33.3%, suggesting that the market remains vibrant. Specifically, the financing situation in recent years is as follows:

Figure: Statistics on Financing of Surgical Robotics Companies Since 2020

Data Source: Public information including company websites

The Surge in Popularity of Surgical Robots: Three Key Drivers

1. The substantial and unmet clinical demand for surgical robots is clear;

2. The Da Vinci system’s outstanding market performance has led to high expectations for surgical robots;

III. The “gap” in surgical robots among China’s medical device giants has made it a “promising market.”

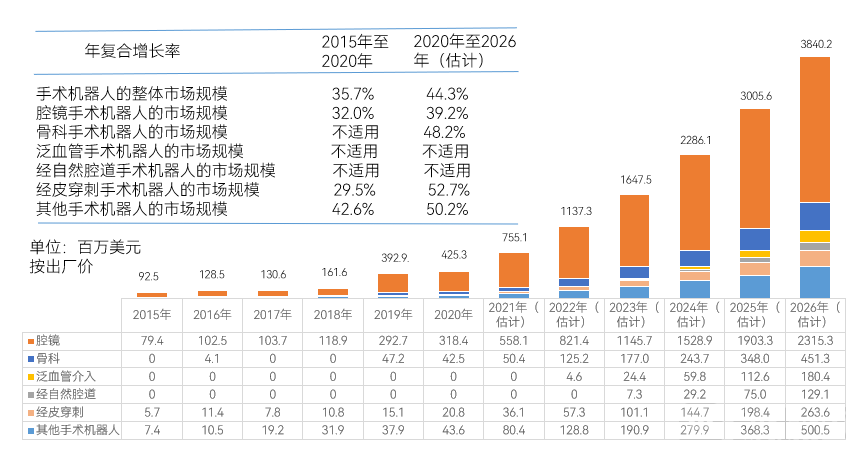

Market: The domestic compound annual growth rate exceeds the global average of 18.1%, indicating immense potential.

According to Frost & Sullivan, the market size of surgical robots in China reached US$430 million in 2020, with a compound annual growth rate (CAGR) of 35.7%. It is estimated to reach US$3.84 billion by 2026. The global CAGR from 2020 to 2026 is projected at 26.2%, while China’s CAGR is expected to be 44.3%, exceeding the global average by 18.1 percentage points, indicating substantial potential in the domestic market. Specifically, the market size for laparoscopic surgical robots is projected to reach US$2.32 billion by 2026, and that for orthopedic surgical robots is expected to reach US$450 million. Details are as follows:

Figure: Market Size of Surgical Robots in China

Data Source: Frost & Sullivan

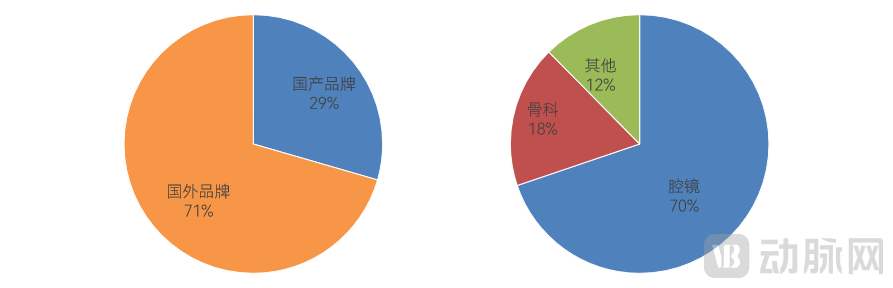

According to the China Bidding and Tendering Network, based on the published bid award data for the first half of 2023 (January 1 to June 30), excluding consumables and services, domestic brands accounted for 29.5% of the market share, while imported brands accounted for 70.5%. Specifically, laparoscopic surgical robots accounted for approximately 70%, and orthopedic surgical robots accounted for approximately 18%, as detailed below:

Figure: Analysis of Surgical Robot Bid-Winning Results in H1 2023

Data Source: China Bidding Network

Technology: Real-Time Intraoperative Navigation is the Key Focus, with Major Companies Vying for Breakthroughs

“Soft” and “Hard” Integration: Distinct Operational and Positioning Characteristics

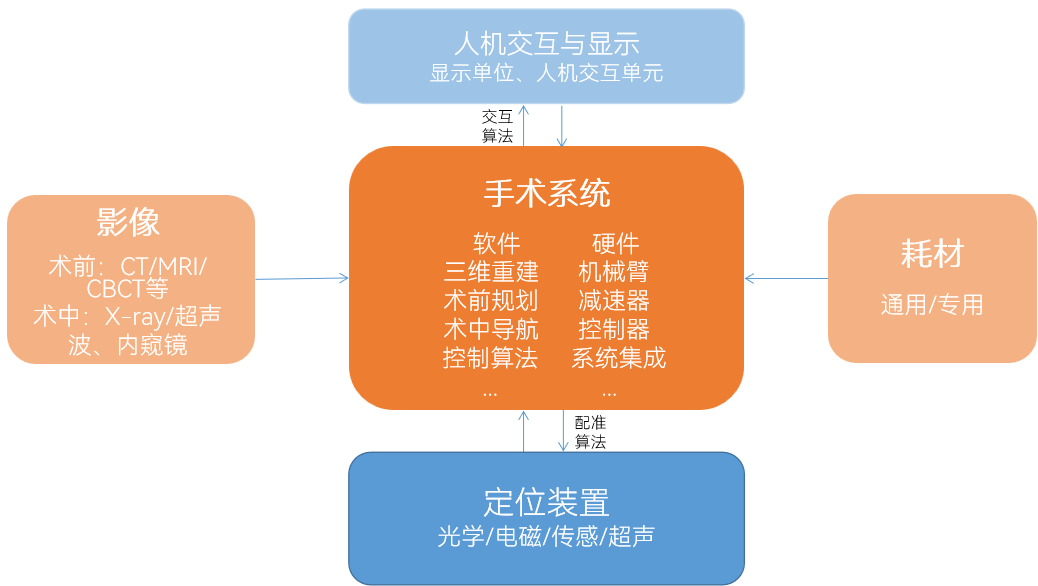

Surgical robots are characterized by multidisciplinary integration and high technical barriers. Overall, the functional modules of surgical robots are distributed as follows:

Figure: Distribution of Functional Modules in Surgical Robots

Image source: VCBeat

Operational capabilities and positioning accuracy represent distinct technical focal points. Currently, surgical robots emphasizing positioning are predominantly found in orthopedics, percutaneous puncture, neurosurgery, and oral surgery; whereas those prioritizing operational dexterity are mainly seen in laparoscopic, vascular interventional, and natural orifice transluminal endoscopic surgery (NOTES) robots. In light of the latest product developments, certain orthopedic and neurosurgical robotic systems also incorporate enhanced operational functionalities.

For example, Geerui Technology’s “Newton” orthopedic surgical robot integrates the master-slave design of endoscopic surgical robots into its system. It adopts a multi-robotic-arm plus modular surgical instrument architecture and incorporates force feedback technology, enabling physicians to safely and efficiently perform all core procedures in minimally invasive orthopedic surgery.

Laparoscopic Surgical Robots: Variations in Robotic Arm Design, with Force Feedback as the Future Breakthrough Point

Currently, the domestic market for laparoscopic surgical robots is characterized by a landscape of “one dominant player and several strong competitors.” In the field of laparoscopic surgical robots, the da Vinci system maintains a near-monopoly position globally. In recent years, with substantial investments by Chinese enterprises, domestically produced laparoscopic robots have explored innovations in technology and product forms, achieving diversification.

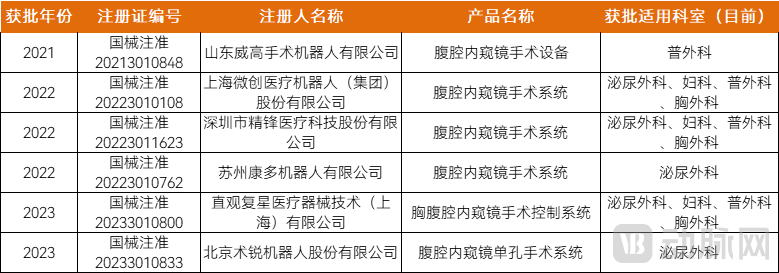

Currently, there are six laparoscopic surgical robots approved by the National Medical Products Administration (NMPA) for use within China, with the total number of approvals achieving year-on-year growth.

Specifically, with the exception of Shurui’s single-port system, all others are multi-port systems. Due to export controls imposed on da Vinci’s single-port robot, the approval of domestically produced single-port surgical robots represents a major breakthrough in the development of laparoscopic robots in China. Furthermore, Jingfeng and MicroPort have expanded their applicable clinical departments, securing approvals for use in four specialties in August and September 2023, respectively. The specific approval details are shown in the figure below.

Figure: Overview of Laparoscopic Surgical Robots Approved in China

Data Source: NMPA

Orthopedic Surgical Robots: Improving Bone Handling Precision and Achieving Accurate Implant Placement

Robotic joint replacement systems enhance the precision of bone preparation. These robotic systems are primarily used to assist surgeons in performing procedures such as total hip arthroplasty, total knee arthroplasty, and unicompartmental knee arthroplasty.

Compared with conventional surgery, robot-assisted joint replacement surgery can achieve more precise grinding, cutting, and drilling operations, improve the accuracy of bone processing, make the position of the implanted prosthesis closer to the preoperative plan, and also has certain advantages in postoperative functional improvement and patient satisfaction.

For instance, Keya Medical’s ARTHROBOT joint replacement surgical robot leverages advanced navigation and positioning along with 3D visualization technology to precisely monitor bone resection progress and assess patient soft-tissue balance, delivering high accuracy. The system is equipped with a seven-degree-of-freedom robotic arm that utilizes robotic arm control technology to assist surgeons in controlling the angle and depth of bone resection as well as the accuracy of prosthetic implantation.

The main advantages of spinal surgical robots are:

① Precise implantation of surgical implants;

② Reduced radiation exposure;

③ Shortened operative time;

④ Reduced the surgical incision.

In fracture reduction surgery, the robot operates on unstable bone fragments whose spatial positions vary during the reduction process, necessitating multiple adjustments to achieve proper alignment. Therefore, well-designed human-robot interaction is critical for fracture reduction robots.

Based on domestically approved products, as of October 15, 2023, a total of 20 orthopedic surgical robots with navigation and positioning capabilities have received approval. Among these, the largest number are indicated for joint replacement, followed by those for spinal applications, as detailed below:

Figure: Overview of Orthopedic Surgical Robots Approved in China

Data Source: NMPA

Upgrades in Both Operation and Positioning from Preoperative to Intraoperative Phases

In the field of vascular interventional surgical robots, historically, only Siemens’ CorPath 200 and CorPath GRX have obtained both FDA clearance and CE marking globally; Robotcath’s R-One (a collaborative project with MicroPort MedBot) has received CE marking; and Johnson & Johnson’s Sensei X2 and Stereotaxis’ Genesis RMN have obtained FDA approval.

Unlike most procedures primarily used for coronary interventions, Vans Medical’s VAS HERO vascular interventional surgical robot is designed for neurointerventions and received approval from the National Medical Products Administration (NMPA) in March 2023, becoming the first such device approved in China.

The VAS HERO surgical system meets the requirements for total cerebral angiography applications. It enables real-time recording of contrast agent dosage, detection of hemorrhage and air bubbles, and timely alerts. With sub-millimeter precision and a minimum rotational angle of less than 1 degree, its minimalist design and modular installation make procedures safer, more precise, and more efficient.

Compared with traditional biopsy procedures that rely on radiologists to manually insert needles, percutaneous puncture surgical robots offer higher stiffness and precision through robotic arms that are more stable than the human hand.

Percutaneous interventional surgical robots first perform rapid and accurate 3D reconstruction based on the patient’s medical imaging to obtain the three-dimensional structure of the affected area and conduct “path planning” to identify the “optimal needle insertion point,” avoiding hazardous structures such as surrounding blood vessels and nerves. This process, known as preoperative planning, is analogous to “navigation before driving.”

High-precision “navigation” is based on the patient’s target location and affected anatomical structures to accurately plan the puncture trajectory and angle, enabling physicians to avoid or minimize deviations. This allows even novice operators to perform procedures with confidence, assisting clinicians in conducting percutaneous interventional surgeries that are more precise, safer, and more efficient.

Natural Orifice Surgical Robots Offer Higher Accuracy and Diagnostic Rates. Natural orifice surgical robots typically consist of one camera and two robotic arms, with end-effectors generally being forceps and electrocautery knives. The diameter of the operating arms, the dexterity of the end-effectors, and the gripping force of the forceps are key technical considerations in the design of natural orifice surgical robots.

From a technical perspective, robotic bronchoscopy systems are still in their early stages of development; however, their safety and efficacy have been well established. Compared with electromagnetic navigation-guided bronchoscopy and conventional bronchoscopy, they demonstrate higher accuracy and diagnostic yield, along with a relatively lower incidence of complications.

Perception and localization are key technologies for neurosurgical robots. Here, perception and localization encompass lesion-specific, local, and global levels. Lesion perception and localization are achieved through multimodal 3D visualization image processing techniques, including CT, MRI, PET, and Diffusion Tensor Imaging (DTI), which are primarily used for preoperative planning.

Currently, the dominant model in China combines collaborative robotic arms with infrared optical navigation systems. To fully unlock the potential of surgical robots in neurosurgical system integration, greater investment is needed in imaging software, planning software, and end-effectors.

Three neurosurgical surgical robot companies have received domestic approval in China: Huake Precision, Baihui Weikang, and Wuhan United Imaging Intelligence Medical Technology Co., Ltd.

Oral surgical robots can make surgery more precise. Compared with dentists implanting teeth, the biggest advantage of dental implant robots is precision. It is understood that the shoulder error of robot implantation is 0.285 mm, the root error is 0.311 mm, and the angular deviation error is 1.807 degrees. This data shows that the accuracy of robot implantation is much higher than the statistical data of doctors using guide plates for implantation.

In conventional dental implant surgery, the surgeon must incise the patient’s gingiva, place the implant, and then suture the site. The surgeon’s perception of force relies solely on tactile feedback, making clinical experience and technical proficiency critically important.

Ophthalmic surgical robots enable high precision, reduced surgical trauma, and more accurate treatment. The specific advantages of ophthalmic surgical robots are as follows:

1. It can filter out the physiological tremors of surgeons, enhancing the stability and control of surgical maneuvers, thereby reducing the difficulty of surgical procedures and the stress on surgeons, and minimizing complications in ophthalmic surgery; 2. It improves surgical precision, making personalized and precise treatment, as well as new surgical techniques, possible;

3. Shorten the learning curve for novice ophthalmic surgeons and extend the prime surgical career of senior surgeons.

Currently, there are five major technical schools of ophthalmic surgical robots, each with its own characteristics. Overall, parallelogram and serial-parallel hybrid technologies demonstrate the strongest practicality, while magnetic navigation technology remains relatively distant from clinical implementation.

Among these, Weimou Medical’s serial-parallel structure enables micron-level high-precision RCM control and end-effector positioning. The surgical robot features five degrees of freedom, allowing for flexible RCM with high accuracy and enhanced safety. The company’s master-slave design is compatible with a highly user-friendly operating system, while its structured design aligns with surgeons’ natural operational patterns.

As of October 15, 2023, a total of 24 surgical robot products (including navigation systems) other than laparoscopic and orthopedic surgical robots have been approved in China. Among them, oral surgical robots are the most numerous, with 8 approvals, mostly used for dental implantation; there are 7 puncture surgical robots; 6 neurosurgical surgical robots; and 1 vascular interventional surgical robot. The details are as follows:

Figure: Overview of Approved Surgical Robots Other Than Laparoscopic and Orthopedic Systems

Image source: VCBeat

Haptic Feedback, Precise Positioning, and Intraoperative Registration Are the Directions for Iteration

Haptic Feedback Systems Are a Key Technology in Surgical Robot Operation. At present, most laparoscopic surgical robots employ visual feedback systems; when controlling robotic arms during surgery, surgeons must analyze visual information to make real-time judgments about the forces exerted by instruments on tissues and other tissue characteristics, which affects surgical efficiency to some extent.

High-fidelity physical models of tissues and organs, as well as haptic feedback physical models based on the anatomical characteristics of human tissues, should be established here. By integrating force feedback with tactile feedback, the realism of surgical procedures can be enhanced.

Imaging, tracking, and display are key technologies in the positioning and navigation of surgical robots. In terms of imaging equipment, optical positioning systems employ a binocular vision system composed of two near-infrared cameras. Infrared LEDs are mounted around the optical axes of the two cameras to provide illumination. The infrared light emitted by these LEDs is reflected off marker spheres attached to surgical instruments back into the cameras’ photosensitive chips. These marker spheres feature a special reflective coating consisting of tens of thousands of microbeads, enabling them to reflect infrared light during the tracking process.

Images of marker spheres are captured by cameras, and marker points are identified and localized through digital image processing techniques with computer assistance. Based on the three-dimensional coordinates of the marker points, the position and orientation of surgical instruments can be calibrated, thereby enabling precise surgical navigation.

For instance, AimPosition, a near-infrared optical tracking system independently developed by AimEye Technology, is built on an FPGA technology platform. It enhances the high synchronization and stability of binocular visual image acquisition, enabling real-time dynamic tracking of tool positions within specific three-dimensional spaces with a tracking accuracy of up to 0.12 millimeters. Related products have currently achieved mass production and are widely applied.

Registration is a critical component of the entire surgical navigation system. From a technical perspective, the registration of preoperative and intraoperative data is a key technology in image-guided surgery. It aligns preoperative data (such as preoperative patient imaging, anatomical models derived from these images, and surgical plans) and intraoperative data (including patient images, positions of surgical instruments, and tracking systems) into a common coordinate system. Compared to hard-tissue surgeries, which are akin to "shooting at a fixed target," soft tissues undergo significant intraoperative displacement and deformation, thereby imposing higher requirements on intraoperative registration.

For instance, Weide Precision’s percutaneous interventional robot effectively addresses key challenges such as lesion drift caused by intraoperative deformation and displacement, as well as real-time, multi-dimensional registration of multimodal data during surgery, leveraging its respiratory phase technology. Furthermore, it enables fully automated, real-time processing of intraoperative data based on artificial intelligence.

Commercialization: Challenges and Opportunities, Domestic Products Are Better Suited to Their “Soil”

Start with Irreplaceability, Expand with Strong Supportive Capabilities

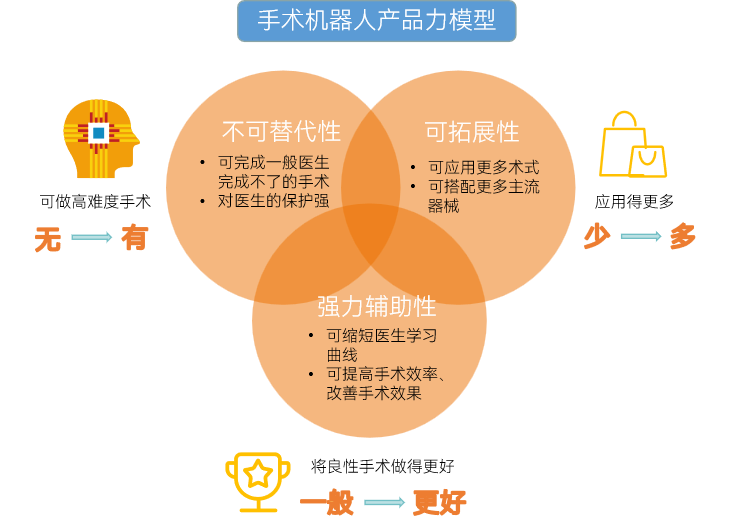

In terms of application, product strength—defined as the surgical robot’s ability to deliver its core value—is fundamental. We believe that the product strength of surgical robots primarily comprises three aspects: irreplaceability, robust assistance, and scalability.

Figure: Product Competitiveness Model of Surgical Robots

Image source: VCBeat

In terms of product promotion, the da Vinci Surgical Robot entered the Chinese market by emphasizing its “irreplaceability.” Taking this as an example, prostate surgery requires three-dimensional high-definition visualization and precise surgical instruments, which are beyond the capabilities of ordinary surgeons. The surgical robot serves as a powerful tool to address this gap, effectively solving the problem of “going from nothing to something.” After being introduced into hospitals, the da Vinci Surgical Robot initially found its breakthrough in urology and gradually expanded into gynecology, hepatobiliary surgery, thoracic surgery, and other specialties.

At this stage, the conditions are ripe for surgical robots to enter the market by emphasizing their “powerful assistive” capabilities. Currently, the da Vinci Surgical System’s functions are roughly split evenly between “irreplaceability” and “powerful assistance.” Going forward, promoting surgical robots to hospitals from the perspective of “powerful assistance” is likely to be equally acceptable.

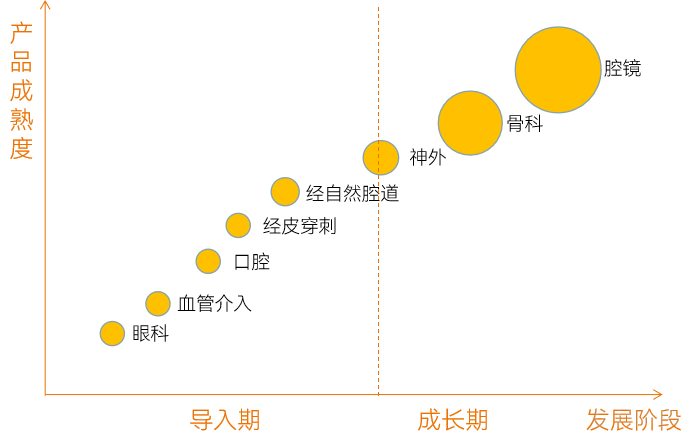

Eight Major Tracks Show Uneven Progress; Four Types of Enterprises Each Have Their Unique Characteristics

Currently, apart from the da Vinci laparoscopic surgical robot, most surgical robots are still in the stage of “specialization.” The figure below illustrates the maturity and development stages of surgical robot products worldwide, with the size of the circles representing the current market size.

Figure: Maturity and Development Stages of Surgical Robotic Products by Category

Image source: VCBeat

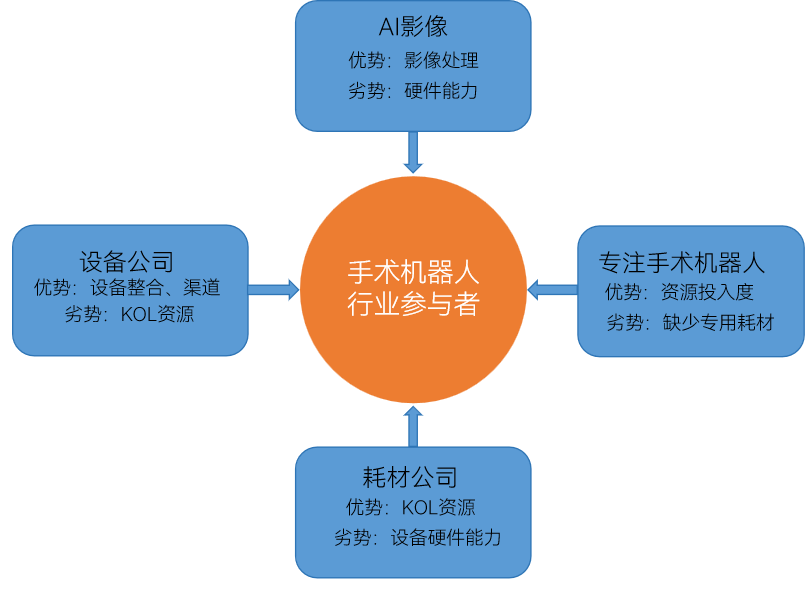

From the corporate perspective, there are currently four main types of companies deploying in the surgical robotics sector, as detailed below:

Figure: Four Types of Companies Deploying Surgical Robots

Image source: VCBeat

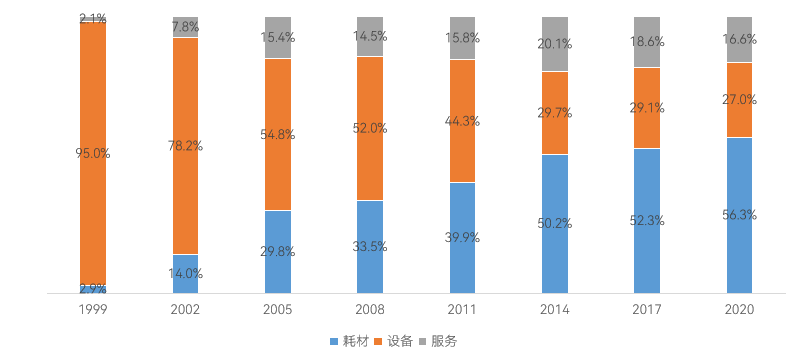

From a business model perspective, the surgical robot market is primarily divided into three segments: equipment, service fees, and consumables. Taking the da Vinci Surgical System as an example, equipment drives short-term revenue, while consumables and services account for long-term growth.

Chart: Revenue Composition of Intuitive Surgical

Data Source: Intuitive Surgical Official Website

Challenge: Policy-Driven Price Controls and Competition with Foreign Brands

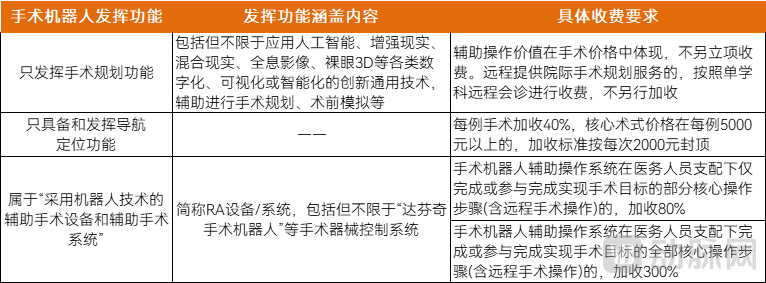

In September 2022, the Hunan Provincial Healthcare Security Administration issued the “Notice on Regulating the Use and Charging Practices of Surgical Robot-Assisted Operating Systems.” Subsequently, other provinces and cities have followed suit, leading to the gradual standardization of fees for surgical robots. The specific details are as follows:

Figure: Billing Requirements for Surgical Robots

Image source: Hunan Provincial Healthcare Security Administration

The policy aims to guide surgical robots back to their clinical value and toward higher-value innovation. Essentially, the policy seeks to encourage companies that prioritize clinical value, as market demand encompasses the entire procedural workflow—particularly core operative steps. Isolated minor or non-core segments fail to meet physicians’ needs; the ultimate clinical value of surgical robots lies in having the robot perform all core actions throughout the entire procedure.

This will have significant implications for the standardization of surgical procedures and the equitable distribution of medical resources. This policy also serves to optimize social resources and, in the long term, will drive high-quality development within the industry.

Global Giants Enter the Fray as the Market Poises for Takeoff. In a bid to capture market share, U.S. medical technology leaders such as Medtronic, Johnson & Johnson, Stryker, and Zimmer Biomet have all entered the arena, pursuing strategies ranging from direct acquisitions and independent R&D to joint development with upstream technology companies. The overseas surgical robotics market is poised for significant growth.

Meanwhile, orthopedics has been the most frequently targeted sector in overseas acquisitions, with most deals involving large medical consumables companies acquiring orthopedic surgical robot manufacturers. On one hand, these major consumables companies aim to establish a closed-loop ecosystem similar to that of the da Vinci Surgical System. From a long-term perspective, they acquire robotic companies at premium valuations and bundle them with their proprietary consumables. On the other hand, orthopedic surgical robot companies often lack dedicated consumables and struggle to build their own ecosystems. This creates a mutually beneficial arrangement.

In China, laparoscopic surgical robots continue to see products “break through the siege,” whereas the “centralized procurement environment” may not be equally suitable for orthopedics. Although the da Vinci Surgical System holds a clear advantage, single-port laparoscopic surgical robots developed in China have still gained regulatory approval. In orthopedics, while foreign products enjoy certain advantages in algorithms and clinical maturity, they were subjected to centralized volume-based procurement before establishing dedicated consumables business models.

Whether it is Stryker or Medtronic, foreign brands ultimately aim to generate profits from consumables. Under the backdrop of centralized procurement, their profit margins have been eroded, and their bundled business models have not performed as well as anticipated. In this context, Chinese companies may find opportunities to grow in such an environment.

Reducing costs and enhancing product performance is an inevitable path. In China, it is necessary to precisely control the costs of products and consumables, while also creating strong product value to meet clinical needs. How can costs be reduced? For instance, from a design perspective, adopting modular design, simplifying structures, and making technical trade-offs without compromising functionality;

On the other hand, consumables remain a key component of sustainable business models, with companies reducing their reliance on consumable revenue by trading volume for lower prices. Nevertheless, as surgical procedures become more widespread, there remains significant market potential.

Trend: Covering Core Operations and Expanding Surgical Procedures

“Eye,” “Hand,” “Brain,” and “Body” All Evolve, Automation Upgraded Again

In the future, surgical robots will evolve and iterate in terms of their “eyes,” “hands,” “brains,” and “bodies.” Minimally invasive approaches will remain the core direction for product evolution, as exemplified by natural orifice surgical robots.

In the long run, miniaturization represents another key trend in the development of surgical robots. This evolution begins with more compact and user-friendly designs, progressing to capsule robots and micro/nanorobots, thereby further promoting non-invasive surgery and achieving greater minimization of the device itself.

Figure: Product Development Trends of Surgical Robots

Image source: VCBeat

Meanwhile, although current surgical robots can achieve greater precision, they do not offer significant advantages in improving surgical efficiency or reducing overall operative time. This remains a challenge to be addressed in the future; if both accuracy and speed can be achieved, there will be substantial market potential.

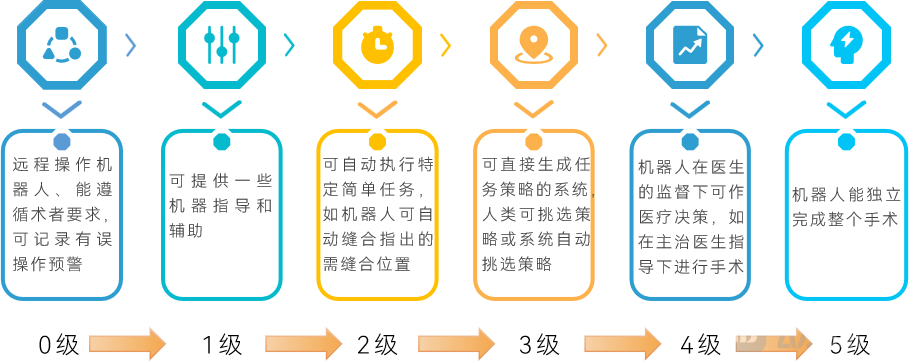

Furthermore, the progression of surgical robots toward automation and intelligence is inevitable. The field will advance to Level 2 and Level 3 automation, achieving technological integration by combining Level 0, Level 1, and partial Level 2 capabilities to collectively progress toward Level 3.

Figure: Automation Stages of Surgical Robots

Image source: VCBeat

Coverage of Core Procedures and Expansion of Surgical Techniques; Consumables Trending Toward Intelligence

From preoperative to intraoperative stages, covering core surgical procedures throughout the entire process. After the Hunan Provincial Healthcare Security Administration released its pricing policy for surgical robots in September 2022, Hainan, Shanxi, and Henan provinces followed suit. We anticipate that nationwide pricing standards will be established within approximately two years. Under these pricing policies, products that offer only partial functionality, particularly those not supporting core surgical procedures, will have very limited profitability in the future. The market demands surgical robots that cover core surgical procedures and assist throughout the entire surgical workflow.

During this phase, surgical robots will expand their clinical applications to cover a broader range of surgical procedures. To address challenges related to price controls and hospital procurement barriers, these systems will undergo functional expansion by integrating technologies with similar underlying principles. This will enable multi-purpose functionality and modular configurations, thereby enhancing hardware integration capabilities. Specifically, switching software modules will allow the same platform to be adapted for different anatomical regions, such as in comprehensive orthopedic and pan-vascular applications.

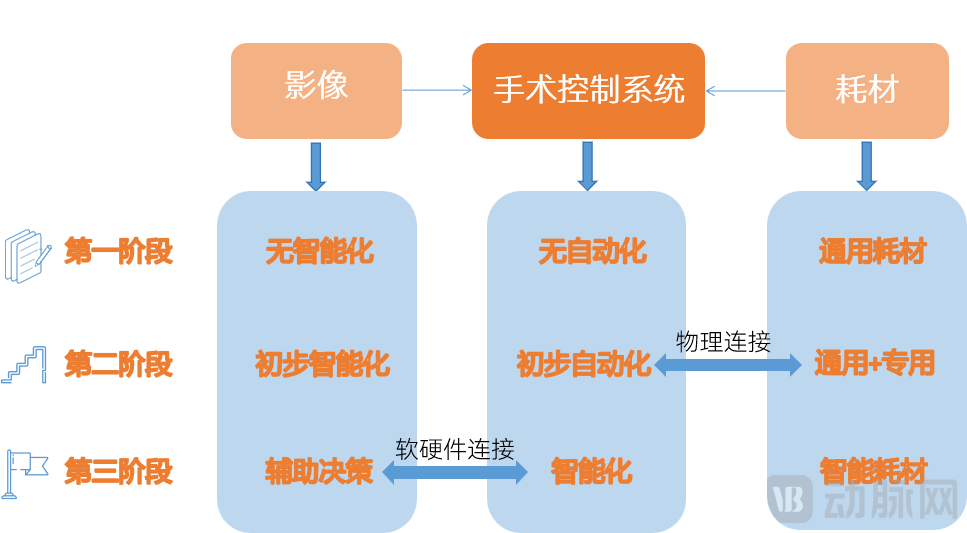

Furthermore, for vascular interventional surgical robots, the intelligentization of consumables is also a trend.

At the current stage, the focus is primarily on replicating manual procedures; imaging has not yet achieved intelligence, and only general-purpose consumables are used. In the second stage, image-guided localization will enable preliminary intelligence, with both general-purpose and specialized consumables available, while the connection between consumables and the surgical system remains physical. By the third stage, imaging will become more intelligent, allowing for software and hardware integration with the surgical system, along with the application of smart consumables such as sensors and chips. This progression, however, may take a considerable amount of time.

Figure: Development Trends of Vascular Interventional Surgical Robots

Image source: Aibo Medical Robotics

Amid Tighter IPO Regulations, Self-Sustaining Revenue Generation Is Key; Consumables Remain Indispensable in the Long Run

With the tightening of IPO regulations, improving profitability has become a key evaluation criterion. Due to the long R&D cycles and high technical barriers associated with surgical robots, there is a mismatch between profitability expectations and listing expectations in China. In late August 2023, the tightened IPO policies significantly impacted the surgical robot industry, making profitability a critical assessment factor as capital markets grew more rational.

Tighter IPO policies may restrict financing channels for R&D-focused companies in the surgical robotics industry. Additionally, the tightened IPO environment will prompt surgical robotics companies that have already obtained regulatory clearance to place greater emphasis on financial stability and commercial performance. For these companies, self-sustaining revenue generation capabilities will become increasingly critical.

In the long run, consumables are an indispensable component of the business model. From a product perspective, the Chinese market places greater emphasis on the cost-effectiveness of surgical robots, while still adhering to the potential business model prevalent in foreign markets: the “surgical robot + consumables” approach represents a sustainable ecosystem.

Globally, the five major players in the orthopedics sector have all engaged in acquisitions within the consumables segment. Furthermore, an analysis of the da Vinci Surgical System’s development reveals that consumables account for more than half of its market size. From the hospital perspective, generating revenue is also difficult without consumables. Therefore, in terms of business model, consumables represent a particularly critical component.

The above is an excerpt of the main content of the report. The complete framework of the report is as follows:

Chapter 1 Overview: Over 100 Financing Rounds in Four Years Driven by Policy and Capital

1.1 Policy: Significant Tailwinds, Accelerated Approvals, Expanded Coverage, and Enhanced Insurance Support

1.2 Financing: Outpacing the Competition with Over 100 Funding Rounds in Four Years

1.3 Market: China’s CAGR exceeds the global rate of 18.1%, indicating significant potential

Chapter 2 Technology: Intraoperative Real-Time Navigation as the Key Focus, with Major Companies Striving for Breakthroughs

2.1 Fundamentals: Integration of “Soft” and “Hard” Technologies with Distinct Operational and Positioning Characteristics

2.2 Endoscopes: Variations in Robotic Arm Design, with Force Feedback as the Key Future Breakthrough

2.3 Orthopedics: Improving Bone Handling Precision to Achieve Accurate Implant Positioning

2.4 Others: Upgrades in both operation and positioning from preoperative to intraoperative phases

2.5 Innovation: Haptic Feedback, Precise Positioning, and Intraoperative Registration Are the Directions for Iteration

Chapter 3 Commercialization: Challenges and Opportunities, Domestic Products Are Better Suited to Their “Soil”

3.1 Promotion: Positioning the product based on its irreplaceability and rolling out strong supportive measures

3.2 Landscape: Eight Tracks Show Uneven Progress, with Four Types of Enterprises Each Possessing Distinctive Characteristics

3.3 Challenges: Policy-Driven Price Controls and Competition with Foreign Brands

Chapter 4 Trends: Covering Core Operations and Expanding Surgical Procedures

4.1 Product: Evolution and Automation Across “Eyes,” “Hands,” “Brains,” and “Bodies”Upgrade

4.2 Evolution: Covering Core Procedures, Expanding Surgical Techniques, and Trending Toward Intelligent Consumables

4.3 Implementation: Under Tightened IPO Regulations, Cash-Flow Generation Capability Is Key; Consumables Remain Indispensable in the Long Run

Chapter 5 Corporate Case Studies

5.1 Aimuyi——Provider of Integrated Smart Surgical Solutions

5.2 Weide Precision – Focused on Intelligent Surgical Robots for Soft Tissue Intervention

5.3 Wans Medical—The First Vascular Interventional Surgical Robot Manufacturer in China Approved by the NMPA

5.4 Keya Medical – Providing High-Precision, Intelligent Surgical Solutions

5.5 Geerui Technology — Building a Full-Process Surgical Robot Platform

5.6 MicroEye Medical – A Leader in Intelligent Ophthalmic Surgery

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please proactively reach out:

Special Acknowledgments (in order of research interviews):

Ms. Yu Fang, Partner at Northern Light Venture Capital; Mr. Yin Xiankai, Partner at Kunyu Capital; Associate Professor Yang Rongqian, Founder of Aimuiyi Technology; Mr. Li Chuntian, Sales Director of Aimuiyi Technology; Dr. Ren Wenyong, Co-founder of Aibo Medical Robotics; Dr. Xie Weiguo, Founder of Veede Precision; Mr. Li Jin, COO of Wansi Medical; Mr. Li Haomin, CTO of Wansi Medical; Mr. Gao Shang, Founder of Gerui Technology; Jianjia Medical; and Professor Yan Pisong, Co-founder and CEO of Weiyou Medical